Can China Finance One Belt One Road Without Jeopardizing Its Own Financial Stability?

The answer, I think, is yes. Even after Moody’s downgrade. At least so long as China’s ambitions for scaling up what seems to have been a roughly a $15 billion-a-year financing program are reasonable.

I still remember a time not so long ago when China was adding $500 billion a year to its reserves and shadow reserves and was channeling $300 or more billion a year into the U.S., mostly by buying bonds (Not selling reserves and selling U.S. assets, as it did in 2016. The swing from 2013 to 2015-2016 was large). I still have a great deal of respect for the raw financing capacity of China’s state. China saves a ton, the raw material for a large current account surplus is still there—see Martin Wolf

Estimates of the cost of One Belt and One Road vary—in part because the initiative’s scope is relatively elastic (is Yamal LNG part of OBOR? Chinese investment in Swiss seed companies? Chinese investment in Sudan and Angola?). But a common estimate is around $1 trillion (some have higher numbers, but the top end of the range seems implausible to me).

Not all of that necessarily will be borne by China. Bradsher and Perlez of the New York Times report that China’s actual commitment at the summit in Beijing was around $120 billion—on top of $50 billion that already has been disbursed (over four years). Add in China’s commitment of paid-in ($10 billion) and callable capital ($40 billion) to the Asian Infrastructure and Investment Bank and its commitment to the New Development Bank ($10 billion) if you want. And there may be investments from state firms that aren’t funded by the New Silk Road Fund or the development banks. That brings China’s existing commitments up to around $200 billion.

If that is right, the balance will either be financed by other sources (including banks in the countries hosting the projects), or simply not done — at least not in the next five years.

I certainly would worry (very much) if China ever committed so much foreign exchange to financing the Belt and Road that it found itself short on reserves. China still has plenty of reserves in my view, but not so many that can completely ignore potential risks.

But I also suspect $200 billion over five years—a sum in line with China’s reported actual financial commitment, though not with common estimates of the overall size of the program — is something that China can manage fairly comfortably. Why? Simple: it is in line with the state banks recent pace of external lending, and consistent with China’s balance of payments.

