The World Bank Stepped Up During the Pandemic

The World Bank (and the IMF) should get credit for increasing their lending to the world’s poorest countries during the pandemic. But without additional action, net flows to developing economies will fall off a cliff.

The World Bank plays many roles in the global economy, but its most important one is leveraging its paid-in capital and providing a steady supply of loans to countries that would otherwise struggle to access the market on financially viable terms. Those loans can cover the cost of building essential infrastructure, or the budget cost of a vaccine campaign. Helping to finance the infrastructure needed for production of low carbon energy in low-income countries certainly should be an important part of the Bank’s mandate going forward.

But helping low-income countries manage unexpected shocks is also important. The Bank—and for that matter, the International Monetary Fund (IMF)—should get credit for stepping up their financial support for the world’s low-income and lower-middle income countries during the early days of the pandemic. Without this help from the multilateral system, financial flows to low-income countries would have collapsed along with exports in 2020 and 2021 would have been a struggle.

Such financing helped avoid even worse outcomes in the world’s least resilient countries— countries that by and large don’t have the ability to easily absorb an unexpected cut off in external credit.

I haven’t always agreed with the outgoing World Bank President David Malpass on a number of economic issues. For one, Malpass has been a big believer in a strong dollar and spurring growth through tax cuts. Before the global crisis, as the Chief Economist of Bear Stearns, Malpass argued that concerns about trade deficits, the housing sector, and saving imbalances were overstated.

But in the face of the shock from an unprecedented and unexpected pandemic, the Malpass-led Bank did what it needed to do. It helped to limit the impact of one the largest shocks the world economy has experienced in recent history.

Malpass, together with Carmen Reinhart, put great emphasis on alleviating the burden of the existing stock of debt on low-income countries. The Debt Service Suspension Initiative (DSSI), set up in May 2020, sensibly proposed that the world’s creditors agree to allow low-income countries to defer making payments on their external debts during the pandemic—freeing up resources for managing the shock, medical testing, and eventually getting shots (often with donated vaccines) into arms.

The DSSI was never enough on its own—for example, it didn’t do anything to help financially prudent countries that hadn’t taken out a lot of loans from Chinese policy banks and commercial creditors.

And it turned out not to work all that well. Commercial creditors never agreed to take part, and countries feared forcing participation by suspending payments because it would impair their credit ratings. Chinese policy lenders appear to have only participated reluctantly. Many Chinese state lenders, led by the China Development Bank, argued that they were commercial lenders. The other bilateral creditors often didn’t have that much debt coming due to them and thus didn’t have much to reschedule. The World Bank’s ex post assessment showed that about $9 billion of $80 billion in total payments were rescheduled. Bilateral creditors accounted for all of the $9 billion in debt service payments that were deferred, but they only rescheduled a fraction the $25 billion there were owed (numbers are from the World Bank’s International Debt Report).

There was also concern at the time the DSSI would add to the total debt of low-income countries. But the amount of interest that was rescheduled and thus effectually added to the outstanding principal was too tiny (a few billion dollars) to really have any material impact on countries’ sustainability.

No doubt, there are lessons to be learned here going forward: neither bilateral creditors nor commercial creditors really helped out much. I have long believed that commercial loans and bonds to low-income countries should come with embedded maturity extension options, as negotiated deferments have proved to be almost impossible (Ukraine last year is an important exception, but its circumstances were truly exceptional). The rescheduling of bilateral debt in global emergency should be made far easier as well.

But the limited impact of the DSSI doesn’t mean that the world’s collective financial response to the pandemic’s financial and economic impact on low income countries was a failure. Concessional lenders like the World Bank were more effective at using their own balance sheets to keep credit flowing to low-income countries in Africa and around the world.

