Trade Deals or Macroeconomic Shocks?

With ongoing euro uncertainty in Italy, financial turmoil in Argentina and Turkey, and potential fiscal risks to demand in Asia, does the Trump administration’s focus on trade deals miss the larger macroeconomic picture?

The Trump administration, at least for now, is moving forward with tariffs on steel and aluminum imports from Canada, Mexico, and the EU. That is the most consequential measure to limit trade that the Trump Administration has taken so far—though it could be just the first of a sequence of trade restricting measures if the Adminsitration goes forward with the 301 case now that talks with China appear to have broken down.

The Trump Administration—particularly the President—believes that trade deficits are a function of bad trade deals, and has put all of its efforts into trying to renegotiate existing trade deals—China’s WTO accession, NAFTA and perhaps the series of GATT rounds that left the EU with a 10 percent tariff on autos.

The Trump Administration hasn’t focused, to put it mildly, on the macroeconomic drivers of trade surpluses and deficits.

But with new fears about Italy and a sell-off in some key emerging economies it isn’t hard to see how a set of global shocks and policy shifts could combine to push the U.S. trade deficit up even if the Trump Administration ends up striking a set of new, “good” trade deals.

- The market is putting pressure on high deficit, oil-importing emerging economies like Argentina and Turkey to adjust.

- The eurozone’s recovery remains fragile, and could easily be derailed by a bout of severe financial turbulence. A euro priced at a level that assures strong export-led growth in Italy would help reduce internal political tensions, but it also would lead, over time, to a further increase in the eurozone’s already large external surplus.

- And—a bit further off on the horizon—the fiscal tightening in Japan (there is a consumption tax hike on the table for late 2019) and quasi-fiscal tightening in China could weaken Asian demand, and push up Asia’s surplus (for any given oil price).

In all these cases, a weaker currency and exporting more is either necessary or potentially the path of least resistance.

And that, in turn, is partly a function of Trump’s fiscal policy.

Macroeconomically speaking, the U.S. can only avoid a rise in its trade deficit if the fiscal spur to demand in the U.S. is matched by strong demand growth elsewhere.

That in some sense is what happened last year, at least in the first three quarters of the year.* The fiscal loosening that was expected after Trump’s election took a while to materialize (it also ended up being bigger than expected). The Eurozone surprised to the upside, and the market, rather than focusing on the Fed’s ongoing tightening, was focused on the prospect that the ECB would eventually tighten too. The euro rose against the dollar—which helped a lot globally.

The Trump administration benefitted, in other words, from relatively benign global macroeconomic conditions.

Yet there seems to be a real risk that the happy macroeconomic constellation of 2017—a demand recovery in Europe (admittedly from a very weak starting point) and better-than-expected politics (notably in France), the lagged impact of the 2016 Chinese fiscal stimulus, the absence of any fiscal drag from Japan, and strong internal demand growth from at least a few emerging economies—may not persist much longer.

Oil-Importing Emerging Economies with Large Deficits

We know that a couple of emerging economies now face pressure to bring their external deficits down. Argentina and Turkey aren’t that big—their combined external deficit was somewhat under $100 billion. But they also won’t be contributing to global demand growth this year—and it’s possible that oil-importing emerging economies with stronger external fundamentals (like India, see the rather remarkable op-ed from the RBI’s governor in the Financial Times) will also need to adjust a bit. Weakness in emerging economies after the 2013 taper tantrum and the 2014 commodity shock contributed to both the slowdown in global trade in 2015 and a large rise in the United States non-oil deficit in 2014 and 2015.

Italy

The standard line is that Italy is both too big to bail out and too big to fail. Both ultimately cannot be true in the event of a real test—but the path that returns Italy to a stable political and financial equilibrium inside the eurozone isn’t yet totally clear.

Italy wants changes in the eurozone’s broader economic policy mix that would make it easier for Italy to grow. Italy’s partners by contrast have historically placed responsibility for Italy’s poor performance inside the eurozone on Italy’s own policy failings.*

A prolonged period of uncertainty while Italy and its European partners try to renegotiate (in effect) the terms of Italy’s eurozone membership could push the euro down. And, well, if the strains created by the eurozone’s combination of a monetary union with an incomplete fiscal union are resolved in part through a weak currency, well, that matters for the rest of the world economy. Euro weakness means dollar strength, and trouble for liability-dollarized emerging economies.