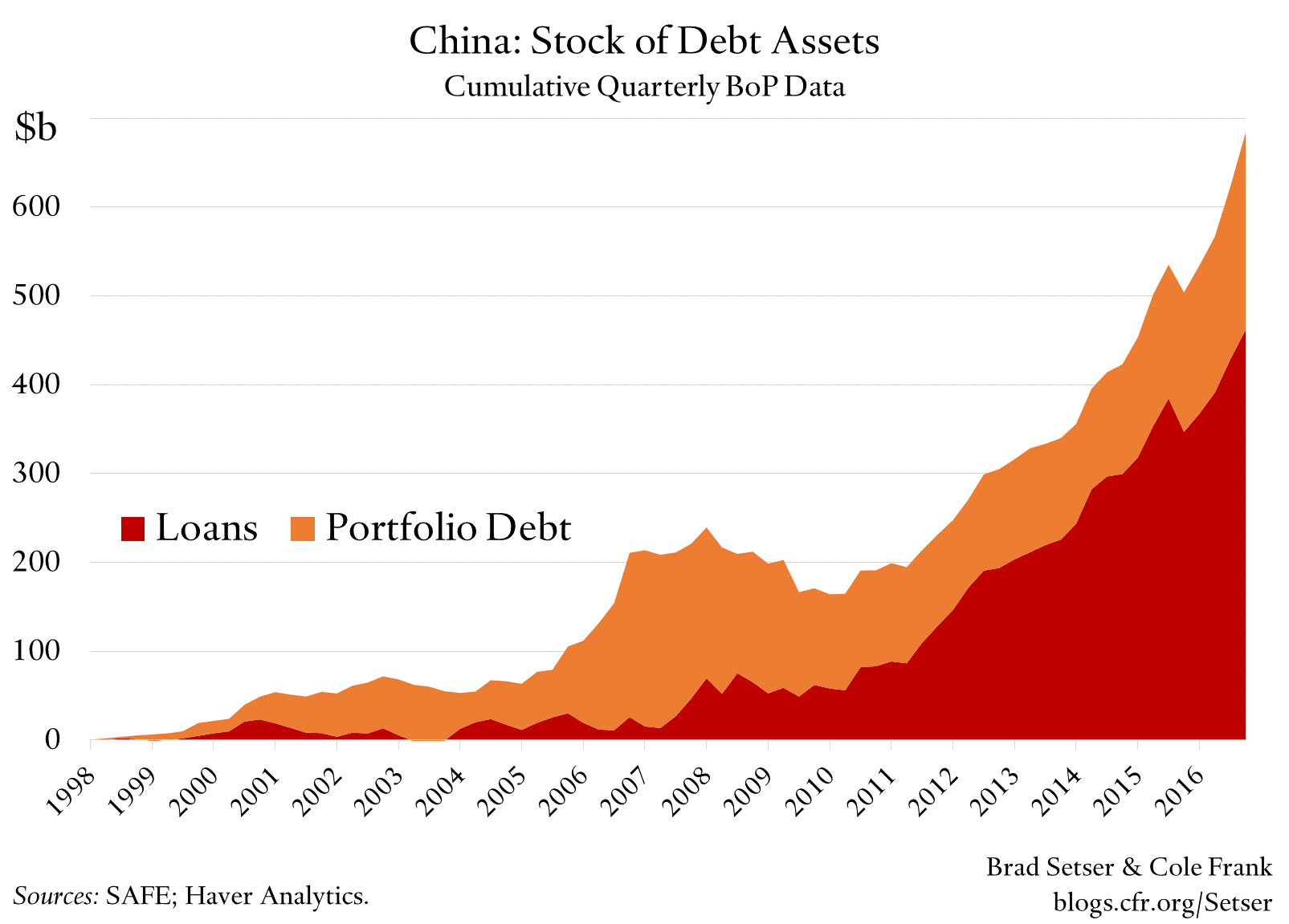

Best I can tell, China’s state banks have been adding about $100 billion a year to their “illiquid” long-term external loan portfolio in the past few years. The $10-15 billion a year ($50 billion over 4 years) current pace of lending to One Belt One Road projects reported by the New York Times remains well below their current overall pace of external lending.*

Projecting out the current growth of China’s external lending over five years would generate roughly $500 billion in financing. And if the bonds China now is purchasing from abroad (over $50 billion a year in the last four quarters of data, with the state banks accounting for much of the buying) are added to the external lending of the state banks that sum rises to $750 billion over five years. The bulk of those bonds appear to have been purchased the the state banks.

So the more modest accounting provided by the New York Times of China’s commitments to One Belt One Road does not imply anything that is wildly out of line with the current pace of growth in the balance sheet of its state banks —though it might imply Chinese banks have a bit less to lend to Chinese firms looking to buy New York real estate, or to Latin America.

Now look at the sums being tossed around from the point of view of China’s balance of payments. This is a complementary view to the analysis of the state banks: the banks right now are either a vector for moving China’s current account surplus abroad, or a draw on China’s stock reserves—the legacy of past current account surpluses.

China ran a current account surplus of $200 billion in 2016. The surplus has been coming down in the last two quarters, but I suspect it is likely to go back up as China reigns in its credit stimulus—especially given the recent fall in oil and iron prices. **

It though is a bit unrealistic to assume that all of China’s surplus all goes to funding state lending, let alone all to the One Belt One Road countries. In 2015 and 2016 the surplus wasn’t large enough to finance private outflows and the increase in state lending (hence the draw on reserves). So if private outflows are large, China could have a bit more of a problem funding its commitments out of its current account. Private outflows from China have been going to Australia, Canada, the United States, and the like. Not to Central Asia.

On the other hand, private outflows have slowed significantly this year. The combination of the yuan’s stability against the dollar, and China’s controls seem to be working.

Finally, what would happen if China had to dip into its reserves to meet its commitments (this would be the case if net private outflows are equal to its current account surplus)?