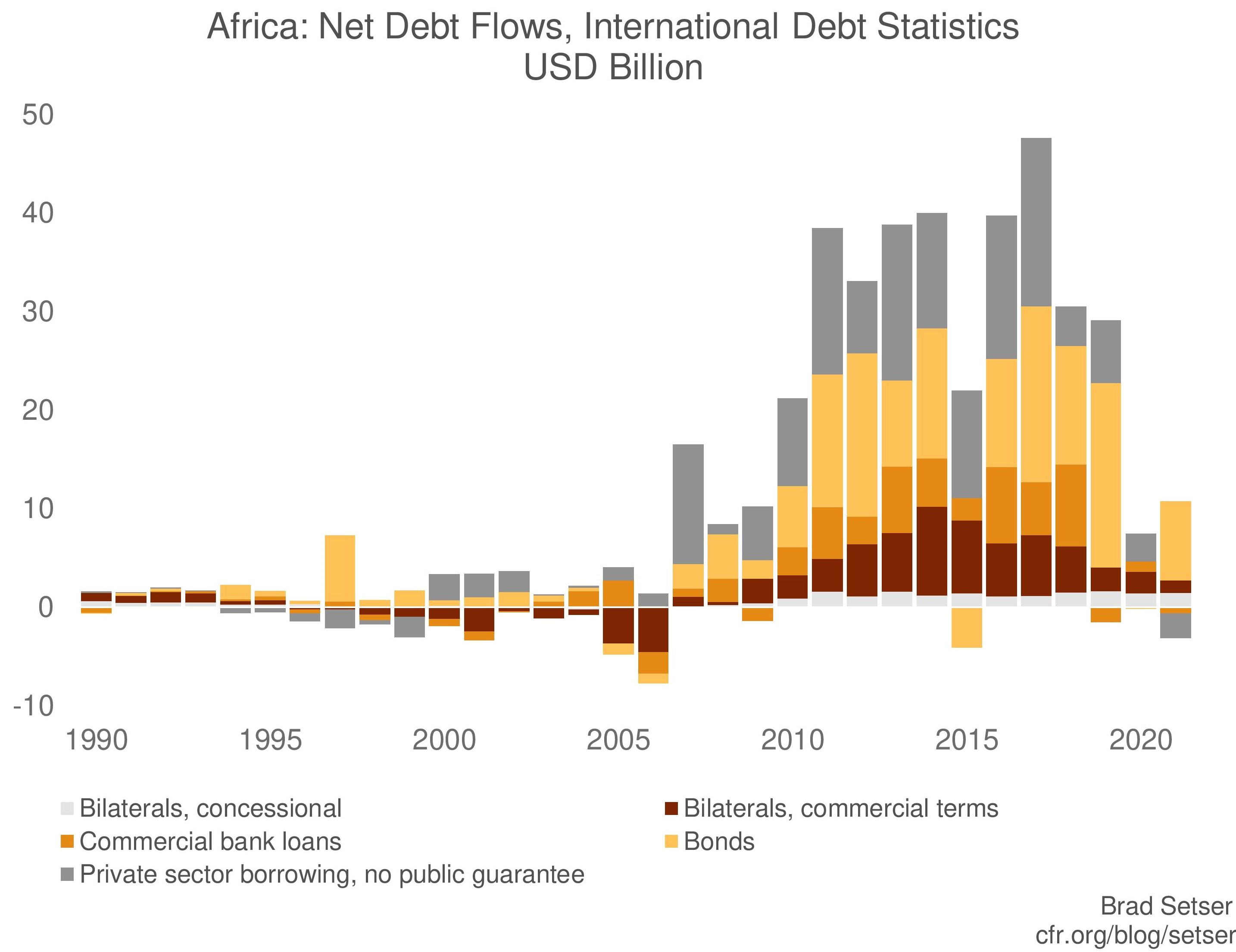

Consider a chart of bilateral flows with commercial interest rates (this will capture most of the activities of the Export-Import Bank of China) and commercial flows (commercial bank flows will capture the impact of many other Chinese state lenders) to African countries over the last thirty years.

There was a massive increase in bilateral and commercial lending to Africa from 2010 to 2019. Net flows from this set of lenders to public sector borrowers rose from almost nothing to around $30 billion a year and total net flows reached $40 billion—real money for a region with a GDP of around $1.6 trillion.

Yet these flows fell sharply in 2020 and 2021. They will likely be negative for 2022.

