Looking Back at China’s 2019 Balance of Payments Data

Trump’s trade war didn’t really put a dent in China’s balance of payments. And China looks like it has the kind of external balance sheet needed to weather the corona virus shock. China has a lot of domestic debt, but it remains a pretty big global creditor.

Right now, there is—appropriately—a premium on looking forward. The world’s central banks and key financial institutions need to be preparing for the economic and financial fallout of the COVID-19 shock.

Looking back feels like a luxury.

But looking back sometimes can help policy makers look forward too. So hopefully there is still interest in China’s 2019 balance of payments

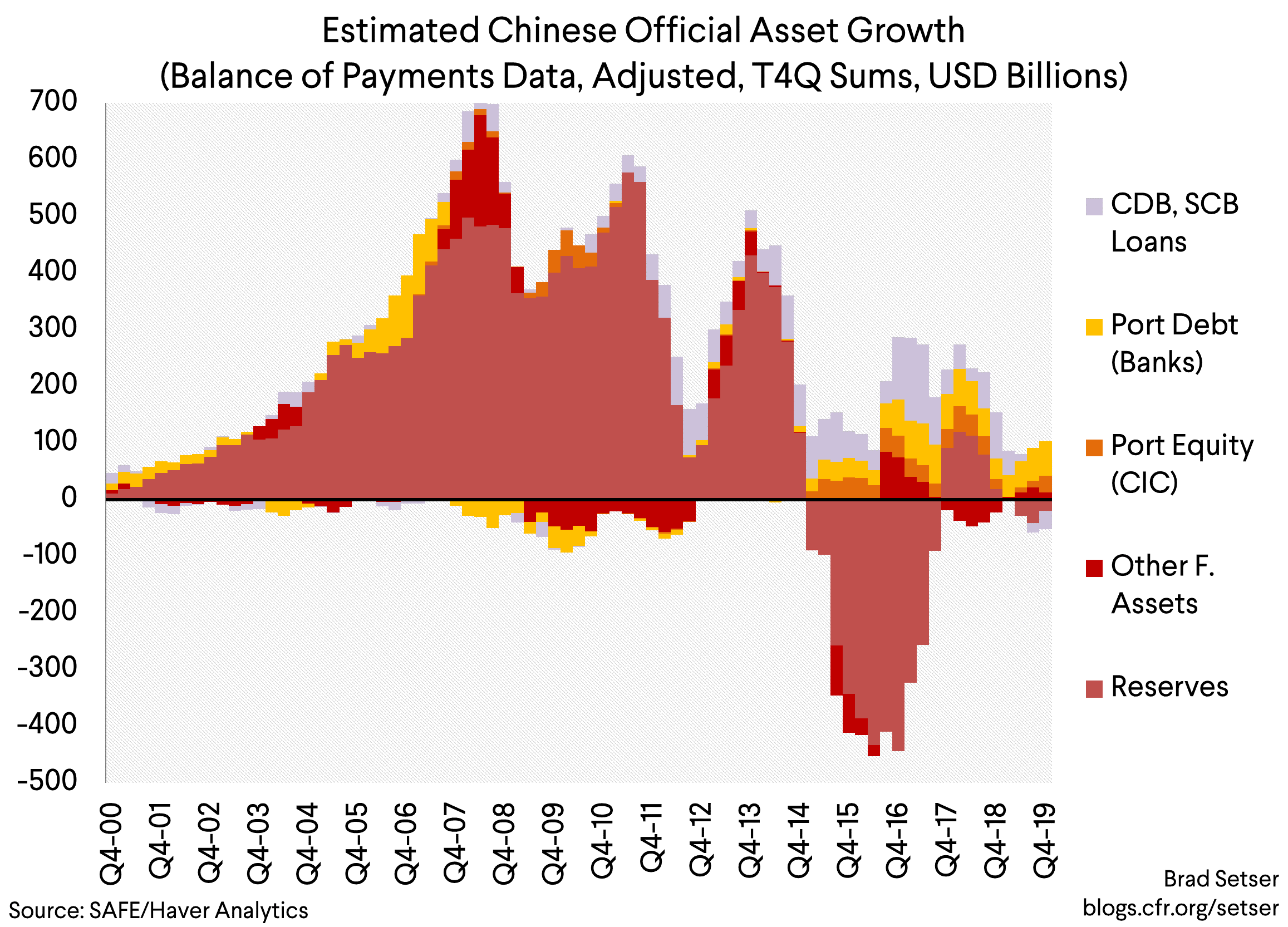

China was under a lot of stress in 2019 from the trade war. But its balance of payments stayed in relatively good shape. Much better shape than in 2015 or 2016. Reserves only fell a tiny bit, and by my calculation the total foreign assets of China’s state sector (PBOC, state banks, state investment funds) rose just a bit over the course of 2019.

