The Continuing Chinese Drag on the Global Economy

Trump’s trade policies aren’t the only reason for the slowdown in global trade …

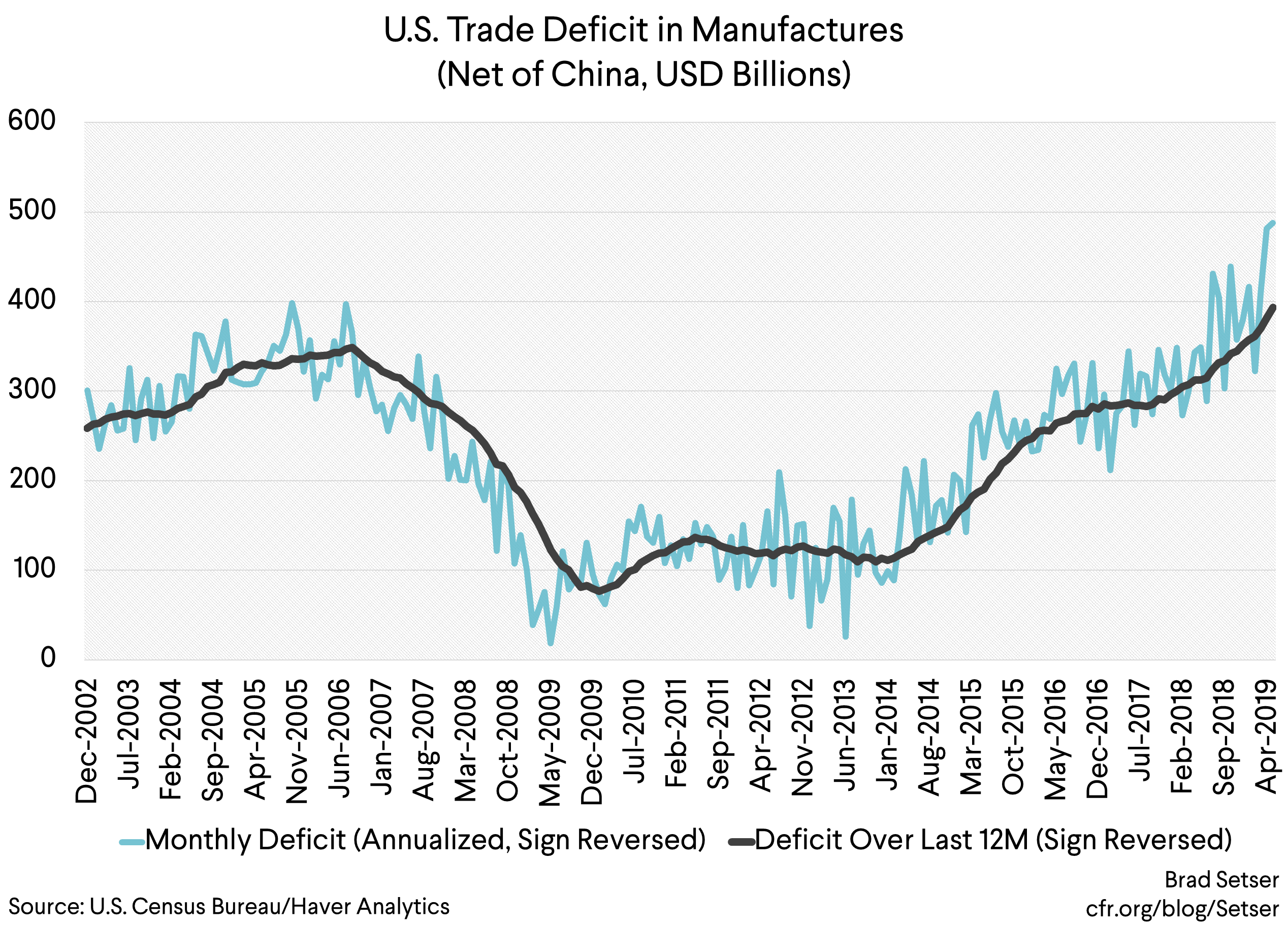

