Germany Cannot Quit Fiscal Consolidation

Fiscally Driven Rebalancing Turns Out to Be Hard

Germany looks poised to continue to run a (general government) fiscal surplus of about 1 percent of GDP this year. And there is reason to think that the underlying fiscal position of the German government is a bit stronger than the headline numbers imply, as a one-off energy payment pushed the federal balance into a (tiny) deficit in the first half of the year.

If the results for the first half continue in the second, Germany’s surplus may be a bit higher than 1 percent of GDP. That will throw a lot of projections off. The IMF thought the general government surplus would be just under a half point of GDP this year (thanks to a 0.6 percentage point of GDP structural fiscal expansion). And since Germany is a big part of the eurozone, and without the projected German expansion, the eurozone’s overall fiscal stance also will be a bit tighter than expected (see paragraph 29 and figure 5 of the IMF’s assessment of the Eurozone).

That means that German fiscal policy won’t be supporting either internal rebalancing in the eurozone (a fall in Germany’s surplus that helps support a rise in the surpluses or fall in the deficits of Germany’s eurozone trade partners) or global rebalancing. Germany, remember, runs a current account surplus of about 8 percent of its GDP.

Eurozone demand growth has been solid this year and private demand has shown real momentum, so Germany’s likely fiscal “miss” won’t necessarily derail the eurozone’s recovery. But it still matters. It makes it less likely that the eurozone’s growth will spill over to the world through a reduction in the eurozone’s current account surplus. And it would be nice if Europe would now, during its recovery, repay the rest of the world for the negative demand and trade spillovers that went along with the second dip in the eurozone’s double dip recession.