And it’s possible that the resilience in China’s 2019 balance of payments may provide some clues for this year, even though the circumstances differ.

China stands to lose from the general contraction of global trade. But it is also the single biggest winner from lower commodity prices—and, how should I put it, less tourism also means many fewer opportunities for Chinese residents to move funds abroad.

So why didn’t China come under more balance of payments pressure during the trade war?

Four reasons, in my view.

The first is that the trade war was only with the United States, and China’s overall exports held up reasonably well. Not great, but exports to markets other than the United States continued to grow. With relatively weak imports, China’s measured trade surplus improved significantly over the course of 2019.

The second is that some of the measures China put in place back after the yuan scare of 2015 and 2016 worked. FDI outflows have fallen off in a sustained way, removing one source of pressure on the balance of payments

The third is that China actually did take some steps to help conserve foreign exchange in 2019—opening up to portfolio inflows (selectively) helped, but so did slowing the pace of external lending by China’s state institutions.

Finally, China’s balance of payments has always been in a better position than the alarmists claimed.

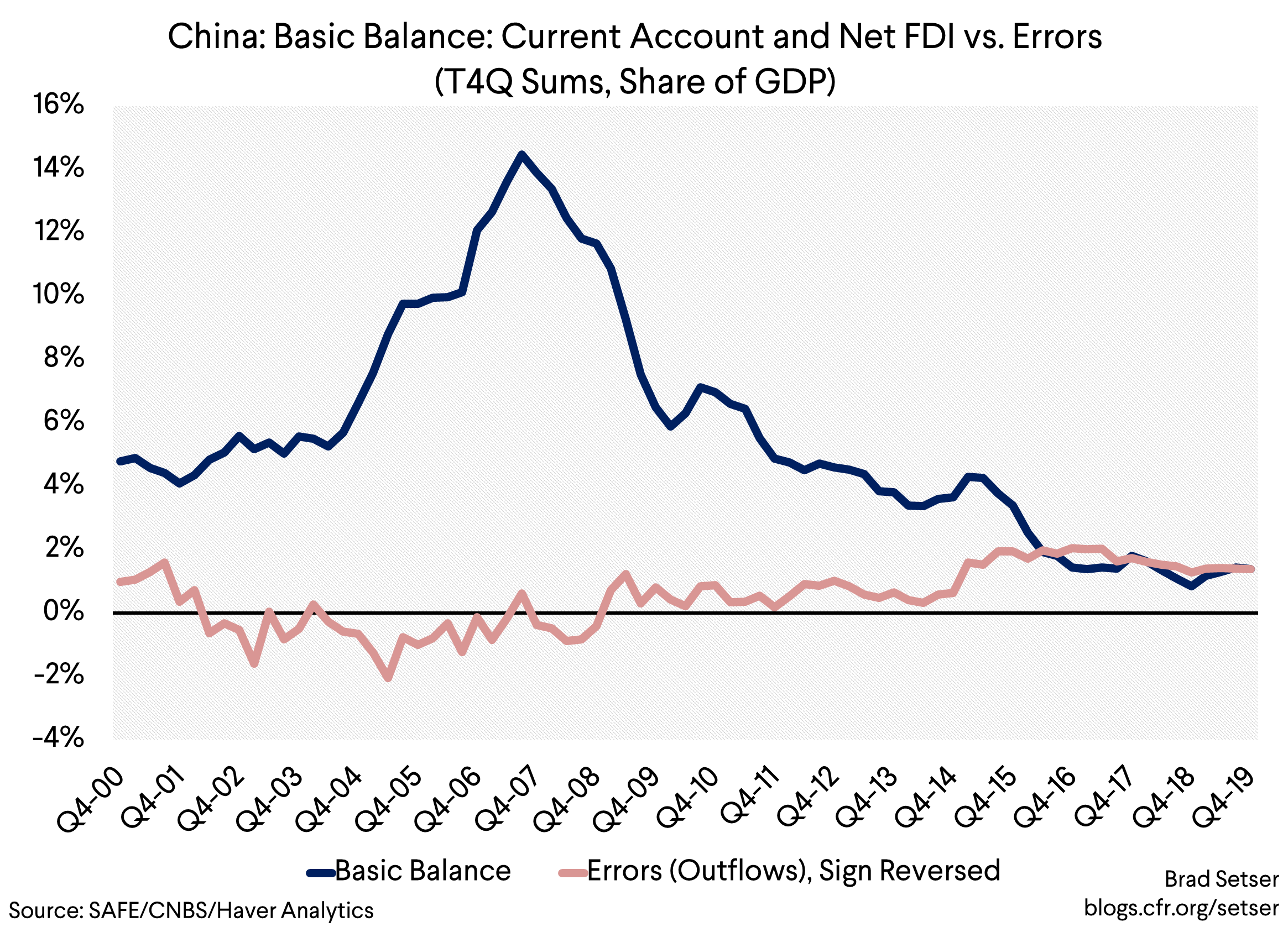

A high level of domestic investment and rapid domestic credit growth doesn’t mean a high level of external debt in a country with high savings. Thirty years of current account surpluses have created a large net foreign asset position—and much of the reserve fall in 2015 and 2016 was actually a shift in China’s foreign assets away from reserves towards (admittedly riskier) foreign loans. The leakages in the controls from tourism and errors and omissions over the last three years have basically been covered by the ongoing surplus in China’s basic balance (net FDI inflows from reinvested earnings and the current account)*