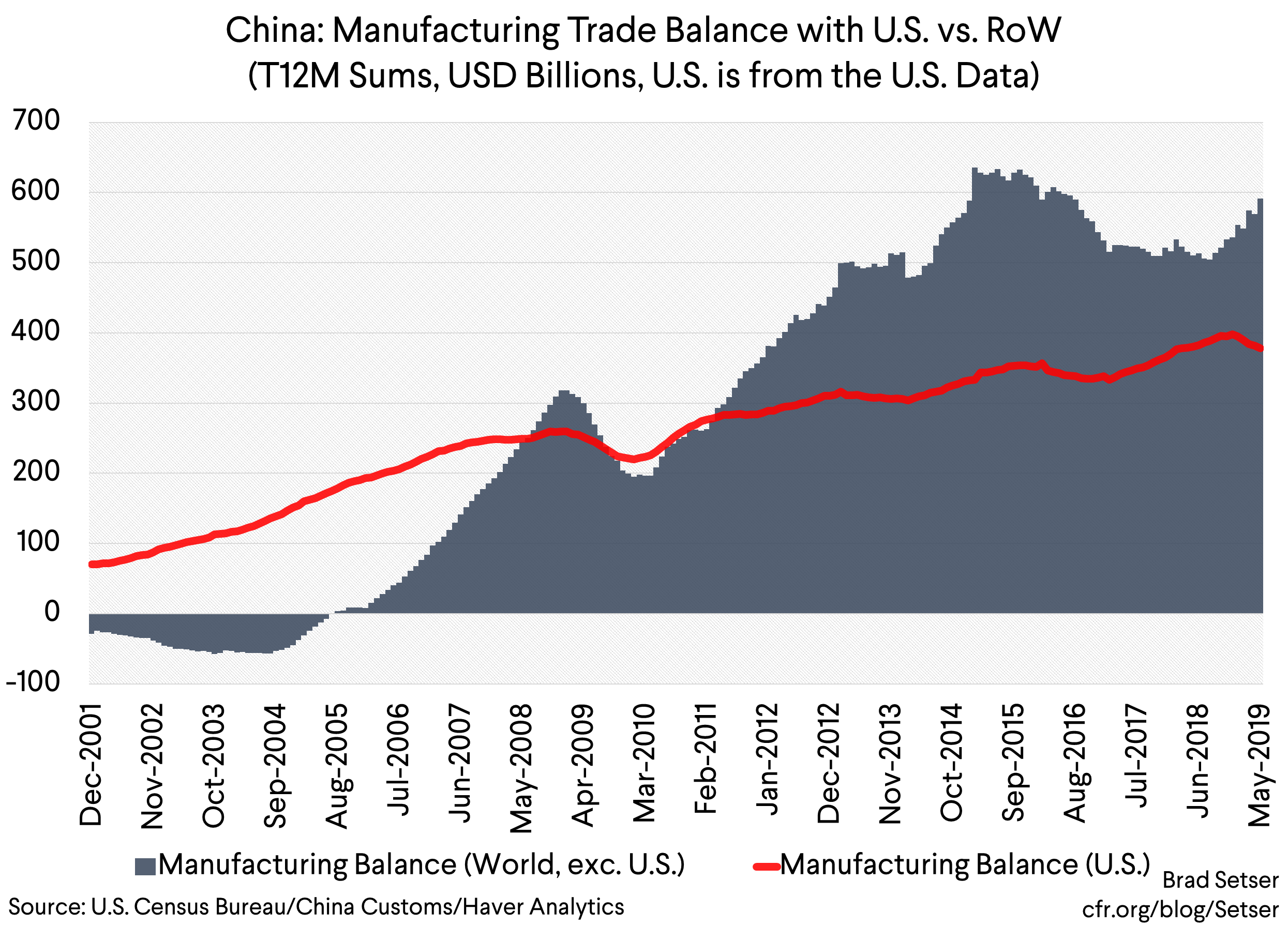

The June trade data shows a rising Chinese trade surplus. And that isn’t just a function of lower oil prices. China’s manufacturing trade surplus is up significantly.

