Cross-border Rx: Pharmaceutical Manufacturers and U.S. International Tax Policy

Brad Setser’s testimony to the United States Senate Committee on Finance addresses pharmaceutical manufacturers and U.S. international tax policy.

[Video: https://youtu.be/dcG3mP0sb3c]

I want to thank Chairman Wyden, Ranking Member Crapo, and the distinguished members of this committee for the opportunity to testify today.

Tax avoidance by American pharmaceutical companies is a very real problem.

It is also a very solvable problem. Straightforward changes to the U.S. tax code would encourage American and global pharmaceutical companies to produce more patent-protected pharmaceuticals in the United States, and to onshore rather than offshore their global profit.

America’s pharmaceutical companies clearly have a critical role to play in creating a more resilient American and world economy. They have been at the forefront of many of the world’s most important medical innovations – helped, in many cases, by research funded by the National Institute of Health and other government agencies. To cite the most prominent recent example, mRNA vaccines helped dramatically limit the loss of life associated with the COVID-19 pandemic.

Unfortunately, most of America’s leading pharmaceutical companies currently have structured their businesses to shift the profit from their U.S. sales to their offshore subsidiaries. As a part of these tax strategies, American pharmaceutical companies also have shifted production and jobs to other jurisdictions.

My testimony will be divided into three parts.

The first part will examine the incentives in the tax code that favor offshoring profits and production, to the detriment of the U.S. Treasury and the strength and resilience of the U.S. biopharmaceutical industrial base.

The second will review the empirical evidence of profit shifting in the pharmaceutical sector, drawing on both the data disclosed by the large listed pharmaceutical companies in their own annual reports and on the trade data.

The third will identify the reforms that I believe would substantially reduce the current incentive to offshore profits and jobs.

1. The U.S. tax code

For many years, the U.S. tax code combined a relatively high (35 percent) corporate tax rate with the ability to indefinitely defer profits that were technically the payment of tax on income earned outside the United States. Technical tax rules evolved over time so that it became relatively easy for a U.S. firm to transfer its intellectual property rights to one of its offshore subsidiaries without incurring a U.S. tax penalty, and then to shuffle those rights among its offshore subsidiaries to gain additional tax advantages.

The results of the incentives created by this tax structure were quite apparent. Several prominent U.S. firms – particularly firms in the technology and pharmaceutical sectors – paid relatively low effective tax rates and accumulated large offshore profits. Firms learned how to borrow onshore against their offshore profits to pay dividends and conduct buybacks onshore, but there was widespread agreement that the combination of global taxation and indefinite deferral generated perverse incentives that only advantaged offshore financial centers. By the end of 2016, analysts calculated that the deferred profits of U.S. firms had reached close to $2 trillion. That included at least $150 billion in accumulated offshore profits by the 8 largest U.S. pharmaceutical firms.

The 2017 Tax Cuts and Jobs Act changed the structure of the U.S. tax code without, unfortunately, changing the underlying incentive to move profits and jobs offshore to obtain a lower tax rate.

The Trump corporate tax cuts reduced the headline corporate tax rate from 35 percent to 21 percent. This new tax system was generally designed so that income earned in the United States would be taxed at the U.S. rate, and income earned abroad typically would not be subject to U.S. tax. In an inadequate attempt to put in place guardrails against abuse intrinsic to such an international tax system, the U.S. Congress created two special tax regimes – a 10.5 percent tax on some of the global profits of U.S. companies (the Global Intangible Low Tax Income or GILTI) and a special U.S. tax preference for export earnings above a 10 percent return on U.S. tangible assets. In technical terms, the result was a hybrid tax system – territorial in its concept, but with a low worldwide tax on foreign income that was taxed abroad at an exceptionally low rate.

By institutionalizing a large gap between the U.S. headline corporate tax rate and the low GILTI tax on U.S. firms’ global income, the new tax code generated strong incentives to continue to transfer profits and production abroad. The exemption of a deemed return on tangible assets located abroad from even the special 10.5 percent GILTI rate further encouraged firms to produce abroad, as increasing a firms’ foreign assets works to reduce its GILTI income and thus lower its global tax. Tangible assets located in the United States received no such special treatment. Dr. Kimberly Clausing has rightly called this an “America last” tax policy, as the reform structurally favored foreign income over domestic income. The last place an internationally mobile firm would want to book the global profit on its tangible assets is in the United States.

Five years have now passed since these reforms were enacted and the results are clear. A minority of firms, primarily technology firms that generate most of their revenues from the sale of advertising, repatriated the global right to make use of their intellectual property and simplified their tax structure. But the bulk of U.S. multinational firms have opted to maintain global businesses models designed to shift mobile income out of the United States into low tax jurisdictions.

