China Bought Foreign Exchange in September (Just Not Very Much)

Analysis of the September intervention proxies for China and q2 Chinese balance of payments data.

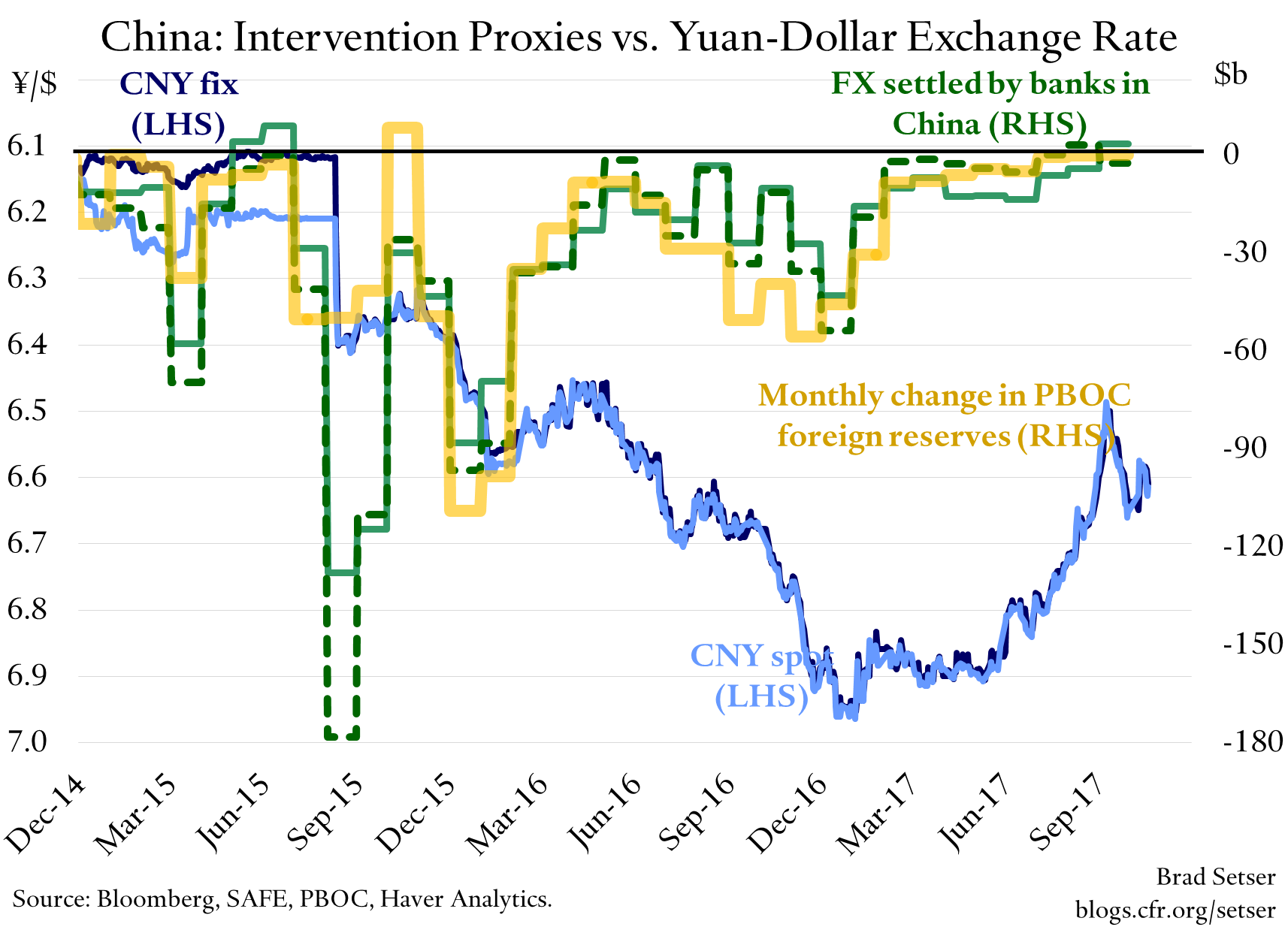

China, it seems, is now a buyer not a seller in the foreign exchange market.

There is no need to get carried away though: China looks to have—per the foreign exchange settlement data, and the change in the PBOC’s balance sheet—bought about a billion dollars in September. That’s nothing for an economy of China’s size.

