Lessons From Phase One of the Trade War With China

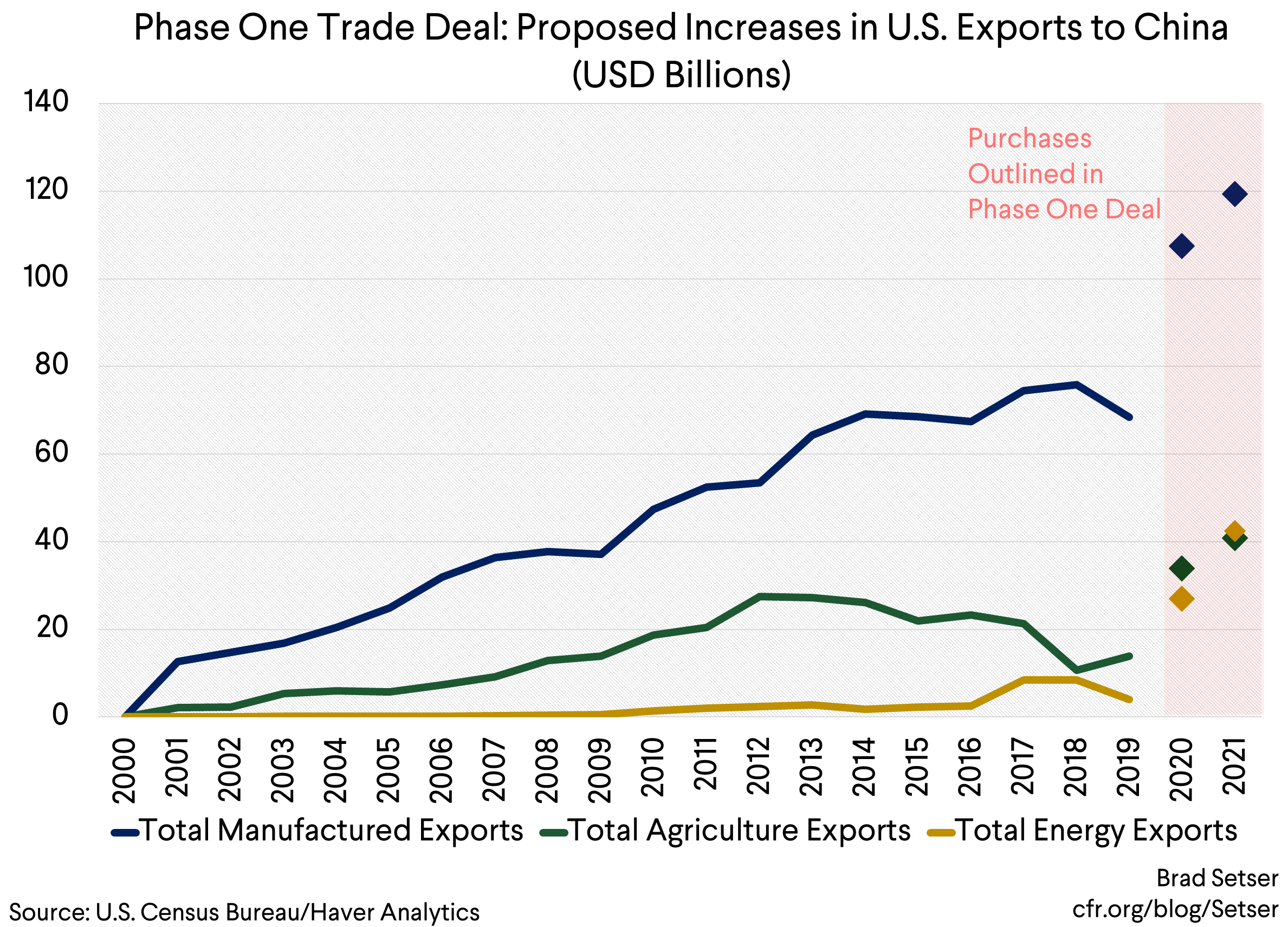

With the phase one trade deal signed—and with China now promising (somewhat credibly in my view) to raise its imports of agriculture and energy above their pre-trade war levels and (less credibly) promising to raise its imports of U.S. manufactures—it is now possible look back at how China decided to respond to Trump’s tariff pressure.

Five points stand out to me…

1. China never was prepared—it seems from the outside—to negotiate on China 2025 or the subsidies and procurement preferences at the center of its industrial policies. (It will be interesting to see what Bob Davis and Lingling Wei have to say on this in their coming book).

On one level that is understandable, China views these programs as central to its efforts to upgrade its own technological capabilities and assure its future growth. At the same time, China’s determination to preserve an import-substituting industrial strategy almost guarantees future trade conflict. The means China uses to support its technological development are at odds with those employed by its large-economy peers and assure that any Chinese achievements can credibly be attributed to unfair (though not necessarily WTO illegal) practices. And, well, China’s vision of technological independence likely implies that over time its imports of advanced manufactures from the rest of the world will fall. And in a world where China doesn’t import (much), some of its trade partners may start to wonder why they keep their markets open to China and Chinese-made goods. But these trends won’t play out over the next year—Boeing has bigger problems right now than the C919, China doesn’t yet have indigenous manufacturer of jet engines, China’s efforts to build an indigenous semiconductor industry aren’t going to have a huge impact on its 2020 imports, and Germany’s machine tools haven’t yet been reversed engineered out of the Chinese market.