Let’s look at each point—

Trade

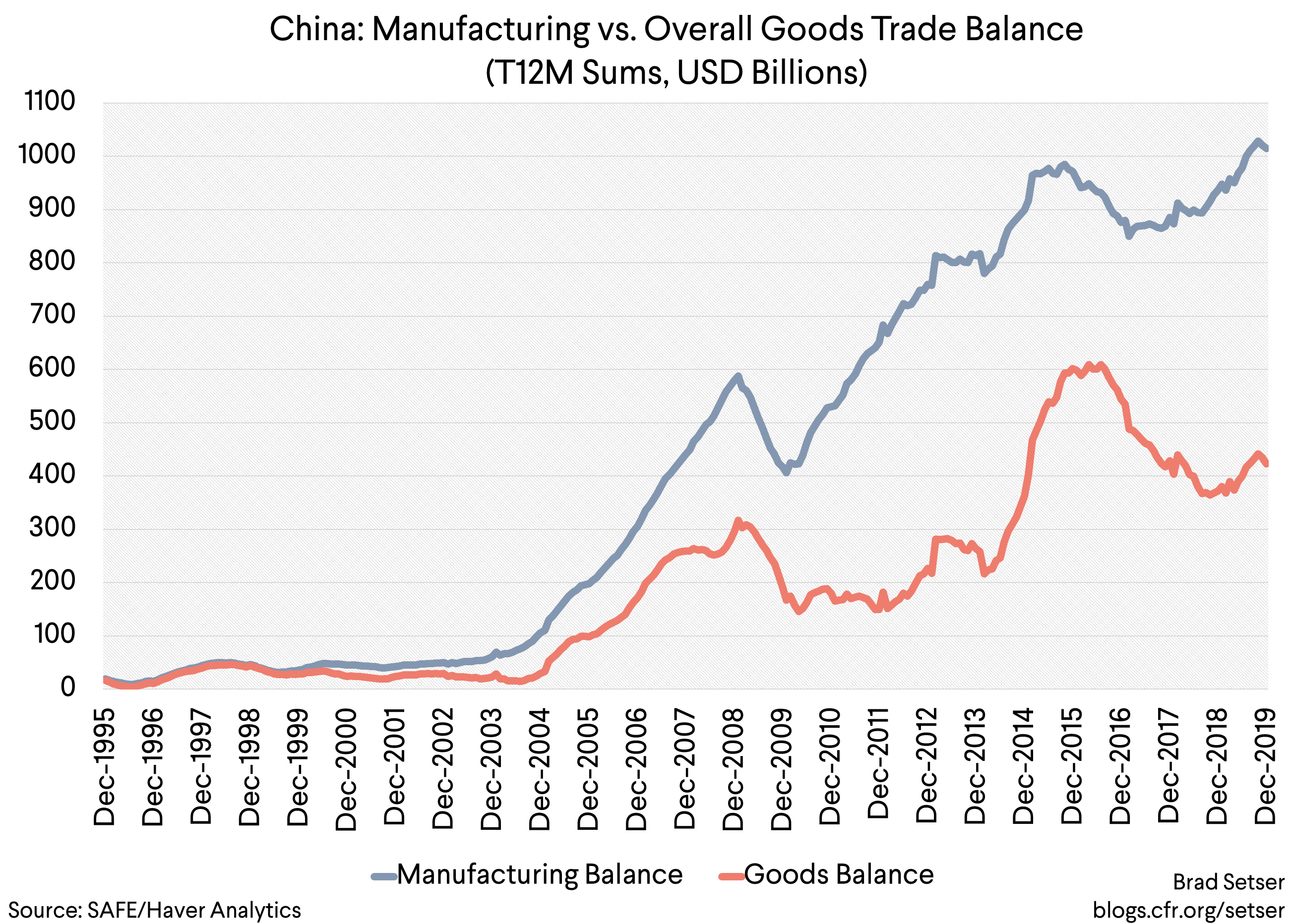

The United States is a far less important market for China now than it was twenty years ago—exports to the United States (judging from the U.S. import data, as the Chinese data is distorted here by flows through Hong Kong) are somewhere between a fifth and a quarter of total exports. Those exports fell enormously.

But China’s exports to the rest of the world rose, best I can tell. Overall manufactured exports were basically flat y/y in the fourth quarter. And with imports down, China’s surplus in manufacturing trade with its non-American trading partners rose substantially over the course of 2019, driving its overall trade surplus up.

At some point, this might have become an issue, but with Trump fighting trade skirmishes with everyone most of the world was more focused on what was happening to their trade with the United States.

There is another point here—for all the talk about how China has opened up to bond flows and the like, current account flows still dominate China’s balance of payments. This is something that some voices in the U.S. security establishment who think financial sanctions would provide the United States with significant leverage over China tend to overlook.

