The Disappearing Japanese Bid for Global Bonds

The rise in Japanese holdings of foreign bonds had an enormous impact on global markets between 2011 and 2020. The markets will now have to adapt to a sustained reduction in Japanese demand.

This a joint post by Brad Setser, a senior fellow at the Council on Foreign Relations, and Alex Etra, a senior macro strategist at the financial research firm Exante Data.

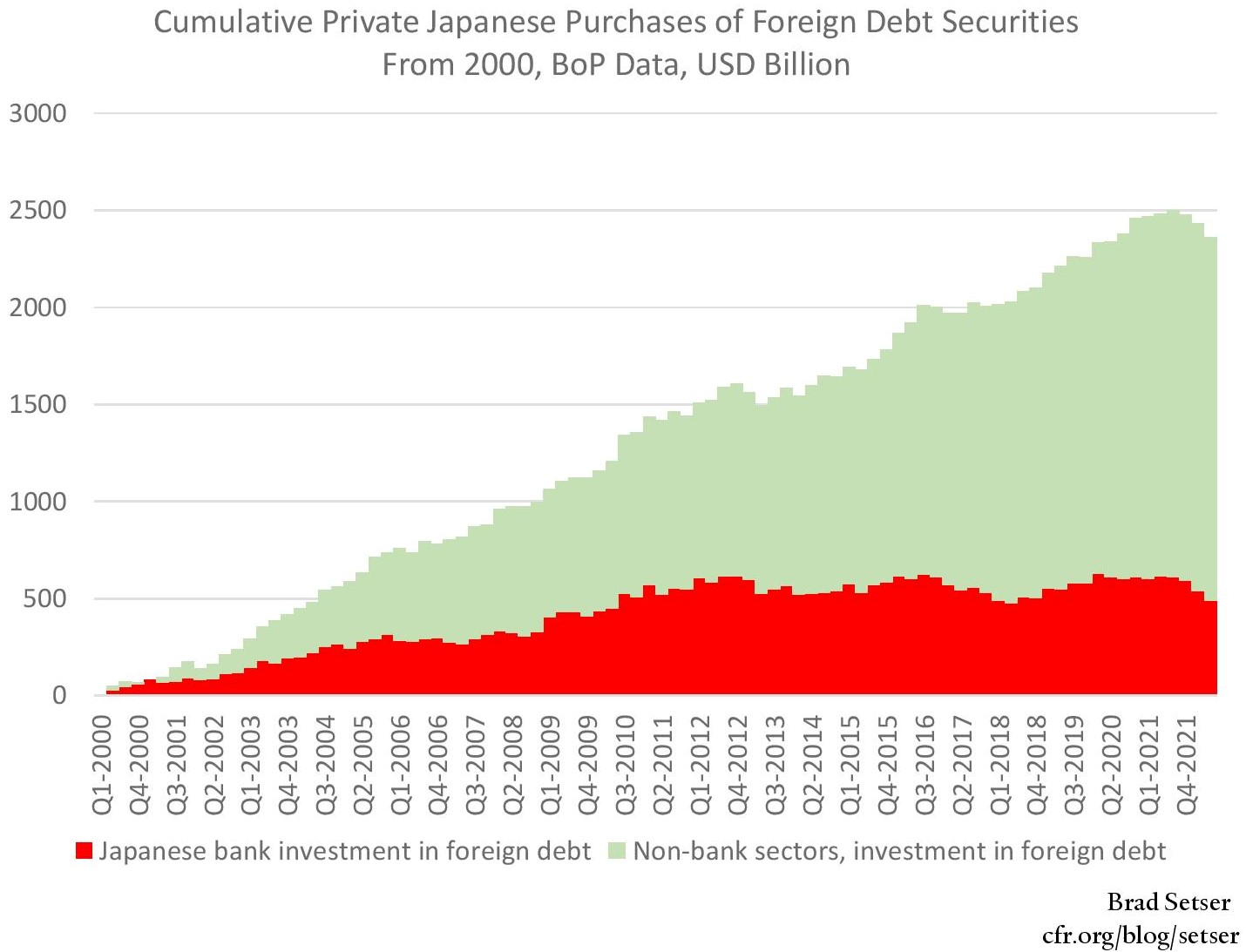

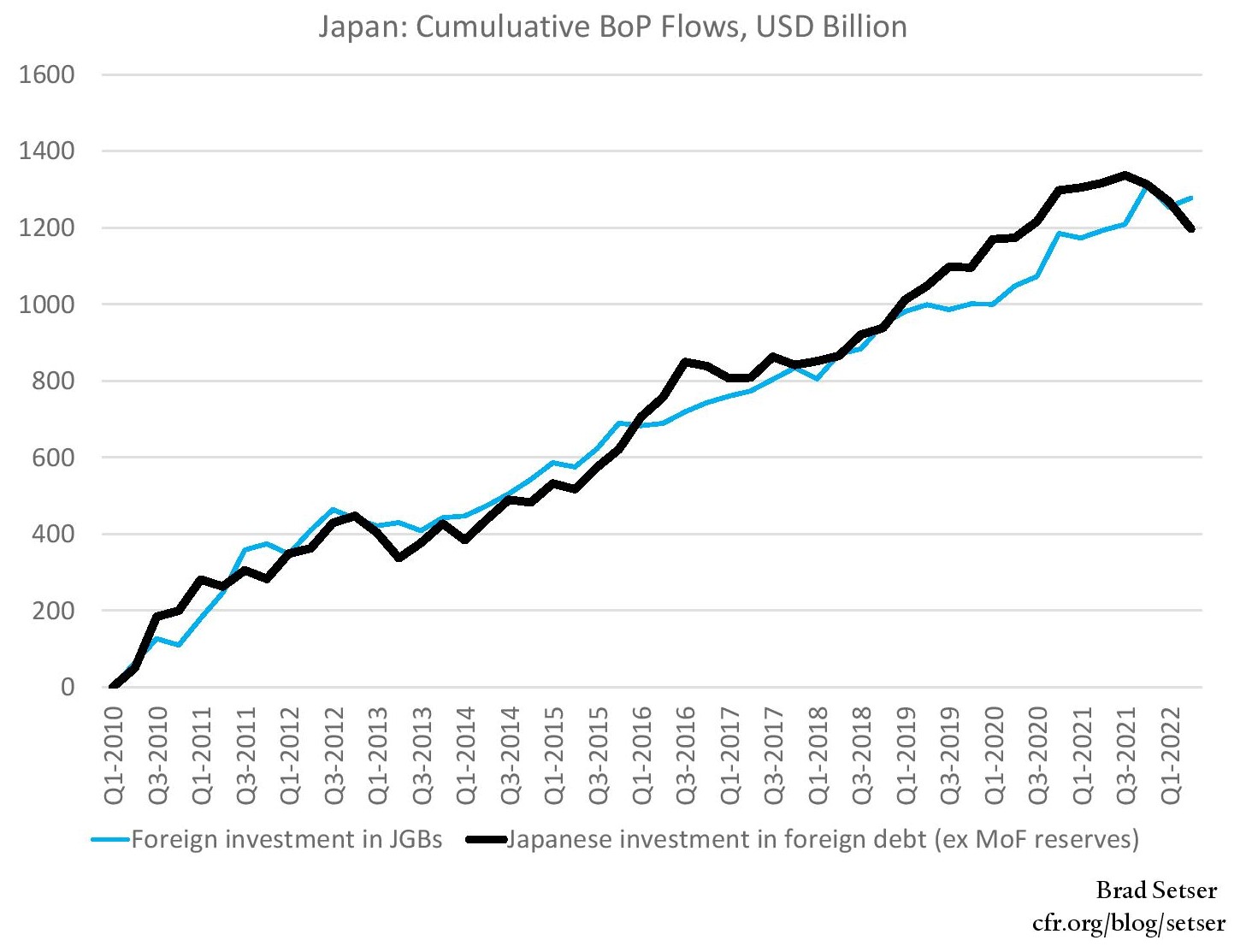

Japanese investors have bought enormous quantities of foreign bonds over the last twenty years. Total holdings of foreign bonds by “private” Japanese institutional investors—so excluding Japan’s $1 trillion reserve portfolio ($967 billion in securities at the end of 2022, held primarily by the Ministry of Finance)—reached $3 trillion at their peak.