Over the Horizon: Fiscal Risks to Asian Demand

One of the lessons that I learned in 2014-15 was that swings in the euro-dollar can be amplified through their impact on China and the market’s assessment of the stability of its currency regime. China now manages its currency against a basket (more or less), and seems to have gotten a bit better at it—though the transition from a crawling peg against the dollar to what looks like a loose band around a basket was rocky.**

But we won’t really know how stable China’s new currency regime is before it is tested by dollar strength. And the real test will come if the dollar rises at a time of domestic weakness in China—as a slowing domestic economy would create a temptation on China’s part to allow the market to push China’s exchange rate down. And, well, China is now in a tightening cycle …

Japan doesn’t fit well into this dollar-centric narrative. But it is not too early to note that Japan is moving towards another round of consumption tax hikes in late 2019—and a new bout of fiscal tightening would only add to existing fiscal and monetary policy divergences among the major advanced economies. Consumption tax hikes historically have set back Japanese demand growth—and could make Japan more reliant on exports for growth and generate further weakness in the yen that puts pressure on the dollar-linked currencies in Asia.

Sum it all up. It isn’t hard to see how recent financial and macroeconomic developments could end up pushing the U.S. trade balance in the opposite direction Trump wants it to go. And it isn’t at all clear that his administration has internalized these risks.

* The non-oil trade deficit then jumped significantly in q4 2017. It then stabilized in q1 and looks perhaps to have fallen a bit in the first two months of q2. The monthly data though is notoriously volatile, and some retrenchment from the blowout in q4 isn’t really a surprise.

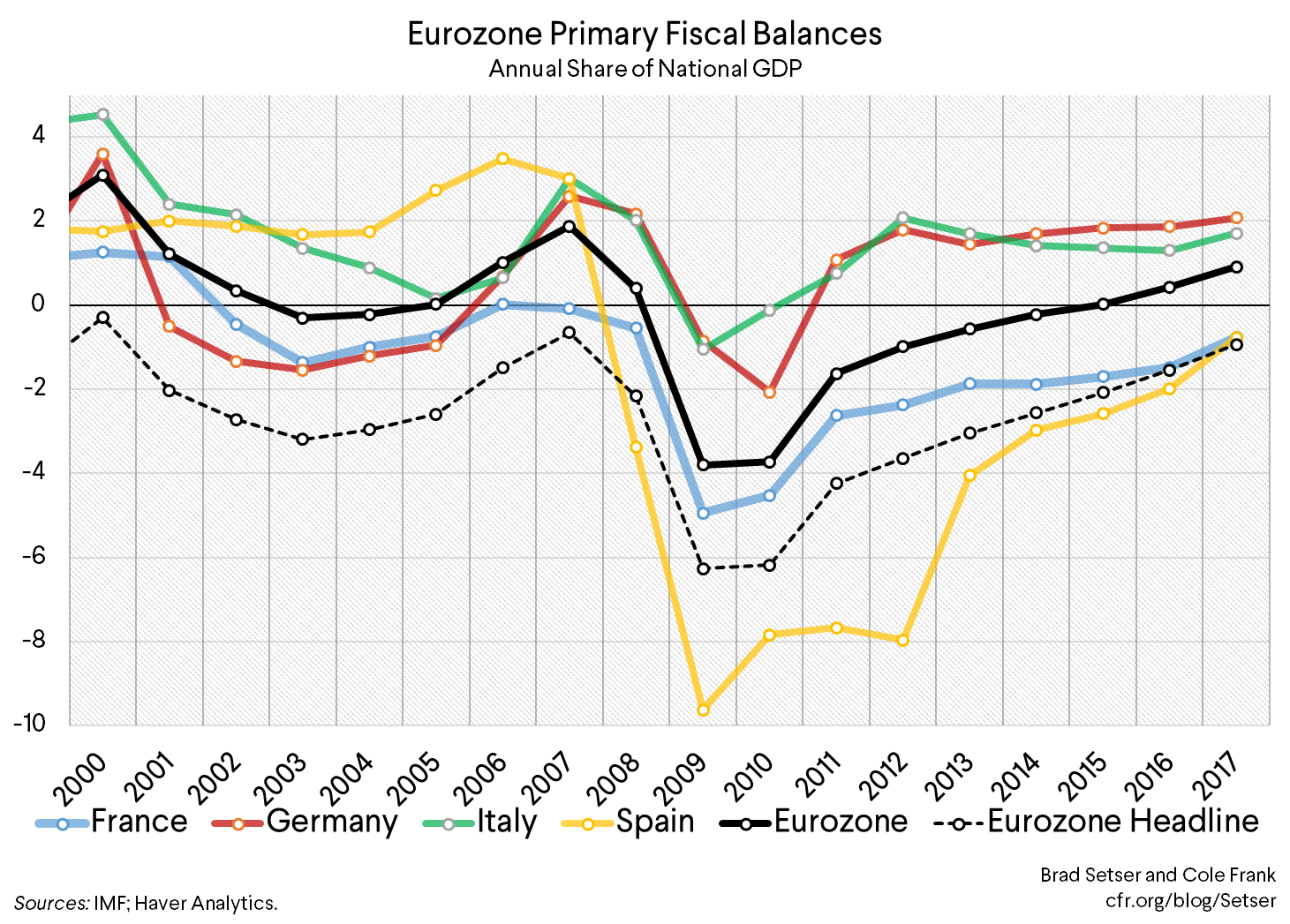

** On one level it is relatively easy to understand why Italy has rebelled against eurozone orthodoxy—it hasn’t grown for years, and faces the prospect of running an even tighter fiscal policy (its primary surplus is already around 2 percent of GDP, only slightly below that of Germany) going forward to comply with eurozone fiscal rules that require, at least in theory, Italy to bring its debt to GDP ratio down over time. On another level, an Italian rebellion against European rules poses far larger risks than Greece’s rebellion a few years back.