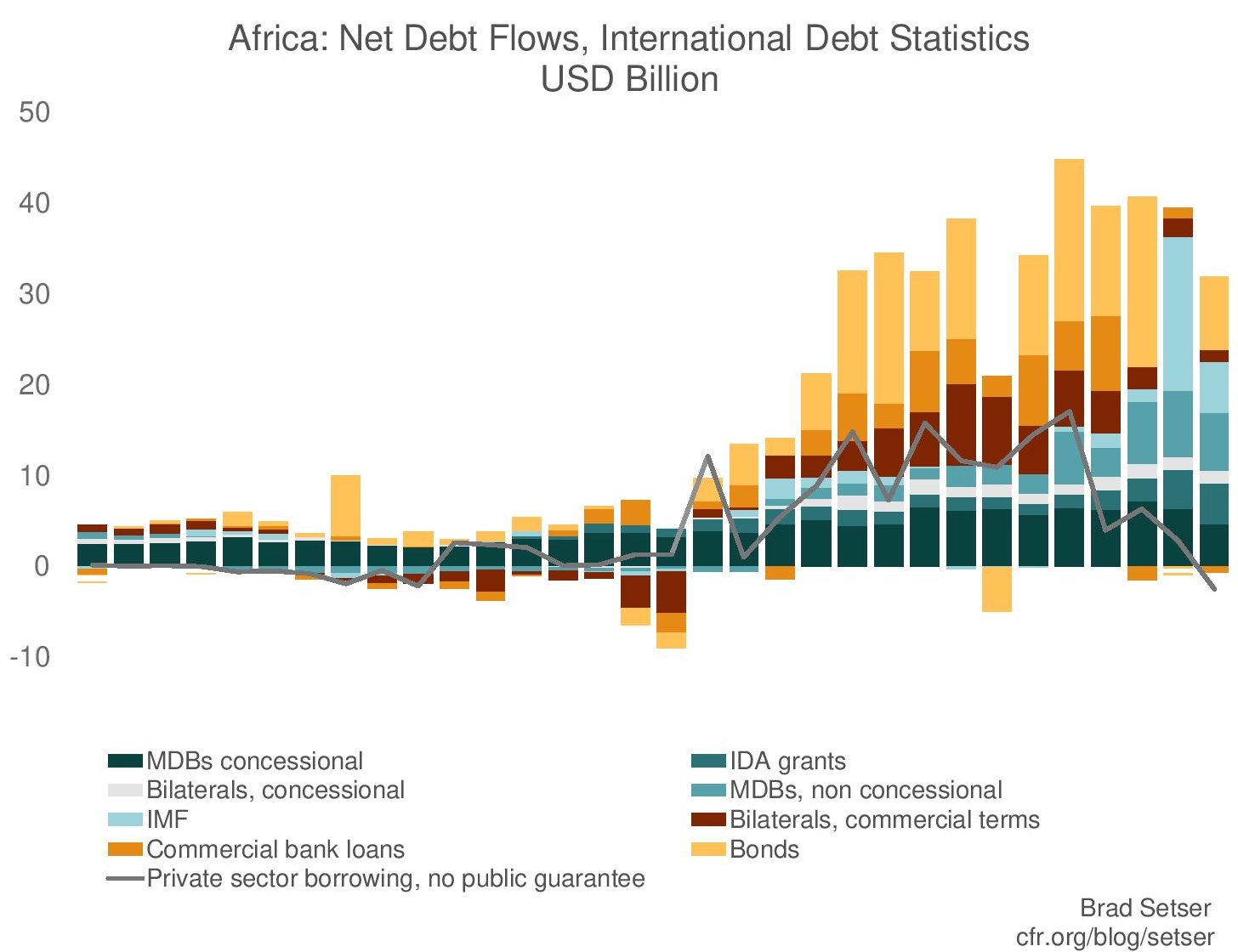

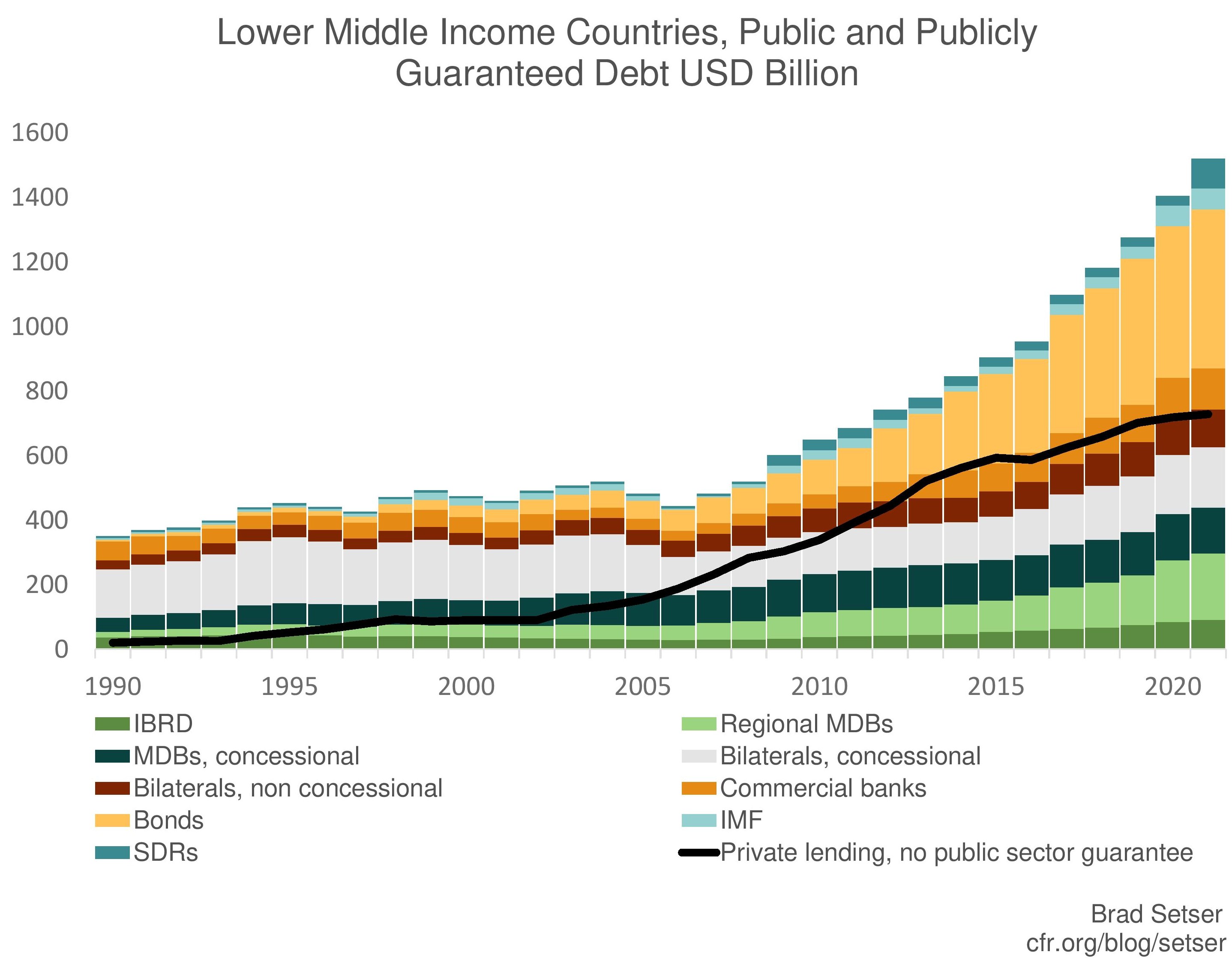

Now look at the same chart with flows from the Multilateral Development Banks (MDBs) and the IMF added in, using data from the World Bank’s International Debt Statistics.

Total flows to public sector borrowers remained at around $40 billion a year (they were a bit lower in 2021, but the SDR allocation made up for the drop). The IMF got concessional funds out the door quickly in 2020. The MDBs, led by the Bank, also increased their net lending.

Such a “surge” in official financing was one of the proposals made by the Group of Thirty back in the fall of 2020.* Such a surge made financial sense, and was a moral imperative as well. The Bank and the IMF, and thus President Malpass and Managing Director Kristalina Georgieva, deserve credit for making it a reality. The system, in a sense, worked. Low income countries had to struggle through the pandemic, but they didn’t lose access to new financing at the same time.