It is no exaggeration to say that Japanese flows have had at least as much of an impact on the global bond market as Chinese flows over the last decade—and there is now understandable concern about the risks posed by large potential shifts in the portfolio of Japan’s institutional investors.

This post aims to disaggregate—and hopefully, demystify—the Japanese flow. Japanese demand for global bonds, particularly US corporate and mortgage-backed bonds, French Treasuries (OATs), and Australian bonds, came primarily from a set of large Japanese institutional investors. Two government-owned institutions drove most of the increase in Japanese holdings over the last ten years: Post Bank, with over $1.5 trillion in retail deposits, and the Government Pension Investment Fund (GPIF), Japan’s de facto sovereign wealth fund.

There are risks, of course, if the Bank of Japan moves away from negative short-term policy rates and yield curve control. But the most likely outcome is continuation of the pattern of sales out of Japan that marked 2022 rather than a wholesale liquidation of all foreign holdings.

Drivers of Japanese Outflows

The Japanese outflow should not be thought of as a single flow, as it is not driven by a single dynamic. Rather, Japanese institutional investors invest abroad for three distinct reasons:

the absolute yield pickup available on unhedged bonds given low Japanese rates

a steeper yield curve outside of Japan than inside, and thus the opportunity to make money on currency-hedged bonds

access to the global corporate bond market, and thus the opportunity to collect credit spreads that are hard to find inside Japan. Japanese companies are (famously) cash rich and thus have a limited financing need

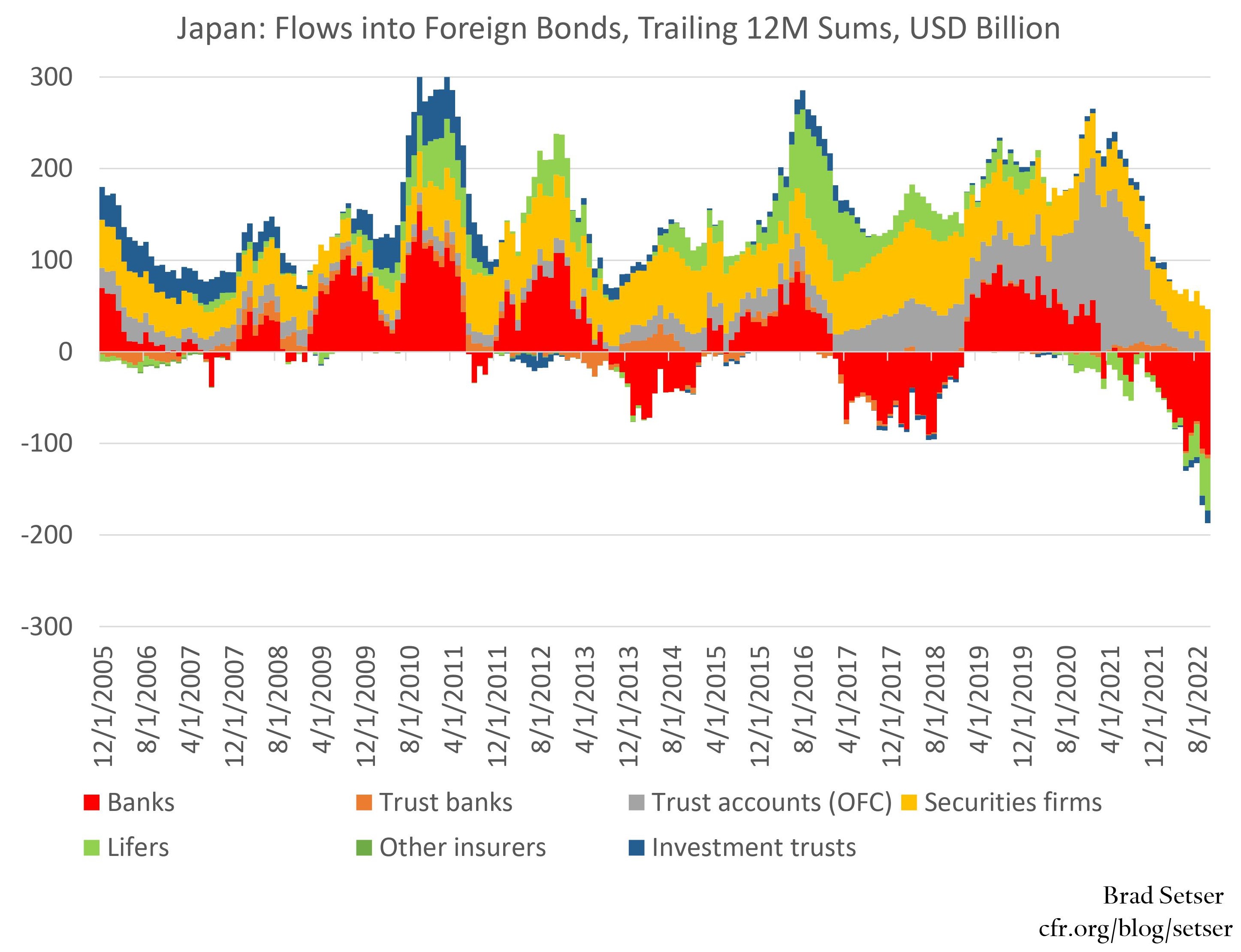

These distinct motives matter right now: Japanese investors continue to have ready access to an unhedged yield pickup but have trouble making money on hedged investments. The intersection of hedged and unhedged demand resulted in significant Japanese sales of foreign bonds over the course of 2022—sales that started well before the MoF sold a portion of its reserves in September and October.*

And these different motives will matter going forward, as the balance between these motives will shape how Japanese investors respond to potential shifts in Bank of Japan, Federal Reserve, and European Central Bank policy in 2023.