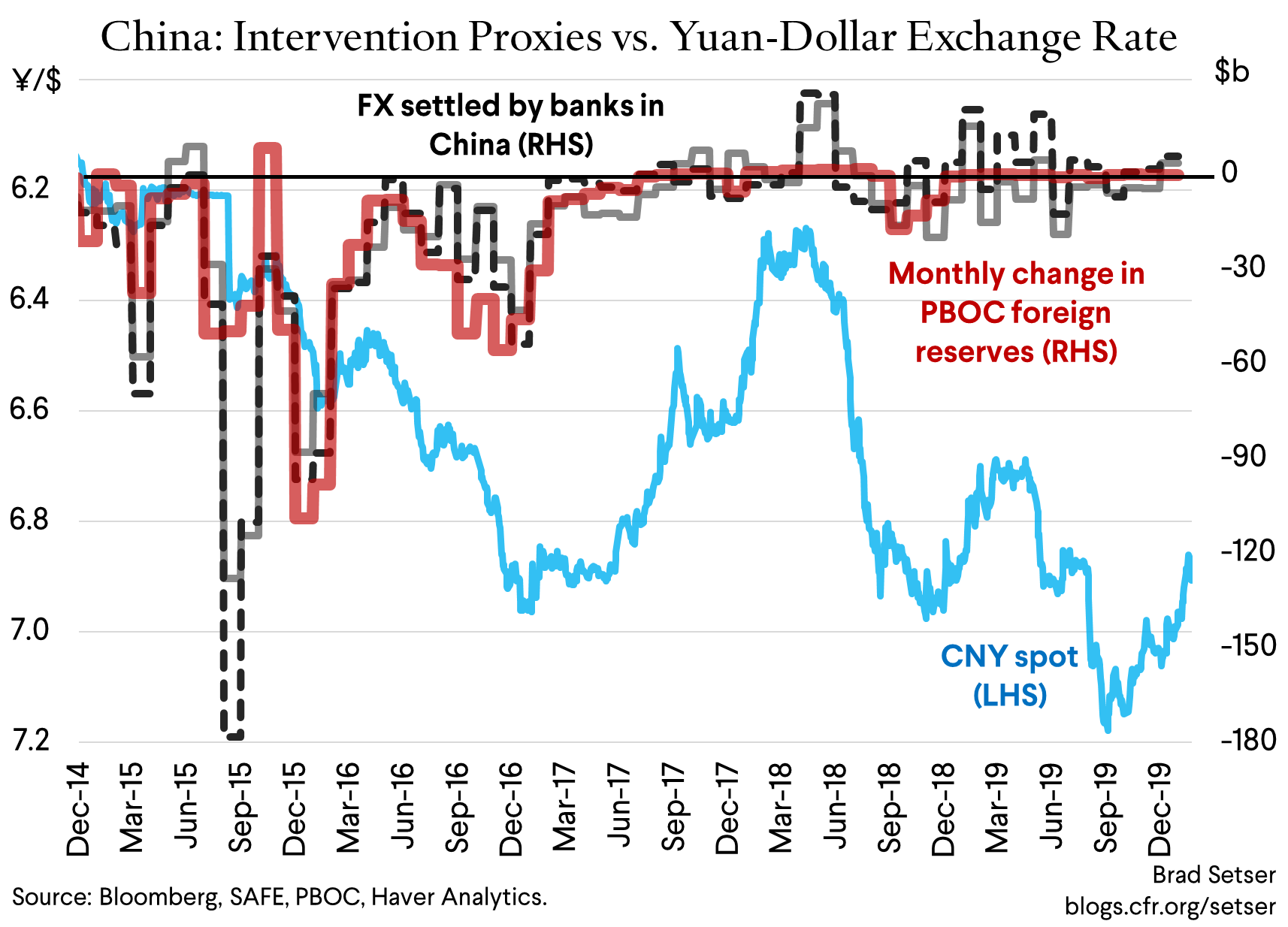

2. China was able to use its currency to buffer the impact of the trade war without ever losing control—and without burning through a lot of reserves.

The yuan has fallen by 8 percent vs. the dollar and 4 percent vs. a broad basket since May 2018. That, in my view, is part of the reason why China’s overall exports have held up reasonably well even as its exports to the United States have fallen.

This volatility in the yuan hasn’t prompted the kind of panic—or the kind of large outflows—that the yuan’s surprise 2015 move generated. In part, that is because China tightened its controls on outflows back in late 2016 and early 2017, and those controls worked. In part, that is because Chinese banks are in a different position that they were in 2015—there wasn’t the dry tinder of a lot of carry trades that could unwind quickly. In part, it is because the yuan remains an attractive alternative to the euro for countries looking to diversify their reserves away from the dollar (at the margin) as China pays interest on reserve assets while the euro area effectively charges a tax on foreign holding of reserves (through negative rates). And in part it is because there never seemed to be a moment when China’s moves seemed all that surprising—the moves in the yuan were commensurate with the tariffs, and thus didn’t seem to signal a bigger future move. And in part, it is a result of the rise in China’s overall trade surplus over the course of the trade war, which provided underlying support for the yuan and helped offset the modest increase in hot money outflows last spring.