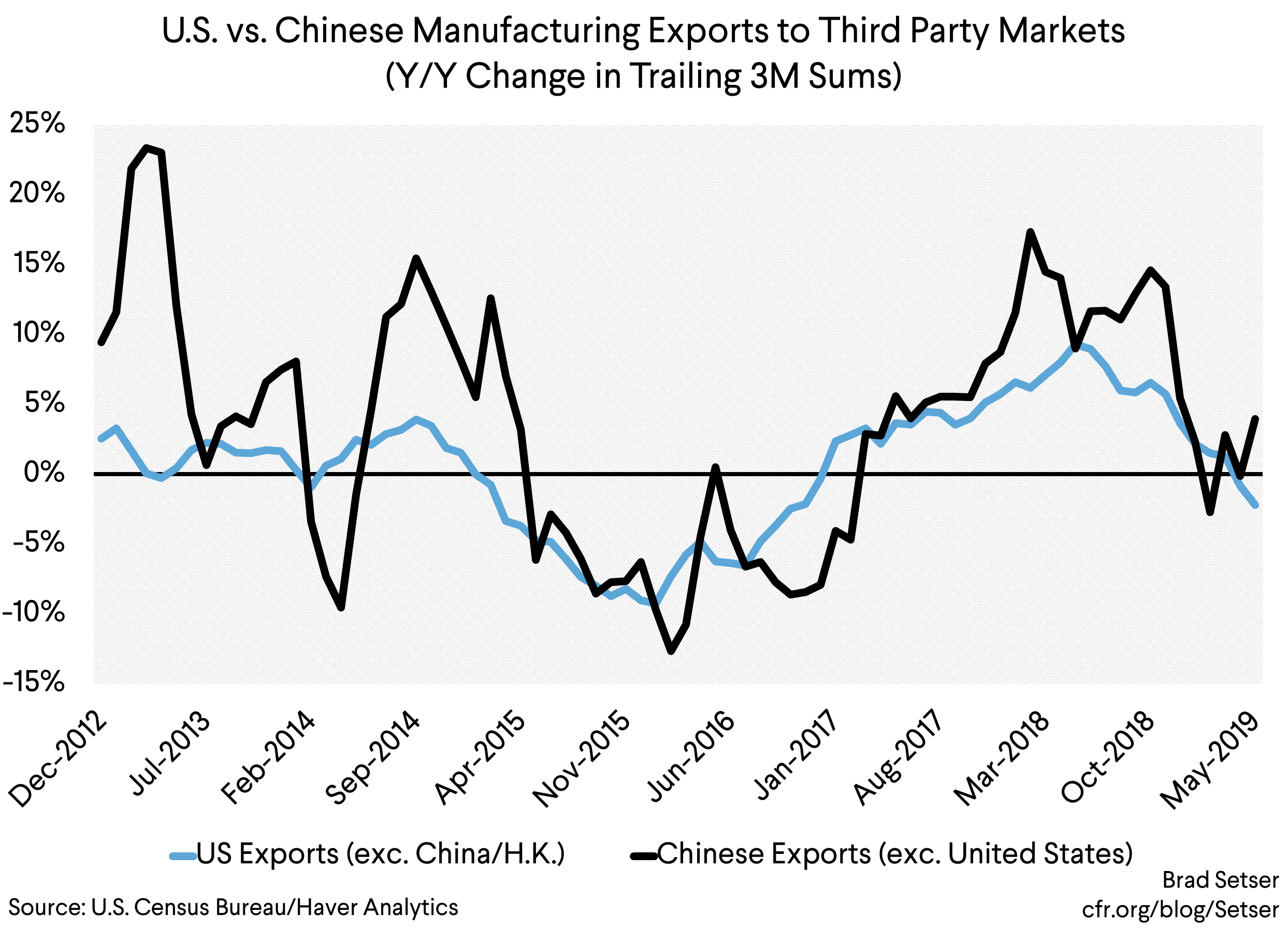

And that rise has come even as China’s manufacturing surplus with the United States has fallen a bit—which by definition means that China’s surplus with the rest of the world is rising. In fact, China’s manufacturing surplus with countries not-governed by Donald J. Trump is up about $100 billion over the last 12 months.*

