Will the Proposed Restructuring of COFINA Bonds Assure Puerto Rico’s Return to Debt Sustainability?

Puerto Rico’s government and the bulk of the holders of Puerto Rico’s Sales tax backed bonds (COFINA) appear to have reached agreement on restructuring terms (details here). The deal will reduce Puerto Rico’s near-term payments, freeing up a bit more money to support Puerto Rico’s reconstruction. But the terms, in my view, still fall short of providing Puerto Rico with a clear path back to debt sustainability.

This is largely because the payments on the restructured bonds rise over time—while Puerto Rico’s capacity to pay may fall over time. It isn’t clear what will support Puerto Rico’s economy once the $80 billion or so from federal disaster relief funds and private insurance payments run out.

The rise in payments on the sales tax backed bonds might be justified if Puerto Rico was paying back the bond’s principal—and thus reducing its debt stock over time (and freeing up borrowing capacity to finance new investment).

But that isn’t what is happening—or rather, it isn’t exactly what is happening.

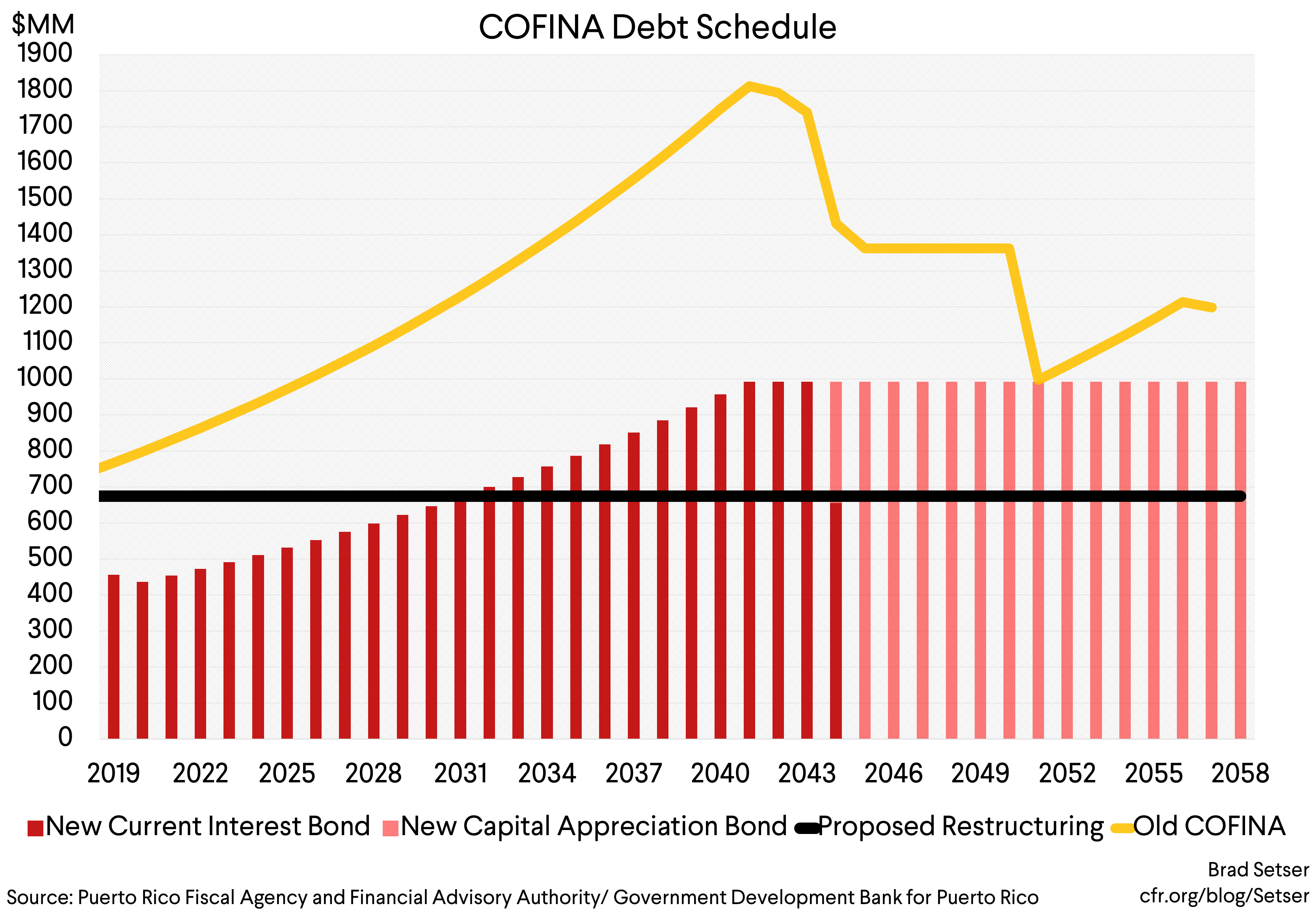

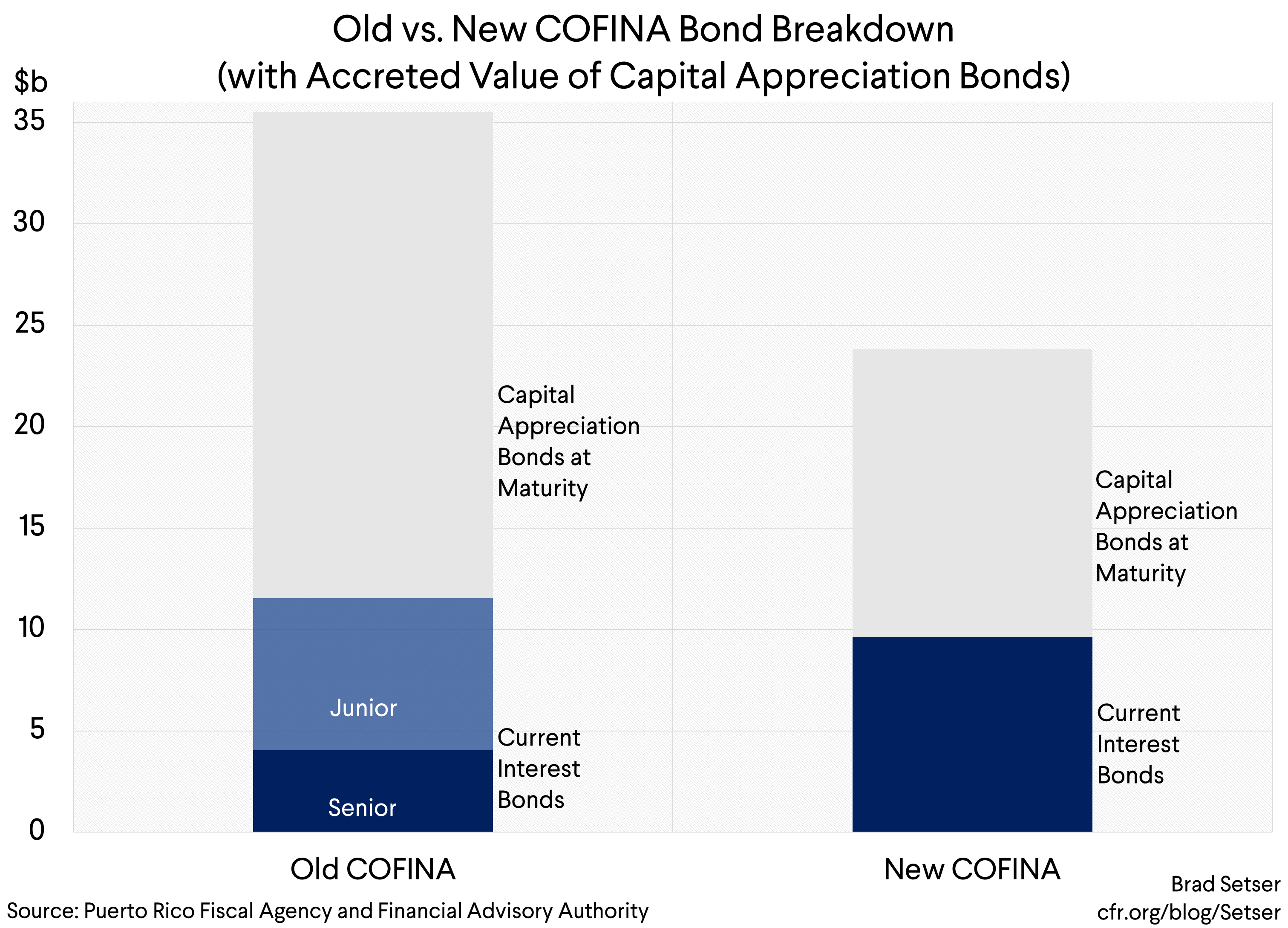

Technically Puerto Rico will be paying back the principal on some of the new sales tax backed bonds it plans to issue—but those payments will be offset by the growing amount Puerto Rico owes on a second bond (a capital appreciation bond) that is lurking in the background. When the $9.6 billion in new sales tax backed bonds issued in the restructuring are paid off, Puerto Rico will still owe….$14.2 billion on its sales tax backed bonds (Exhibit A, see p. 130 of the .pdf).