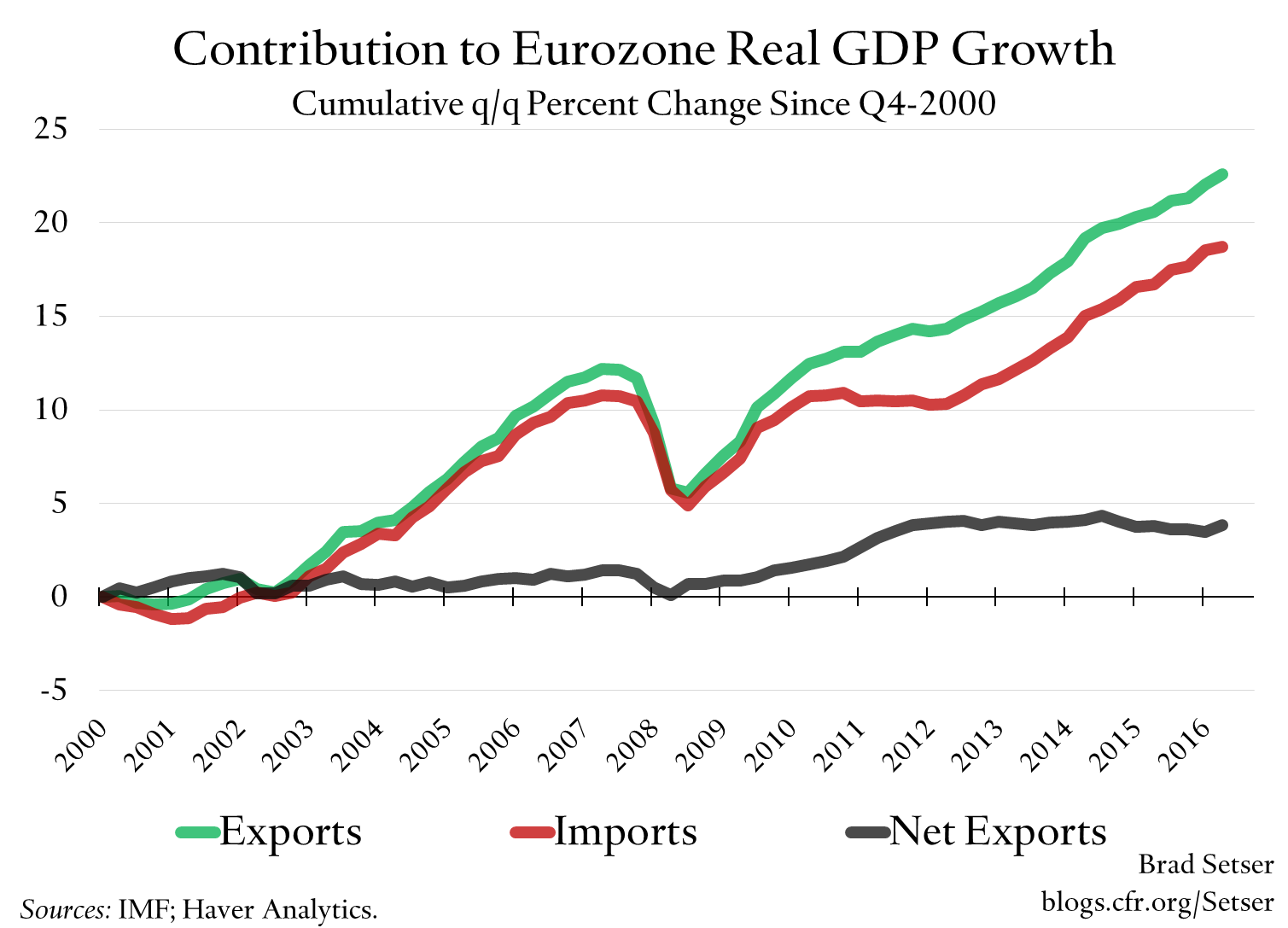

Remember, from 2010 to 2013, net exports contributed quite significantly to eurozone growth (the sum of contributions from net exports over this period totaled 2 percentage points of eurozone GDP)—pushing up the eurozone external surplus.

And it highlights a broader point. Using fiscal policy to drive rebalancing turns out to be quite hard. With the surplus countries posing particular problems.

For two reasons.

One, countries that run fiscal and external surpluses generally seem to like their current policy mix, and don’t want to change it.

Germany falls in this category. The IMF forecasted that Germany’s fiscal surplus would go away in 2016. It didn’t. The IMF doubled down and forecasted the fiscal surplus would go away in 2017. So far it hasn’t. The 2017 structural fiscal surplus is currently almost 1.5 percentage points of GDP larger than the IMF forecast two years.

Korea falls in this category too. Its general government surplus in 2016 was—according to the latest External Balance Assessment (see table 3)—almost 2 percent of its GDP. In its annual assessment last year, the IMF projected it would be “only” 1 percent of GDP. Korea’s new prime minister is talking a good game right now – but I still worry that the new government’s fiscal plans also may be less than they seem—annual stimulus packages often do little more than offset the rolloff of past stimulus, and the investment banks aren’t currently forecasting a change in Korea’s borrowing requirement. Remember, Korea runs a big surplus in its social security system (about 2.5 percent of GDP, see table 4 in the IMF’s Article IV), so the general government can be in surplus even with headline fiscal deficits.

The Netherlands too. It has continued with its drive to get to fiscal balance even when the IMF argued that fiscal consolidation was not necessary—the Dutch have little fiscal debt—and cyclically counterproductive (the Dutch recovery from the global crisis has been far weaker than the German recovery).

And two, the largest important external surplus countries also run large fiscal deficits, and thus policies that reduce fiscal risk work against external rebalancing.

I am of course thinking of China and Japan.

Japan’s external surplus is around 4 percent of its GDP. And Japan runs a sizeable external surplus even with a fiscal deficit of around 4 percent of GDP. It you take the estimated impact of fiscal deficits on the current account from IMF’s baseline model (the fiscal coefficient is now 0.47), moving to fiscal balance would raise Japan’s current account surplus by 2 percent of GDP, to around 6 percent of its GDP.

China’s external surplus officially is between 1 and 2 percent of its GDP—but the IMF now recognizes that it is likely understated by about a half point of GDP (see paragraph 3 here). Tourism. (Anna Wong of the Fed staff thinks the mismeasurement is more like 1 percent of China’s GDP). China’s fiscal deficit is officially around 4 percent of GDP, but the IMF thinks China’s fiscal deficit is mismeasured in China’s official statistics: the so called “backdoor” (local government financing vehicles and SOEs that fund public investment) hasn’t really been closed. The IMF puts China’s real fiscal balance at just over 12 percent of China’s GDP (with around 2 percentage points of the deficit financed by land sales not by borrowing).

Think about that for a minute. A country with a 12 percent of GDP fiscal deficit is running an external surplus. Usually that kind of fiscal excess leads to an external deficit. If the fiscal deficit were reduced by 10 percentage points of GDP, the IMF’s coefficient for estimating the impact of fiscal policy changes implies that China’s external surplus would rise by between 4.5 and 5 percent of its GDP. So with the kind of fiscal and credit consolidation some want, China’s external surplus might be 6 or 7 percent of its GDP (to make it real: a trillion dollars…)—unless, of course, off balance sheet fiscal consolidation is combined with some serious policy changes to lower savings.

It is quite common now to note that trade imbalances are a function of the balance between national savings and national investment, not a function of good (or bad) trade deals.