But I don’t think many expected that China would be able to keep its reserves stable through the trade war, and to manage the yuan without appearing to burn through many reserves. In fact, the two standard indicators of Chinese intervention suggest either no activity over the course of 2019 (the PBOC’s balance sheet) or small purchases (the settlement data). The balance of payments shows a tiny sale of reserves, but, all things considered, the scale of these sales are modest (even now Chinese data never quite fully lines up, which bothers me more than most).

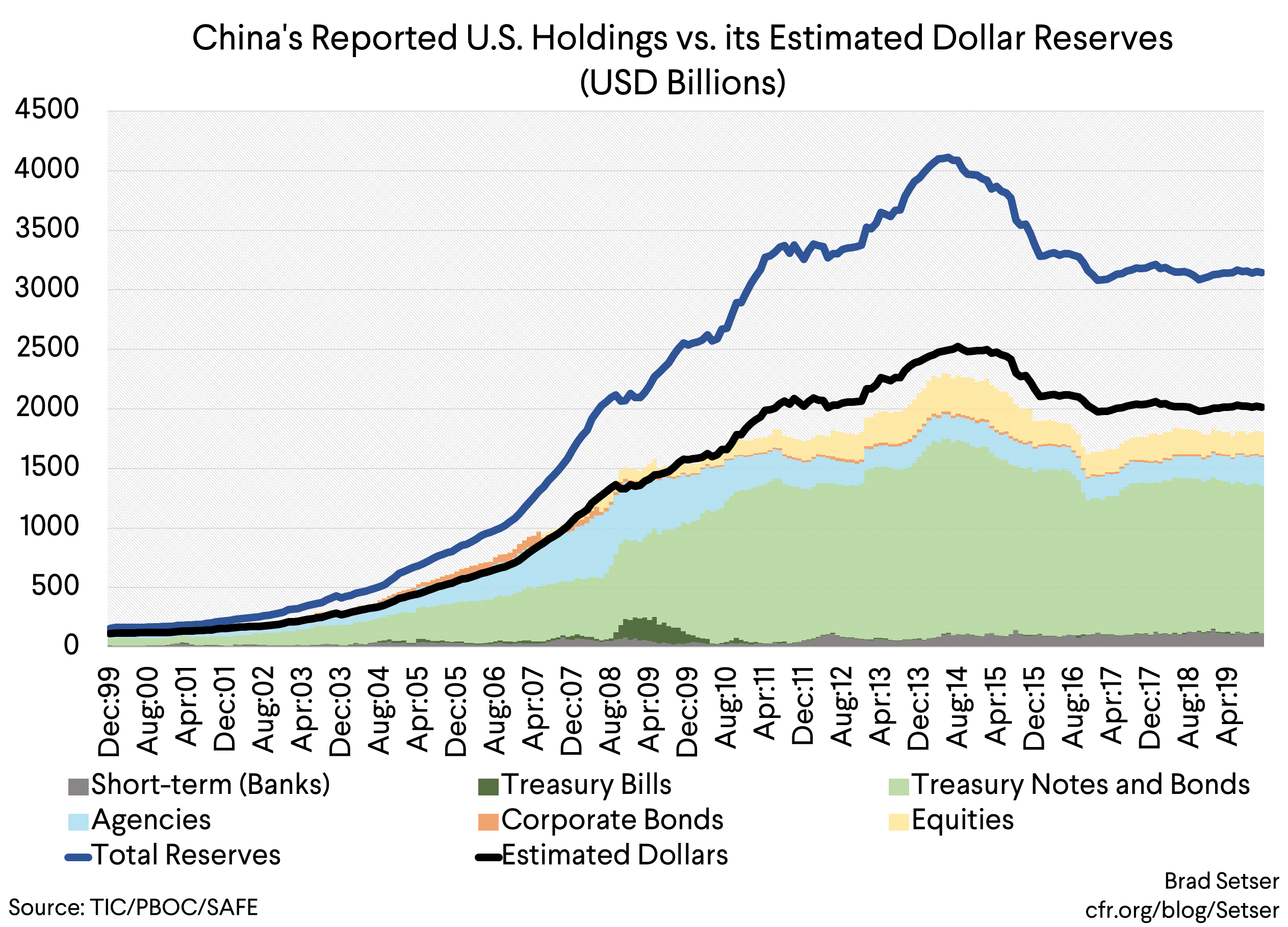

3. China did not try to use its Treasuries as a weapon.

China’s Treasury holdings are down just a bit, but only a bit after you take into account China’s not so hidden holdings in Belgian custodial accounts. And to the extent China has reduced its Treasury holdings, that is because it looks to have been looking for higher yields than Treasuries now offer—it has been buying Agencies again for example, and likely joining other central banks in taking the yield advantage offered by holding Japanese yen denominated bonds and hedging out the currency risk (creating a synthetic T-bill).

At the end of the day, in an era where central banks have recognized that balance sheet expansion (see this paper from my friend Ramin Toloui) and yield curve control are part of the monetary policy toolkit, China presumably realized it didn’t actually have much leverage here—if it tried to push Treasury yields up, the Fed would react. And well China also may simply not have liked the idea of giving up the safe yield that Treasuries provide for negative yielding euro area assets.

