Finding Ireland in the U.S. Balance of Payments Data ...

Turns out a small and very green island dominates financial flows from “other euro area countries.”

Ireland’s impact, of course, is a case study in the role that “trade-in-tax” plays in driving global trade and financial flows in today’s global economy.

One strange thing about the data the U.S. reports on the balance of payments is that the country-by-country breakout covers Luxembourg but not Ireland.

I suspect that is because the United States reports the country-by-country data for all of the original members of the European Economic Community.

But Ireland today is a balance of payments colossus, thanks to its emergence as the key link in the tax strategies used by many tech firms and many pharmaceutical firms. Ireland is the United States’ largest export market for software services (see Table 2.2), its second largest market for exports of “research and development” services (behind Switzerland), and the biggest single source for U.S. imports of pharmaceuticals.

And, thanks to all the “offshore” profits that U.S. firms built up abroad (under the old tax code, they could defer U.S. income tax payments indefinitely so long as the funds legally were not repatriated back to their parent) and Ireland’s role as a financial center, Ireland was, at least notionally, a large source of financing for the United States.

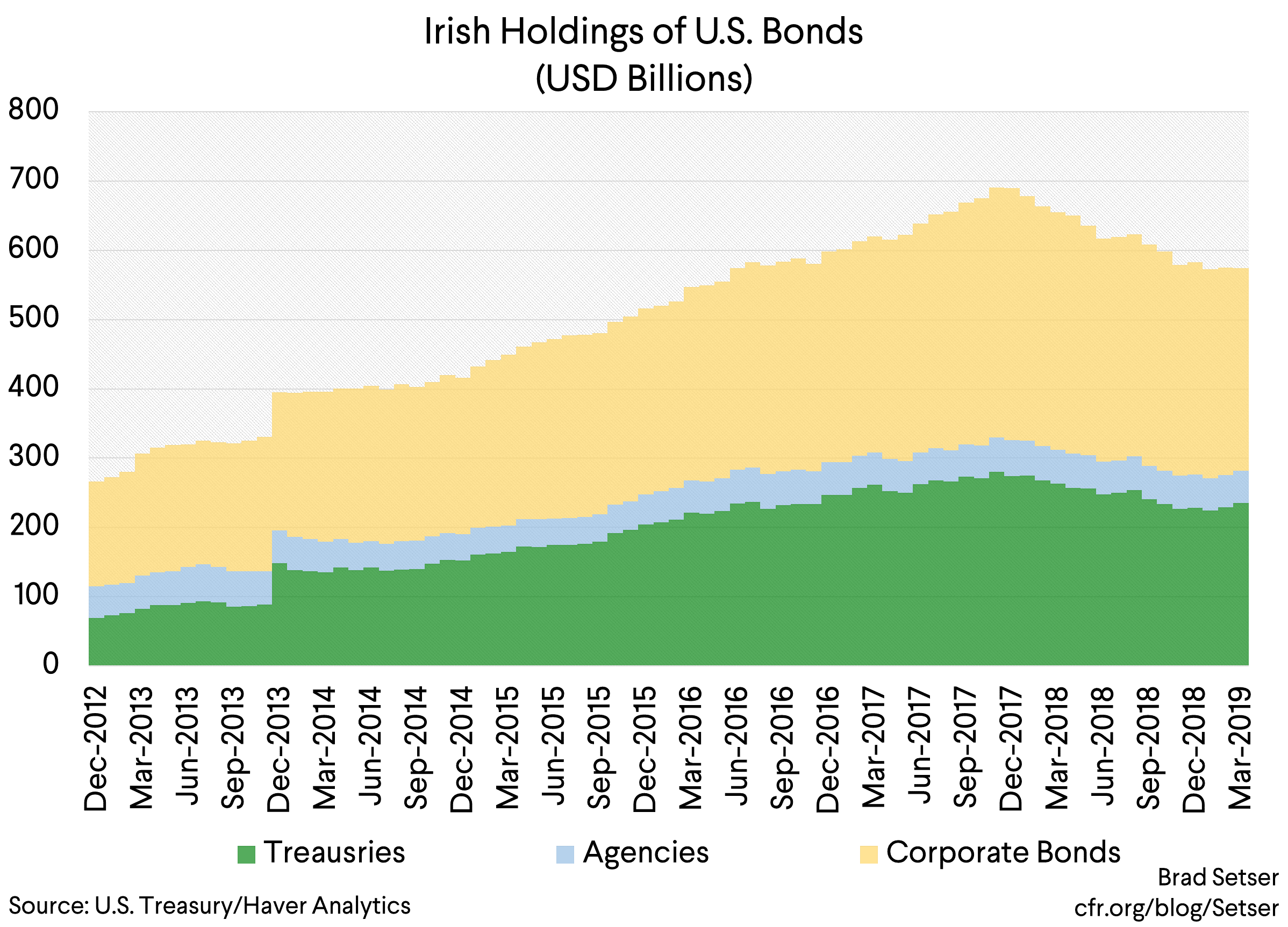

Back in 2017 and 2018, Ireland was the world’s third largest holder of U.S. Treasury bonds…and it also held another $305 billion of corporate bonds.

