How Durable is China’s Rebalancing?

I increasingly suspect my view on Chinese “rebalancing” is at odds with the current consensus (or perhaps just with a plurality of the investment bank analysts and financial journalists who watch China).

In two significant ways.

One. I think China’s balance of payments position is fairly robust. In both a “flow” and a “stock” sense. The current account isn’t that close to falling into a deficit (and it wouldn’t be that big a deal if China did have a modest deficit). And China’s state is back to adding to its foreign assets in a significant way. The days of “China selling reserves” are long past.

And two, I think the rebalancing that has lowered the measured current account surplus is more fragile than most think. It is a function of policies—call it a large off-budget “augmented” fiscal deficit or excessive credit growth—that some believe to be unsustainable, and many think are unwise. The IMF, for example, wants China to bring down its fiscal deficit and slow the pace of credit growth, policies that directionally would raise not lower the current account surplus.

I think these views are consistent—I tend to think that China’s current account surplus has come down by a bit less than many, but it has come down. Yet the way it has come down (through higher investment rather than a large fall in savings) doesn’t create confidence that it will stay down. China hasn’t embraced the set of policies needed for a more durable rebalancing, notably centralizing and expanding the provision of social insurance and creating a far more progressive tax system that relies less on regressive scoial contributions (payroll taxes).

Let me try to document both points.

The continued robustness of China’s balance of payments

The Economist has highlighted the deficit in China’s current account in the first quarter. The Financial Times has noted that China doesn’t appear to be intervening in the foreign exchange market (though one measure of intervention, FX settlement, did suggest someone was buying in April, rather surprisingly). Many—from the IMF to Paul Krugman—have emphasized that the bulk of the global balance of payments surplus is now found in aging advanced economies (e.g. not China).

I would highlight two competing points:

A: China’s manufacturing surplus remains large, and shows no sign of falling at current exchange rates.

China’s annual manufacturing surplus is still around $900 billion (for comparison, Germany’s manufacturing surplus is around $350-400 billion depending on the exchange rate and the U.S. deficit in manufacturing is around $1 trillion) and doesn’t show any sign of falling. I don’t see signs that the (modest) real appreciation this year will seriously erode China’s competitiveness—though it should moderate China’s export outperformance (Chinese goods export volumes grew at a faster pace than global trade in 2017).

China naturally will export manufactures and import commodities. Some surplus in manufactures is normal. And since it is now the world’s largest oil importer, its overall balance increasingly will swing with the price of oil. Every $10 a barrel price rise increases China’s oil and gas import bill by about $30 billion and pulls the surplus down by roughly that amount in the short-run (what matters for the current account is the price of oil relative to spending in the oil importing countries, but in the short-run, a rise in oil prices raises oil exporters income more than spending).

And China exports to manufactures to pay for its imports of “vacations”– though its deficit in tourism is almost certainly somewhat smaller than the inflated number in the official Chinese data.

No matter—China’s very real surplus in manufactures continues to provide real support for China’s overall balance of payments. And I have no doubt that China could slow the outflow of tourism dollars (or yuan) if it really was worried about its current account.