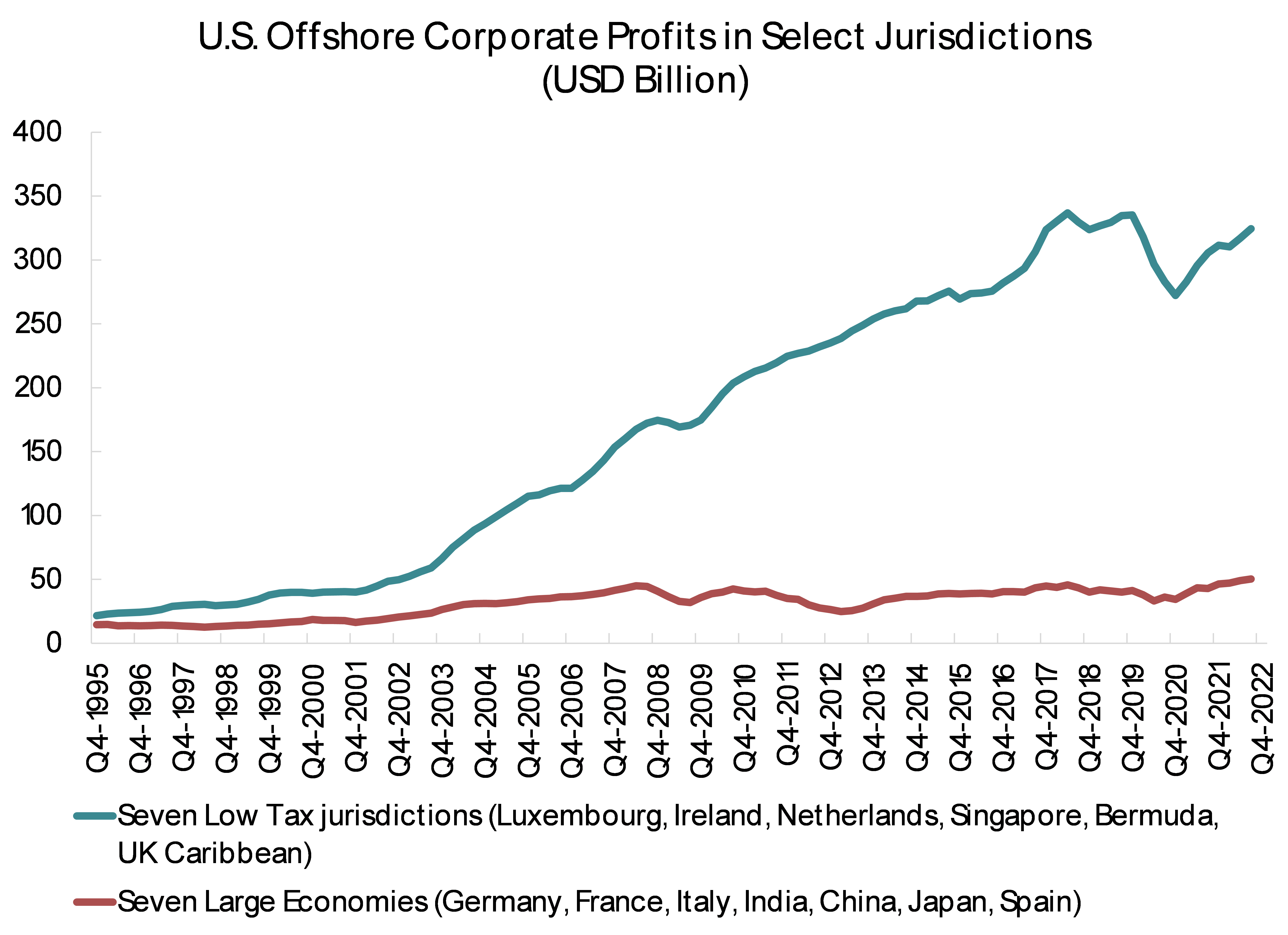

The U.S. balance of payments data provides clear evidence of the aggregate impact of these practices. U.S. multinational companies report earning $325 billion in seven low tax jurisdictions (Bermuda, the Caymans, Ireland, Luxembourg, the Netherlands, Singapore, and Switzerland) and only $50 billion in seven of the world’s largest economies (China, France, Germany, India, Italy, Japan, and Spain). The IRS data on firms’ country-by-country profits tells the same story – in 2019, the last available data point, American firms report earning far more profits in the Caymans than Canada and China combined.

2. The pharmaceutical sector in the tax and trade data

After the enactment of the Trump corporate tax cuts, American pharmaceutical companies in particular have doubled down on business models based on offshore production to shift profits on drugs sold in the U.S. market to their offshore subsidiaries. There are two independent sources of data that illuminate the extent of profit shifting in the pharmaceutical sector: the data that publicly listed U.S. firms disclose to their own investors as part of their SEC reporting requirements and the U.S. trade data.

SEC Disclosure

America’s pharmaceutical companies are known the world over for their innovativeness, but they increasingly do not produce their most significant products in the United States. Rather, they produce many of their most lucrative patent protected drugs outside the United States in order to facilitate the transfer of the profits generated from U.S. sales outside of the United States and to avoid reporting a U.S. profit on their global sales.

This is the clear pattern that emerges from a systemic examination of the 10-k annual financial reports of the main U.S. listed pharmaceutical companies. In these reports, companies generally detail the reasons why their actual tax rate differs from the 21 percent headline rate as well as disclose key risks, including risks to their current tax treatment.