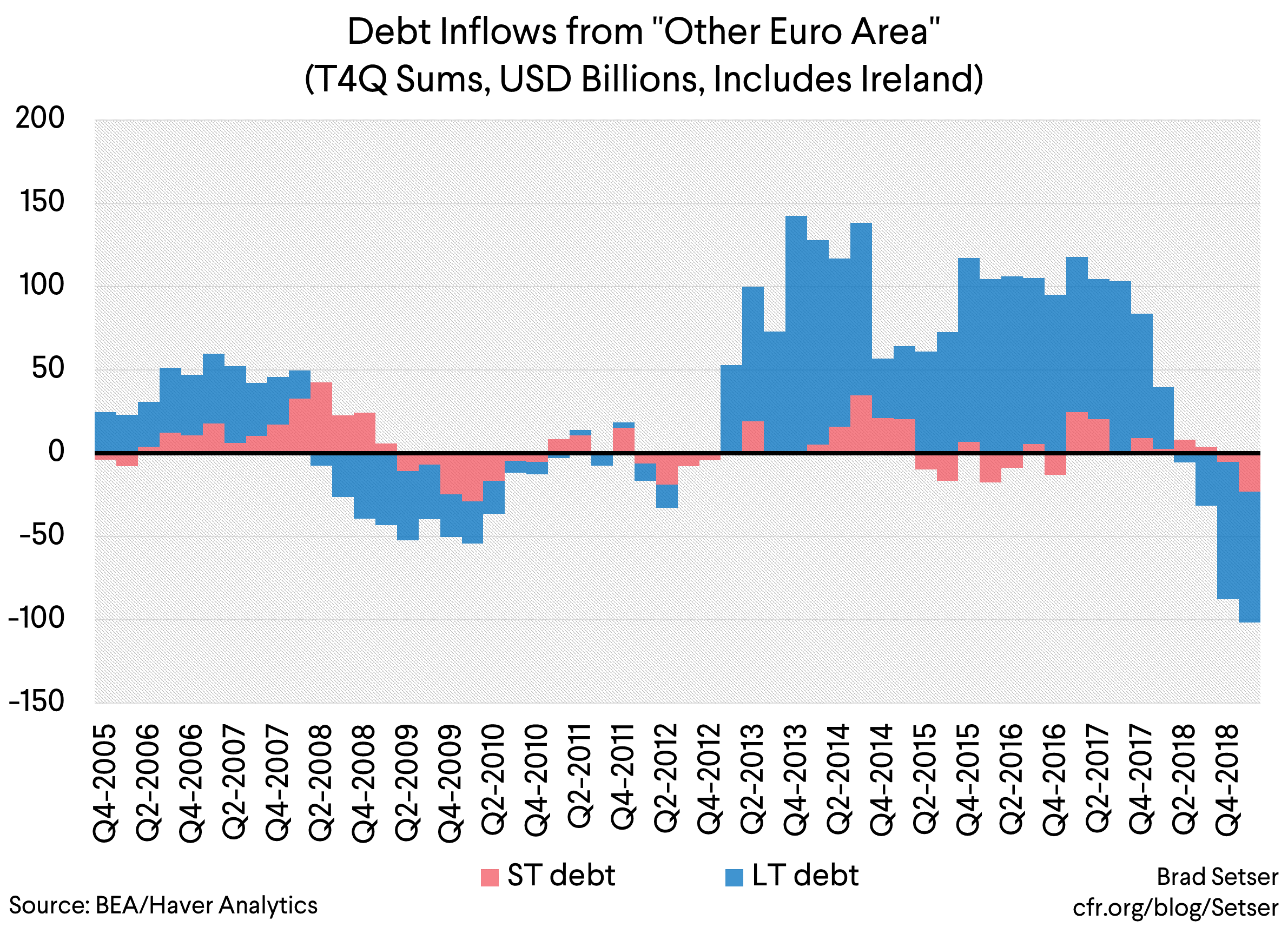

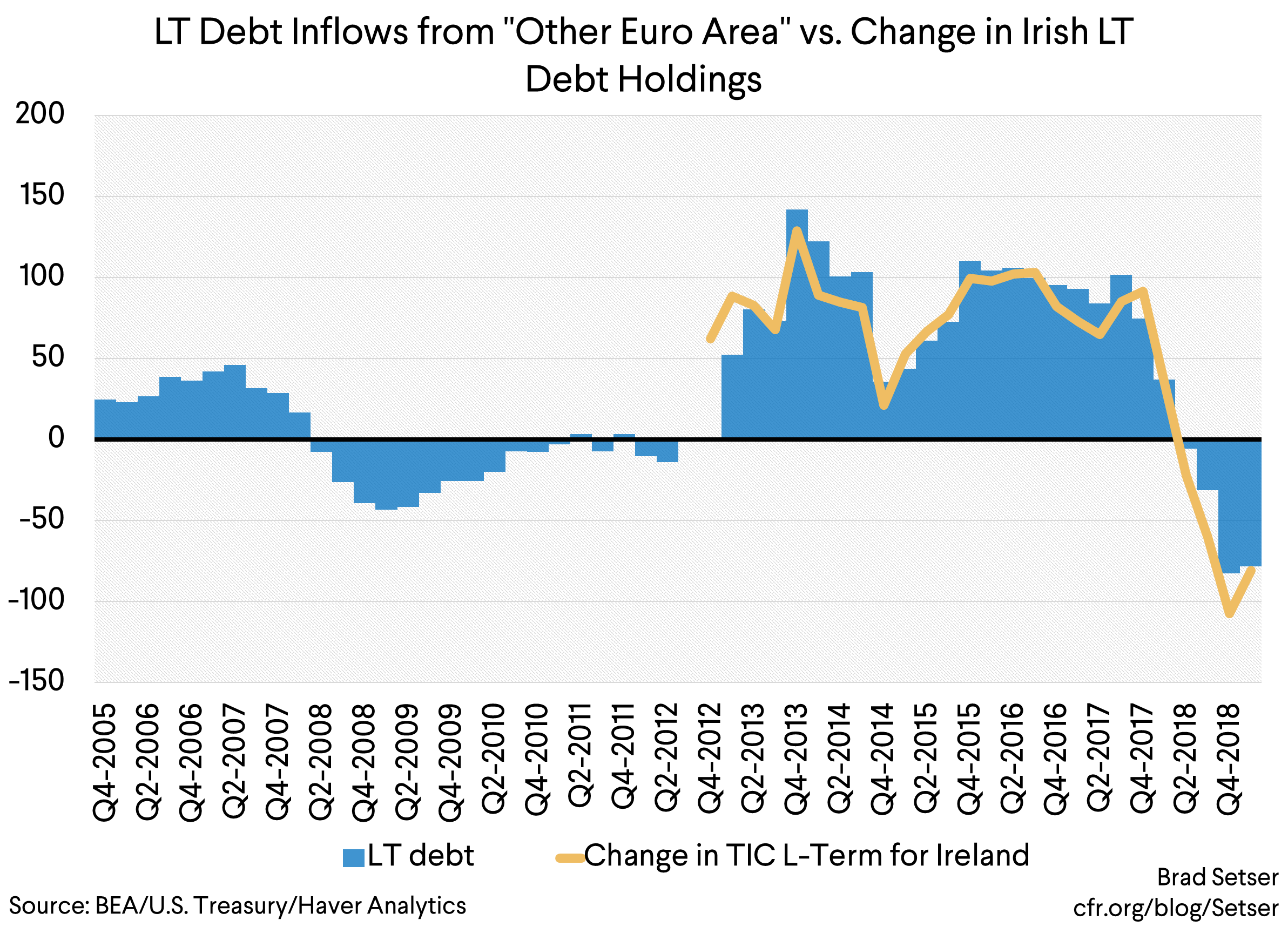

And it turns out that Ireland is big enough that it is possible to identify its impact on the balance of payments data—look at a plot of the long-term bonds bought by “other euro area countries” (data is from table 1.3 of the interactive data).

Before the tax reform, “other euro area countries” were buying $100 billion a year in U.S. bonds. In the year after tax reform, they sold about $100 billion of U.S. bonds. That’s almost equal to the y/y change in reported Irish holdings of U.S. Treasury and corporate bonds.

If you understand why, then you understand the deep impact that “tax” now has on U.S. balance of payments flows.

Under the old system, U.S. firms effectively could avoid paying corporate income tax on their offshore income by deferring repatriation and legally holding funds in their offshore subsidiaries. That meant that they build up large stock piles of cash on the books of their foreign subsidiaries.

The firms in turn could bring funds home indirectly by borrowing onshore against their offshore cash (see Zoltan Pozsar).