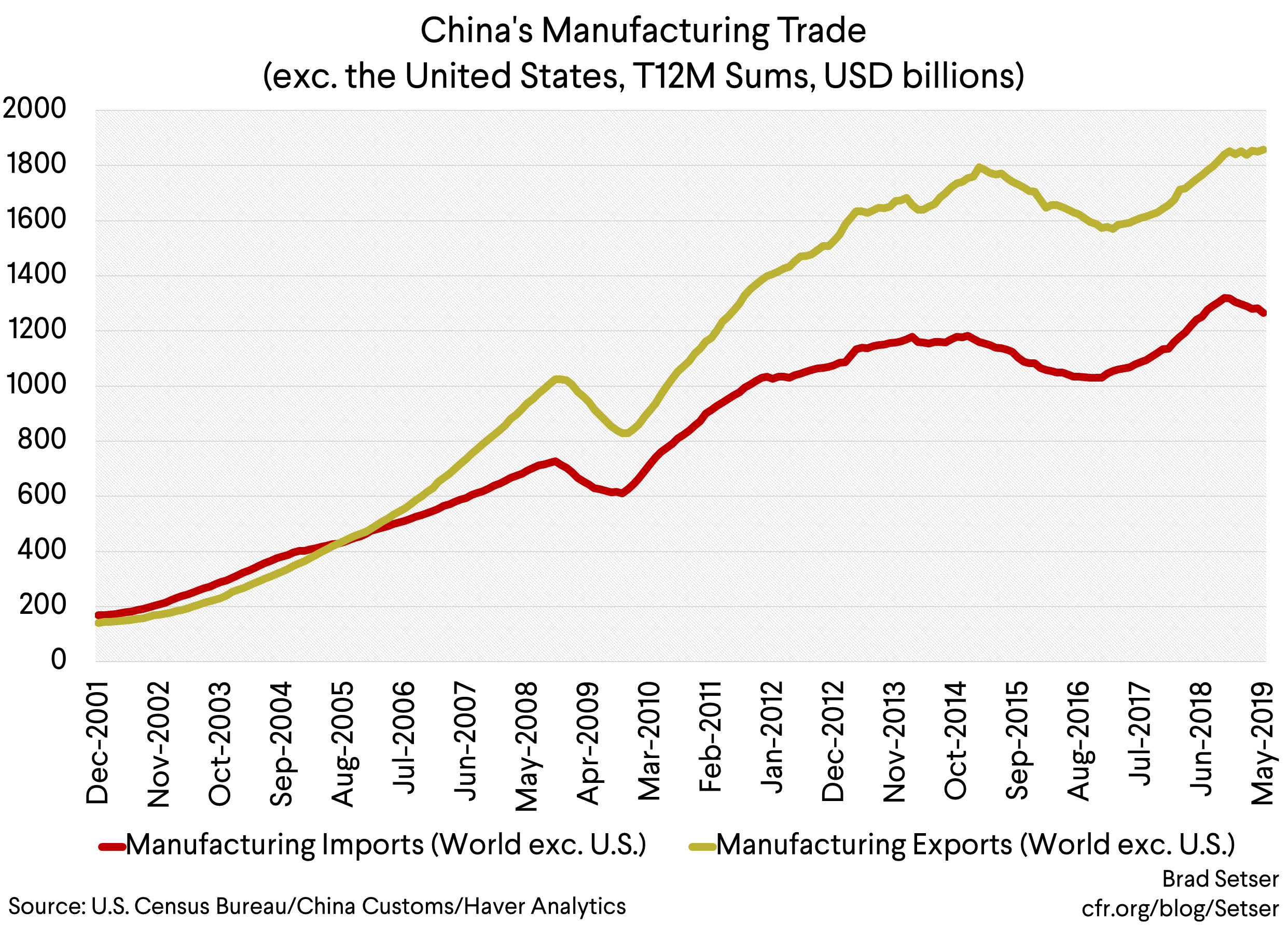

The rise in China’s overall surplus in manufacturing trade hasn’t come from particularly strong Chinese exports. Take out trade with the United States and Chinese exports are up a bit. But the pace of growth is modest. The rise in the surplus is mostly the result of weak Chinese imports.