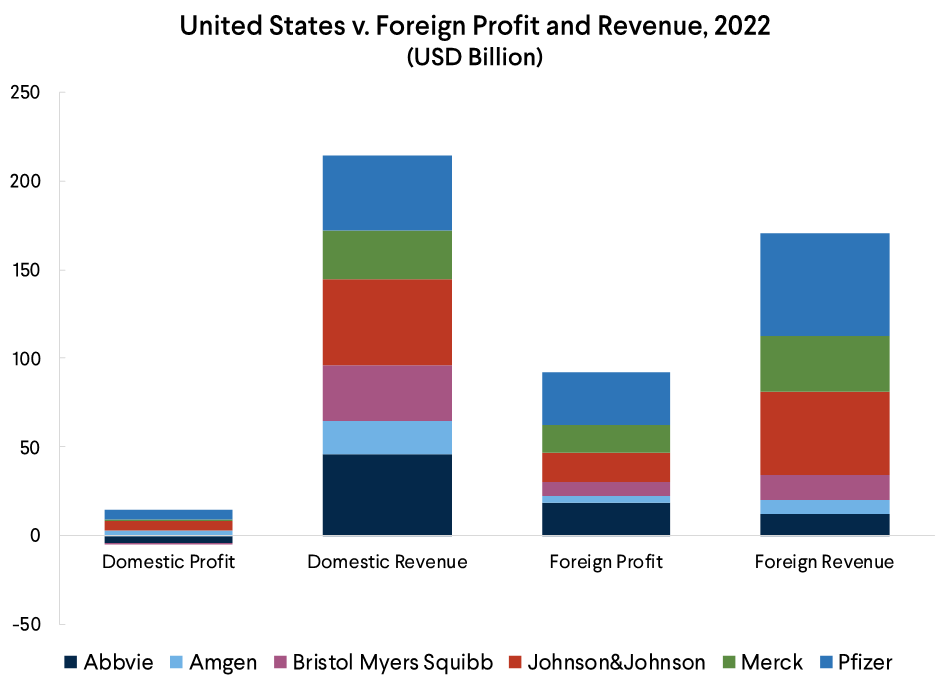

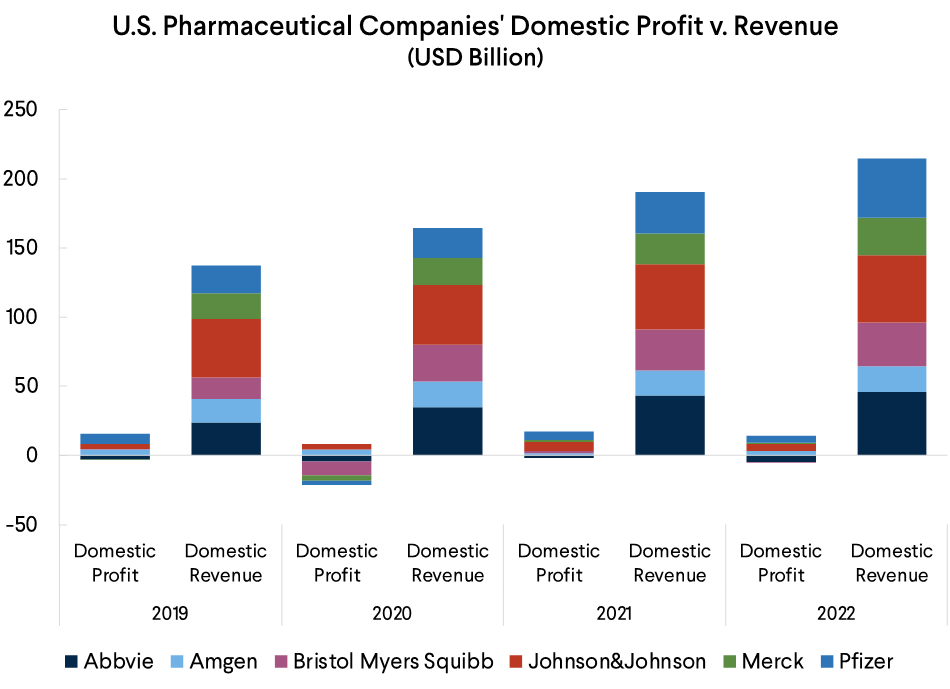

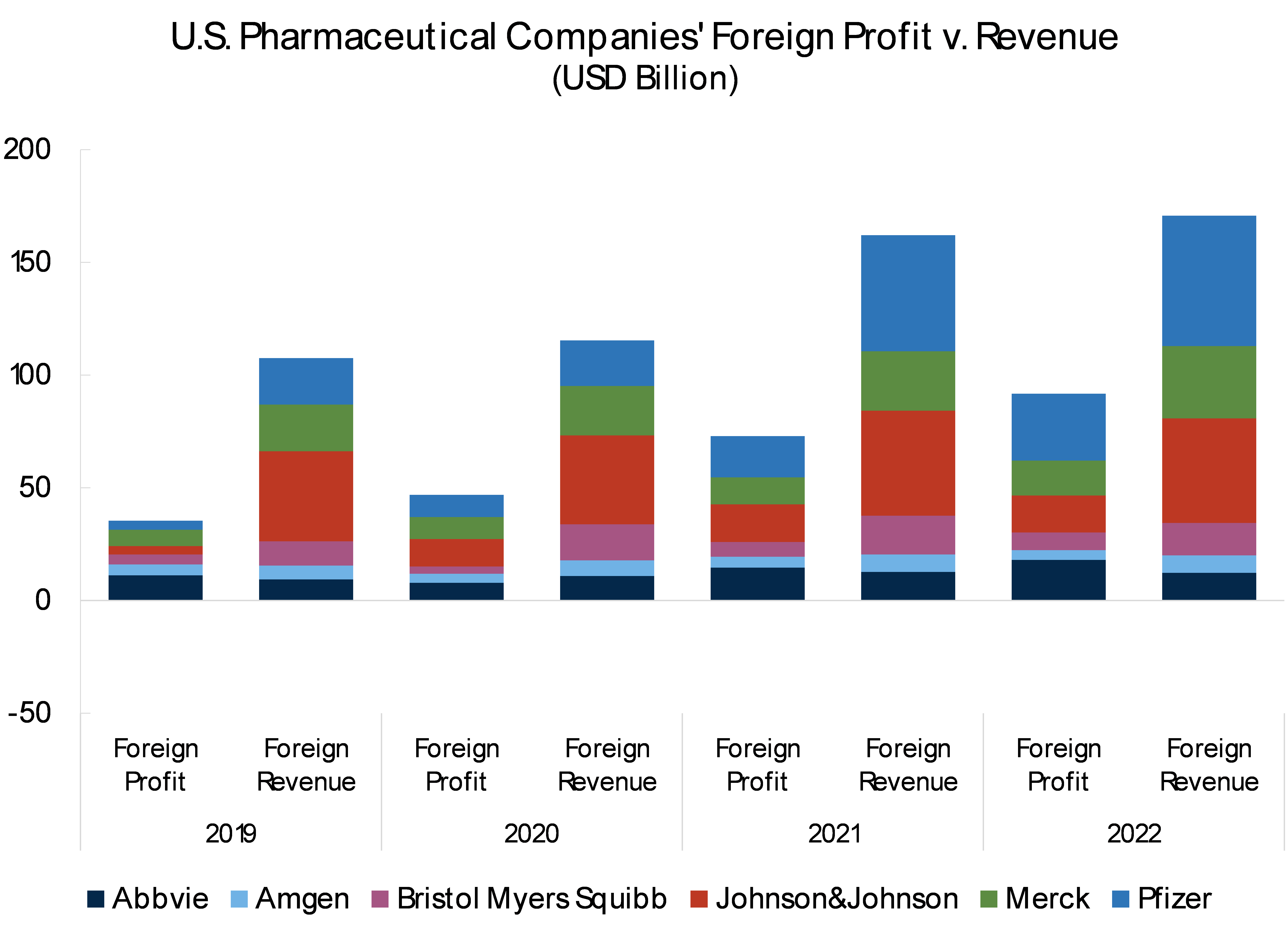

Excluding Gilead, whose reported data is incomplete but suggests that it now books the bulk of its global income in the United States, and Eli Lilly, whose data is also incomplete but unfortunately suggests it engages in significant profit shifting, the major U.S. listed pharmaceutical companies reported earning around $10 billion in U.S. profits on $214 billion of U.S. revenue in 2022. These firms also reported earning over $90 billion abroad – a quite significant fraction of their almost $171 billion in reported foreign revenue. Actual tax paid follows the reported profits: these U.S. firms reporting paying a bit over $2 billion in U.S. tax and close to $11 billion in tax abroad.