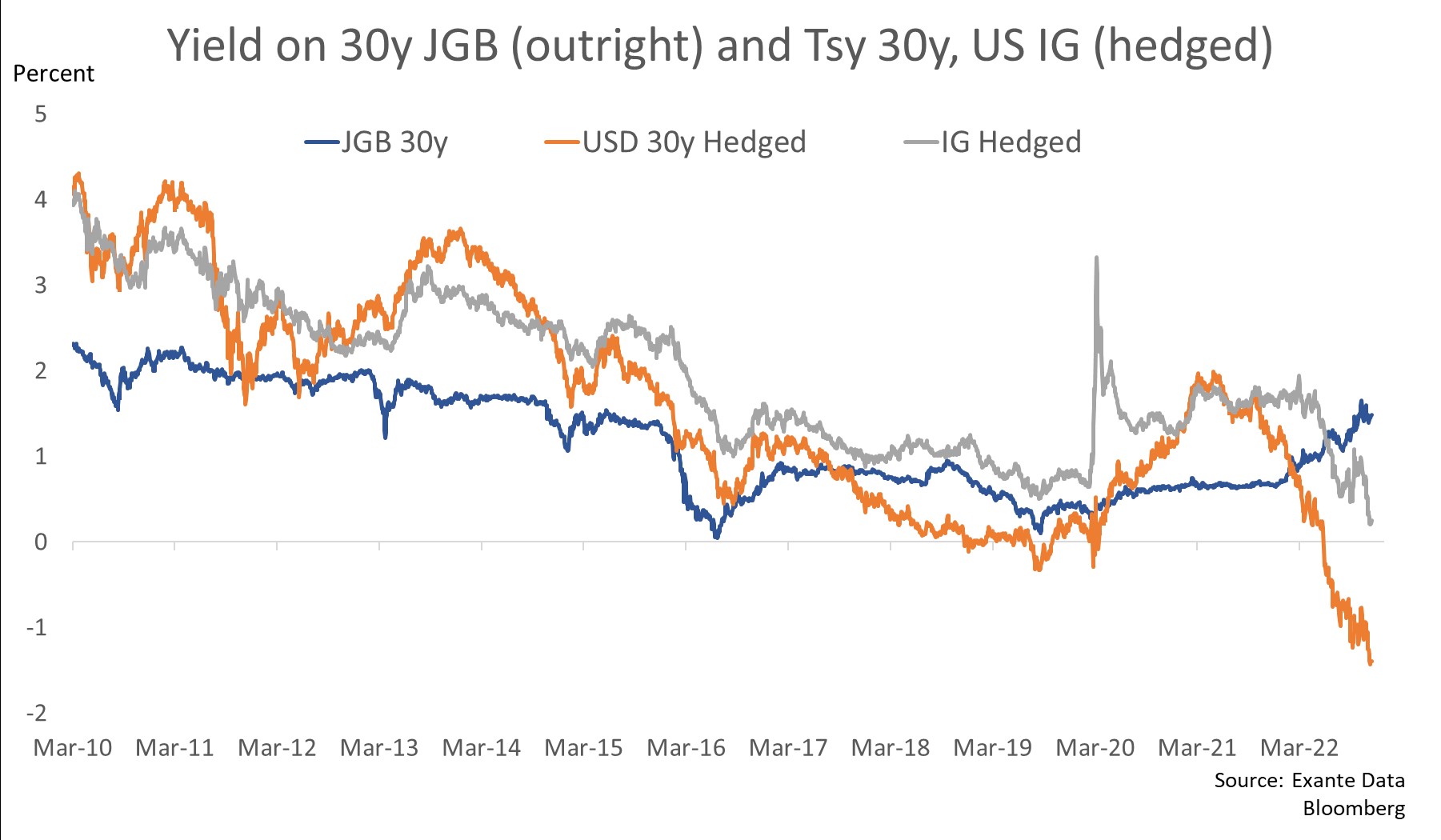

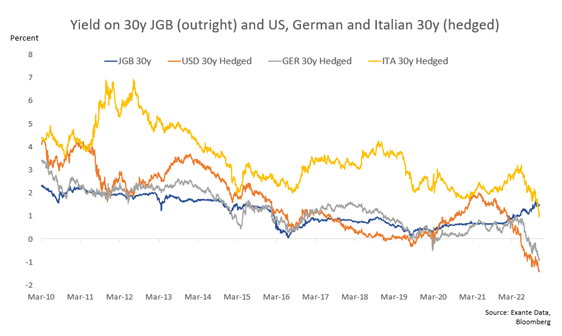

In fact, monetary policy shifts over the course of 2022 have already had an enormous impact on Japanese institutional investors. The Fed’s rate hikes pushed yields on ten-year U.S. Treasuries up from under 2 percent at the start of 2022 to a peak of around 4 percent. Yields on French bonds (2.8 percent), Spanish bonds (3.3 percent) and Italian bonds (4.3 percent) all increased.

On the surface, this shift should have increased Japanese demand for foreign bonds. Even after the surprise increase in the cap on Japanese ten-year government bond yields from 25 bp to 50 bp in December, Japanese investors clearly can get a substantially larger yield pickup on unhedged investments in foreign bonds than was possible at the end of 2021.

But even as wider interest rate differentials on unhedged foreign bonds should have pulled funds out of Japan, hedged investors saw the market move against them.