But the story—told in the Treasury’s latest foreign exchange report, among other place—that China is intervening to prop its currency up rather than hold it down is now a bit dated.

From the PBOC’s point of view, life has rarely been better, at least on the foreign exchange management side—flows in and out are in rough balance (in part because both inflows and outflows are managed), and the exchange rate has been broadly stable without much intervention.

The monthly change in the PBOC’s reported balance sheet reserves has been less than a billion for each of the last three months. The only previous period of comparable stability came in late 2014.

There even has been a bit more volatility in the exchange rate recently (using the eyeball test)—though no one seems to think the yuan will be allowed to stray too far from its current level against the basket.

It isn’t obvious to me that it is in China’s interest to rock the boat with a major exchange rate reform right now: the PBOC isn’t running through its reserves, it isn’t buying a lot of reserves and thus risking catching the Treasury’s attention, and the yuan is at a level that doesn’t seem to be generating any obvious pressure from either exporters or importers.

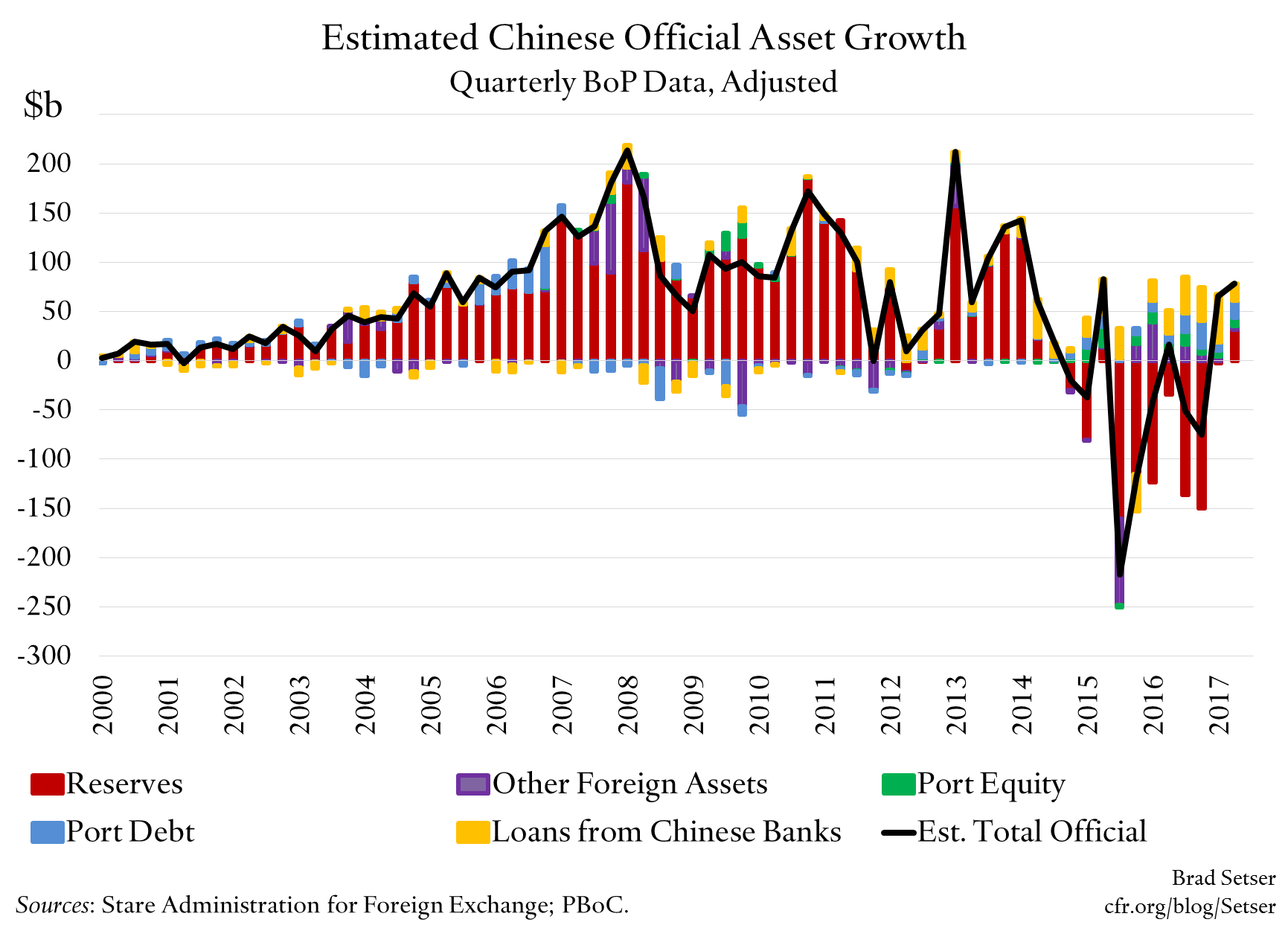

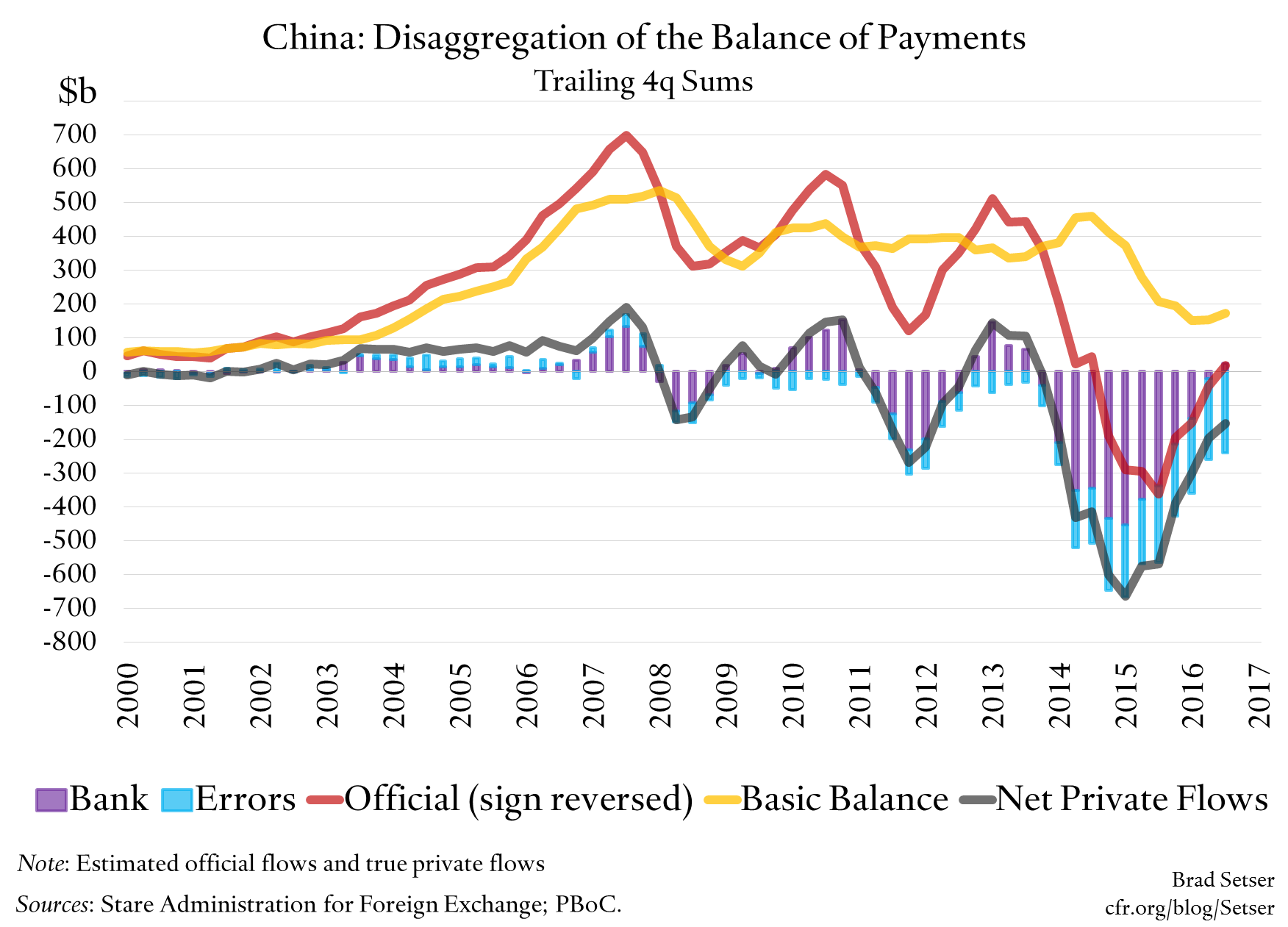

Reserve growth, as reported in the balance of payments (BoP), has actually been a bit stronger than implied by the change in the reserves on the central bank’s yuan balance sheet (one possible explanation is that balance of payments reserve flows include interest income, but that is just a guess).