But it turns out to be quite hard to go from that observation to a coherent set of policy recommendations that would change savings and investment balances in a way that would bring existing imbalances down.

I do think the IMF is trying. Its last Article IV really highlights Germany’s external surplus. The latest Article IV for Japan clearly calls for Japan to delay the consumption tax increase in 2018 and prioritize demand support (to help the BoJ meet its inflation target) rather than fiscal consolidation in the next few years (the BoJ needs a bit of help from fiscal policy if its ever going to meet its inflation target). Its Article IV for China argues that China has fiscal room to support consumption as it scales back on its credit driven stimulus, and advocates for a serious increase in social benefits and transfers to low-income workers to reduce national savings (paragraph 16 of the staff report is excellent).

But at the end of the day, the IMF is only calling for a pause in fiscal consolidation: Its long-term fiscal recommendation for China, Japan, and the eurozone is still for a consolidation that would raise national savings and thereby would be expected to raise the current account surpluses of all three.*

In Japan, the IMF wants Japan to eventually move toward fiscal balance to put its debt-to -GDP ratio on a clear downward trajectory, which implies a long-term fiscal consolidation of around 4 percent of GDP. And it still recommends that this consolidation occur through consumption tax increases, even though such tax hikes have a history of killing demand growth.

In China the IMF argues that the current fiscal trajectory is unsustainable even taking into account the favorable dynamics created when nominal interest rates are much lower than nominal growth (also true in Japan by the way). The optimal lopng-term headline fiscal deficit in the External Balance Assessment is about 1 percent of China’s GDP, which implies a needed contraction of around 3 percentage points over time—and I think it is fair to say that the Article IV calls for a larger—though gradual—cut in the augmented fiscal deficit.