2022 was a particularly profitable year for many pharmaceutical companies. But the pattern of small U.S. profits relative to U.S. revenues – and a small U.S. share of global profits – has been consistent over time.

Over the same time frame, many large U.S. pharmaceutical companies have consistently reported sizable foreign profits relative to their foreign revenues.

Such a pattern is all the more striking because the United States is well known to have the highest pharmaceutical prices in the world. The cost of pharmaceutical production does not vary significantly from jurisdiction to jurisdiction, so the profit margin on high priced U.S. sales would normally be expected to be much higher than the margin on foreign sales. It consequently is particularly noticeable that the bulk of the American pharmaceutical industry appears to barely make any money on their U.S. operations, while reporting large profits in countries that more intensively regulate pharmaceutical pricing.

I want to highlight three companies in particular, based on their SEC disclosed tax structures over the last five years.

As Senator Wyden and his team have highlighted, AbbVie systematically transfers nearly all the profits on its patent protected medicines out of the United States. In fact, AbbVie reported a $4.6 billion loss in the United States in 2022 – and a near $20 billion offshore profit. The reported U.S. loss is not an aberration – AbbVie has reported a U.S. loss every year between 2013 and 2022. These domestic losses occur even though AbbVie reports that it generates 75 percent of its revenue in the United States, and its blockbuster drug Humira sells at a substantially higher price in the United States than in Europe.

Bristol Myers Squibb now displays the same pattern as AbbVie – it reported a U.S. loss of $0.14 billion while reporting nearly $8 billion in offshore earnings. It also reports that the United States generates nearly two-thirds of its revenues.

Pfizer also historically reported losses on its U.S. operations and large profits abroad. That pattern was attenuated by the success of its Covid-19 vaccine, which Pfizer produced in the United States for the United States and many other global markets. Nonetheless, there are indications that Pfizer continues to be among the firms that aggressively shift profits out of the United States. In 2022, Pfizer reported that it only generated $5 billion of its $35 billion global profit in the United States. That is a change from its $2.9 billion loss on its U.S. operations in 2020, its $4 billion loss in 2018 and its $6.9 billion loss in 2017 – but it is still a remarkably small profit on $42 billion in U.S. sales in 2022.

Such profit shifting strategies explain why many major listed U.S. pharmaceutical companies report effective tax rates close to ten percent. Merck’s 2022 10-k notes that tax differentials tied to foreign earnings lowered its effective tax rate by about 10 percentage points. To quote its annual report: “the foreign earnings tax rate differentials in the tax rate reconciliation above primarily reflect the impacts of operations in jurisdictions with different tax rates than the U.S., particularly Ireland and Switzerland, as well as Singapore and Puerto Rico.” Pfizer reports that lower taxation on its operations abroad lower its tax rate by about 5 percentage points; it observes “the reduction in our effective tax rate is a result of the jurisdictional location of earnings and is largely due to lower tax rates in certain jurisdictions, as well as manufacturing and other incentives for our subsidiaries in Singapore and, to a lesser extent, in Puerto Rico.” Reporting from the Irish journalist Thomas Hubert indicates that Pfizer should also have highlighted its Irish operations; Hubert’s investigation concluded: “what will not appear in the group’s consolidated accounts is the central role Ireland plays in the development, manufacture and distribution of its ground-breaking medicines around the world – as well as its finances and tax affairs.”