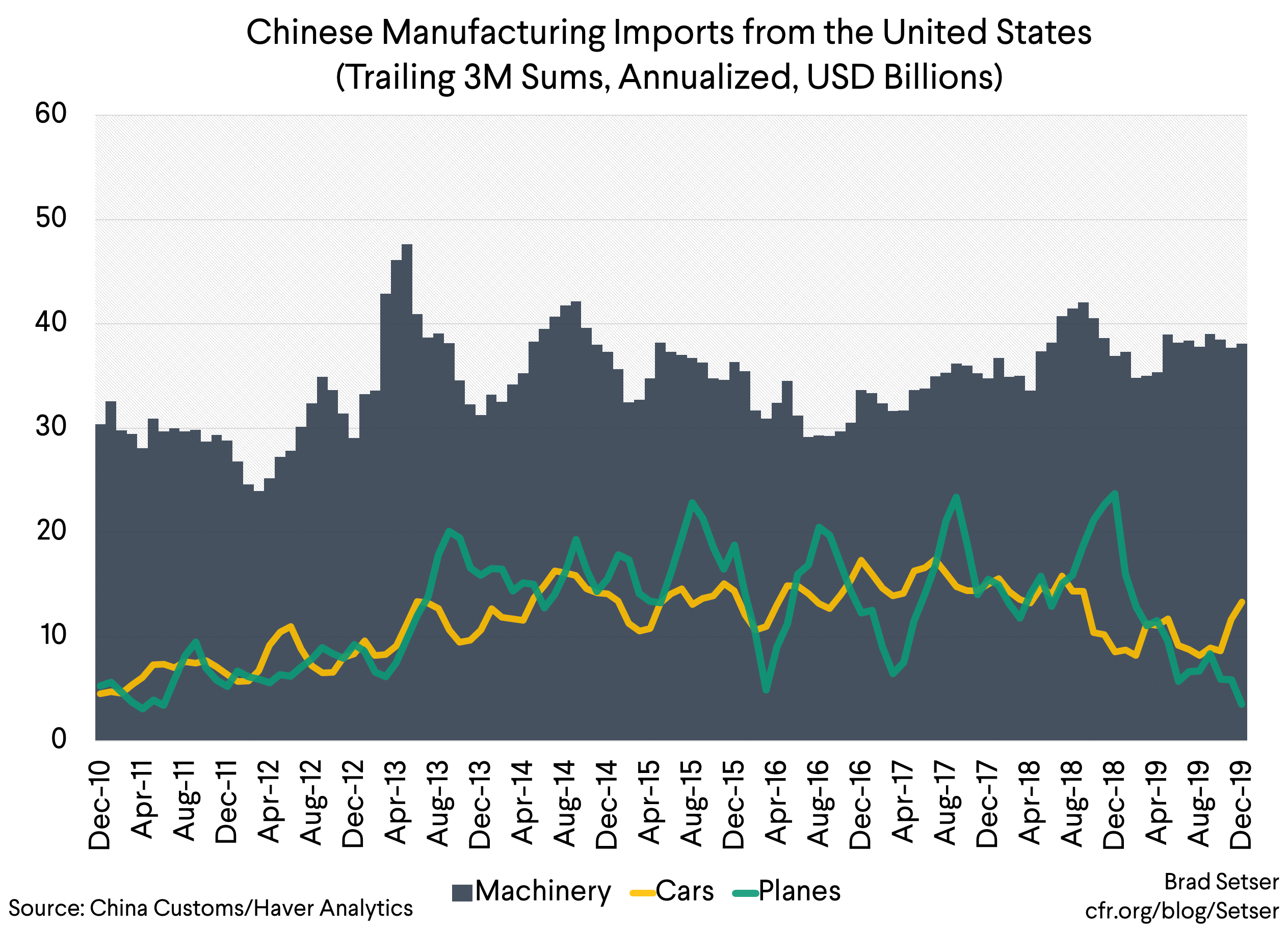

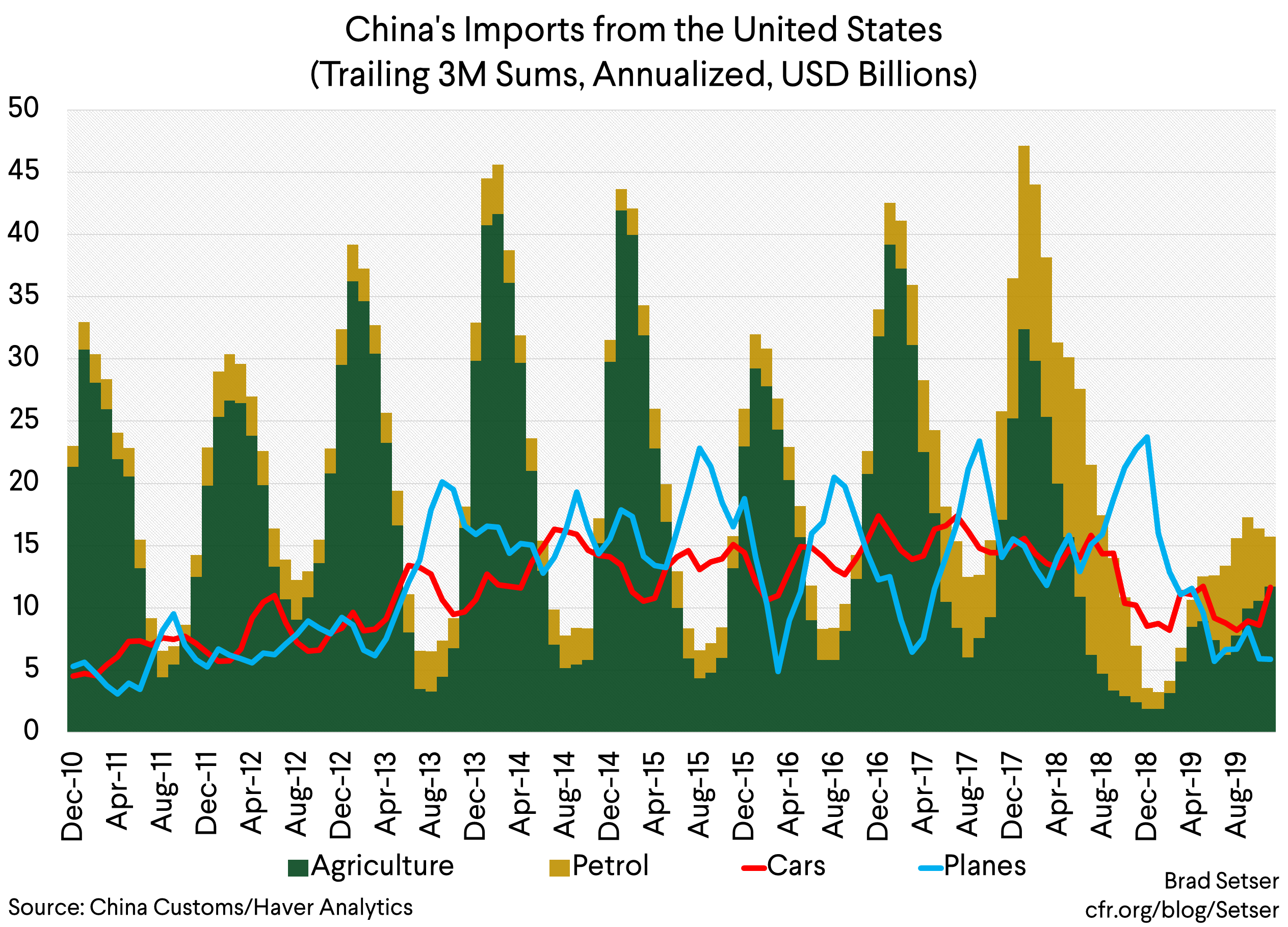

4. China didn’t target U.S. manufactured exports in a big way …

I know this goes a bit against the grain, but if you look at China’s imports of manufactured goods from the United States—excluding cars and planes—there wasn’t much change. Yes, there was a modest fall, but China’s overall imports of manufactures fell by about as much. The United States was not singled out.

I am not quite sure why this is the case.

One theory is that, well, China had already been pretty good at squeezing manufactured imports out of its market, and the remaining U.S. imports were goods that China needed (whether for its own exports, or because of a lack of domestic capacity).

Another is China wanted to preserve some space for retaliation in the event that Trump eventually expanded the scope of the tariffs.