I personally think could China could safely draw on a small portion of its $3 trillion in reserves. China has a bit more than $3 trillion actually, the central bank’s $125 billion in “other foreign assets” are for all intents and purposes reserves.*** With around $750 billion in short-term debt, China could $500 billion of its reserves to finance lending to One Belt One Road (over 5 years) and still cover its short-term external debt three times over.

So, I do not see any real constraint that would preclude China from raising its current $10-15 billion a year in lending to the Belt and Road (and equity investment from state funds in related projects) to $40 to $50 billion a year —assuming China’s doesn’t lose control of its financial account.

On the other hand $100 to 200 billion annually ($500 billion to a trillion over five years) would be a stretch, as it would imply the bulk of China’s current surplus would need to flow toward the One Belt One Road countries. Or, if private outflows resume, China might need to dip heavily into its reserves

There is another possibility as well — one highlighted by Christopher Balding.

China could start raise most of the funds it needs for its external lending by borrowing —through its state institutions — in global markets. Chinese led multilateral institutions, like the Asian Infrastructure and Investment Bank, are certainly likely to do so. China could thus try, in a sense, to draw on Japanese—or European—savings to fund its strategic ambitions.

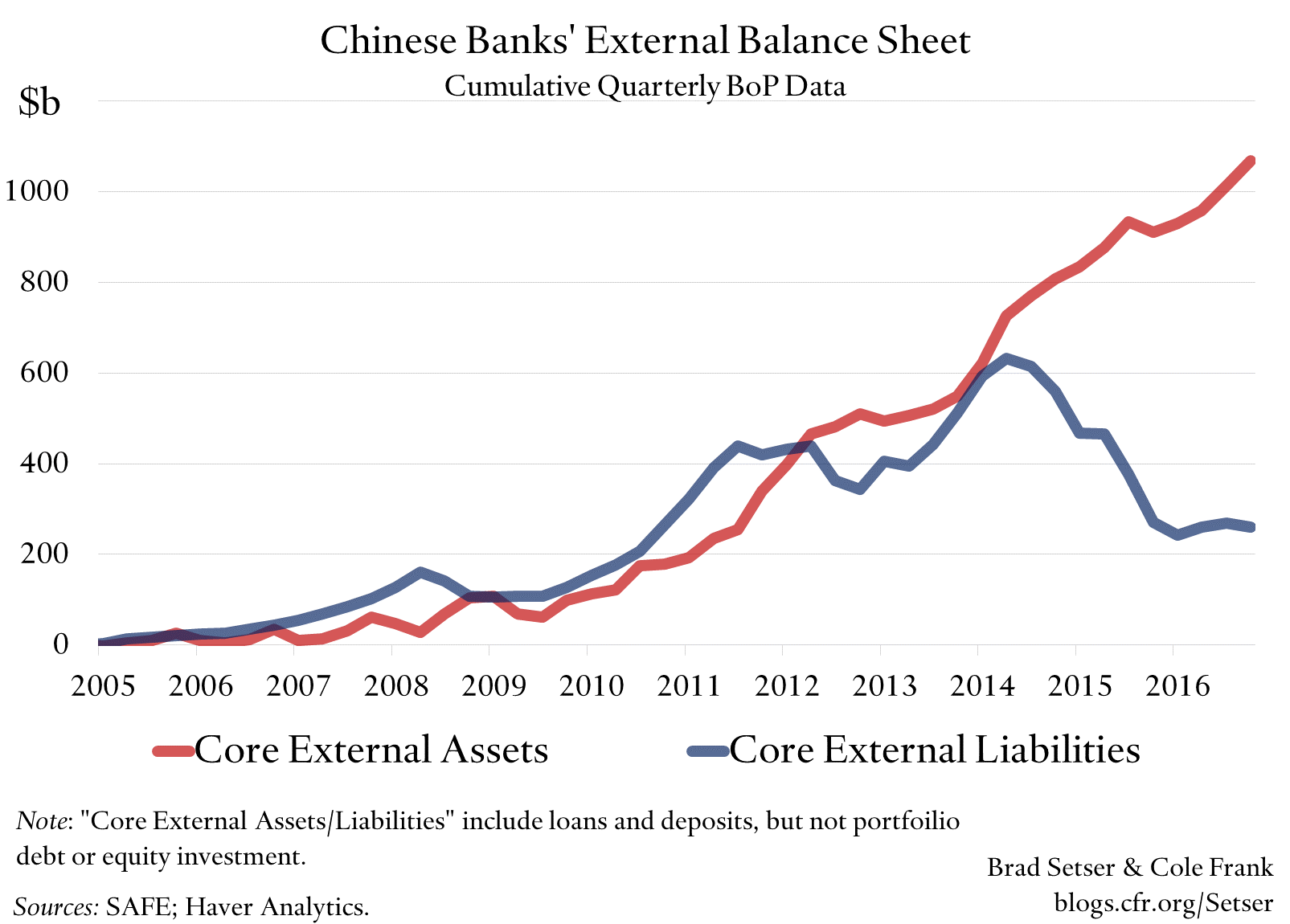

To be clear, though, that doesn’t appear to be how the state banks have funded the recent growth in their external lending. The balance of payments suggests that the net external position of China’s state banks has actually moved into a substantial surplus in recent years, as the banks continued to lend abroad while repaying their “carry trade” related external liabilities.****

Yet China also needs to be at least somewhat cautious. The external borrowing of any state institution is effectively a claim on China’s reserves. China has a bit of leeway —a country with China’s characteristics (little short-term external debt and a current account surplus) would be fine with less than $3 trillion in liquid reserves — but not much leeway that it is freed from any budget constraints.

There is a second reason why the low-end of estimates of One Belt One Road financing seems far more reasonable than the high-end estimates. There are limits on the ability of Central and South East Asia to absorb massive inflows over the next five years. Even sums that are closer to $200 billion than to $1 trillion (over five years) would imply large current account deficits in some fairly small economies.