It isn’t hard to think of alternative deal terms that wouldn’t leave creditors that much worse off but that would substantially reduce the long-run risks to Puerto Rico. I hope it is not too late for those alternatives to receive serious consideration.

The COFINA Restructuring

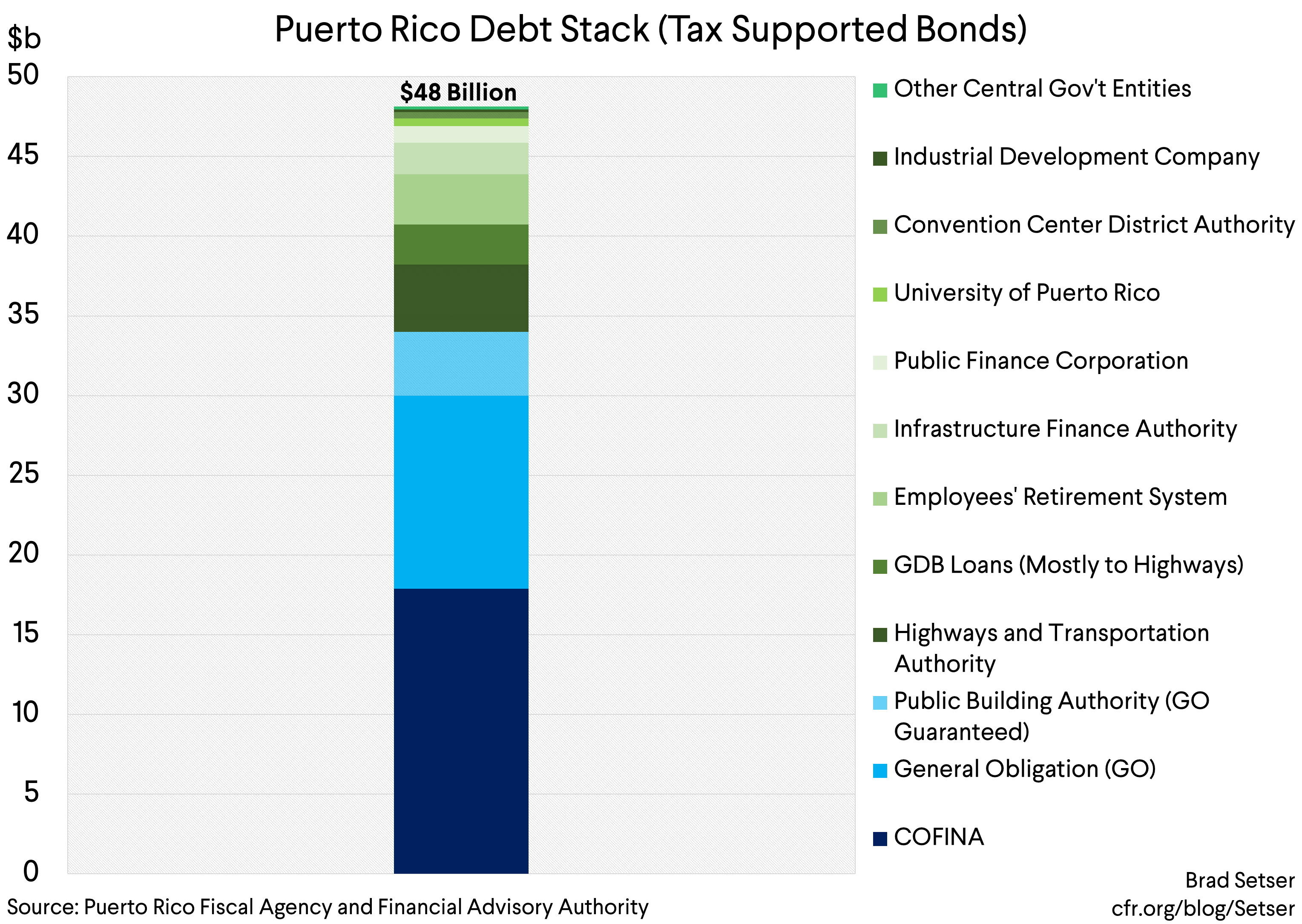

The old sales tax backed (COFINA) bonds in many ways posed the greatest long-term risks to Puerto Rico’s debt sustainability, even though they account for roughly a third of Puerto Rico’s tax-supported debt.*