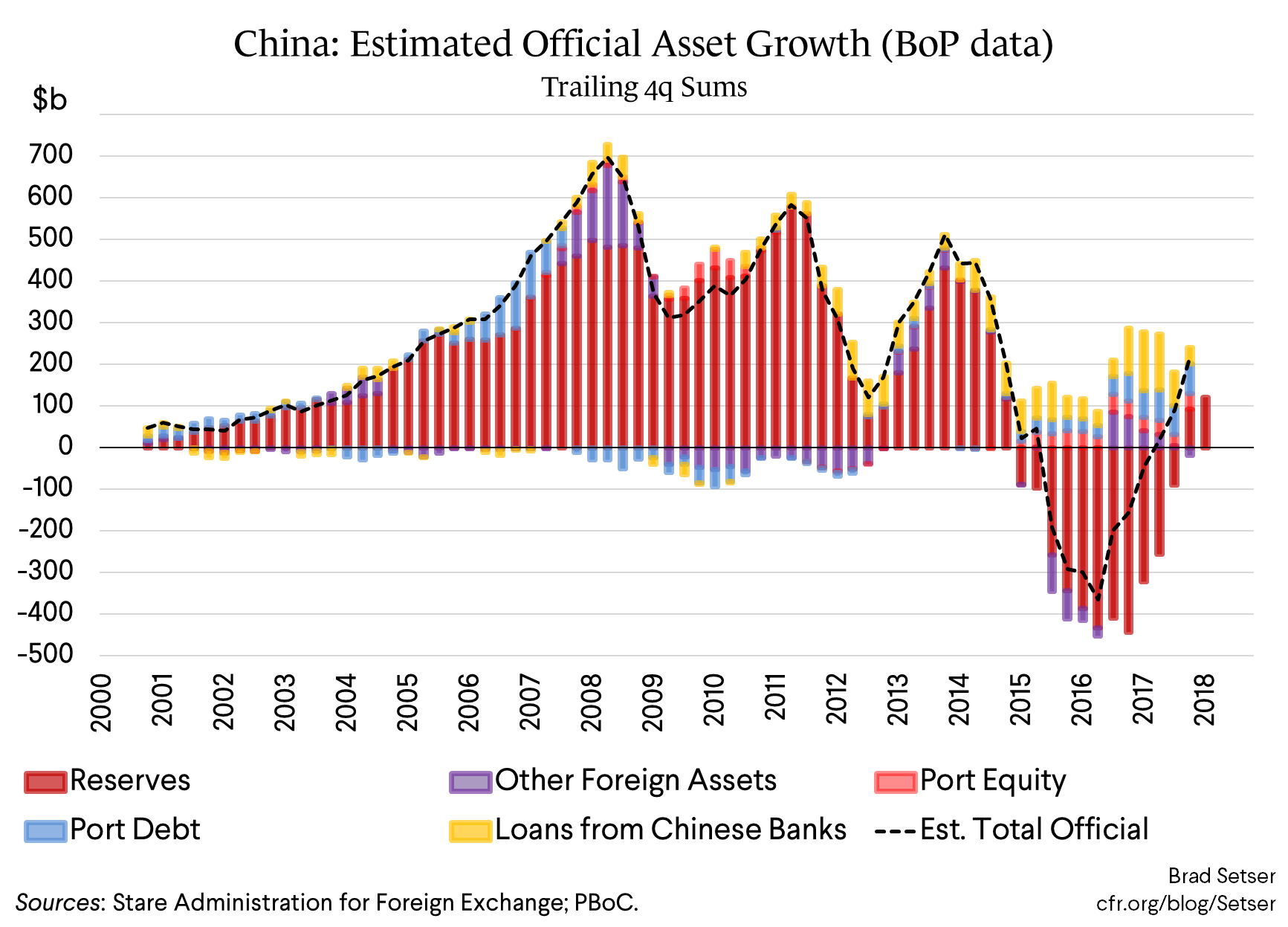

B: China is once again adding to its reserves.

A current account surplus would still be associated with weakness in the overall balance of payments if the surplus was smaller than needed to finance a large underlying pace of private capital outflows—as was the case after China’s 2015 devaluation/ cum depreciation. But here too I think China’s position is fairly strong. Net private outflows have fallen, and China’s state is again accumulating foreign assets.

To be sure, the reported foreign exchange reserves on the PBOC’s yuan balance sheet aren’t growing—and that’s an important data point.

But in the balance of payments, reserves are growing—they were up about $90 billion in 2017, and are up by $120 billion in the last four quarters of data. The discrepancy between the balance of payments and the PBOC’s balance sheet is a bit mysterious. Interest income is the most obvious explanation. Yet $120 billion in interest income seems a tad high, as it implies China has found a way to earn about 4% on its $3 trillion in reported reserves (though Trump’s fiscal policy should eventually make China’s interest income great again … as it should push up the interest rate the U.S. pays on its external debt).