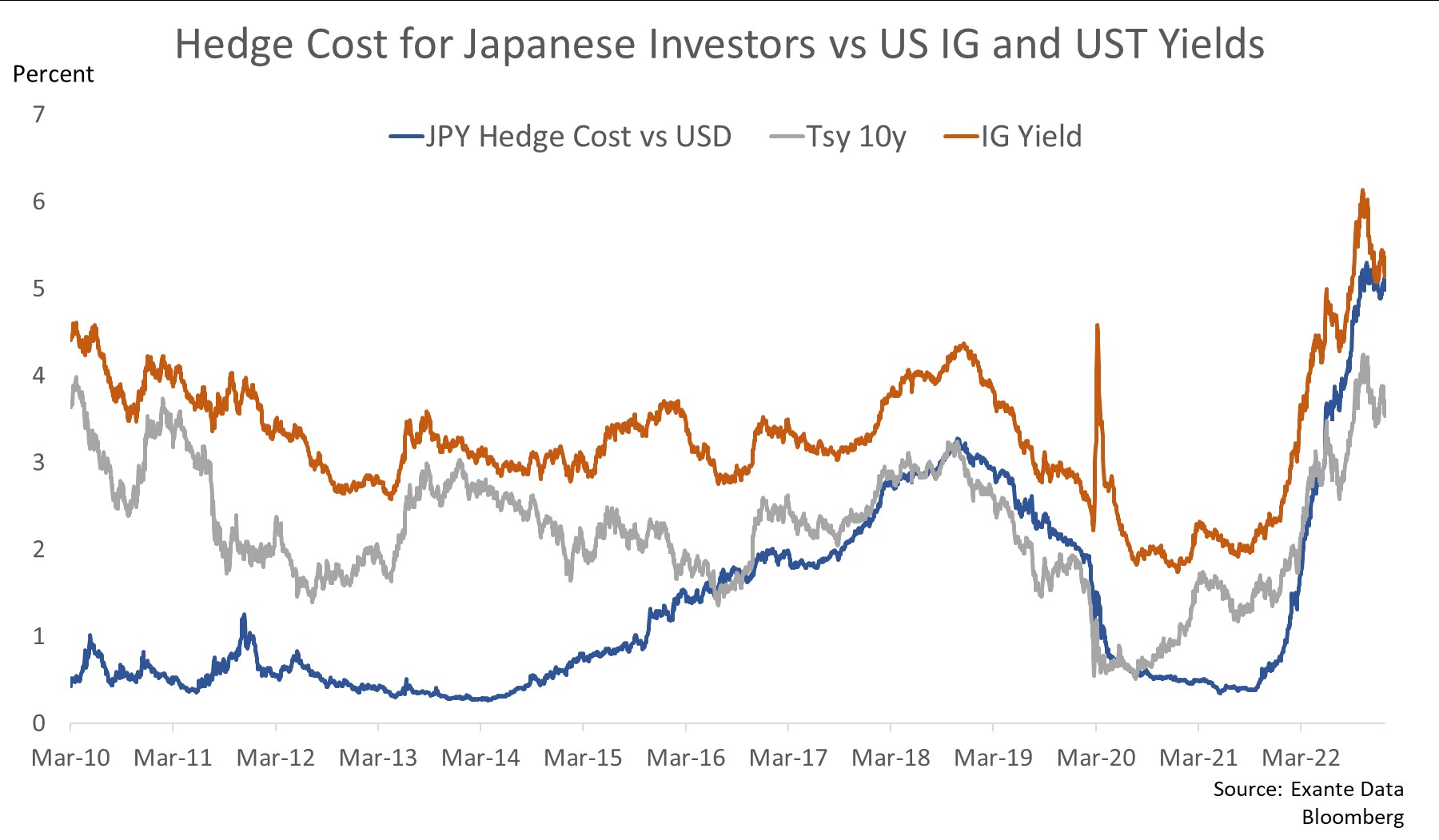

Most hedges economically can be reduced to borrowing short-term money in order to buy longer-dated securities, among other financial assets (say, through a 3M currency swap; see this blog for background on various ways of hedging). The cost of hedging thus is the difference between the cost of borrowing in dollars for a period of months and the cost of borrowing in yen at a similar tenor plus a premium (often called the basis) that gives foreign investors an incentive to lend their dollars to a Japanese institution, rather than to a foreign one (say, to buy U.S. Treasury bills).

The rapid rise in short-term U.S. interest rates relative to long-term interest rates—and now the inversion of the U.S. interest rates curve—have made it unprofitable for Japanese investors to borrow dollars in the short-term (including through the swaps market) and buy safe U.S. government bonds. In fact, by the end of 2022, it wasn’t even attractive to buy currency-hedged U.S. investment-grade bonds.