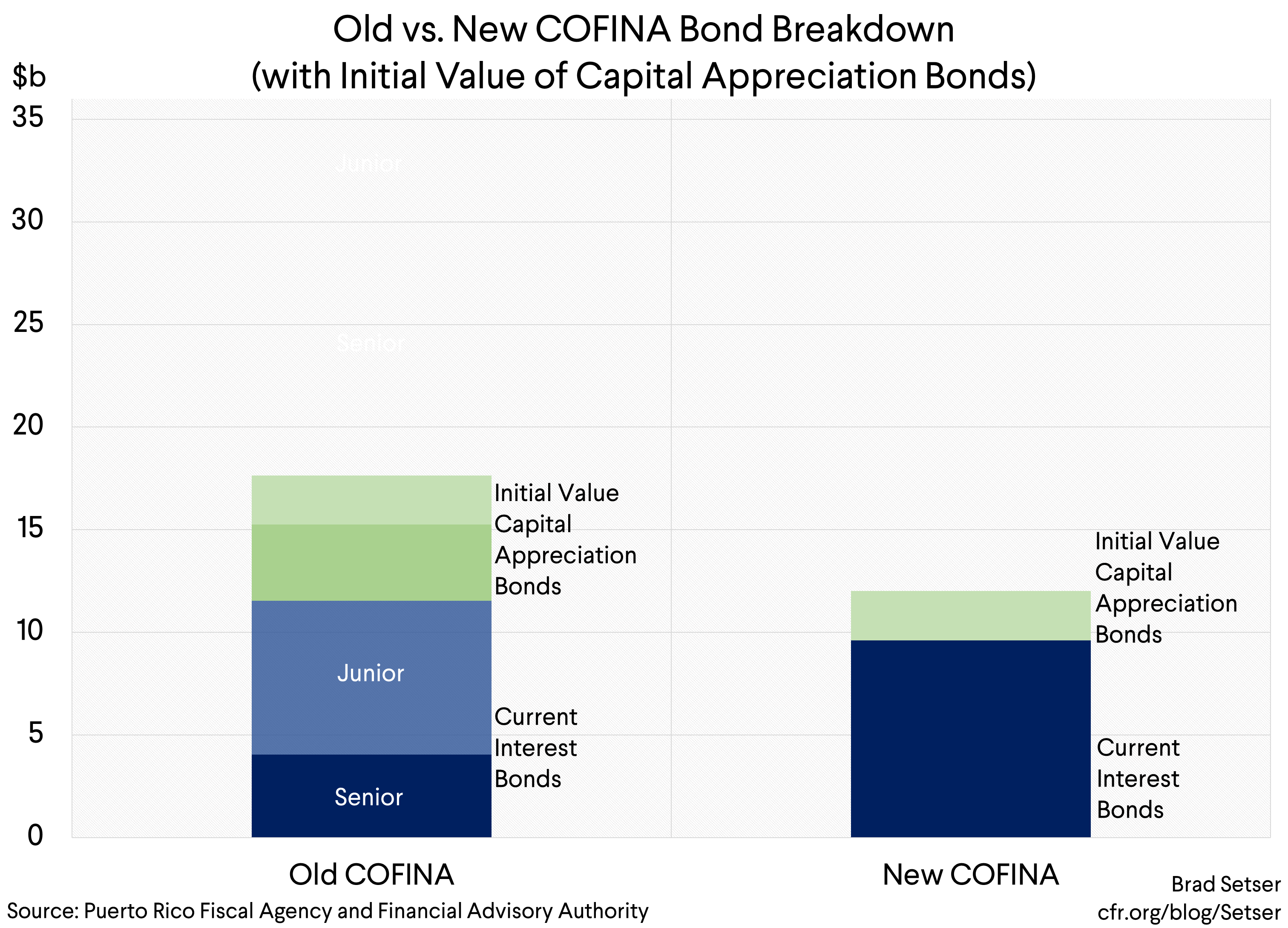

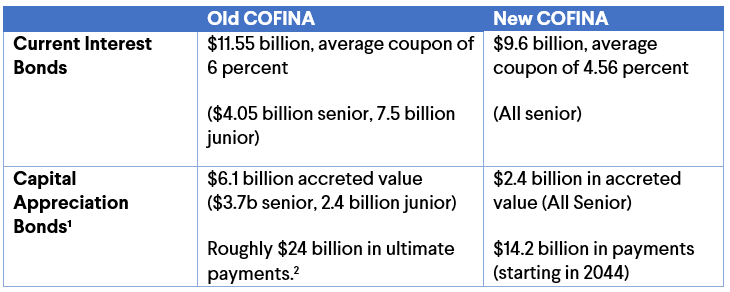

Because of the diabolical structure of the capital appreciation bonds, the real burden of the COFINA bonds was actually a lot higher than implied by the $17.5 billion in bonds outstanding in 2017 ($11.5 billion in current interest bonds, $6 billion in capital appreciation bonds).** Puerto Rico faced an increase in debt service over time from around $700 million back to $1.8 billion. And since the bonds had a direct claim on 5.5 percentage points of Puerto Rico’s sales tax revenue, rising debt service would effectively starve the government of funds.

So what happened in the restructuring (outlined in exhibit A, p. 130 and appendix B, p. 140)?

About $11.5 billion in current interest bonds, with a coupon of almost 6 percent (current interest payments are around $700m), will be swapped into $9.6 billion of new bonds with an average coupon of 4.5 percent.

There is some real debt relief in this deal—payments on COFINA bonds fall from the current level in the near term, freeing up funds for the budget.

But creditors are also trading up in a couple of important ways.

The old bonds were a mix of senior and junior bonds. The new bonds are all senior bonds. The debt reduction (not surprisingly) is coming from the junior bonds, which get equal status with the senior bonds.

The payment structure on the current interest bonds is also being pulled forward—they are all paid off over the next twenty-five years. Payments on the capital appreciation bonds were moved back.

1Accreted value of the CABs is misleading, as payments were pushed back, providing more time for the bonds to grow in value

2See this link.

And by reducing the size of the maximum annual payment from $1.8 billion to $1 billion the bond holders substantially increased the strength of the sales tax pledge.

There is an easy way to see this—under the terms of the COFINA deal, the bondholders get first dibs on a 5.5 percentage point sales tax, up to a certain defined amount (the pledged sales tax base). The sales tax now raises close to $250 million per percentage point—so 5.5 percent raises something like $1.5 billion. If that tax didn’t grow over time, well, the bond holders would be in trouble, as under the old payment schedule Puerto Rico has to pay a peak of $1.85 billion or so. By reducing the peak payment, the bondholders made it much less likely that the 5.5 percent sales tax will not generate enough revenue to cover the payments.****