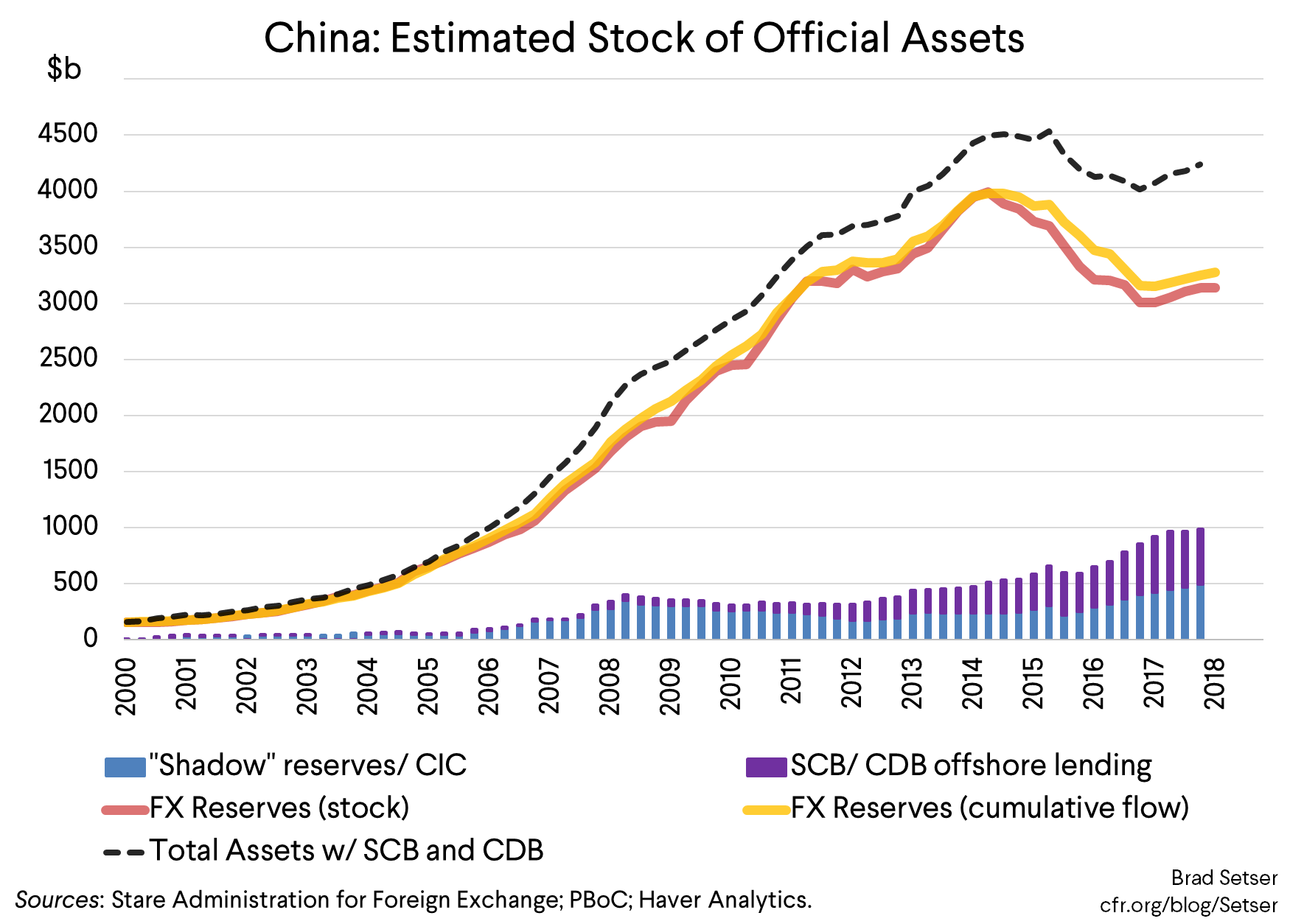

Broader measures of official asset growth that count lending by the state banks and the buildup of the foreign bonds held by the state banks and the foreign equity held by the CIC and China’s various social security funds show an even larger buildup. Full data isn’t yet available for q1, but there is no real doubt that the state banks have continued to add to their external portfolio (there is data on the foreign currency assets of the state banks).

To be sure, some of the foreign lending of the state banks is financed now by their borrowing from abroad—policy lending is no longer all about absorbing the current account surplus. That’s math—a $150 billion external surplus (2017 number) cannot finance both $90 billion in reserve growth (2017 number), $100 billion or so in state bank purchases of foreign bonds/policy lending, and $200 billion in outflows through errors and omissions. There is more going on.