U.S. Trade Data

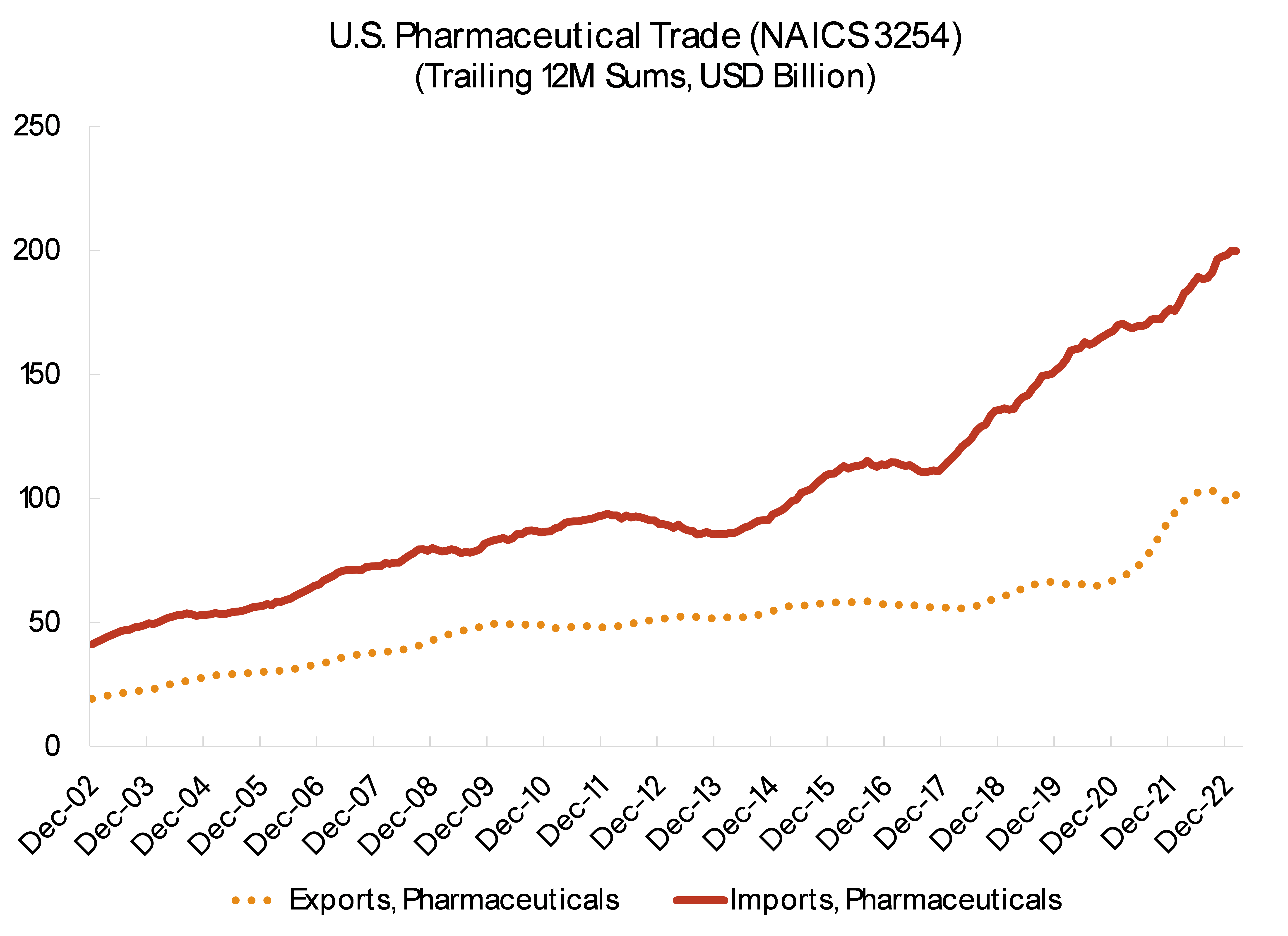

The story that emerges from a close reading of the SEC filings of American pharmaceutical companies is supported by the U.S. trade data.The United States now imports around $200 billion of pharmaceutical products (NAICS 3254) while exporting about $101 billion. If imports from Puerto Rico are included, imports would increase to over $230 billion (Puerto Rico, a U.S. territory, is inside the U.S. customs border but outside the United States for corporate income tax purposes).

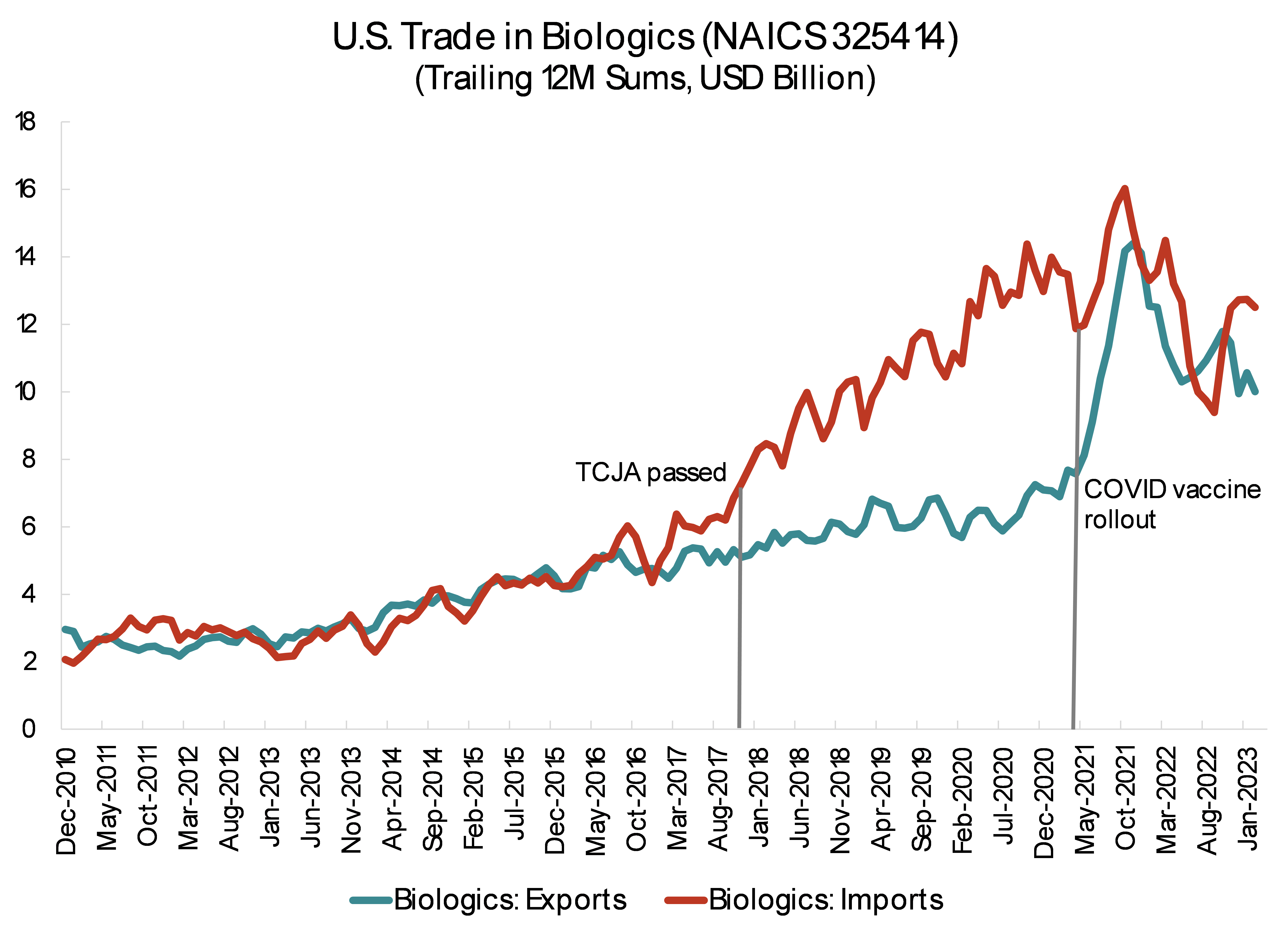

U.S. biopharmaceutical exports increased during the pandemic as a result of U.S. production of the COVID-19 vaccines, which were produced in the United States for the global market and have raised U.S. exports of “biologics (NAICS 325414)”.