In q2, the PBOC balance sheet reserves showed almost $15 billion in sales, but the BoP showed a rise in reserves of around $30 billion. If that pattern holds in q3, China likely added about $40 billion to its reserves in q3 on a flow basis, given the PBOC’s balance sheet reserves were essentially unchanged in the third quarter.

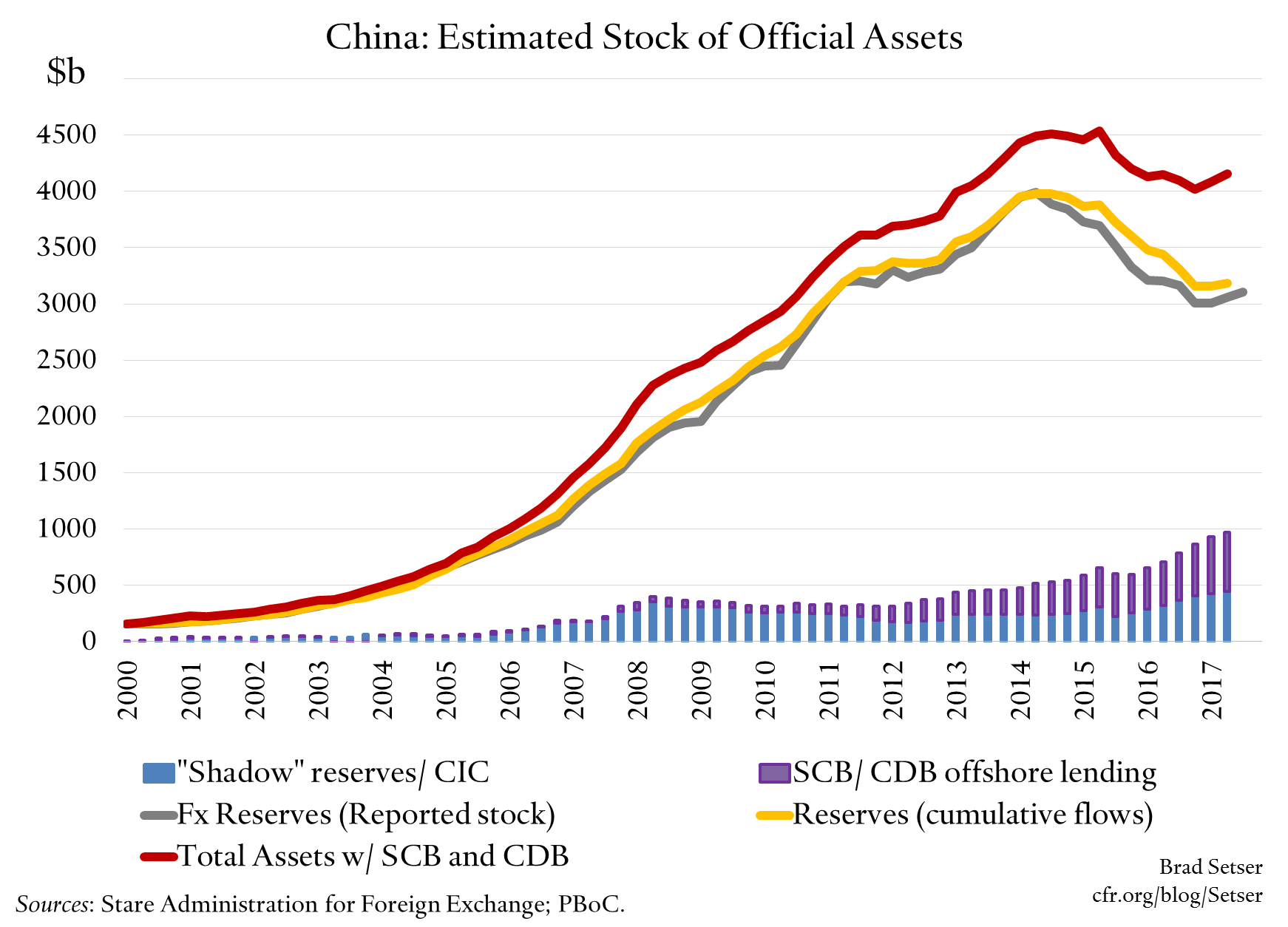

My broad measure of the growth in China’s official (e.g. government-controlled) foreign assets—a measure that counts the assets of the China Investment Corporation (CIC) and longer term loans from the state banking system alongside reserves*—showed a jump of about $75 billion in both q1 and q2, and likely will show a similar rise in q3. I think my broader measure catches some important aspects of the balance payments—it was designed to capture the ways in which China hid its intervention in the past. But it comes out with a lag: it is only possible to calculate when the detailed balance of payments data is released at the end of the quarter.

So generally speaking, based on the detailed data from the first half of the year and partial data from the third quarter, I think China’s state is on track to add something like $200 billion to its external portfolio this year—counting the Belt and Road lending as well as the reserve flows in the balance of payments.

So what accounts for the swing from the sale of foreign assets in 2016 to purchases in 2017?

- The yuan’s story is also in some sense a dollar story. There is a natural tendency to think that capital outflows from China are a function of what is happening inside China. But large outflows started when the dollar strengthened in late 2014. And those outflows subsided when the dollar weakened this year. When the dollar is too strong for the U.S. (or at least U.S. exporters), the market—which for China is primarily the Chinese firms and banks able to arbitrage the border—starts to think it is too strong for China too, and starts to expect a depreciation.

- The rebound in China’s economy has allowed the PBOC to keep the repo rate (one is de facto policy rates) above the Federal Reserve’s policy rate, making it costly to bet against the yuan. China’s economic cycle (and policy cycle) is no longer at odds with that of the United States: both the Fed and the PBOC are looking to tighten (modestly) this year.

- The controls on FDI “worked.” FDI outflows were running at $60 billion a quarter (well over $200 billion annualized) in 2016. They have fallen to about $20 billion a quarter this year. Clamping down on Anbang and HNA and the like has had a material impact.