But the big and growing balance sheet of the state bank system does provide China with lots of hidden scope to manage the exchange rate in subtle ways. The reported foreign currency assets of the state banks—bonds, and overseas loans—now top $600 billion; the balance of payments data if anything suggests a larger stock of offshore claims.

Sum it up, and China’s state continues to sit on the biggest pile of external assets in the world—and that pile has grown significantly in the past 18 months. By my measure that China’s state has well over $4 trillion in foreign assets, and its total holdings will be back to its pre-devaluation, pre-reserve fall level by the end of this year.

A small external deficit—say from an oil shock combined with a trade war with the U.S.—consequently shouldn’t put China’s exchange rate management at risk unless it creates expectations that Chinese policy makers now want a weaker exchange rate.

The fragile rebalancing

The argument that China’s rebalancing—the fall in its external surplus—is fragile is actually quite simple.

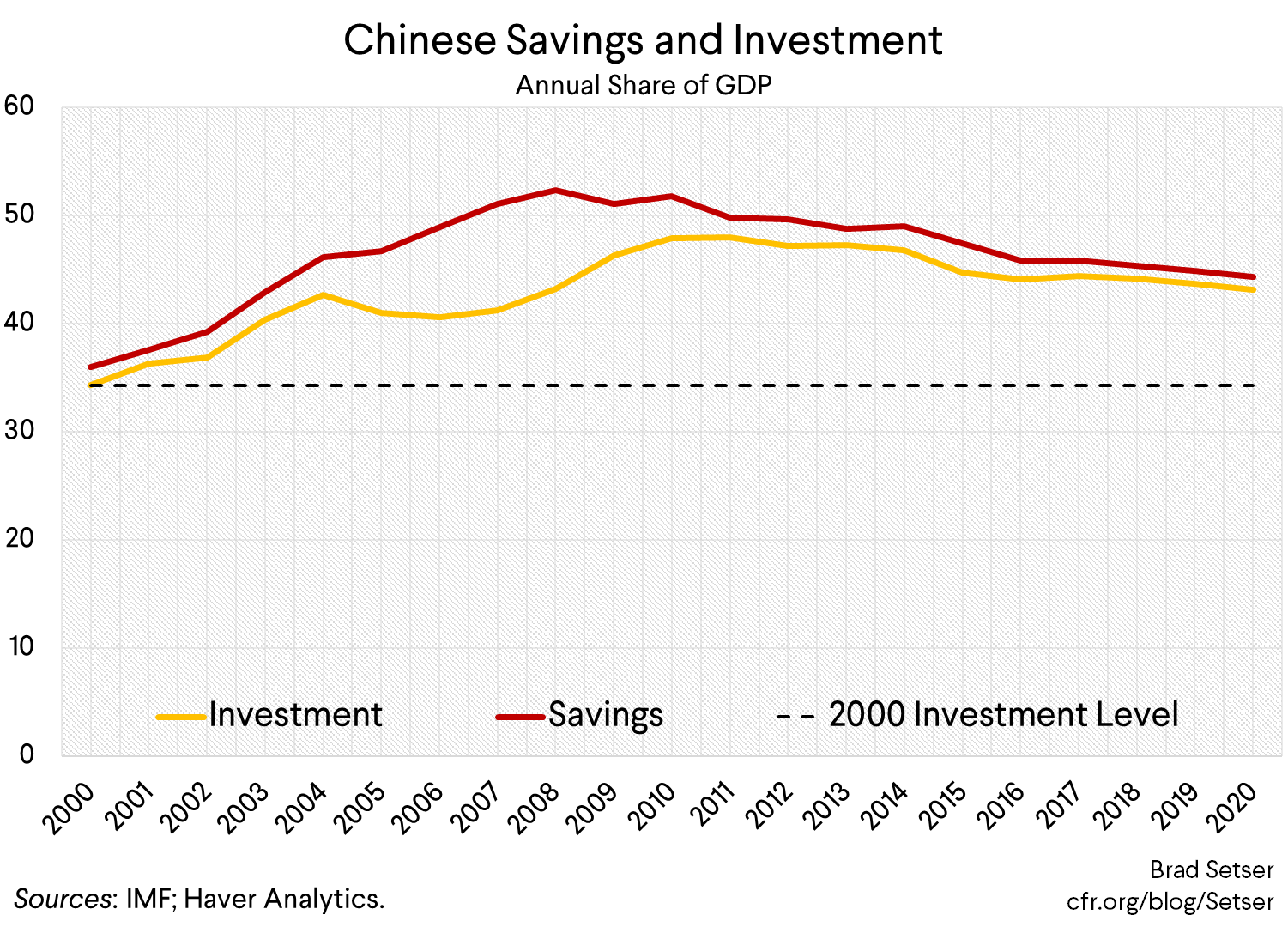

China still saves closer to a half of its GDP than a third of its GDP. And as long as that’s true, avoiding a large current account surplus takes rather exceptional policies, policies that look imprudent and dangerous as they will inevitably result in the buildup of internal debt (see Appendix 2 of the IMF’s 2017 staff report, among others).

Back in 2000, China was saving and investing around 35 percent of its GDP (the current account was in a modest surplus so savings was a tad higher than investment). In 2017 (and in 2018), even with the recent progress raising consumption, China is projected to save and invest around 45 percent of its GDP.

That’s a level of both savings and investment that remains about ten percentage points higher than in 2000. It is still a substantially higher level of savings and investment than has historically been found in high savings Asian economies (setting Singapore aside, as Singapore never disburses the wealth accumulated in Temasek and the GIC).

If investment were to fall back to its 2006-08 level of around 40 percent of China’s GDP and savings were to follow the IMF’s forecast, the current account in 2000 would be around 4 percent of China’s GDP, or well over $500 billion. Four percent of GDP doesn’t sound huge—but it would be a record current account as a share of the GDP of China’s trading partners.* And so long as savings is above 40 percent of GDP there is always a risk that the gap between saving and investment could be even bigger.