Different Investors, Different Preferences

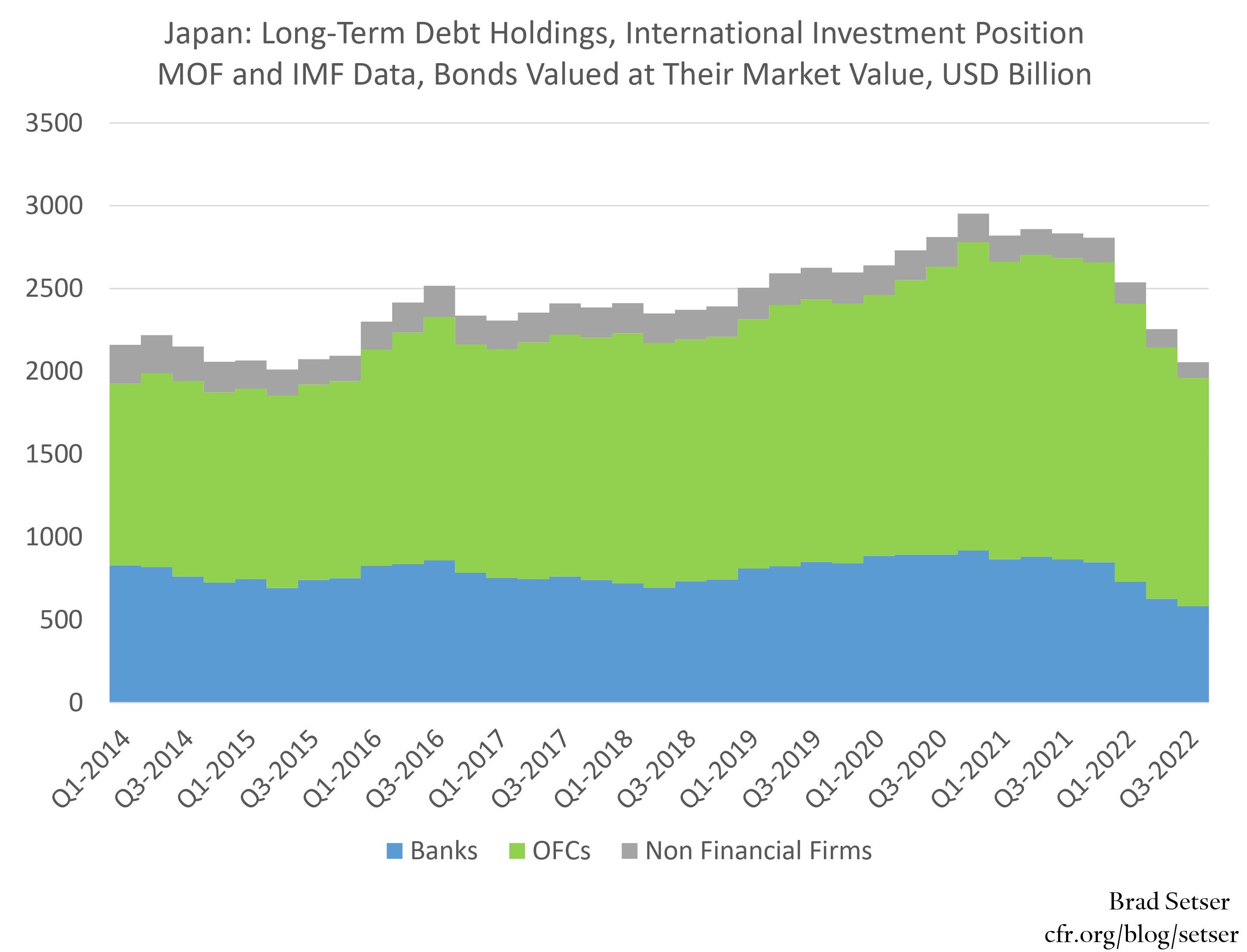

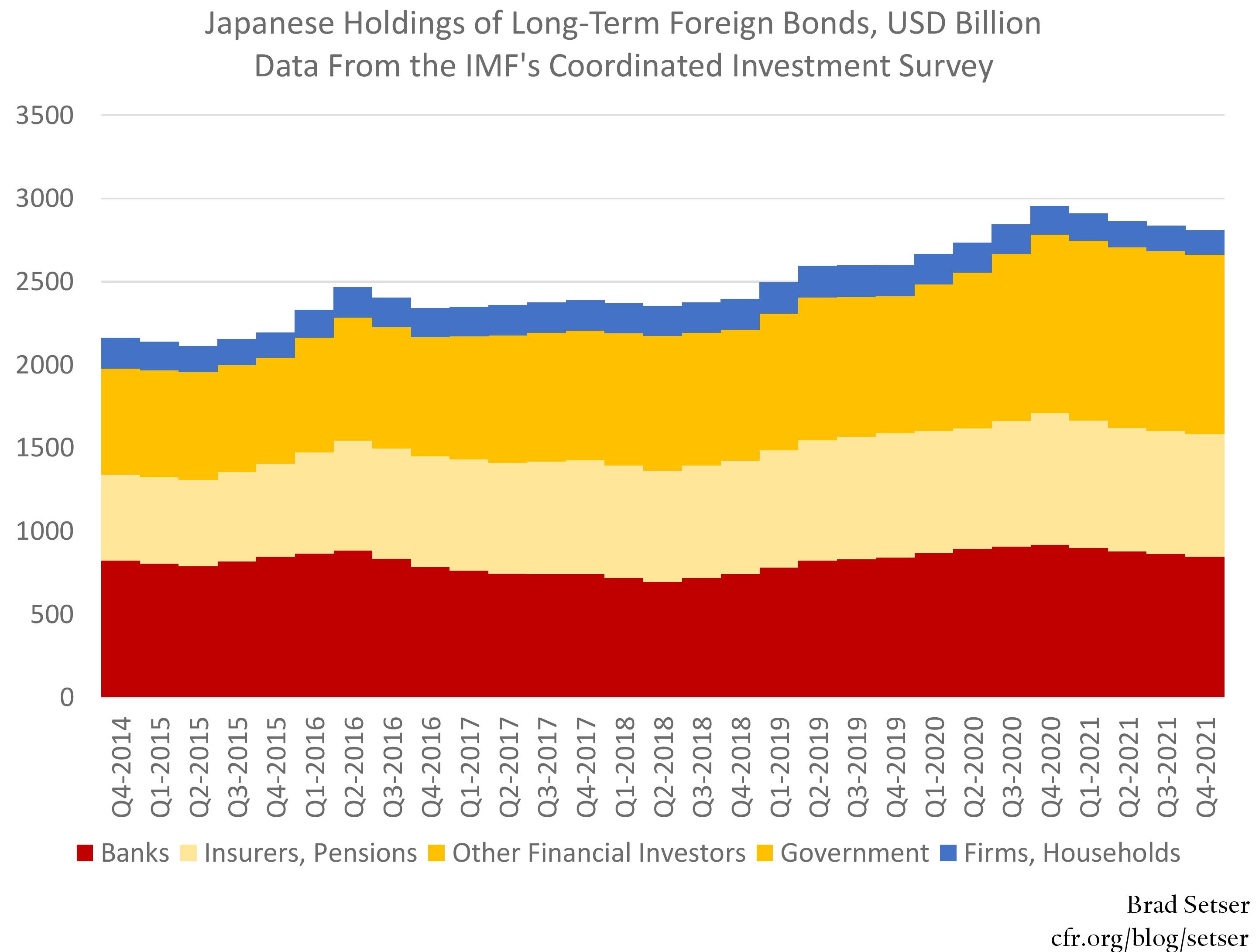

The different return on unhedged and hedged bonds matters, as different groups of Japanese investors have distinct preferences for unhedged relative to hedged risk. The following chart, which shows the distribution of foreign bond holdings at the end of 2021, will change radically when the data for the end of 2022 is available.

Start with Japan’s commercial banks:

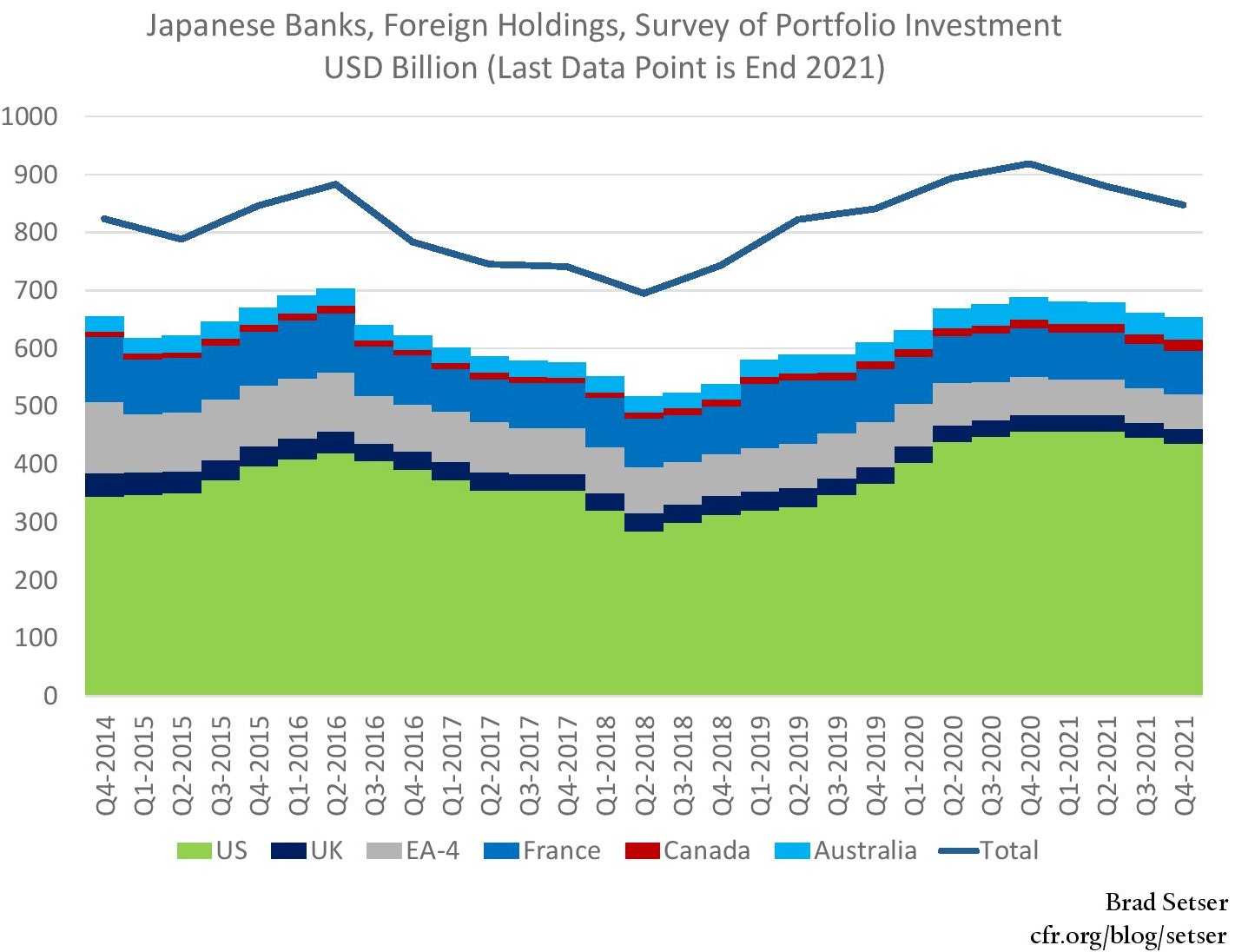

They held about $850 billion in foreign bonds going into 2022, according to a coordinated survey of portfolio investment by the International Monetary Fund (IMF). That included almost $450 billion in U.S. bonds and $75 billion or so in French debt—a number which far exceeds their holdings of the bonds issued by the other large countries in the euro area.

Unsurprisingly, the banks’ holdings fell sharply over the course of 2022 as the banks largely invest on a hedged basis. Between significant sales, the fall in the dollar value of U.S. bonds, and the even bigger fall in the dollar value of European bonds, the commercial banks’ holdings were under $600 billion in the latest Japanese net international investment position data.

But rather than using, say, 3 month cross-currency swaps to hedge, Japanese banks have historically funded the bulk of U.S. bond portfolio in the repurchase agreement, or “repo”, market. It was, more or less, a straightforward carry trade—one that clearly became unprofitable as the Fed started to raise short-term rates and the curve flattened and then inverted. In the past, Japanese commercial banks have reacted quickly to changes in the shape of the U.S. curve: they haven’t been big net buyers of foreign securities over the last ten years (when Post Bank, which isn’t in the banking data, is set aside) and they have generally actively managed their investment portfolio.

The banks also have a foreign loan book of around $1 trillion—a book that the banks appear to have maintained throughout 2022. Those loans are funded heavily with dollar deposits. In the face of regulatory pressure, they have termed out their cross-currency swap funding for their loan book (see Figure IV-4-3 of Japan’s October 2022 Financial Systems Report). Those longer-dated liabilities helped limit the immediate impact of the U.S. interest rate shock on the banks’ external loan book, providing a bit of time for the interest rates on the loans to reset.