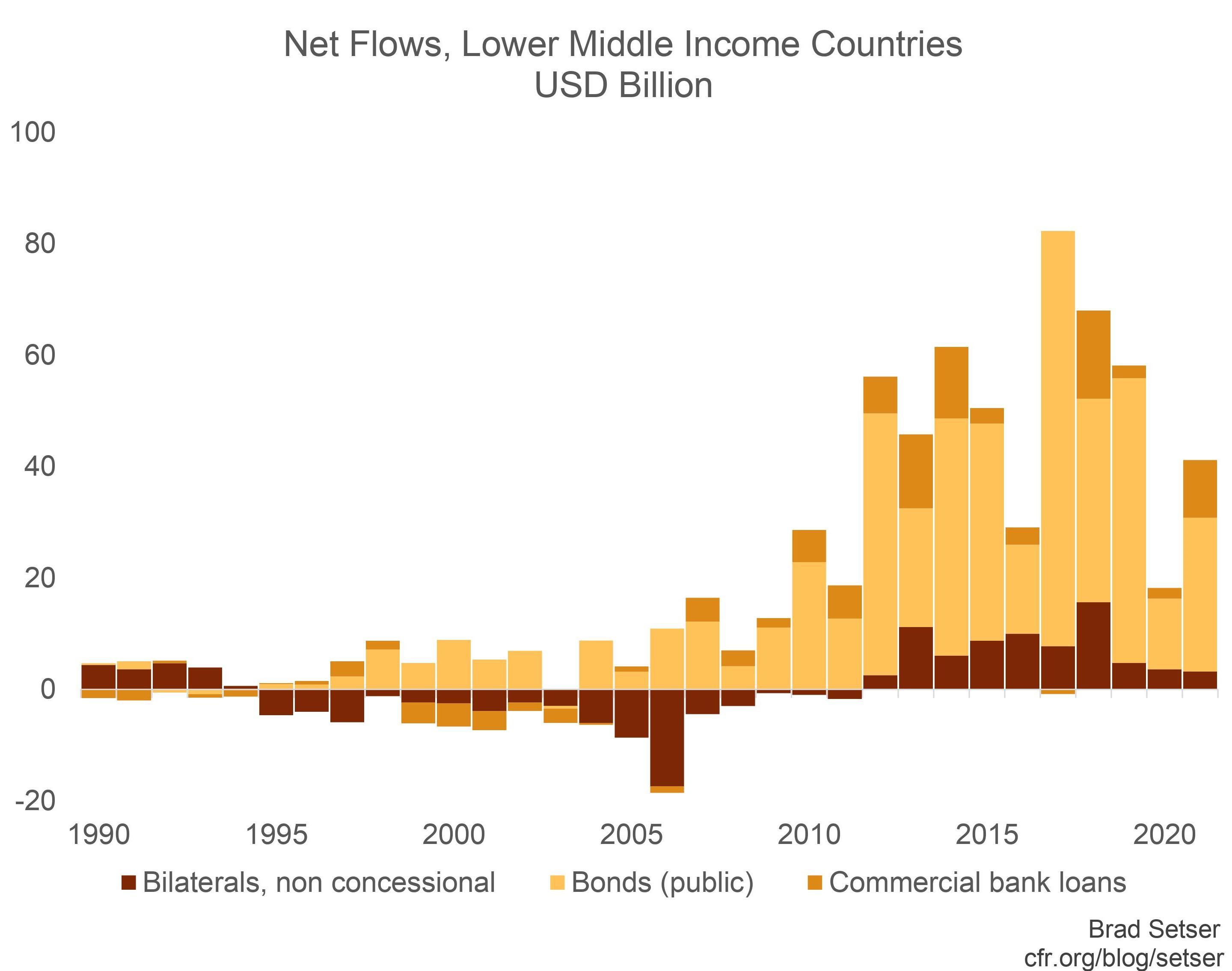

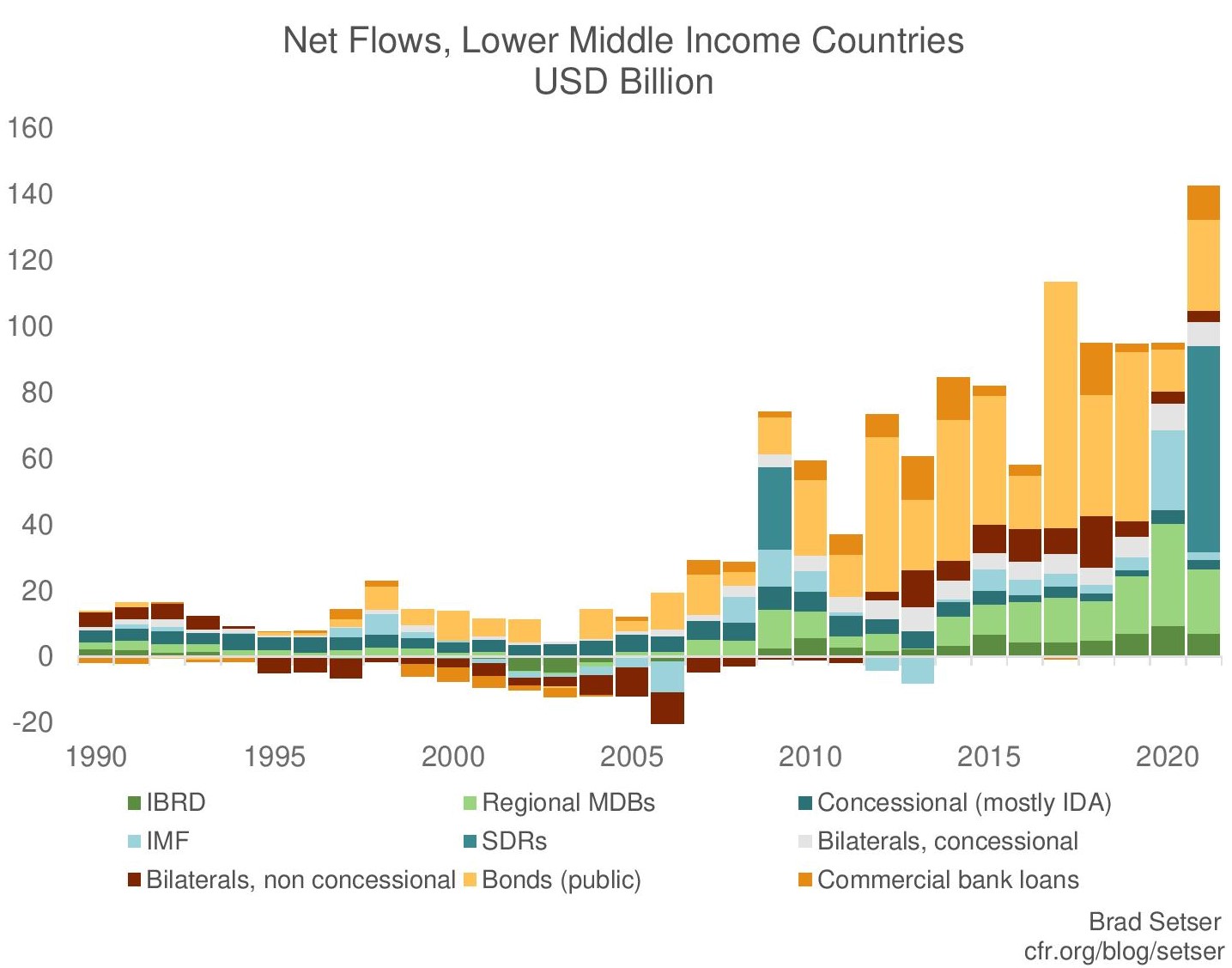

This surge in support for the IMF and the multilateral development banks is in some ways more apparent in the data for all lower middle-income countries around the globe than it is in the numbers for Africa alone. Private creditors (and Chinese policy lenders) pulled back. There was a bit of a recovery in 2021 when the bond market rallied, but that almost certainly reversed in 2022.

At the same time, the official sector stepped up and raised its overall lending. Perhaps more should have been done, but the multilateral system showed its value. Net financial flows remained positive in 2020 and 2021.

Countries retained access to financing thanks to the official sector. That is clear in a chart of aggregate debt levels, which continued to increase (in dollar terms) even as the composition of the debt stock shifted. There wasn’t a break in the trend linked to the pandemic.

But the World Bank and others cannot rest on their laurels. The world’s poorer countries now face two looming problems.

First, lot of funds extended in the last ten years were extended at floating rates, meaning the interest burden many poorer countries are facing on their legacy loans is rising quickly. Grace periods on many Chinese policy loans are also expiring (many Chinese loans have a five year grace period; see the Export-Import Bank of China’s loan to Kenya’s Standard Gauge Railway for a concrete example), so total debt service is also increasingly quickly.

Second, new inflows have dried up, and even credit worthy projects may struggle to get financing. Chinese policy lending has slowed down significantly. Commercial markets that reopened to many lower middle-income countries in 2021 closed in 2022, and more or less remain closed today. New financing isn’t really available for many countries, even when the underlying fundamentals allow a bit more debt.

The net result is a shortage of new financing to support an ongoing recovery—and particularly financing on financially sustainable terms.