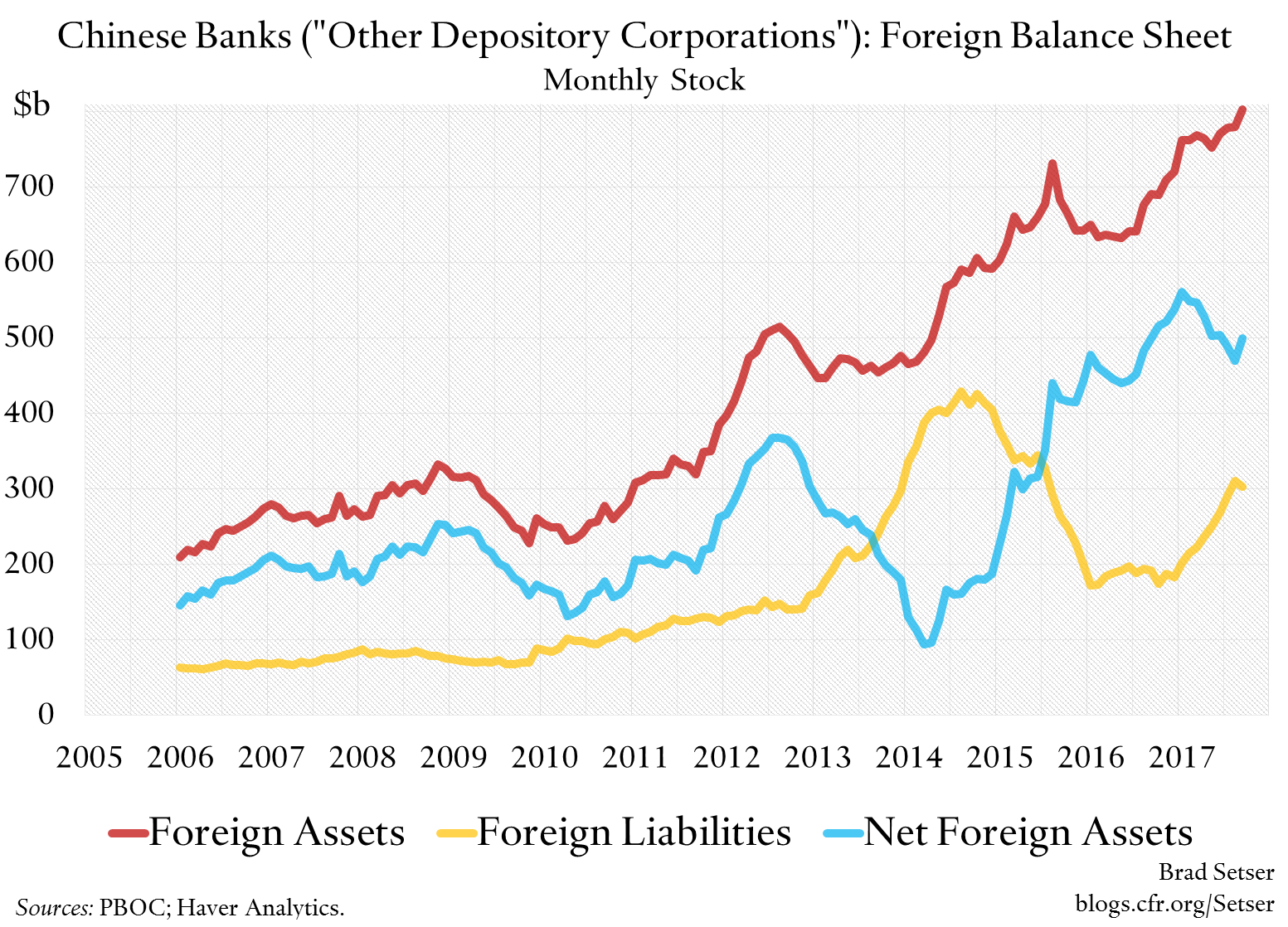

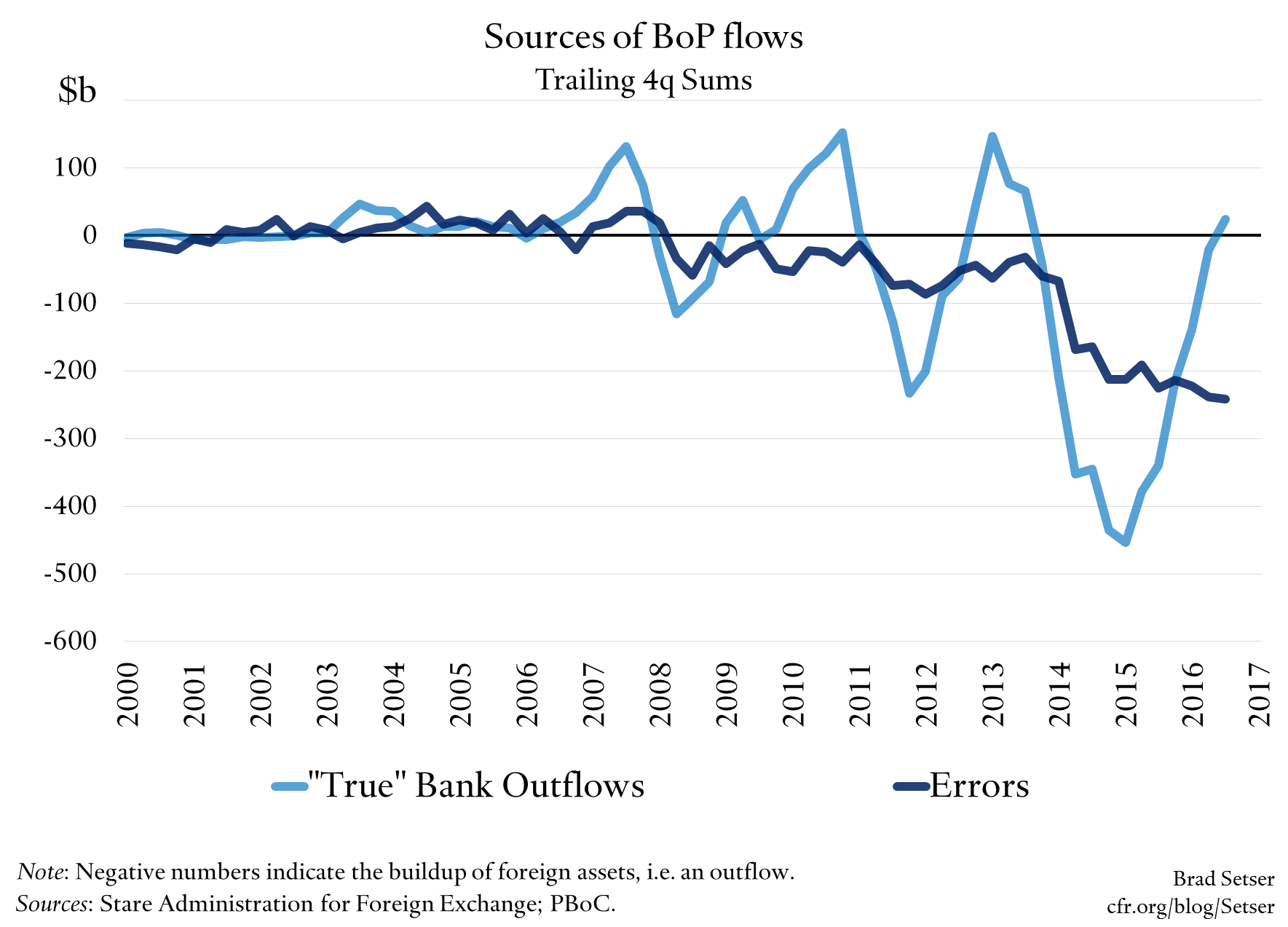

- Outflows through the banking system have fallen significantly. Chinese banks that borrowed from abroad to take advantage of the carry trade paid down those loans—and once the loans were paid down, there was less pressure on the balance of payments. And recently there has been a new influx of offshore deposits into the Chinese banking system. Deposit inflows were close to $50 billion a quarter in the first two quarters of 2015.

- There has been a subtle change in how the ongoing growth in the foreign loan book (and foreign securities book) of the state banks has been financed. In 2016, the state banks‘ offshore loan growth was effectively financed by the PBOC, through a fall in reserves. The banks net foreign asset position was rising even as the central banks’ net foreign asset position was falling. In 2017, the state banks foreign asset growth has been matched by a comparable increase in their foreign liabilities—their net assets aren’t growing, and they are bringing in as much foreign exchange (it seems) as they are using. This of course is related to the fall-off in net banking outflows.**