A stronger pledge is worth a lot, particularly for the junior bonds. So in practice the bond holders aren’t giving up quite as much as it seems. They get less cash, but the quality of their security interest has substantially improved.

If the deal only consisted of the current interest bond, it basically would work—$500m or so of interest is something that Puerto Rico likely can afford, even taking into account that it will need to pay something on its other bonds.

What creates the trouble? Pulling forward the amortizations of the current interest bond, and filling the backend with a new capital appreciation bond. The current $6 billion in capital appreciation bonds are being swapped into a new $2.4 billion capital appreciation bond. But don’t focus too much on the current notional value—capital appreciation bonds (CABs) don’t pay a coupon, so their current value doesn’t represent a current payment burden. They cause problems because they grow in value over time and thus lurk in the background as a threat to long-term debt sustainability.

Since the new CAB doesn’t start making payouts until 2044, it also has longer to quietly accrete (to use the technical term of the increase in the value of the bond). At its peak, it rises to $14.2 billion in value, before it is paid off over about fifteen years (in a series of $1 billion a year installments—it really is structured as a series of zeros, technically speaking, though not for tax purposes). That’s less than the old capital appreciation bonds, but still too much.

The risk of the new bond, as I see it, is that the amount Puerto Rico needs to pay will double (from under $500 million to $1 billion) over the next twenty years before leveling off (exhibit 3, p. 10). And that rise in payments does not help to reduce Puerto Rico’s outstanding debt stock. With a capital appreciation bond hiding in the background, the amortization payments on the current interest bond are in a deep sense fake, as the capital appreciation bond is growing in value faster than the current interest bonds are being paid off.

The increase in payments would be fine if Puerto Rico’s economy could reasonably be expected to double over the same period. That’s the case when for example an emerging economy has just experienced a big depreciation, raising the current value of its foreign currency debt—but also creating a dynamic where the currency should recover in real terms over time. But it isn’t a sure bet for Puerto Rico.