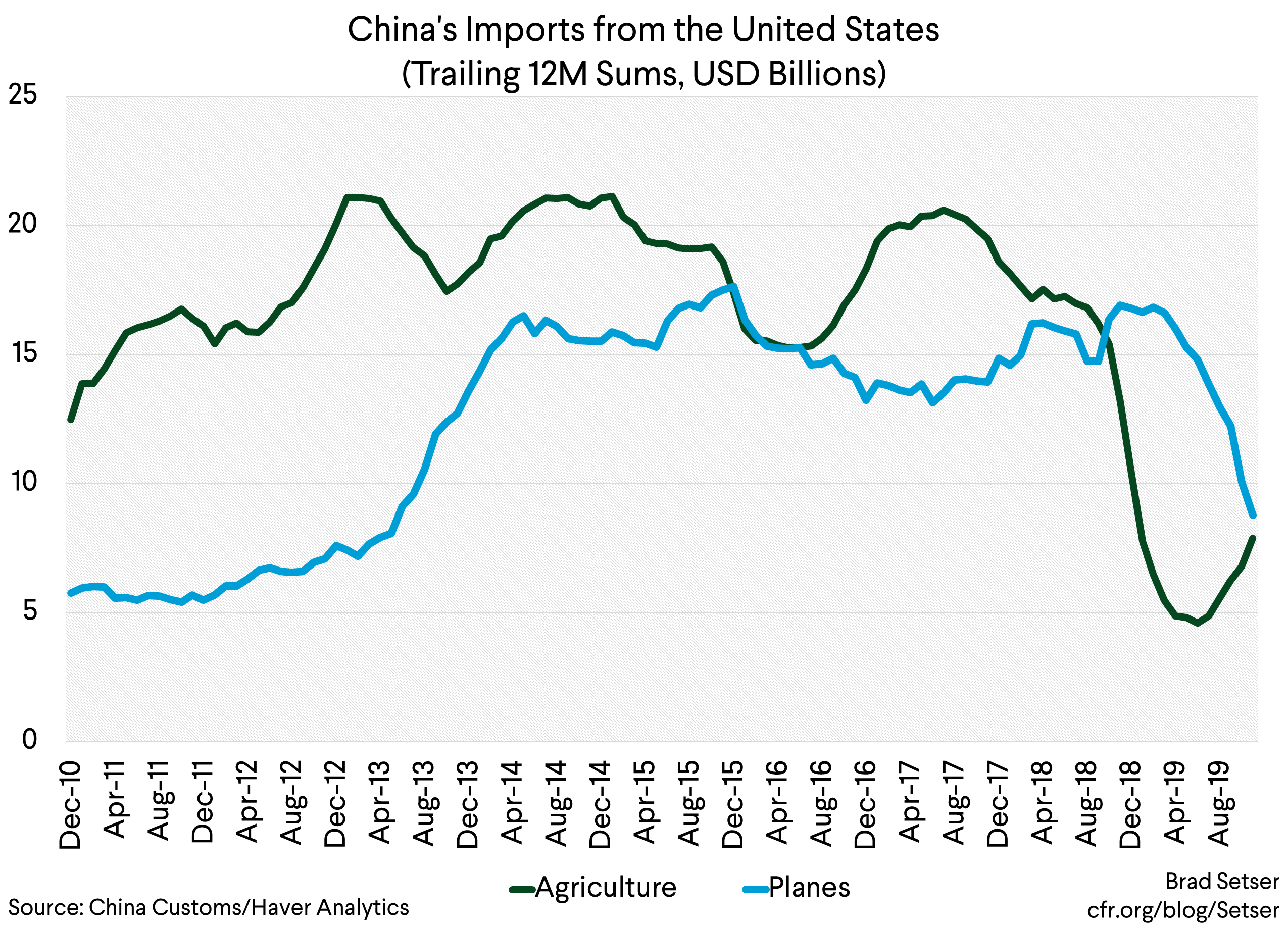

There are of course exceptions—China’s auto imports from the U.S. did fall in late 2018 when China put retaliatory tariffs on U.S. made SUVs. But even before the formal truce those imports had bounced back. And China’s imports of planes have dropped dramatically. That though is almost all Boeing’s fault: China has scaled back its orders to gain trade leverage, but 2019 exports are essentially the function of post orders and Boeing’s capacity to deliver.

(As a side note, I wouldn’t be surprised if a big order for the new 777 and 787s are part of the deal—the text of the deal counts orders as well as actual exports toward meeting China’s commitment in manufacturing).