Finally, it is worth noting that while the banks are mostly hedged, some banks have speculated on the foreign exchange market by adjusting their hedge ratio. In 2022, that generally helped the banks, as the increase in the value of the dollar (relative to the yen) offset falls in the market value of dollar bonds (from the rise in US rates). See Chart IV-3-6 of the October Financial System Report

The second class of large institutional investors is Japan’s large set of deposit taking institutions that are not commercial banks.

Japan Post Bank, Norinchukin (the cooperative bank for farmers, foresters and fisherman), and the Shinkin (regional cooperative) banks collectively held close to a trillion dollars of foreign bonds at their peak.

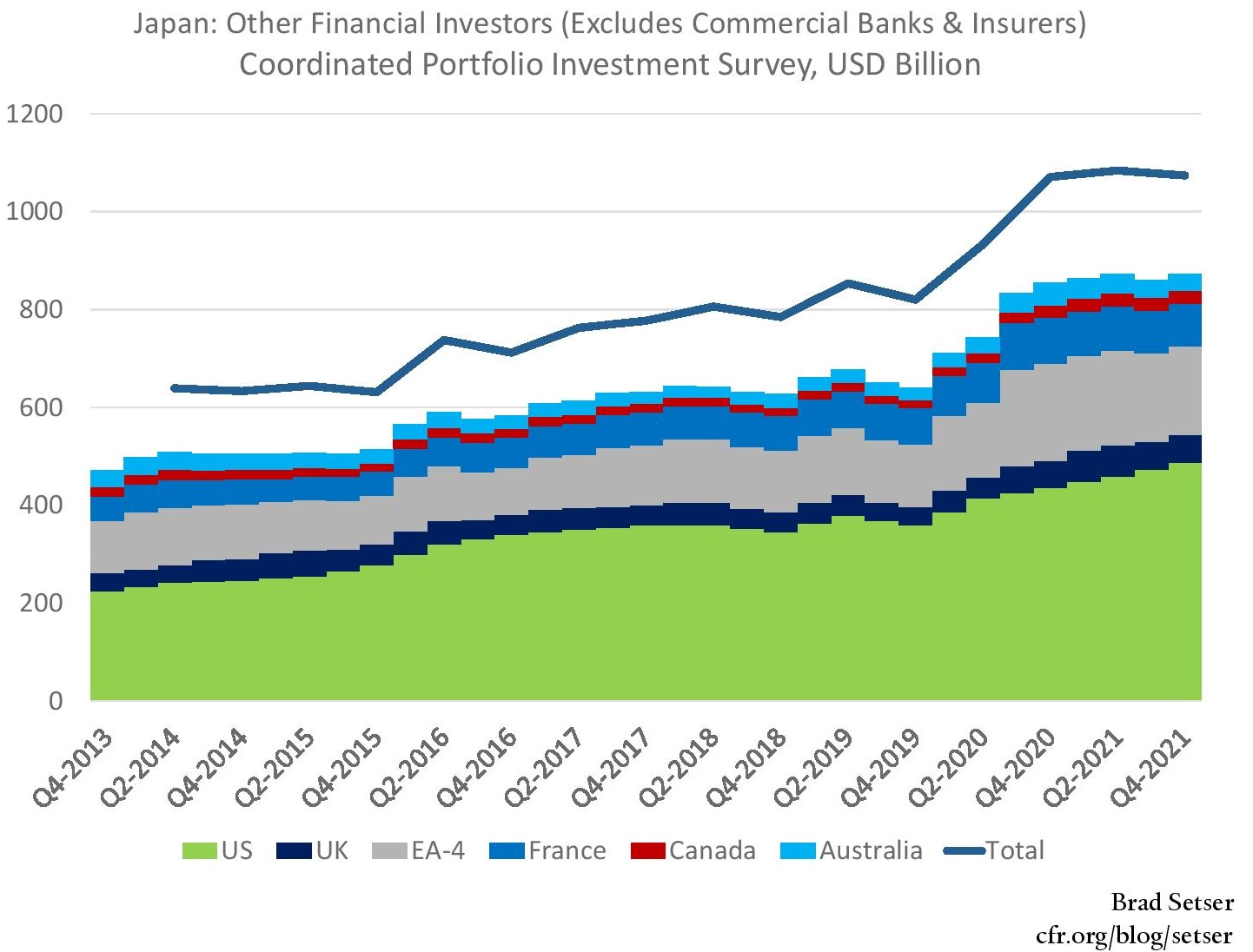

But one quirk of the Japanese data is that these institutions’ large bond portfolio does not appear primarily in the data for “banks.” Both Postbank and the Shinkin Banks (and their “central bank”, Shinkin Central) hold enormous sums in “investment trusts” that are outside the formal data for the foreign bond holdings of Japanese banks. Norinchukin, which reports more direct holdings of foreign bonds, isn’t considered a standard commercial bank for regulatory purposes either. As a result, these institutions appear in the Japanese data under the unhelpful category of “other financial institutions” (which includes an important line item for “trusts”; for more see the April 2021 Financial System Report).

We know this in part because the Japanese data shows that all net purchases of foreign bonds between 2010 and 2020 came from financial actors outside the commercial banking system. The purchases of these institutions tend to appear in the line items for securities firms and for “trust accounts” (both subcomponents of the flow from “other financial institutions”).

We also know this because the holdings of foreign bonds by “other financial institutions” exceed the holdings of the banks or the insurance sector in the IMF’s coordinated survey of foreign portfolio investment (the IMF data lags the Japanese data; the last data point is the end of 2021).