Foreign Direct Investment

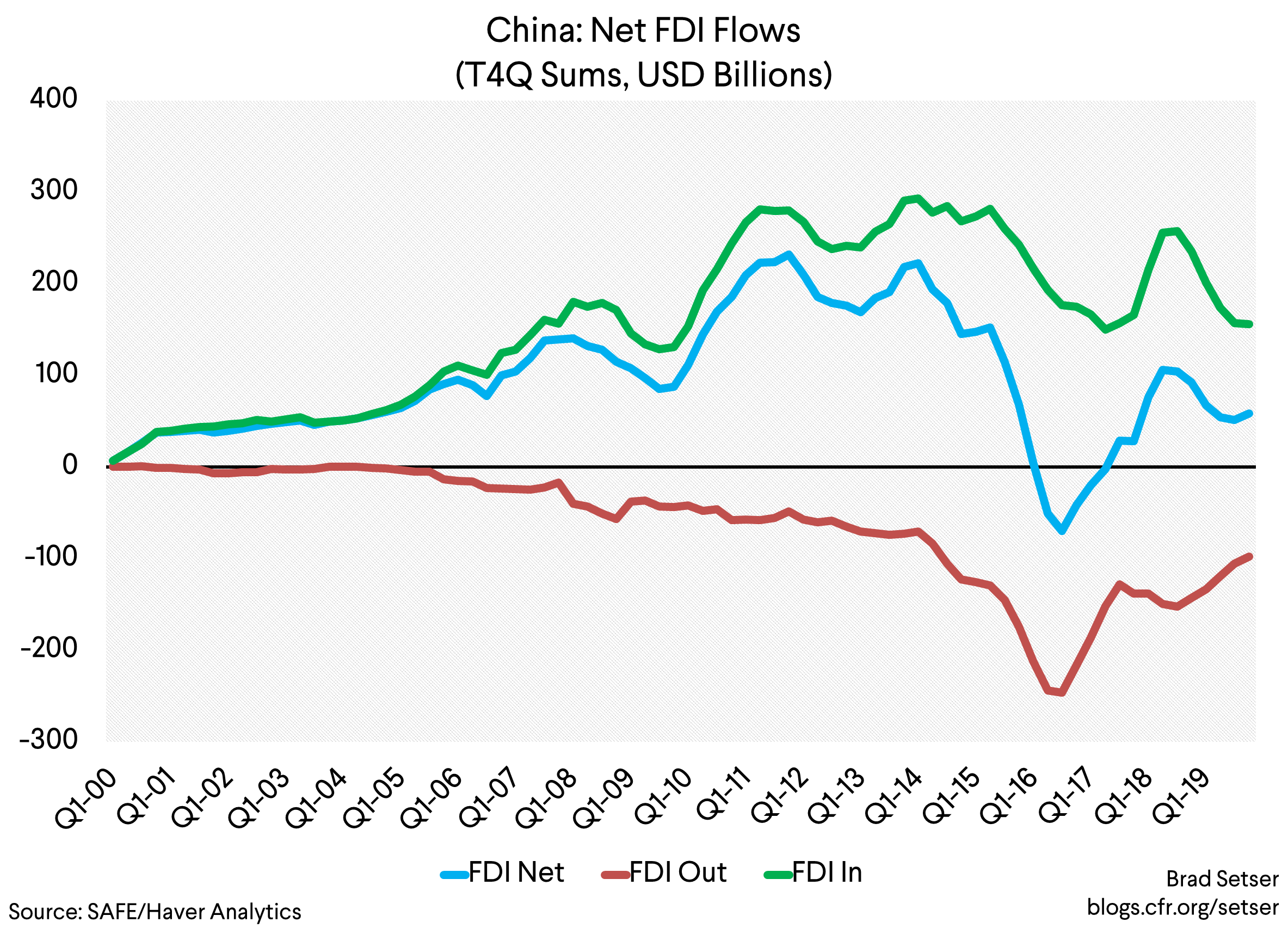

Remember Anbang? HNA? Dalian Wanda? And other Chinese firms that once seemed to be borrowing from Chinese banks to snap up a range of risky assets all over the world? While strategically motivated Chinese direct investment of course continues, headline grabbing property investments abroad by leveraged Chinese investment groups have largely disappeared.

With hindsight one reason why the yuan’s 2015 and 2016 depreciation against the dollar was so financially disruptive was that it came just after a series of steps that China had taken to liberalize the financial account. In the run up to 2015, Chinese firms borrowed a lot of dollars for domestic carry trades, as there was an expectation that the yuan would only go up. Those trades blew up spectacularly in 2015 and 2016. And after China had gone to great lengths to liberalize outward FDI, it took a while before it put the gates back up.

Outward FDI consequently was a significant source of pressure on reserves in 2015 and 2016. At its peak, FDI outflows topped $250 billion over four quarters. Now that outflow is down to under $100 billion.