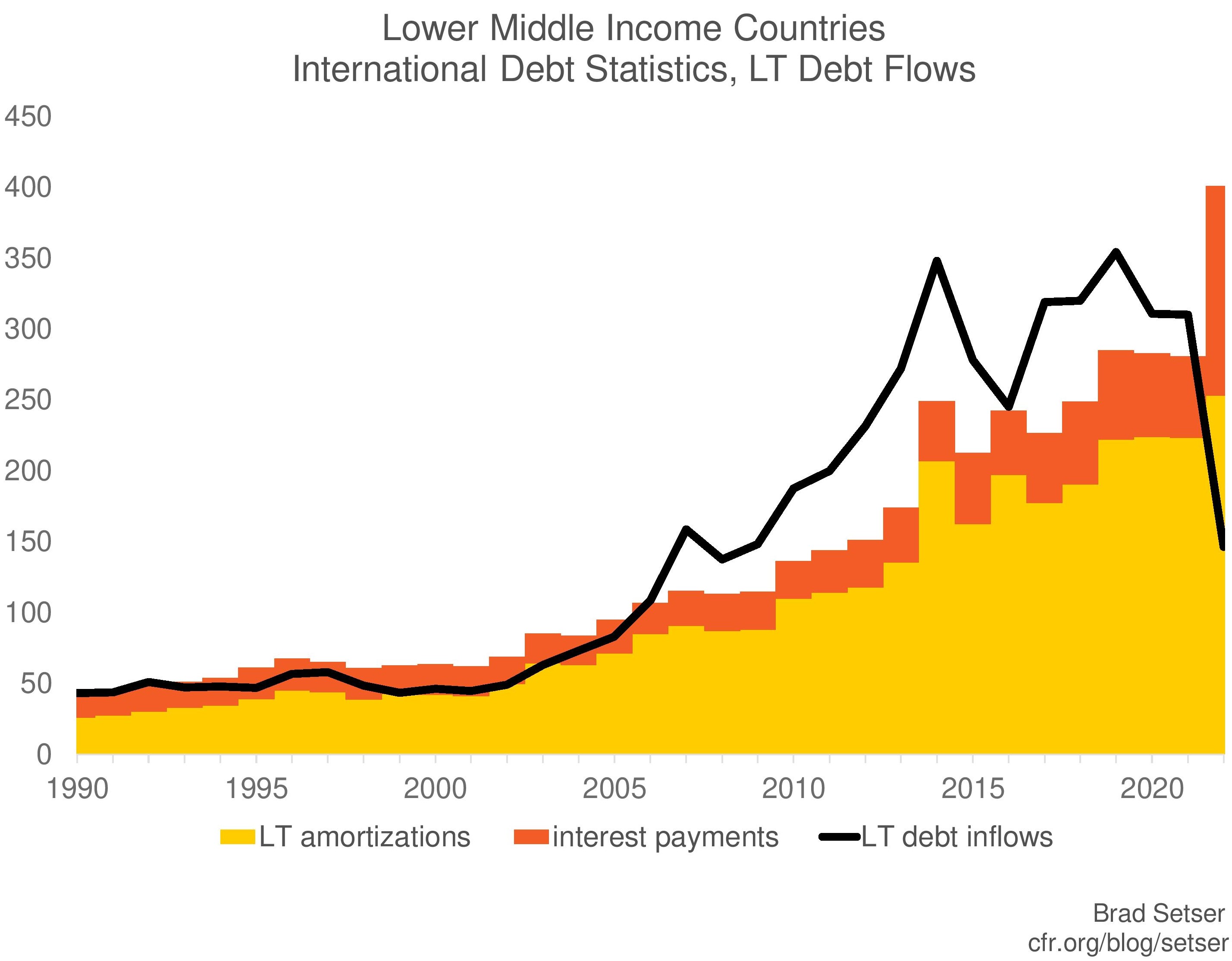

When the financial data for 2022 is tabulated (the World Bank’s International Debt Statistics are excellent, but come out with a long lag), low and lower middle income countries will, on net, be making large payments back to their commercial and Chinese creditors. Amortizations on long-term debt exceeded estimated new long-term lending in 2022, and the interest burden really ratcheted up.

For those countries that already have too much debt, a restructuring will be needed to limit net outflows and lower interest rates.

But there are also countries that can still borrow for the right projects provided the financing comes on reasonable financial terms. The multilateral development banks are critical here: without their support, many poorer countries will be starved of capital for years to come.

That is why expanding the scope of the World Bank’s lending should thus be an important part of the job of the new World Bank President. And it could be an opportunity to unite countries that otherwise compete. China and the United States actually have a common interest in assuring that the world’s low income economies have access to the financing they need to grow and develop.

*/ Full disclosure: Anna Gelpern and I were the project directors of the Group of Thirty report.