Of course, some of that change is nominal. We normally think of swings in prices impacting commodity trade, not manufactured trade. But China imported about $300 billion in imported circuits last year, and memory chip prices were way down before the recent trade fight between Korea and Taiwan. Falling prices on chips though should reduce the nominal value of both China’s imports and its exports (imported semiconductors are re-exported as computers and smart phones and networking equipment)—it doesn’t completely explain the current gap between China’s import and export growth.

And some of the fall in imports reflects falling exports to the United States, as roughly a third of China’s imports are for re-export. But if China’s exports to the U.S. are down by just over 10% ($60 billion, roughly) that only works out to a $20 billion fall in China’s imports from the rest of the world.

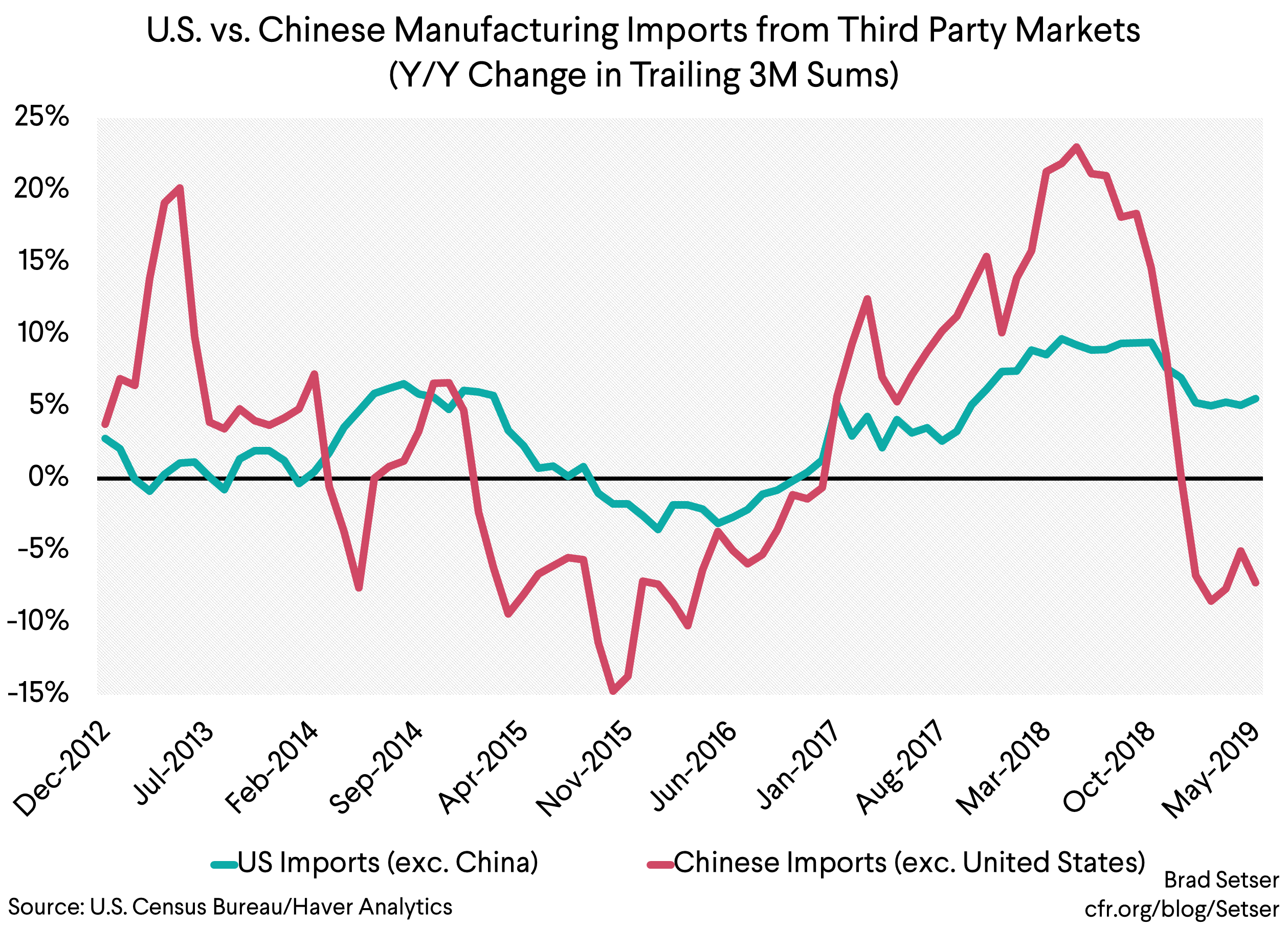

The rise in China’s surplus consequently seems to reflect ongoing domestic weakness (see Nathaniel Taplin of the Wall Street Journal and Keith Bradsher of the New York Times, including his report from last December; if you exclude China’s “processing” imports to capture imports that are mostly for China’s own use, its manufacturing imports are down), not just weakness in China’s exports. And that’s impacting all of China’s trading partners. No one is doing particularly well selling to China right now.**

So China’s trade surplus with countries that haven’t raised tariffs is rising. What of the United States?

U.S. imports of manufactures of non-Chinese manufactures are still up 5 percent year over year in the most recent data (last data point is May). The U.S. isn’t providing the kind of big positive impulse to the world economy that it provided in the first part of 2018 (nothing like a 10 percent y/y increase in the world’s largest importer of manufactures to juice global trade numbers). However, if you set China aside, the net impulse to global trade from the United States is still positive.

And, well, the United States hasn’t been competing that effectively for global demand either.

U.S. exports of manufactures are now down year over year. Unlike China.

Some of the growth in U.S. imports may be the product of the diversion of trade away from China (but likely not that much in aggregate, even if the effect is significant for specific countries—U.S. imports from Vietnam are up a lot, but imports from Vietnam are roughly 1/10th as large as imports from China). And it is possible that China’s weakness is a function of the broader uncertainty that Trump has introduced into the global trading system, and thus Trump’s tariffs have an impact that extends well beyond their direct impact on bilateral Sino-American trade.

But right now, it looks like China’s own self-induced slowdown—China tightened policy out of concerns about excessive credit growth back in 2018, and China’s auto market has been in the doldrums for reasons completely independent from the trade war—has been an important independent factor in slowing global trade.

And, well, for the non-Chinese world, the United States remains a demand locomotive.***