Over the last four quarters of data, my broad measure of intervention is now flat—purchases in 2017 offset sales in the last half of 2016. And banking outflows have also fallen to zero, after adjusting for state banks’ long-term external lending.

There though is still one source of concern in the balance of payments: recorded errors and omissions remain high, around 2 percent of GDP. And there is likely another hidden outflow of about 1 percent of GDP in the tourism deficit (see Anna Wong). But for now, the outflow from Chinese residents who have found creative ways around China’s controls is roughly equal to the goods trade surplus (it likely will be a bit smaller than the goods surplus for the full year).

And the result of that happy coincidence is next to no intervention.

* My broad measure of official asset growth includes the following balance of payments categories: portfolio debt, assets; portfolio equity, assets; other assets, loans; and other assets, other. Portfolio debt and portfolio equity in theory include private outflows, but in practice portfolio debt outflows seem to come primarily from the state banking system and portfolio equity outflows come primarily from the CIC. “Other, loans” includes loans made by the China Development Bank (CDB) and China Exim. It is the category that has been growing rapidly recently. “Other assets, other” corresponds to the other foreign assets reported on the PBOC’s balance sheet: it is primarily the portion of the banks required regulatory reserves that is held in foreign exchange. Historically this has been used to hide some of China’s intervention—both on the way up and on the way down. When China provides a more detailed breakdown of its portfolio outflows that splits out the foreign assets of private and state actors, I will modify my methodology. Right now it likely slightly overcounts Chinese official outflows. All these outflows though are clearly under the de facto control of China’s authorities—they can be dialed up or dialed down as needed.

** My adjustment for official assets counts the rise in state banks’ loans on the asset side, but not changes in the “loans” line of liability side. There is a case that I should look at “net” loans, which would change the number significantly. The problem with including loans on the liability side is that this catches a bit too much of the carry trade related inflows during past periods of yuan strength. For now though my measure of official asset growth is a “gross” number.