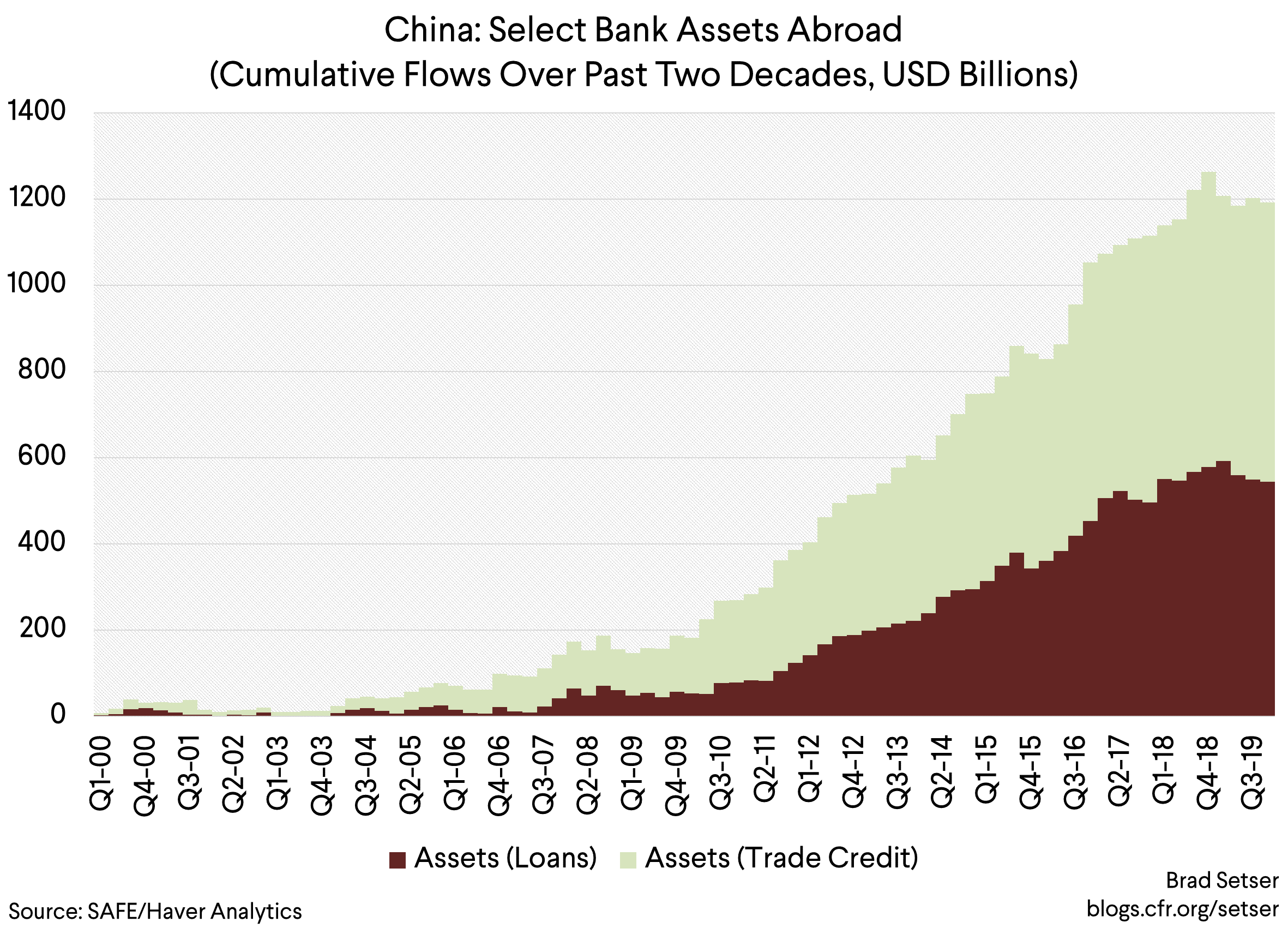

State Bank Lending

Belt and road lending—and the previous push by energy companies to “go out”—was also a significant drain on China’s reserves in 2015 and 2016. State banks’ offshore lending continued as if nothing had happened.

Presumably that was an intentional policy choice. Chinese offshore lending is mostly policy lending, and it almost entirely comes from a small set of state institutions.

Part of the motivation for this lending was to put funds that would otherwise go into China’s reserves toward more strategically valuable use—and in the process, take away the visible evidence of China’s ongoing intervention in the market that attracted the attention of the U.S. Treasury.

But the outflow initially continued—like the FDI outflow—even as circumstances changed.

For a host of reasons (likely including concerns inside China about some of the risks associated with Belt and Road projects) that lending slowed in 2019.

This had the effect of reducing one source of pressure on the balance of payments.