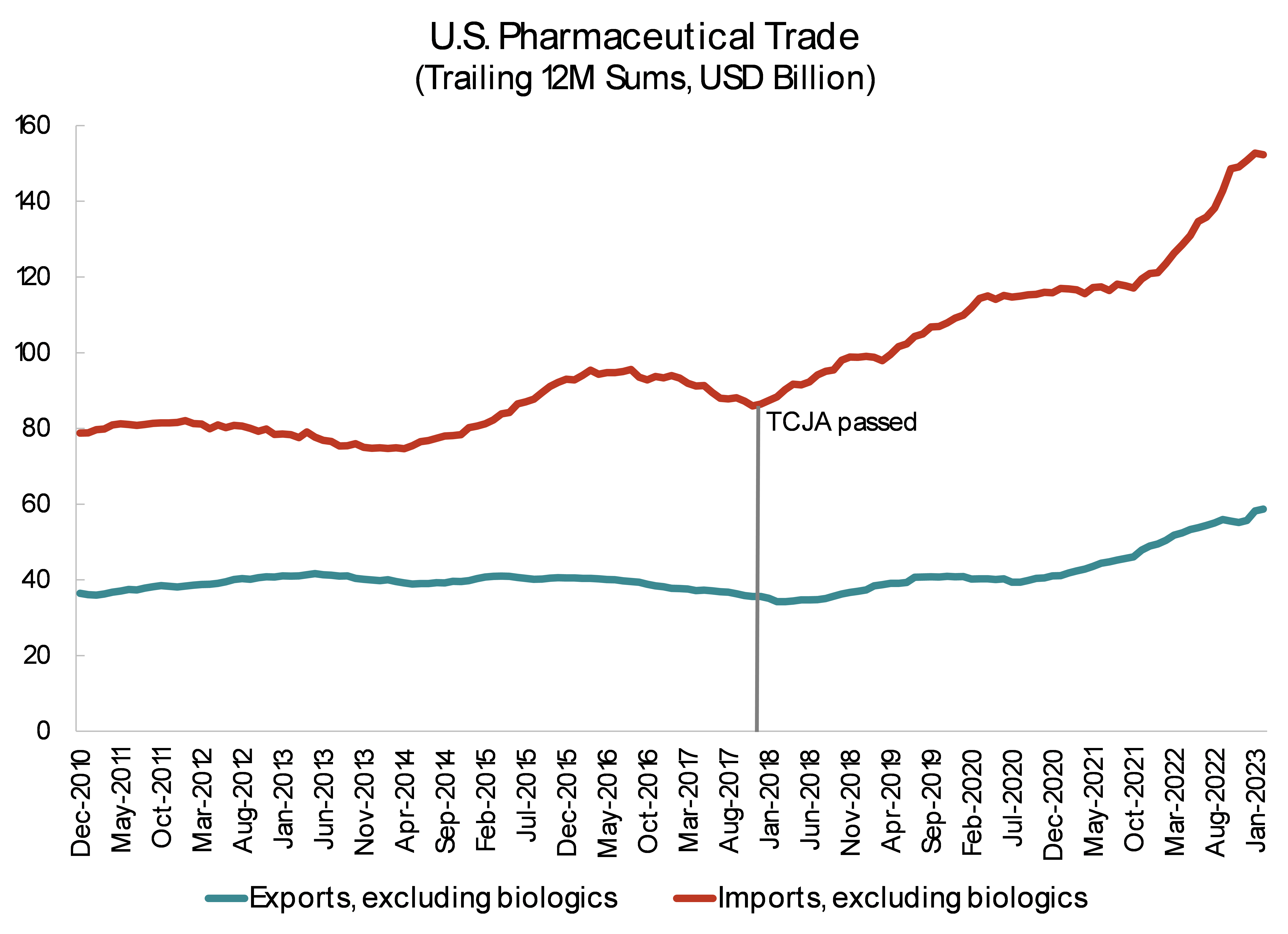

However, excluding the special case of vaccines, which were produced under U.S. government contracts that often required U.S. production, the U.S. trade deficit in pharmaceuticals has increased steadily after the passage of the Tax Cuts and Jobs Act. The United States now imports a bit over $150 billion of pharmaceutical products other than biologics, while exporting a bit under $60 billion – with imports almost doubling since the passage of the Trump corporate tax cuts.