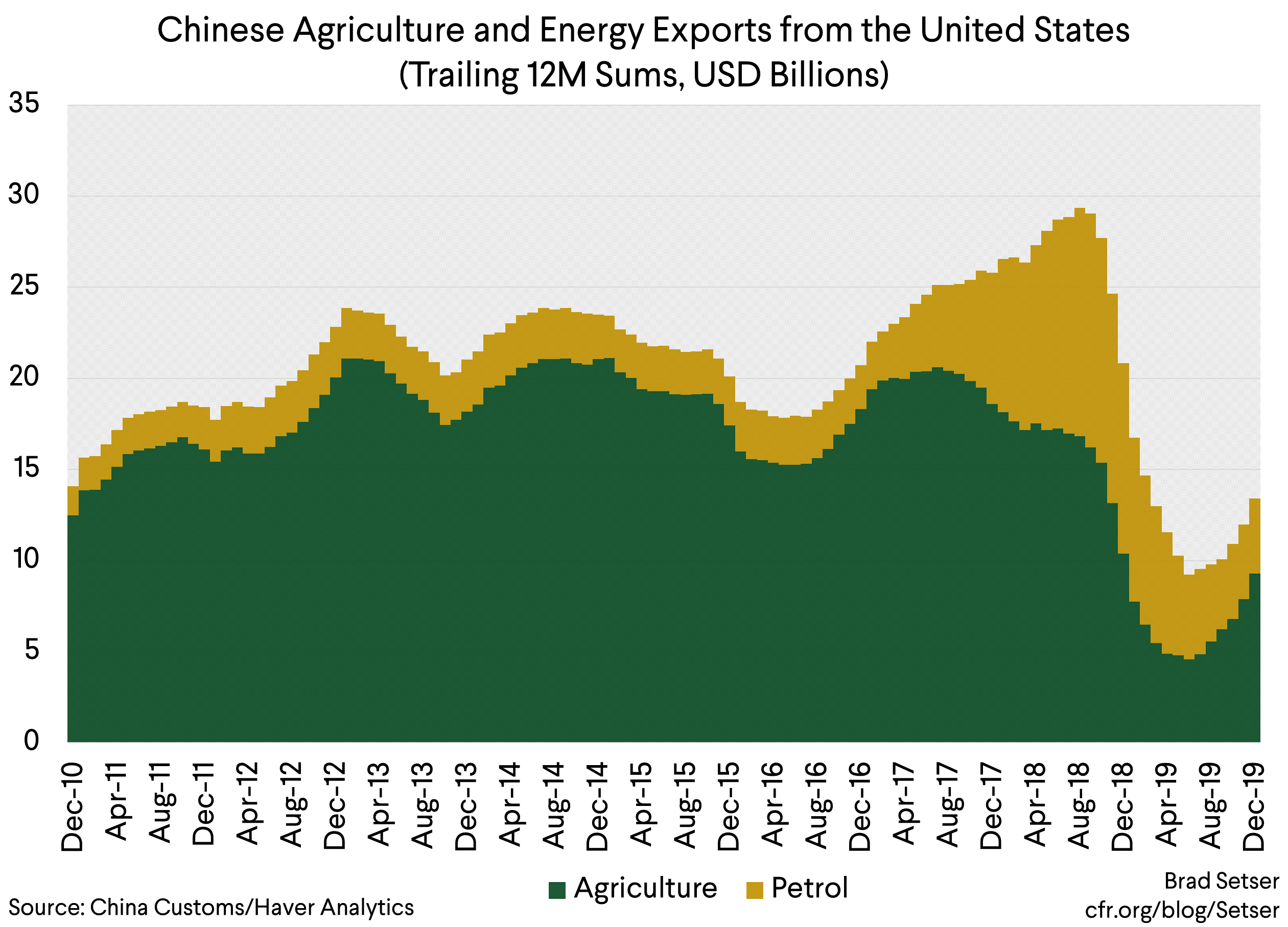

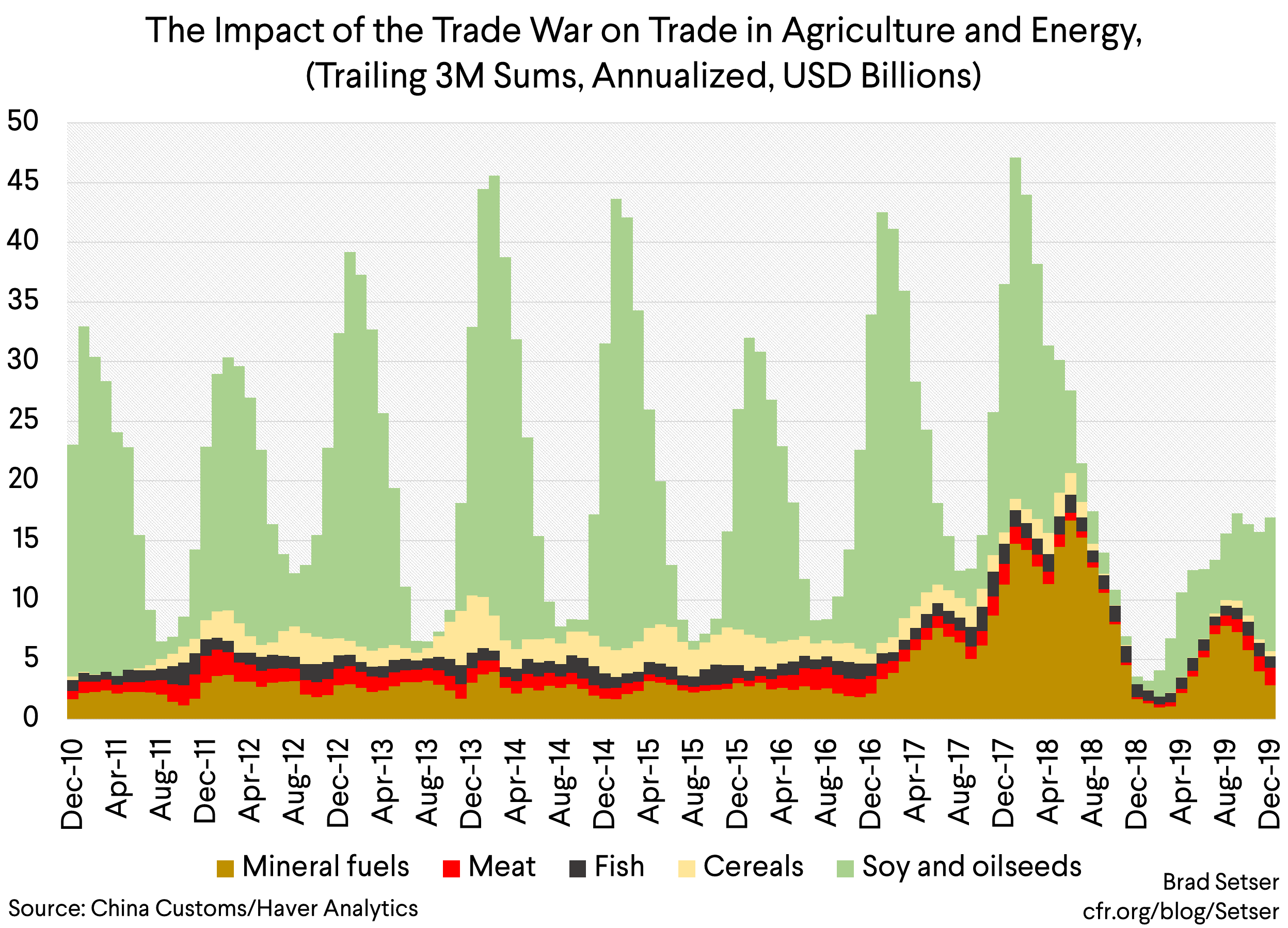

5. China did target American agricultural and energy exports, with mixed success.

The fall off in energy imports didn’t have a big impact on the U.S. economy—there are other markets for sweet light crude and natural gas liquids.

The fall off in agricultural imports though did have a modest economic impact, and a big political impact.

Part of that was fully expected. China’s preferred targets in trade cases have long been the smaller and more specialized U.S. agricultural exports—from chicken paws to distillers dried grain to sorghum to nuts and lobsters.

And soybeans were an obvious big target. I was surprised by the size of China’s impact on the market—I thought U.S. soy would prove to be more of a pure commodity, and the global market would adjust. But China is such a big share of the global market (two-thirds of global imports) and China was sufficiently ruthless in its absolute refusal to import from the United States in the fall of 2018 that the global market couldn’t adapt. U.S. beans traded at a discount to Brazil (unambiguous evidence of an impact). Some of that was being arbitraged away over the course of 2019—when the United States is exporting beans to Argentina so Argentine beans can go to China uncrushed, you know something a bit unusual is happening (the ultimate arbitrage is U.S. beans feed Brazilian pigs and chicken, freeing up all of Brazil’s harvest for China).