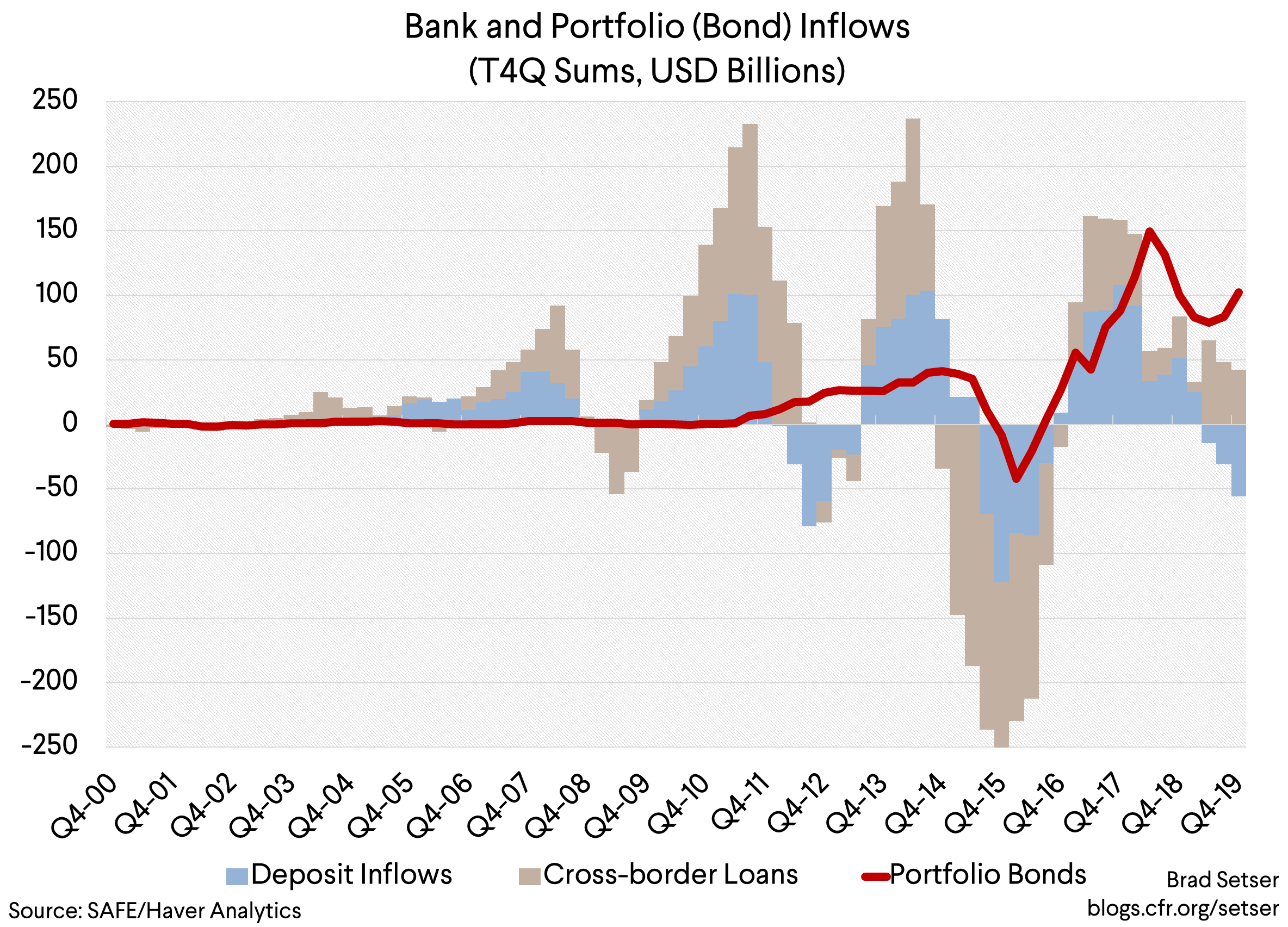

Between reduced state bank lending and China’s selective opening up of its financial account to long-term portfolio inflows, China generated a helpful swing in a portion of its financial account. In 2019, unlike 2016, bond inflows offset deposit outflows (in the chart below a negative number means foreign banks reducing their lending to Chinese banks).