The combined GDP of the main economies of central Asia is about $300 billion. The combined GDP of Laos, Cambodia and Myanmar is about $100 billion. If India stays out, the combined GDP of the main economies of South Asia is $600 billion (Pakistan is the biggest). Obviously expanding the set of countries to cover some larger economies would help. But it isn’t clear Russia, which now runs a current account surplus, particularly wants to be financially dependent on China. And the main economies of southeast Asia and the Gulf do not lack access to market financing and do not necessarily need to rely on China to fund their infrastructure.

Would $200 billion from China over five years be enough to create Asia’s equivalent of Chicago (a brilliant analogy that comes from Paul Krugman), with China enjoying stronger transportation links to Central Asia, South Asia (Pakistan at least), and South East Asia than any of these geographic regions enjoy with each other? To be honest, I do not know.

And I think Krugman’s analogy could be extended to cover oil and gas pipelines as well as roads and railways — though invariably that also raises the Russian angle. More on that at a later time.

* I should note that China could expand its lending capacity by capitalizing offshore financial intermediaries that fund themselves in global markets. That is the model of the AIIB—though it isn’t the model of the China Development Bank, which historically has funded itself domestically.

** The U.S. need not worry that there won’t be spare savings globally to fund the U.S. current account deficit if China’s surplus is channeled towards its neighbors. The combined surplus of Japan, the Asian NIEs, and Europe is over $1 trillion. And the world economy really would be more healthy if the U.S. (along with Mexico and Canada) wasn’t the one absorbing the bulk of the world’s spare savings—the resulting trade deficits put a huge strain on workers in the U.S. manufacturing sector.

*** In addition to $3 trillion in reserves and $125 billion in reserve-like assets (the PBOC’s other foreign assets), China has $550 billion in external loans and $350 billion in portfolio debt and equity (mostly state owned in my view, with the debt held mostly by the state banks and the equity by the CIC and a few others). The total foreign assets of the Chinese state are closer to $4 trillion than to $3 trillion, and the most illiquid parts of the state’s portfolio in my view are held outside of SAFE’s formal reserves. See this post.

**** Cole Frank and I used the line items “currency and deposits” and “loans” in “other” in the balance of payments to construct this graph. That leaves out trade credit, and other, other assets (other, other is the banks assets with the PBOC, e.g. the balance of payments line item that maps to the PBOC’s other foreign assets). The stock is estimated from cumulative flows.