Why does this matter?

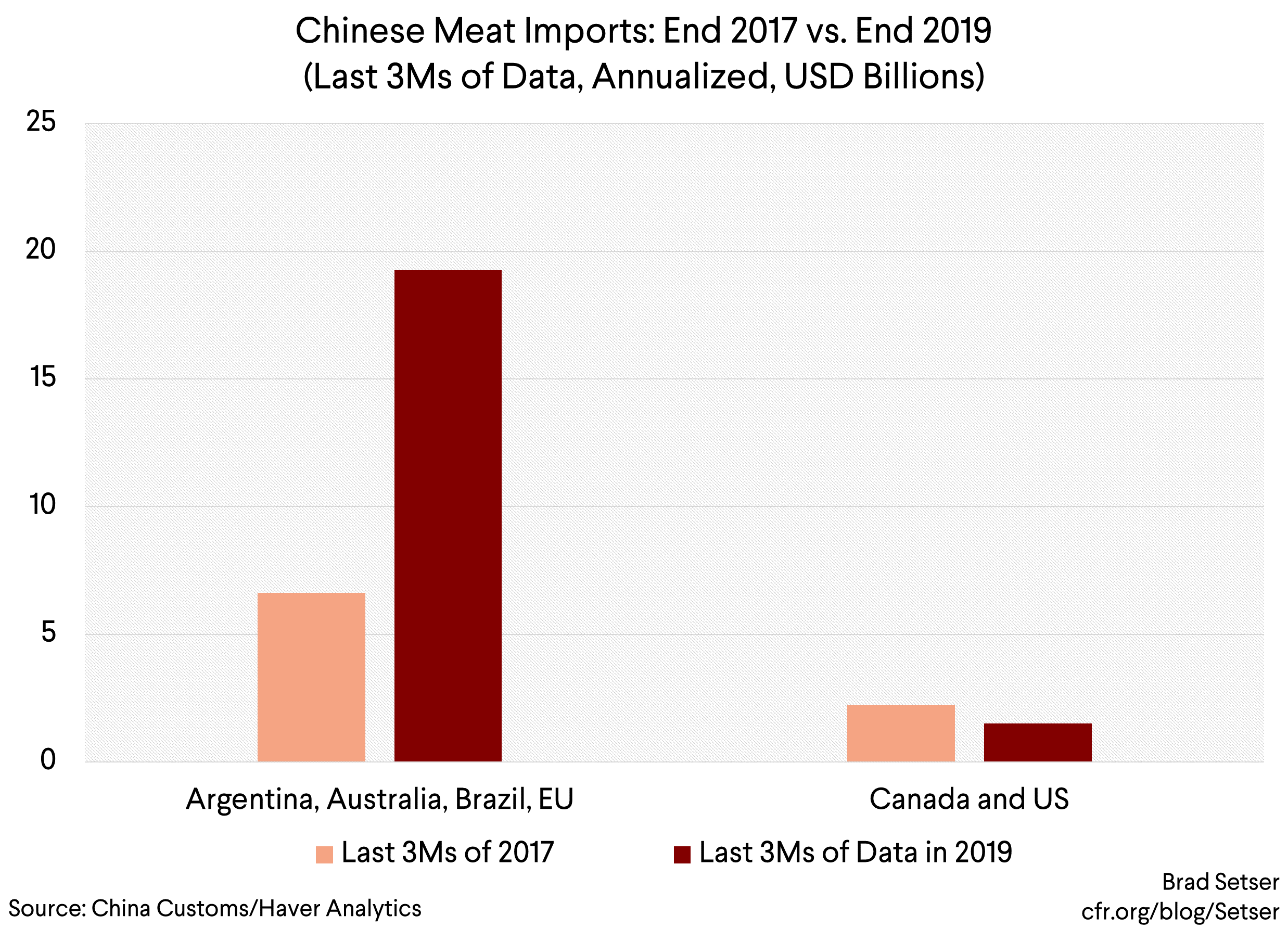

Well, I think China’s revealed capacity to manage its commodity imports over the course of the trade war suggests that it could meet its 2020 agriculture and energy commitments. It of course also helps that China is now importing $25 billion of poultry, pork and beef from the world. There is, for now at least, plenty of demand to share.

But it also reveals one of the risks of Trump’s strategy of managed trade.*

What China’s state gives, China’s state can take away.

We should more or less know that the price of taking on Chinese industrial policy will be renewed retaliation against U.S. agriculture.

That makes life difficult for America’s farmers. China will likely be a big market in 2020. But it isn’t going to be a safe or stable market.

* I thought the Economist’s article did an admirable job of laying out both the disadvantages of Trump’s approach (the U.S. is essentially giving China a big reward for redirecting its imports away from U.S. allies toward the United States, but it isn’t clear the U.S. benefits from exporting say more corn and LNG to China and less to Japan) and the disadvantages of the conventional approach toward China. I am not sure the considerable effort that the Obama Administration put into changing China’s legal rules on indigenous innovation procurement back in 2010 and 2011 yielded much in the end; they certainly didn’t change China’s basic policy approach.