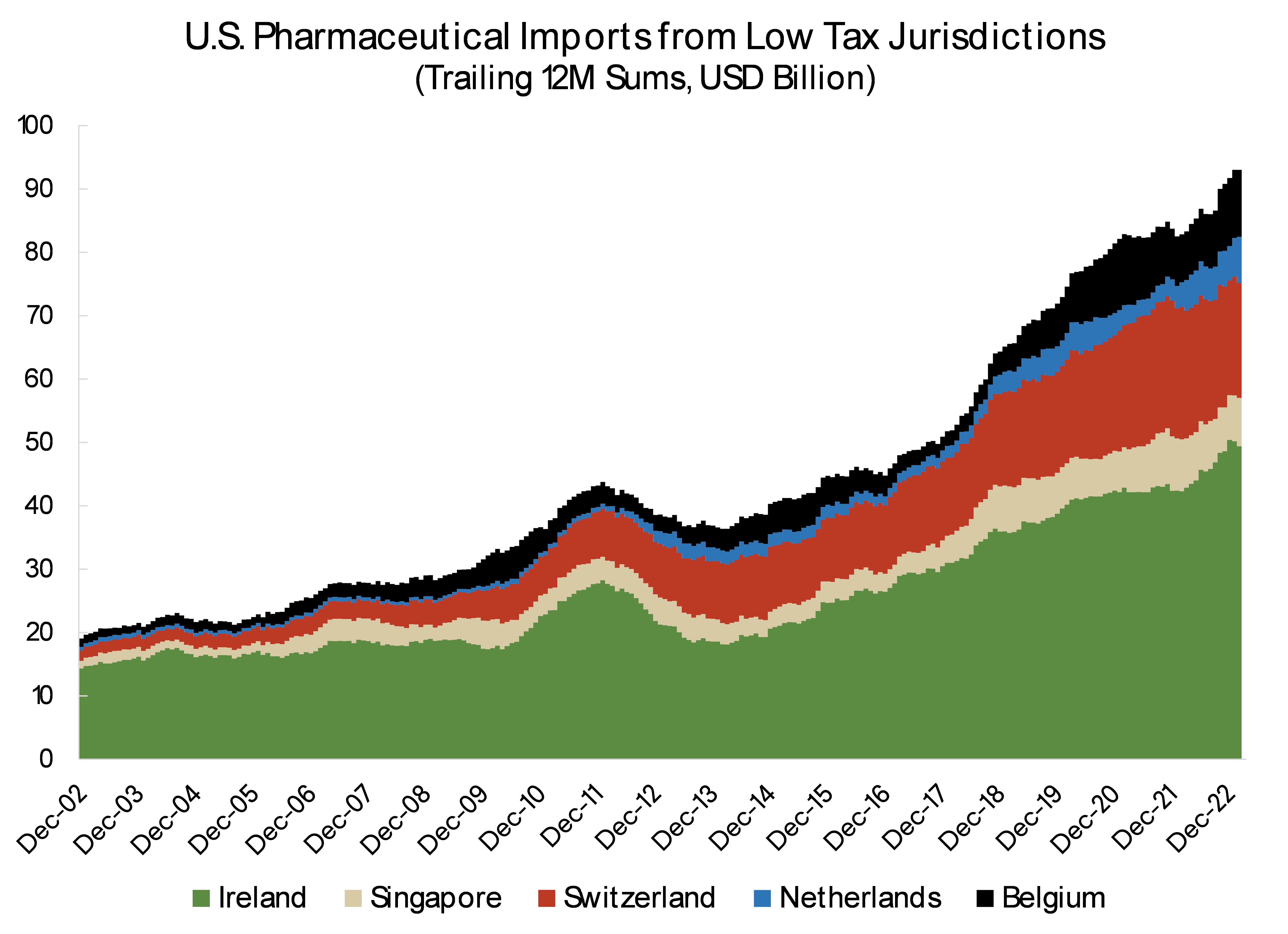

The trade deficit in pharmaceuticals is not primarily with low-wage and low-cost jurisdictions, as one might expect. Rather, the largest sources of imports are Ireland, Switzerland, and Singapore, with increasing imports from countries like Belgium – all of which offer special tax regimes for pharmaceutical companies.

The trade data maps to ongoing reports of U.S. firms increasing their offshore production. Merck has expanded its Irish production of Keytruda (Pembrolizumab), an important immunological treatment. Janssen Biotechnologies, a major subsidiary of Johnson & Johnson, is investing in Irish production capacity for Stelara (Ustekinumab), another blockbuster drug. Eli Lilly has announced a $1 billion new investment in its Irish production facility, reportedly to produce a new Alzheimer’s drug, among others. Pfizer has also reported a $1.3 billion investment in biologic production capacity in Ireland.

In my judgment, there is no plausible explanation for the current scale of U.S. imports of pharmaceuticals from Belgium, Ireland, Switzerland, and Singapore that isn’t tied to tax avoidance. The net result is a loss of tax revenue for the U.S. Treasury and a smaller biopharmaceutical industrial base. This clearly leads to a less resilient U.S. economy. The pandemic showed that a diverse advanced manufacturing base and a technically skilled workforce can be vital assets in rapidly scaling up production of innovative medicines in the face of an unexpected shock.

3. Necessary reforms

Significant changes to the current U.S. tax code are needed to remove the current incentive for pharmaceutical firms, and other high margin manufacturing firms, to shift jobs and profits out of the United States.

The starting point for any reform is straightforward: the U.S. Congress should increase the tax rate that U.S. firms now face on their global intangible income, and thus assure that firms that engage in tax games to shift profit outside the United States nonetheless pay a U.S. tax rate of at least 15 percent. In addition to raising the baseline GILTI rate to at least 15 percent, Congress should assess this tax on a country-by-country basis. Right now, firms that pay zero tax on their profits in say, Bermuda, or perhaps 5 percent in Ireland, can actually lower their overall tax rate by blending those profits with profits in high tax jurisdictions like Germany (a perverse outcome). Such changes on their own would clearly raise a meaningful amount of revenue, given the low effective tax rates that firms report in their SEC disclosures and the large reductions in tax that firms disclose as a result of “the jurisdictional mix earnings”. In addition, careful consideration should be given to deeming patent boxes to be in a separate foreign tax bracket for the purpose of calculating a firms GILTI income and tax liability. Such patent boxes currently create strong incentives to shift profits into what would otherwise be relatively high tax jurisdictions, such as Belgium.

There is little downside to an increase in the U.S. global minimum tax. Thanks to the leadership of Secretary Yellen and others, America’s main trading partners have already committed to a 15 percent global minimum tax. Consequently, the United States should immediately enact the changes in U.S. tax law required to implement – or at least converge with – the second pillar of the OECD-G-20 Inclusive Framework. Without U.S. action, other countries will rightly be able to collect top-up taxes on under-taxed U.S. firms that operate in their jurisdictions and continue to systematically shift profits to low-tax jurisdictions. U.S. firms that have retained their intellectual property in the United States and pay U.S. tax on the associated royalty income by contrast will face much less of a risk of being subject to a top-up tax.