The oversight board is projecting that Maria, and the influx of disaster aid that followed, will in effect jolt Puerto Rico out of its post 2006 torpor. The risk, of course, is that Puerto Rico’s economy fades once the influx of federal disaster funds (estimated to reach close to $10 billion a year at its peak, providing —counting a modest multiplier—something like a $2 billion plus boost to Puerto Rico’s economy; see exhibit 9, p. 20) goes away.

Think of it this way: right now, Puerto Rico isn’t paying the bulk of its debt and it is receiving large sums of federal disaster funding (including $4.8 billion in additional Medicaid funding). In the future, Puerto Rico will need to pay the new debt that emerges out of the restructuring and it won’t benefit from the disaster funding. The next five years should be fine. The five years that follow might not be.

What’s frustrating to me is that there are fairly obvious alternative payment structures on the new sales tax backed bonds that would leave Puerto Rico in a much more sustainable position.

Take one simple alternative: replacing the new capital appreciation bond with an equivalent amount of current interest bonds for example, and amortizing these bonds over 40 years.

Increasing the amount of current interest bonds would raise the interest payment on the new bonds to $540 million—above the level in the proposed deal, but below what Puerto Rico pays now. And in a pure amortizing structure (discounted at 4.5 percent) Puerto Rico would need to pay a flat $650 million a year—but that would be enough to pay the bond off entirely over forty years (and cut its value by a third over twenty years).

That is less than Puerto Rico now pays into the COFINA trust, and far less that it has to pay in the future under the proposed new structure.

And it is the kind of deal that is robust against the most obvious risk that Puerto Rico faces, namely that it falls back into long-term stagnation, with a high rate of out-migration limiting its future economic size (and debt servicing capacity). And it provides a clear path back to the kind of debt load that would be consistent with eventual statehood as well.

Creditors wouldn’t be that much worse off in this structure—they get a bit more cash up front.

The negotiations over COFINA were heavily driven by the terms of the legal settlement over the sales tax pledge—together with the governor and the board’s still fairly optimistic assumptions about long-run growth. No one seems to have imposed a strong debt sustainability overlay on the new deal. If the governor really wants to have a realistic path to statehood, he needs to make sure Puerto Rico’s isn’t out of line with that of the more indebted states—but the call here ultimately rests with the board, which needs to certify that the restructuring is done on terms consistent with Puerto Rico’s long-term sustainability.

Assessing Overall Debt Sustainability

That leads to the most important, and most difficult, question: what would a sustainable debt payments profile for Puerto Rico look like?

Right now, the debt sustainability analysis in Puerto Rico’s latest fiscal plan—and in the COFINA fiscal plan—is thin. The COFINA debt sustainability analysis essentially just showed that the projected sales tax pledge covers the bond’s projected payments, with no analysis of how the pledge would impact Puerto Rico’s overall finances if sales tax revenue doesn’t grow as projected and no clear assessment of how much would be left over for other creditor groups.

To assess Puerto Rico’s debt sustainability, I think it helps to lay out two strong presumptions to help simplify a complicated debate.

The first is that Puerto Rico’s sustainability shouldn’t hinge on an assumption that Puerto Rico’s capacity to pay will rise over time. The payment profile on the debt consequently should be fairly flat—unless the payment on a portion of the debt is contingent on growth and truly poses no burden if Puerto Rico’s economy stalls when disaster relief funds run out.

The second is that Puerto Rico should be aiming to keep overall payments relative to tax revenues on its tax supported debt in line with that of the fifty states (particularly after 2022, when disaster aid falls off and Puerto Rico has to stand on its own two feet).

Let’s go through the argument for both.***

Why should the board assume that Puerto Rico’s payment capacity won’t rise substantially over time? After all, economies do normally grow, at least in nominal terms.

1. Puerto Rico’s economy was shrinking before Maria. One lesson the IMF has learned painfully over time is that assuming that past trends don’t reassert themselves is dangerous. The available studies on the long-term effects of natural disasters also aren’t encouraging.

2. Demographics aren’t going to work in Puerto Rico’s favor. Even without further out-migration, Puerto Rico’s population will shrink (the board forecasts it will fall from 3.4 million pre-Maria to about 3 million in 2022, and further falls are a given as a result of a low birth rate and past out-migration). And so long as workers can earn more—and get more federal benefits—in Orlando than San Juan, a certain fraction of the rising cohort of new Puerto Ricans will move off-island. A natural decline in the working age population of around 1 percent a year could easily turn to 2 percent.