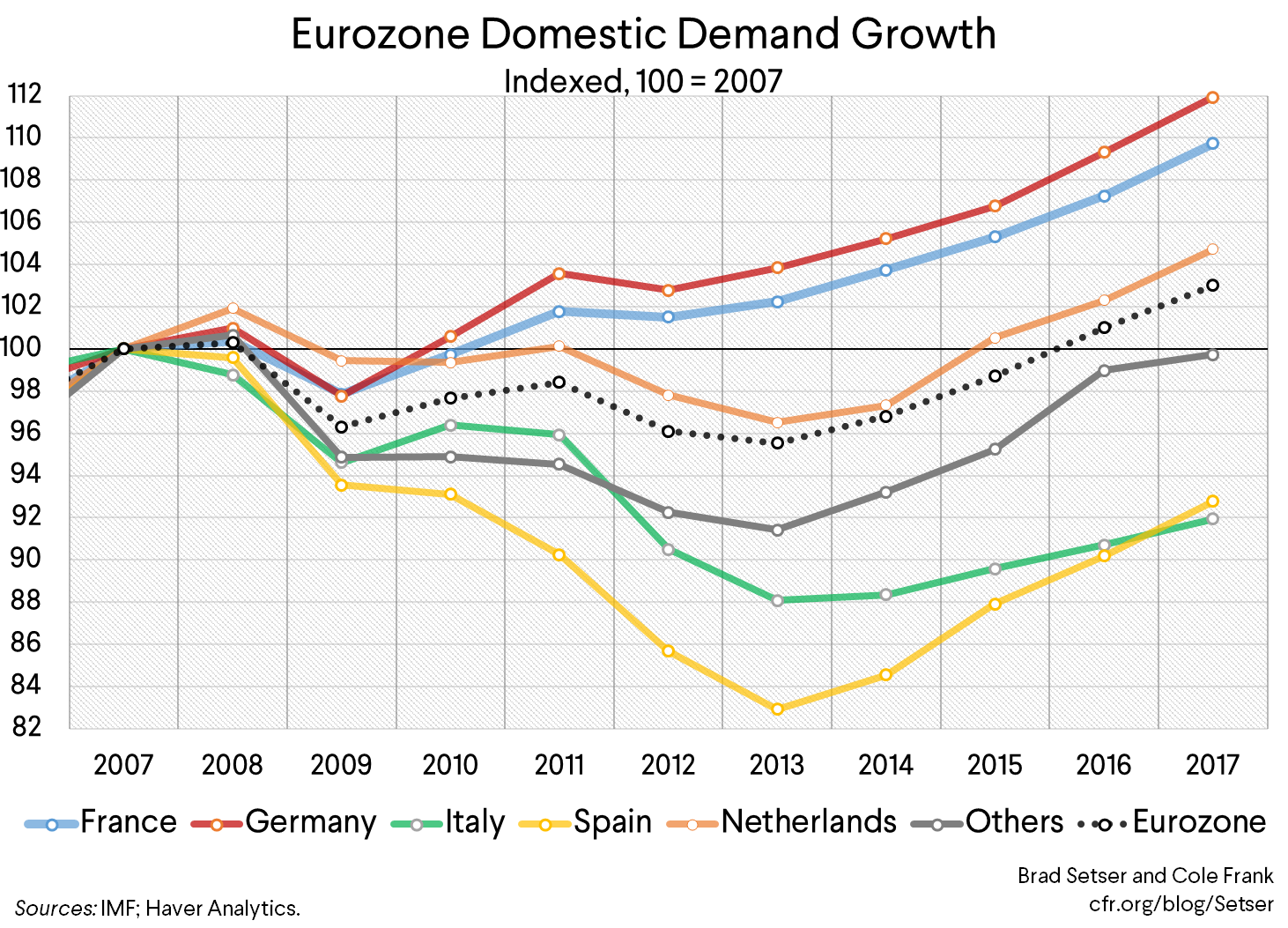

Italian demand has yet to recover from the 2010 to 2012 fiscal tightening.

*** China made its life more difficult by trying to combine a transition to a basket peg with a depreciation against the basket (and the dollar) in late 2015 and early 2016. Stability returned when it became clear that China didn’t want further depreciation against the basket. In fact China has allowed the yuan to creep up against the CFETS basket this year.