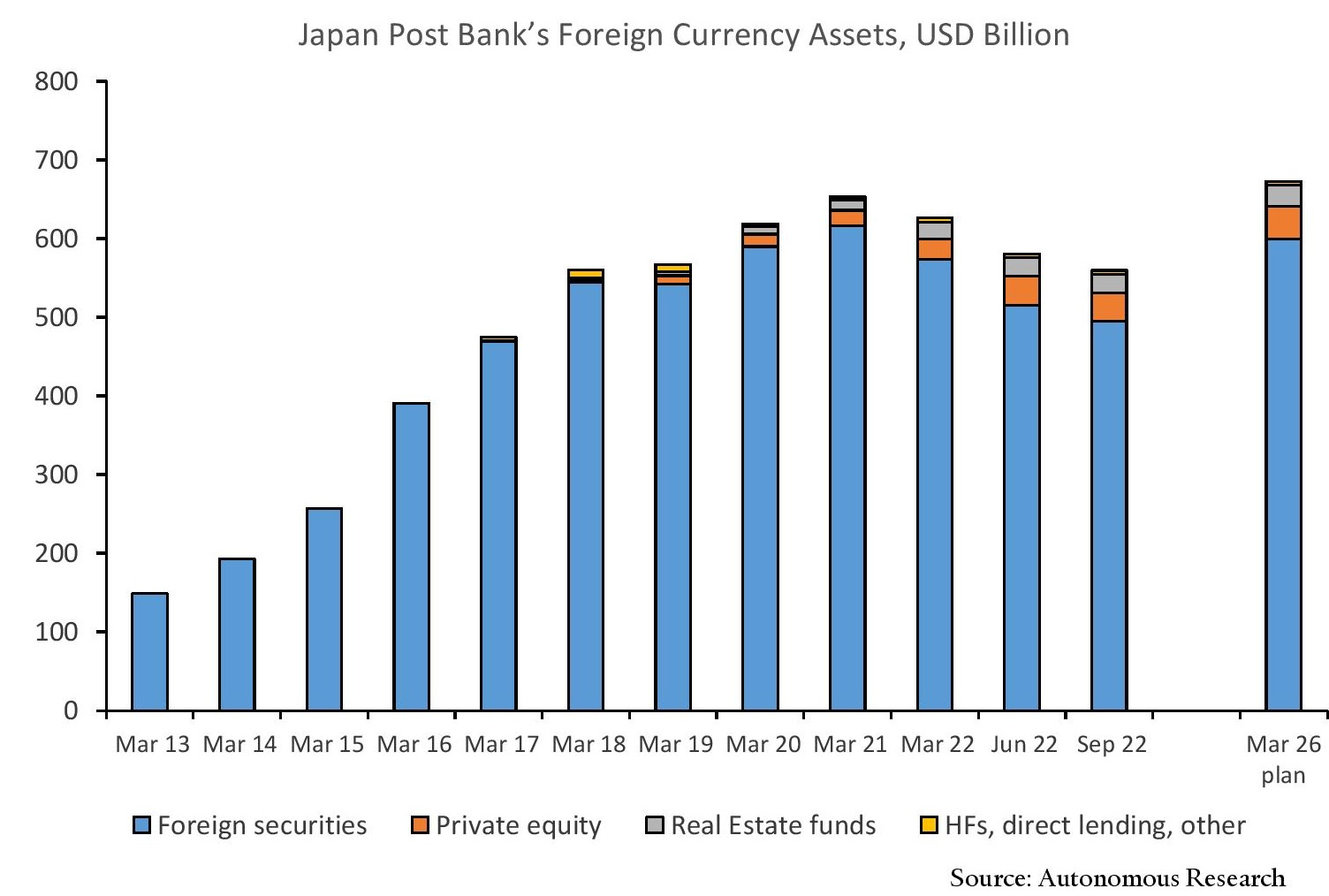

Post Bank is by far the single biggest holder of foreign bonds in Japan apart from the Ministry of Finance. Its latest disclosure (for September 2022) shows that it holds $200 billion in bonds directly on its balance sheet, and $400 billion of investment trusts that are primarily invested in foreign bonds (the investment trusts also include some private equity and real estate funds; see slides 7 and 10). Even with the slump in global bond markets, Post Bank’s total investment in foreign bonds is likely close to $500 billion.

Autonomous Research has shown that Post Bank’s foreign holdings increased particularly rapidly between 2014 and 2018. Post Bank thus drove a large portion of the increase in Japan’s total holdings over that period.

Norinchukin is only slightly smaller than Post Bank. It holds close to $230 billion in securities on its own balance sheet, along with $60 billion in investment trusts (Annual report, p. 15). That portfolio famously includes around $45 billion (down from a peak of over $70 billion; see slide 11) in dollar and euro collateralized loan obligations (CLOs). But, unfortunately for Norinchukin, its holding of fixed rate bonds far exceeds its holdings of variable rate CLOs. Norinchukin also reports, unsurprisingly, that its bond portfolio is now significantly under water—even though it does not need to realize any actual losses simply from market moves. The Shinkin banks are also big holders of foreign bonds, according to Japan’s financial systems report. Their pooled central investment funds report a $40 billion foreign bond portfolio, according to Autonomous Research, and Japan’s Financial Systems Report shows that the individual Shinkin banks are also heavily exposed to investment trusts (Chart III-1-15).

Given the structure of their liabilities, these institutions naturally should hedge the bulk of their foreign currency risk. Post Bank, for instance, historically has hedged the bulk of its portfolio. As a result, there is little doubt that these institutions, along with the insurers, are heavily dependent on continuous access to the swaps market. But mostly hedged isn’t totally hedged: in 2022, the foreign currency gains from the small unhedged book helped offset their mark-to-market losses on their foreign bonds. Going forward, they stand to take further losses in the unlikely event that the dollar falls, and U.S. yields continue to rise.* (See Chart IV-3-10 in the October 2022 Financial System Report).

Going forward, these institutions are in a particularly difficult position. They cannot sell their existing bond holdings without realizing losses and they cannot really run an unhedged book and a large open foreign currency position given the structure of their liabilities. They also need to hold their investment trusts to maturity to avoid realizing losses. Consequently, they will take a hit to their income as hedge costs rise above the interest rate on their legacy foreign currency portfolios. Their only real strategy for limiting losses is to reinvest the funds from maturing government bonds into higher yielding corporate debt, or to unwind hedged investments as they mature and return to the Japanese government bond market.

The last big category of primarily hedged investors are Japan’s large life insurers.

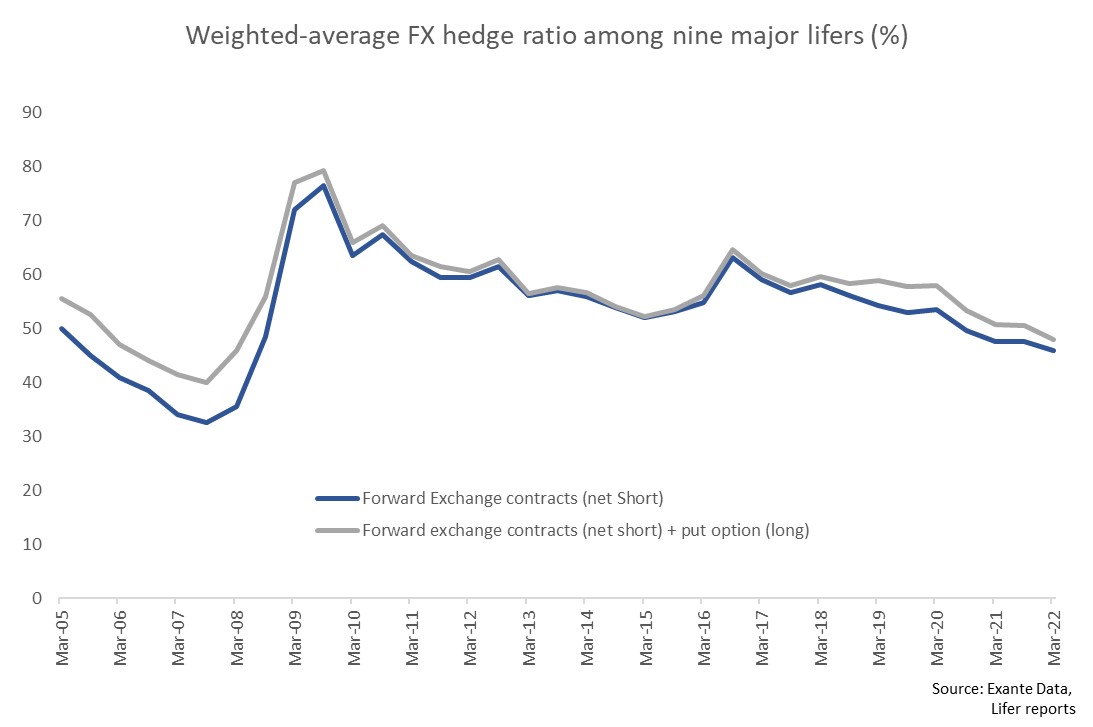

Life insurers held around $740 billion in bonds at the end of 2021 (the coordinated investment survey; the life insurance association number, which includes foreign equities, showed $970 billion in foreign assets at the end of 2021). The Japanese Financial System Report (Chart III-2-4) indicates that the insurers hedge about 60 percent of their foreign securities at the end of 2021; the disclosed data from a smaller subset of insurers tracked by Exante Data suggests that this hedge ratio fell over the course of 2022 (as the insurers took on more foreign exchange risk to avoid losses on their existing foreign securities book).