3. Federal aid falls off a cliff in five years. The $4.8 billion in extra Medicaid funding actually expires earlier, but the governor and board now expect other federal aid disbursements to ramp up as the Medicaid funds fade. The sharp fall off in overall help is now projected to start after fiscal 2022—and the fall off in funding then is steep (p. 20 of the fiscal plan). The board’s forecasts, I think, assume that the fall off in Federal disaster funding isn’t a permanent shock to growth and output. That’s too optimistic in my view. The significant rebound in tax collections that followed the most recent influx in federal aid won’t last forever, so the fall in federal funds also directly impacts the budget.****

4. Puerto Rico’s economy still relies heavily on pharmaceutical manufacturing, and the long-term commitment of the pharmaceutical sector to Puerto Rico isn’t clear after the new tax reform. Puerto Rico’s government also relies heavily on taxes on the pharmaceutical sector and a large software firm that once upon a time produced floppy disks in Puerto Rico—companies that are often in Puerto Rico more for tax reasons than because they really need to be in Puerto Rico. The current tax reform—and the future tax reforms needed to fix the holes in the current tax reform—pose a risk to Puerto Rico.

5. The gains from structural reform are uncertain. There is no doubt that Puerto Rico has room to improve the efficiency of government services, and to make it easier to do business on island. Projecting those reforms will raise the level of output by a couple of percentage points over time is reasonable. But assuming that often painful reforms can offset the drag from the future loss of federal funds and permanently change Puerto Rico’s trend growth is a risk. They could. But if the gains are less than expected and don’t offset the demographic headwinds, Puerto Rico could be in real trouble.

Legally binding increases in payments worry me, as the payment increase is far more certain than the improvement in Puerto Rico’s capacity to pay. I consequently believe the growth baseline that the board uses to assess sustainability should be fairly conservative, with only modest assumed nominal GNP growth.

So much for the slope on the payment curve. What is a reasonable overall level of payments?

This is all an art more than a science, but one key benchmark should be the level of debt service relative to Puerto Rico’s own revenues.

The state average is around 4.5 percent. New York pays 8 percent. The most indebted states, on average, pay just over 9 percent (exhibit 20, p. 36). Puerto Rico’s revenues —using the board’s definition of the entities that make up the commonwealth, net of federal aid—are expected to rise to $15 billion over the next few years (Exhibits 13 and 14, pp. 25-26). Keeping Puerto Rico’s debt service in line with the average state implies overall payments of close to $0.7 billion a year, keeping it in line with say New York would imply payments of $1.2 billion a year, and keeping it below the average of the most indebted states would imply holding payments under $1.4 billion a year.

The high end of that range scares me. Benchmarking Puerto Rico against Massachusetts and Connecticut is risky. Poorer parts of the country likely have less capacity to support high levels of debt than rich states. And Puerto Rico’s core tax revenues are actually well below total revenues. The commonwealth—focusing on the revenues that are central to the General Fund’s budget—historically has struggled to collect $10 billion in tax, even counting the tax revenues siphoned off in various revenue pledges that backed the debt that was designed to stay off the formal budget.

Look at the fiscal 2018 numbers, which, to my surprise, benefited as much from post-Maria disaster aid than they were hurt by the immediate after effects of Maria.

Puerto Rico collected something like $2.5 billion in sales tax (counting funds that went into the COFINA trust for future debt service), around $2.0 billion in individual income tax,***** $1.5 to $2 billion in corporate income tax (an unusually high number thanks to disaster funding, see p. 27), $1 billion in gasoline and auto taxes (also an unusually high number), $0.5 billion in alcohol and tobacco taxes, and something like $0.25 from Puerto Rico’s share of the federal rum tax. To get tax revenue up to $10 billion, you need to include the roughly $2 billion Puerto Rico currently extracts out of the pharmaceutical and software sectors (thanks to Act 154 and non-resident withholdings).

It is hard to get large amounts of tax revenue out of a poor population, and there are limits to Puerto Rico’s ability to use things like university fees to pay debt service. The “true” tax base of Puerto Rico is modest: Puerto Rico cannot rely on the continued willingness of the United States to in effect let Puerto Rico win in a game of tax competition.

For those sovereign analysts used to thinking of the level of debt service relative to GNP, $1.0 billion is roughly 1.5 percent of current GNP, $1.4 billion is about 2 percent of GNP and $2 billion is around 3 percent of GNP.

What’s the risk of pledging a large part of Puerto Rico’s tax base to future debt service (especially if all other debt benefits from a specific revenue pledge that is designed to be bankruptcy remote)?