Moreover, the United States should increase its tax collection from the pharmaceutical industry by enacting the first pillar of the OECD- G-20 Inclusive Framework. Pillar One shifts a portion of the tax a firm owes on its global income to the “market” jurisdiction – essentially the jurisdiction of sales. Foreign pharmaceutical firms that generate large profits on their U.S. sales would thus be required to make a payment to the U.S. Treasury. Pillar One would also raise U.S. tax revenues from U.S. pharmaceutical and medical technology firms that “inverted” and became Irish headquartered companies, even though the bulk of the firms’ operations and sales are in the United States. Even U.S. headquartered pharmaceutical firms could, absent changes in their tax structure, potentially be required to make additional payments to the United States, as many currently generate the majority of their sales inside the United States while booking the majority of their profits abroad. Aligning a portion of the taxing rights to these firms’ global income to the jurisdiction of sales thus would imply greater, not smaller, payments to the U.S. Treasury.

In addition to these reforms, most of which have been proposed by the U.S. Treasury, I would recommend a set of additional hard-hitting reforms to discourage firms from shifting profits earned in the United States outside of the United States. A higher minimum U.S. tax on the offshore income of U.S. firms reduces, but does not fully eliminate, the incentive to offshore future profits.

Specifically, the U.S. Congress should consider a set of reforms to reinvigorate subpart F of the corporate tax code. Subpart F dates back to the 1960s. It was originally introduced to the tax code to discourage U.S. firms from locating the passive profits and income from certain related party transactions, including sales and services income, abroad. Today many firms locate production as well as their intellectual property rights abroad, but the basic principle that firms should not gain a tax advantage by shifting profits outside of the United States remains important. Over time, though, subpart F has been effectively gutted, and it is relatively easy to find ways around its basic requirement that passive income and income from certain related party transactions be taxed in the United States at the headline U.S. corporate income tax.

No doubt there are many specific changes that would strengthen subpart F. I will highlight three. One, foreign royalty income should be denied any exemption from subpart F, and thus taxed at the U.S. rate. To be concrete, this would raise the tax rate on the intellectual property that pharmaceutical firms, like AbbVie, have located in Bermuda and other no or low tax jurisdictions. Two, legacy “cost-shares” that allow firms to shift profits out of the United States by splitting the cost of research and development between the U.S. headquarters and a foreign subsidiary of the same firm located in a low-cost jurisdiction should lose their current special tax status. Three, transactions between foreign subsidiaries of the same firm that generate a substantial increase in the valuation of offshored intellectual property for the purpose of generating larger depreciation allowances in jurisdictions like Ireland could be subject to U.S. tax at the headline rate. To give a concrete example here, it has been widely reported that Apple’s subsidiary in the isle of Jersey was bought by Apple’s Irish subsidiary. This transaction was designed to generate large depreciation allowances for Apple’s Irish subsidiary and thus to substantially lower Apple’s effective Irish tax rate without incurring any U.S. tax liability. Under this proposal, the paper profits that Apple’s Jersey subsidiary earned from the sale of the global rights to Apple’s intellectual property to Apple Ireland would be taxed at the headline U.S. rate.

The intent of all these proposals is to discourage U.S. firms from transferring the right to profit from the intellectual property that they generate in the United States to low-tax jurisdictions, and thus to create strong incentives for U.S. firms to retain their intellectual property onshore. It would have the byproduct of substantially reducing tax incentives to offshore production and jobs, as the bulk of the profit on offshore production accrues to the intellectual property and the goal of many offshoring strategies used in the pharmaceutical sector appears to be to create the legal basis for moving the profit on U.S. sales out of the United States. As I noted earlier, in 2022, the large American pharmaceutical firms reported earning remarkably little – $10 billion – on their $200 billion in U.S. sales. Their reported earning on their foreign operations were equally remarkable: $90 billion on $170 billion in sales, an implied margin of over 50 percent. These firms appear to have paid about $2 billion in tax to the U.S. Treasury on global earnings of over $100 billion, a remarkably small sum.

Such reforms would both raise the overall amount paid to the U.S. Treasury and increase the effective tax rate paid by U.S. pharmaceuticals. Many foreign pharmaceutical firms already pay effective tax rates of around 20 percent, or close to the headline rate in their country of origin. Denmark’s Novo Nordisk is currently taxed at Denmark’s headline tax rate and pays the bulk of its income tax in Denmark. France’s Sanofi also pays and effective rate of close to twenty percent. Even the Swiss firm Novartis pays an effective tax of close to 15 percent. These firms also tend to pay the bulk of their corporate income tax in their “home” country. The United States now stands out by allowing many of its major companies to achieve effective tax rates of 10 percent by moving both production and profits out of the United States – a giveaway to the shareholders of the pharmaceutical companies that comes at substantial cost to both the U.S. Treasury and the U.S. economy.

In the context of a significant tightening of subpart F, I would also support reinstating full expensing for Research and Development expenditures, structured to be effective in the context of Pillar two of the OECD’s global tax reform. Generous tax treatment for genuine innovation though should be combined with new rules that would claw back expensing for Research and Development if a firm moves its intellectual property to one of its foreign subsidiaries. Such a rule would be technically challenging, but I am confident that it is feasible.

Conclusion

The United States generates the bulk of the revenue for American pharmaceutical companies, largely because Americans pay the world’s highest prices for essential medicines. Yet American companies typically report that they earn, at least for tax purposes, almost all of their profits abroad.

The information that American pharmaceutical companies report to their own investors provides strong evidence of systemic tax avoidance. In 2022, the United Stated accounted for 55 percent of the sales of a select group of large pharmaceutical companies, but only 10 percent of their profits. The most recent round of U.S. corporate investment in Irish pharmaceutical production highlights how the Tax Cut and Jobs Act only reinforced prior incentives to offshore both production and profits. I unfortunately do not think it is unfair to call the Tax Cuts and Jobs Act the Pharmaceutical Tax Cuts and Irish Jobs Act.

There consequently is an urgent need to reform the U.S. corporate tax code to both to assure that some of America’s most profitable companies pay their fair share to the U.S. Treasury and to strengthen the U.S. biopharmaceutical industrial base. The incentives to offshore the production of some of the world’s most important medicines in the current U.S. tax code are in my view an issue of supply chain security and thus ultimately of national security.

I applaud the Finance Committee for calling this hearing and encourage the Senate to move quickly to make necessary changes in the U.S. tax code.