---

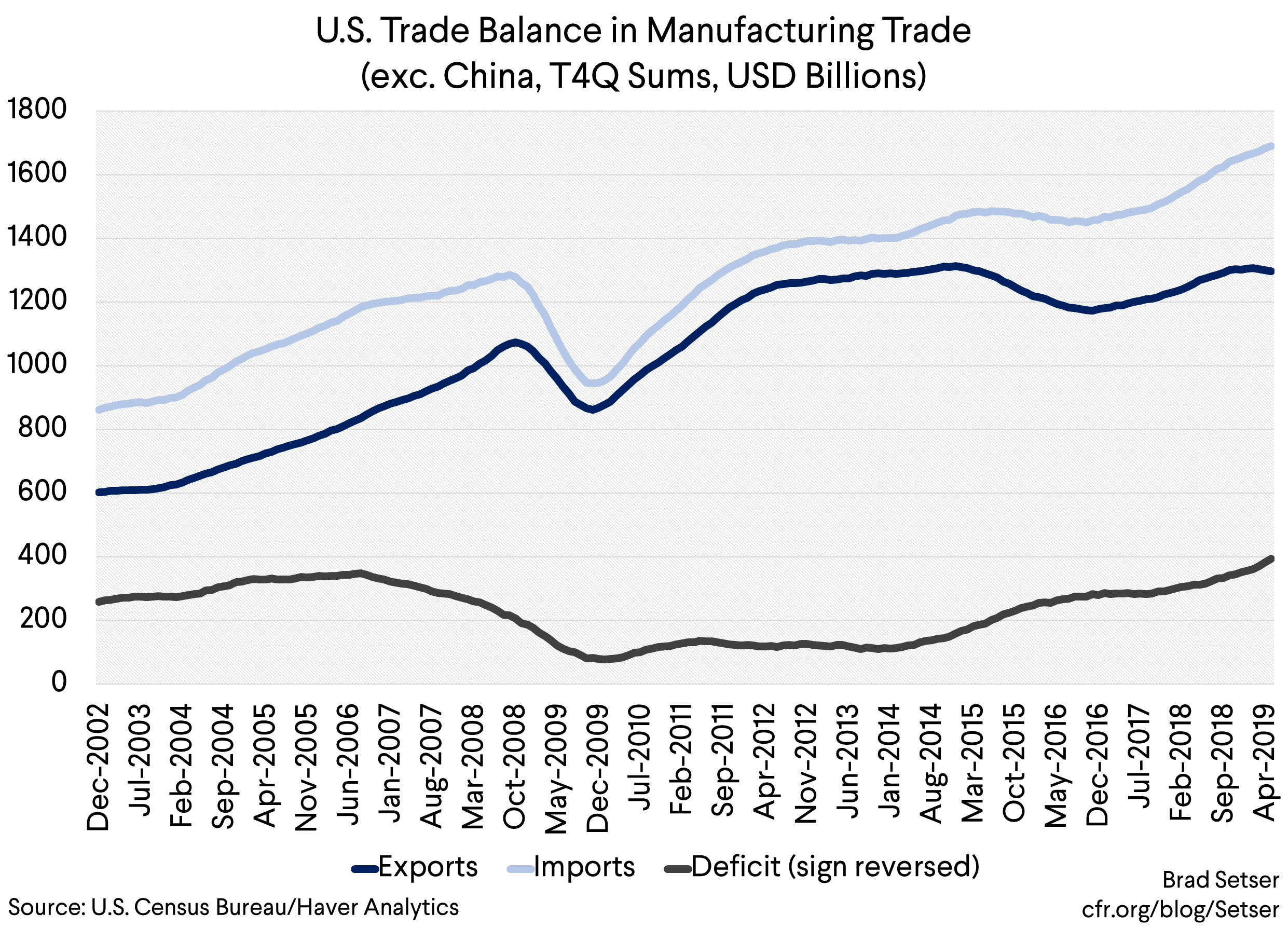

* All the charts here use the U.S. data for imports from China as the best measure of China’s exports to the United States. Non-Chinese manufacturing exports are thus calculated by subtracting the U.S. number on imports (which is much bigger than the Chinese number for exports to the United States) from the Chinese number on manufacturing exports. It isn’t a precise match, but I think it has information value.

** A bit of throat clearing. Obviously this analysis relies on two splits of the trade data, first a split between commodities and manufactures, and then a split between China (the U.S. for China) and the rest of the world. Those who object to any analysis of the bilateral numbers and argue that only the aggregate numbers matter thus have many grounds to object to this analysis. I also totally understand that in a world where China’s trade balances, China would run a surplus in manufactures that would be offset by a deficit in commodities and (to a degree) tourism. There though are two points in defense of this split. First, commodities trade is heavily driven by trade in oil, and the United States and China are on on opposite paths here—China is the world’s largest oil importer, and the United States is about to become a net exporter of oil and product. And second, the aggregate data right now is heavily influenced by the fall in Sino-American trade, and thus it doesn’t tell us much about the evolution of trade that hasn’t been subject to the same kind of tariffs and restrictions.

*** Higher frequency measures actually point to an even bigger rise in the U.S. trade deficit with the world exc. China. There is another point here, one I hope to explore later—it is pretty obvious that the non-Chinese manufacturing trade balance has moved inversely with the lagged dollar.