Yet the IMF—reflecting a global consensus—wants China to scale back the growth in its great wall of (internal) debt (yes, that was meant as a reference to Dinny McMahon’s book). The Fund—and many others—didn’t think China’s 2016 fiscal stimulus was a good idea, even though that fiscal stimulus likely played a key role in bringing China’s external surplus back under two percent of China’s GDP after the fall in the oil price.* It now wants “less public investment, tighter constraints on SOE borrowing, and [curbs on] the rapid growth in household debt.”

That’s the kind of policy recommendation that the Fund typically makes for a country with a large external deficit—it sounds completely reasonable for say Turkey. But for China, such a fall in domestic absorption would mean a return to a large external surplus—unless, as the Fund recognizes, it is accompanied by a serious effort to reduce savings and raise consumption.

Yet there is a risk that when China scales back what no doubt is an inefficient level of investment it will end up doing so without adopting the kinds of policies needed to bring down national savings. Neither Liu He nor President Xi has shown much interest in expanding China’s social safety net, or extending real social protection to China’s migrant workers.

This isn’t entirely a theoretical risk. Cutting public investment while residential investment was falling without providing policy support for consumption led to a sharp rise in China’s current account surplus in 2014 and 2015, though the full scale of the rise was masked by some shifts in how China measures its current account.

A policy agenda built around supply side reform (with Chinese characteristics) consequently scares me a little bit. So long as China saves so much, it also has an underlying problem with internal demand.

* If China’s current account surplus had remained constant at its 2007 level as a share of non-Chinese world GDP it would now be a bit over $400 billion (and China’s hasn’t far from that level in 2015 after adjusting for the inflated tourism number). If China’s surplus had remained constant as a share of China’s GDP at its 2007 level is would now be about $1.2 trillion. The choice of scale variable matters: China’s current account surplus could not have realistically remained at its 2007 level as a share of China’s GDP without causing tremedous global disruption.

** See for example paragraph 4 of the 2016 article IV staff report, and paragraph 4 of the 2017 staff report. The Fund was has been fairly clear (see paragrpah 8) that it viewed the substantial fiscal loosening between 2014 and 2016 (“general government net borrowing widened by 2¾ percent of GDP between 2014 and 2016, driving a similar increase in the “augmented” deficit which reached an estimated 12¼ percent”) as a mistake as it put China’s “augmented” fiscal deficit on an unsustainable trajectory.