Simple: A big gap between what Puerto Ricans pay in tax and what they receive in government services could mean more out-migration, as Puerto Ricans can avoid paying these taxes by moving to Florida. The negative impact of a large debt service burden though isn’t really in the board’s economic forecast, thanks to a host of very technical modelling assumptions (the board’s economic model assumes that fiscal consolidation only temporarily reduces output, so a bigger primary surplus has no impact on long-term growth; there is no hysteresis effect).

The only way to make Puerto Rico sustainable then would be to have the federal government provide more help—as Puerto Rico’s taxes won’t be available to pay for essential government services. That starts to look a bit like the Federal bailout that Congress wanted to avoid.

The sales tax backed debt accounts for just over a third of the tax supported bonded debt ($17 billion of $45 billion). The constitutional bonds have a similar share of the total debt (the Puerto Rico Building Authority (PBA) debt has constitutional status along with the listed GO debt). Holders of the constitutional debt will no doubt argue for a mirror image deal that would raise Puerto Rico’s debt service to $2 billion even if the more junior bonds get zero. That is substantially too high in my view: it would put Puerto Rico’s debt service well above that of any state.

In other words, the COFINA deal, as currently structured, only works if other groups of creditors get relatively little.

There is an enormous gap between the tone of the articles that have looked back at Maria a year on, and the optimistic forecasts that are embedded in the economic plans that are being used in the restructuring deals that Puerto Rico is negotiating with various groups of creditors. If Puerto Rico’s growth disappoints, the proposed $1 billion in annual debt service on the sales tax backed bonds on its own would leave Puerto Rico with a higher debt service burden than an average U.S. state. That’s why I think it is important to keep the long-run payment commitment to COFINA under $700 million—and why I hope the alternative deal outlined here isn’t rejected as out of hand.

*Puerto Rico’s tax supported debt can be broken into three broad buckets: the sales-tax backed bonds, the constitutional “GO” bonds (which have special protection under Puerto Rico’s constitution and were in theory subject to a limit on their issuance) and the rest, a set of bonds that are either subject to clawback and thus junior to the “GOs” or that are explicitly junior. The likely junior claims include: the highway bonds ($4 billion), the pension obligation bonds ($3 billion), the rum bonds (PRIDCO, $2 billion), the conventions and UPR bonds ($1 billion) and the very junior bonds of the public finance corporate ($1 billion). The GDB’s estate also has over $2 billion in junior loans to the highways authority and other entities that I think remain outstanding. Pick your number on the recovery of this bucket…

**The capital appreciation bonds have a near nuclear structure. They aren’t consistently disclosed (Capital Appreciation Bonds: “are only shown in a footnote on the balance sheet of the issuer; it is not required that they be shown as a liability or expense since there are no current interest payments. This can serve to hide the future liability”), they raise almost no money when they are sold and they give rise to large future claims. The “headline” number for the size of the COFINA claim thus is a little deceptive. The real debt burden is higher. While the GOs posed the biggest short-term legal risk to Puerto Rico after a default (Puerto Rico owed about a $1 billion in principal and interest on the GOs, funds that might be pulled straight out of the budget), the rise in COFINA debt service from $0.7 billion a year (in 2015) to $1.8 billion a year (by 2040) was going to be a source of enormous pressure on Puerto Rico’s treasury.

***Revenue from the 5.5 percent sales tax is projected to grow from $1.4 billion to over $2.5 billion over the next twenty years, assuring that there is enough to cover $1 billion in debt service. (exhibit 19, p. 30). That though isn’t an assessment of the risk to Puerto Rico’s sustainability of this pledge, as in bad states of the world Puerto Rico bears the downside (it gets less revenue out of the sales and uses tax, so a higher fraction ends up going to the pledge—there is no risk sharing).

****The fiscal plan makes clear that nearly every single tax line item has been influenced by the disaster funding. Corporate income tax receipts notably have increased because of payments from contractors who set up Puerto Rican subsidiaries. Debris removal uses a lot of gasoline, so gasoline tax revenues (clawed back from the Highway bonds) have soared. Insurance funds have led to a surge in car purchases, and thus auto tax revenues. As a result of these revenues, and the Medicaid funding, Puerto Rico didn’t experience the fall off in tax revenue that was initially feared, and didn’t need a Treasury/FEMA fiscal bridge loan.

*****If Puerto Rico fully replicated the federal EITC in its tax code, its income tax revenue would fall to just around $1 billion. The absence of federal income tax on personal income earned in Puerto Rico isn’t the boon that some argue, as the progressive structure of federal income tax implies the federal government would collect relatively little tax out of Puerto Rico.