Either way, the insurers hold a substantial portfolio of both hedged and unhedged bonds—and they have already started to adjust this portfolio in response to the large change in the cost of hedging in 2022.

The Japanese balance of payments data clearly shows that the life insurance sector has turned into a net seller of foreign bonds from March 2022 onwards (Financial Systems Report, Chart III-2-5), with sales of around $35 billion over the last 12 months.

The October Financial System Report expresses clear concern that certain insurers are reaching for yield in the corporate debt market. The U.S. balance of payments data also shows signs that some Japanese investors have increased their exposure to corporate credit risk as Japanese investors have in aggregate sold Treasury and Agency bonds this year while buying corporate bonds. Exante Data has also found evidence that some Japanese investors are shifting toward higher yielding debt inside the euro area, for similar reasons.

One final point: the details of the survey of foreign portfolio investment show that the lifers have been particularly keen investors in Australian bonds. The insurers collectively held 8 percent of their portfolio in Australian debt securities at the end of 2021—well above the 4-5 percent share of the banks.

Pensions are the final major category of institutional investors. Critically, this is the only sector that primarily invests on an unhedged basis. The most important investor in this group by far is Japan’s massive GPIF. After raising its foreign bond portfolio from 15 to 25 percent of total assets, the large GPIF holds $340 billion in foreign bonds unhedged. Other pension funds often follow the GPIF’s lead.

Incidentally, the strong Japanese demand for foreign bonds observed in late 2019 and over the course of 2020 was very clearly the result of the GPIF’s increased allocation to foreign bonds. That flow naturally tapered off in 2021, as it was fundamentally driven by a one-off shift in the GPIF’s portfolio, and it wouldn’t normally be expected to change significantly in response to short-term market shifts.

Relative to other Japanese investors, the pensions appear to hold a relatively diversified portfolio of euro area bonds, with less concentration in French bonds than Japan’s banks.

Thanks to GPIF’s large unhedged book and the MoF’s foreign reserves, the bulk of the Japan’s unhedged investment in foreign bonds is actually held by Japan’s government. The combined unhedged bond investments of the life insurance sector and the private pension funds are significantly smaller than the combined $1.3 trillion (at end of the third quarter bond valuations) held by the MoF and the GPIF.

Implications for the Future

What does this institutional detail imply for the forward-looking risks to the global market stemming from Japan?

Two points stand out.

One is that hedged Japanese investors have already been reducing their exposure to foreign bonds. The banks have significantly reduced their total exposure and the lifers have already turned into net sellers. For insurers and other long-term investors, long-dated Japanese government bonds are already attractive relative to the hedged return on investment grade foreign bonds. An acceleration of these sales could potentially disrupt these sales globally—if, for instance, a big institution was forced into a fire sale of its foreign bond portfolio. Such a fire sale could come from an inability to sustain losses on “negative carry” positions (higher cost of borrowing than return on the long-term investments) in a legacy portfolio. It could also result from losses on other (perhaps even domestic) positions that forced a general reduction in risk or—least likely—the loss of access to foreign currency funding (see the April 2020 and October 2020 Financial System Reports).

The second is that it would take a very substantial upward move in Japanese long-term interest rates to eliminate the interest pickup unhedged investors can now get on their foreign investments. The rise in Japanese rates that will occur if yield curve control is adjusted further has to be compared against the rise in U.S. and European rates that has already taken place.

The global economy has already adjusted to a slowdown in Japanese institutional fixed income demand—Japanese investors have gone from buying about $100 billion a year of foreign bonds on average over the last ten years to selling close to $200 billion in 2022.** The impact of the swing has been mitigated by the fact that Japanese investors have a stronger incentive to sell safe, relatively liquid U.S. government bonds rather than less liquid U.S. corporate bonds. But it is still a real swing that has had an impact on a range of markets—one that was likely compounded by MoF (and other reserve manager) sales in Q3 2022.

The scale of these sales has also been mitigated by the reality that a very large share of total Japanese holdings is held in portfolios that can effectively hold bonds to maturity. Most investment trusts, for example, are held to maturity, with losses only realized when the trusts mature. The Bank of Japan is worried that institutions will lose the buffer that mark to market gains on securities provided in the past, as voluntary sales of bonds that had appreciated in value over time could be used to generate income to offset losses elsewhere.*** But it isn’t yet worried (we think) about involuntary sales forcing the premature realization of losses—a possibility that would likely only materialize if access to dollar and euro funding dried up.

The truly catastrophic scenarios for the global market would likely require a large acceleration of these sales, and the rapid unwinding of the $2 trillion plus foreign bond portfolio that Japanese institutional investors still hold. Such an unwind would likely stem from the intersection of unexpected risks: say, if an important set of Japanese investors bet too aggressively on the persistence of low long-term rates and face capital losses in their holdings of Japanese government bonds at the same time they are bleeding income on their hedged holdings of foreign currency bonds.****

The Bank of Japan has emphasized (hopefully correctly) that Japanese banks hold many bonds in their hold-to-maturity book and have substantial flexibility about the timing of the realization of any mark-to-market losses on their available for sale portfolio. The Bank of Japan also insists that Japanese pension funds haven’t engaged in the kind of levered derivative bets on Japanese bonds that got British funds in trouble. There is always a risk of an overlooked pocket of leverage that generates a fire sale. However, the most likely outcome in 2023 is a continuation of the roll down in Japanese holdings of foreign bonds observed in 2022, as the large pool of hedged Japanese investors allow maturing bonds to roll off at par rather than reinvest abroad. That more mundane reality still implies the large flow into global fixed income from Japanese institutional investors over the last decade will dwindle to a relative trickle.

*/ The Ministry of Finance sold $20b of foreign exchange in September, and $40 billion in October. The U.S. data suggests that the MoF sold more bonds in September than October, as it built up liquidity in anticipation of the October intervention. The data presented here generally excludes the MoF’s sales, as reserves are reported separately from other flows in the balance of payments.

**/ Japan looks set to retain a modest current account surplus in 2023, thanks to the significant earnings from Japan’s large stock of foreign direct investment and Japan’s still large foreign bond portfolio (interest income on the unhedged portfolio of MoF, the GPIF and the pensions should increase significantly over time). However, Japan’s current account surplus has historically been balanced by FDI outflows, not net bond outflows (over the last ten years Japanese purchases of foreign bonds have been almost equal to foreign purchases of Japanese bonds, a fact that reinforces the argument that the bulk of Japanese purchases over this time period have been hedged in the swaps market).

***/ Section V of the October Financial System Report includes a stress scenario linked to a deeply inverted U.S. curve. Post Bank has reported a large reduction in the unrealized gains in its bond portfolio, and Norinchukin has disclosed that a significant portion of its bond portfolio is now under water at current market prices. Antonio Foglia, in an interesting article in the Financial Times, suggested that mark-to-market losses on U.S. bonds could, strangely, drive dollar strength, as currency hedged investors would need to buy dollars to offset the mark-to-market loss on bonds to assure that they had sufficient funds to cover the roll off their FX swaps. Such dynamics could have contributed to the yen’s dramatic fall in 2022, but scope of such dynamics likely was also limited by the large number of Japanese investors that are able to avoid realizing losses by holding bonds to maturity.

****/ For a detailed evaluation of the risks associated with holding fx-hedged bonds to maturity, see the blog Concentrated Ambiguity.