And, well, during the period when U.S. policy rates were close to zero, many firms juiced their returns by shifting from holding “cash” abroad to holding a bond portfolio—Apple could buy Pfizer’s bonds, Pfizer could buy Apple’s bonds, and so on.

With the new tax system, firms no longer have to maintain the charade that the funds are legally offshore: the “global” minimum tax on intangibles cannot be deferred, and that is all U.S. firms with large offshore profits owe back to the United States on their offshore profits. Yet while firms are free to move their funds around without worrying about tax, they are under no obligation to unwind their offshore structures—in fact, the flow of funds back to the United States has been more modest than predicted. But it hasn’t been zero.

Hence, the full reversal in bond flows from “other euro area countries”.

There is a bigger point here—a portion of the bond inflow into the United States over the last ten to fifteen years was the by-product of the buildup of dollar holdings by U.S. based firms, and thus in some sense fake.

The accumulated offshore profits of U.S. firms in the world’s main low-tax jurisdictions were about $2 trillion—at least half of that was held offshore in cash and bonds (see the the New York Fed; S&P put the total at the end of 2016 at $1.1 trillion*). Those holders of U.S. debt didn’t need to hedge—they are intrinsically investors who want to hold dollars (in the balance of payments, the buildup of profits offshore registered as higher U.S. FDI abroad and more foreign holdings of U.S. debt, so the net impact was modest). Indeed, such investors, together with investors holding dollars as part of their reserve portfolio, account for the bulk of the rest of the world’s claims on the United States.

And the rest? Well, some is a hedged flow from yield starved insurers around the world—and well some at least is a now unhedged flow from yield-seeking Asian insurers (led by Taiwan’s life insurance industry). But that’s a topic for another time.

* The Wall Street Journal, drawing on work by Moody’s, has reported that U.S. firms at their peak held $2 trillion in cash and cash equivalents, so the New York Fed’s numbers suggest about half that was legally offshore. Other estimates suggest as much $1.5 trillion was held offshore.