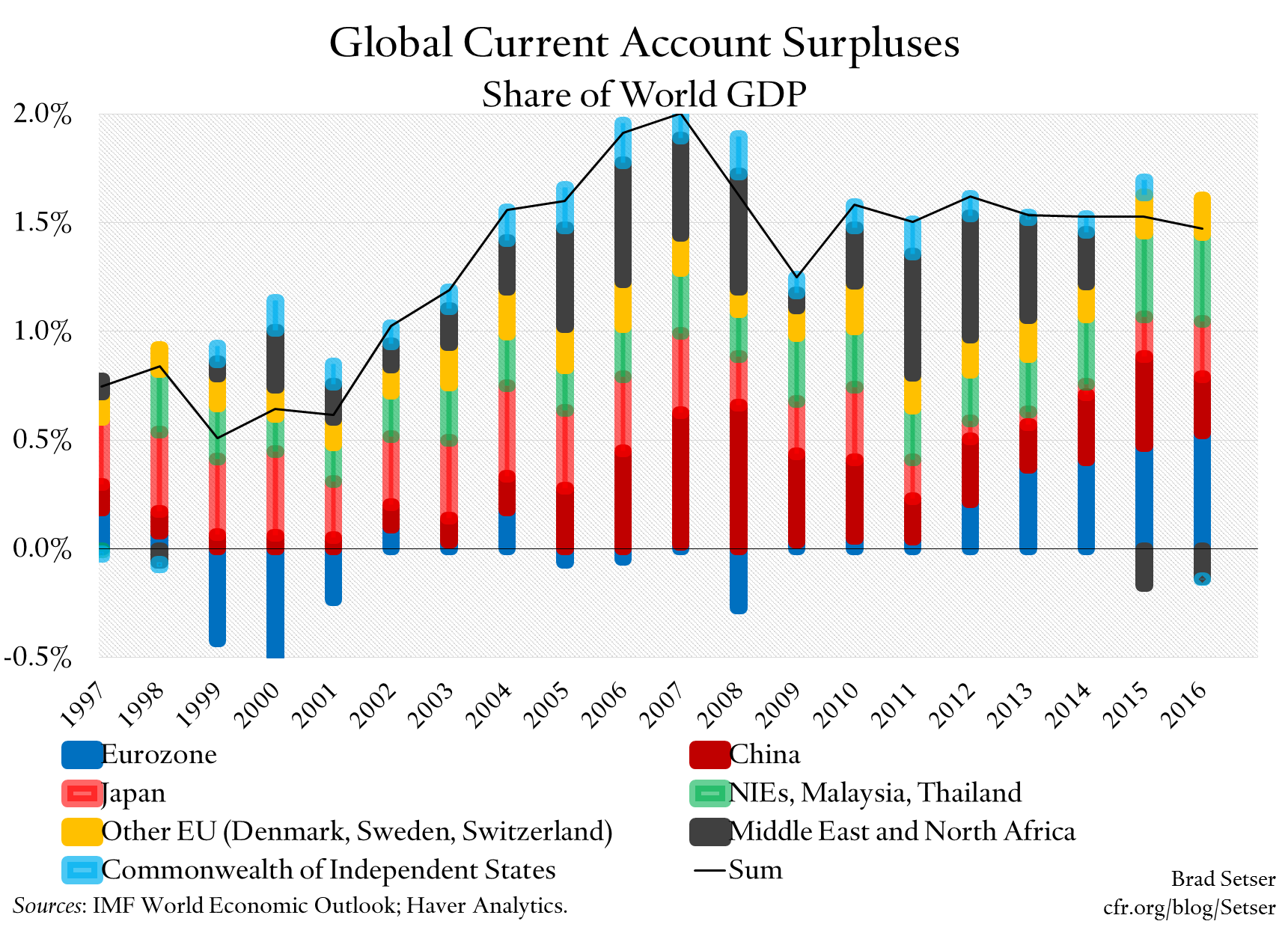

And in the eurozone, the IMF wants another half point or so of additional fiscal consolidation—even though the eurozone’s structural fiscal deficit is only about one percent of its GDP now.** China, Japan, and the eurozone combined are over a third of world GDP, and collectively have a current account surplus of about 1 percent of world GDP. A fiscal consolidation in all three that would raise their national savings (or in China’s case reduce public investment) creates a pretty big headwind to global rebalancing.

Of course, it takes two to tango—imbalances are a function not just of policies that influence the savings and investment balance of the big surplus countries but also the policies that shape the savings and investment balance of the big deficit countries.

So external imbalances could fall over time even if the big “surplus” countries are reducing their fiscal deficits and raising their national savings (or in China’s case, cutting public investment) if the big “deficit” countries cut their fiscal deficits faster than the big surplus countries.

That though would mean that rebalancing could come through policies that in aggregate slow global demand growth, and introduce a deflationary bias to the global economy.

Not precisely what I would recommend. But it is hard in practice to come up with policies that support global demand and lower imbalances at the same time if the three biggest surplus regions in the world economy all need to adopt contractionary fiscal policies.

Back to Germany. The IMF, in its latest Article IV, argues that fiscal policy “gaps” explain about 1.5 percent of Germany’s “excess” current account surplus.

That is a bit deceptive. The IMF wants all of Germany’s trade partners, more or less, to engage in fiscal consolidation. France. Italy. Spain. The UK. The U.S. China. Japan. India. Saudi Arabia. Mathematically it is pretty hard to offset consolidation in all these countries with (small) fiscal expansions in Sweden, Switzerland, and Korea.

As a result, excessive fiscal spending elsewhere accounts for about half of the fiscal policy gap that the IMF identifies for Germany (see the first box in the IMF’s staff report for Germany).

The other half more or less comes from Germany’s own tight fiscal policy—as the IMF thinks Germany should run a deficit of a half point of GDP rather than a surplus of a point. The IMF thinks Germany should be running a fiscal deficit of about 0.5 percent of its GDP, not a surplus of around 1 percent of its GDP.

One final point. It may seem like all of this is a criticism of the IMF’s external sector report. It isn’t. Without the external sector report, it would be next to impossible to test the global consistency of the IMF’s policy recommendations. The EBA modeling exercise has turned out to be quite valuable—even if the coefficient on foreign exchange intervention in the EBA model is way too low (because of the interaction with capital account openness, it typically is between 0.05 and 0.15), so the model has focused all attention on fiscal policy gaps. The ESR process has turned out to be far more useful than the G-20’s mutual assessment process—which probably should be scrapped. Not all policy innovations work out.

* One small point. The IMF doesn’t always forecast that fiscal consolidation will raise the surplus of surplus countries by the amount that might be expected. Look at the long-term fiscal and external forecast for Japan (table 5 here): a two percentage point of GDP fiscal consolidation is not raising the current account by the percentage point that the IMF’s model would suggest. The forecast for China is more consistent, as the IMF doesn’t foresee any real fiscal consolidation and it thus forecasts the current account surplus to be more or less constant.

** Thanks to a set of debatable technical adjustments that have been made to the IMF’s model (raising the contribution of aging to the current account surplus above the basic estimate that emerges from the underlying model), the IMF now believes that the current account “norm” for the eurozone is a surplus of three percent of GDP—more or less what we have now. Before those adjustments, the current account norm for the eurozone was lower—around one percent of the eurozone’s GDP in the 2014 model , around 2 percent in the 2015 model. These technical adjustments make it easier for the IMF to propose further fiscal consolidation in the eurozone, as the fiscal consolidation doesn’t open up a big current account gap.