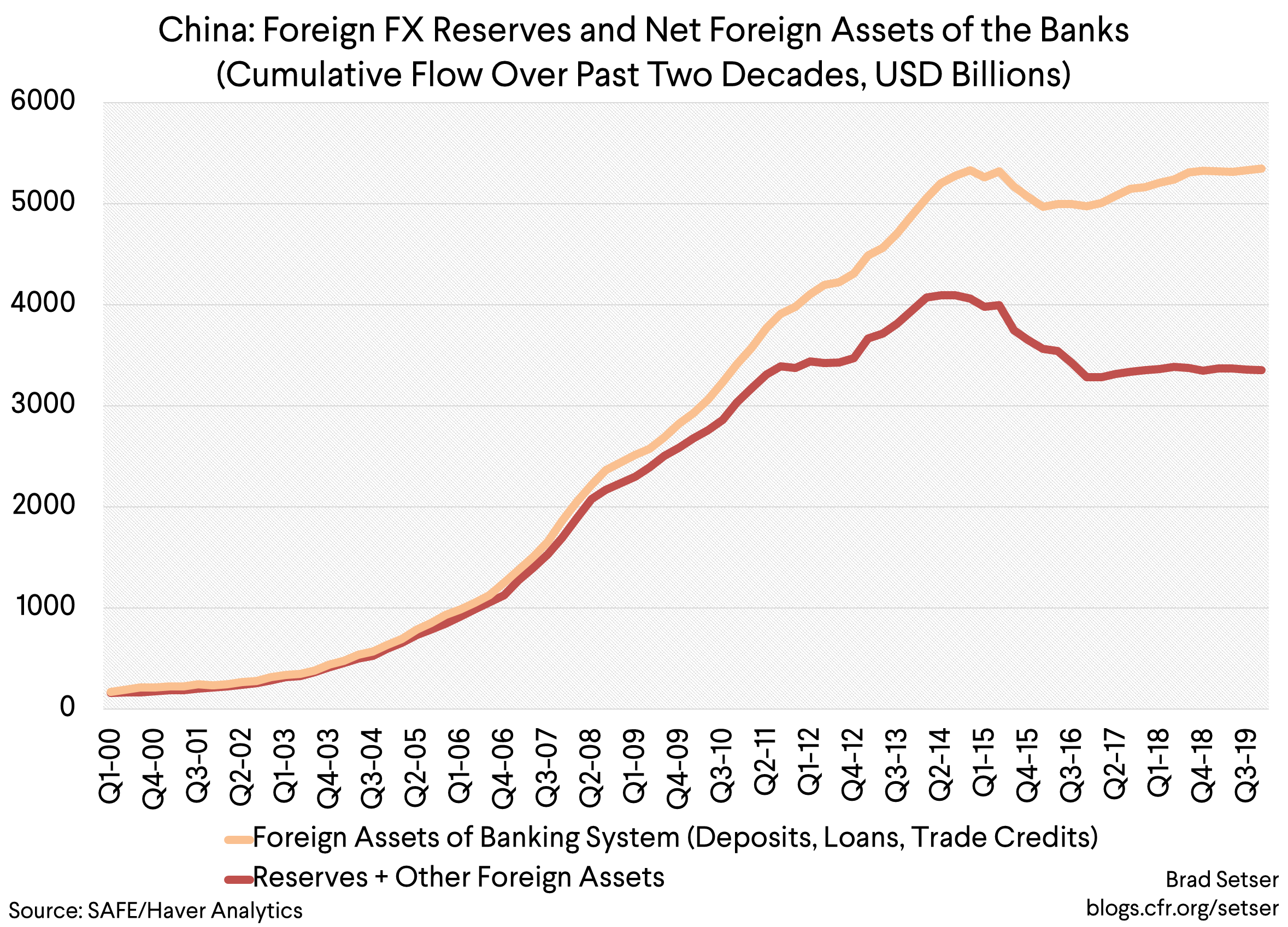

Finally, well, there was a bit more concern about China’s financial position than was ever really warranted. China is a global creditor, thanks to thirty years of current account surpluses. The bulk of the funds accumulated through those surpluses is still sitting on the balance sheet of the People’s Bank of China.

The state banks, according to the BoP, have another trillion or so in foreign assets—yes, they have borrowed from the rest of the world, but their roughly $1 trillion in external borrowing is dwarfed by their $2 trillion in external assets. (Note that I am inferring foreign assets and foreign liabilities by taking the cumulative flow over time in the balance of payments; this technique lets me go back much further than the net international investment position data).

Errors and omissions (essentially private capital outflows) have picked up, but these hidden outflows have been covered by the surplus in the current account and the FDI balance*—they have not generated a significant draw on reserves after 2016.

Sum it all up and it is true that China’s stockpile of state assets abroad hasn’t been growing as fast as it did before 2015. But China is still sitting on a massive stockpile, and thus is in a strong position to manage a range of shocks—particularly if the financial account remains heavily managed.

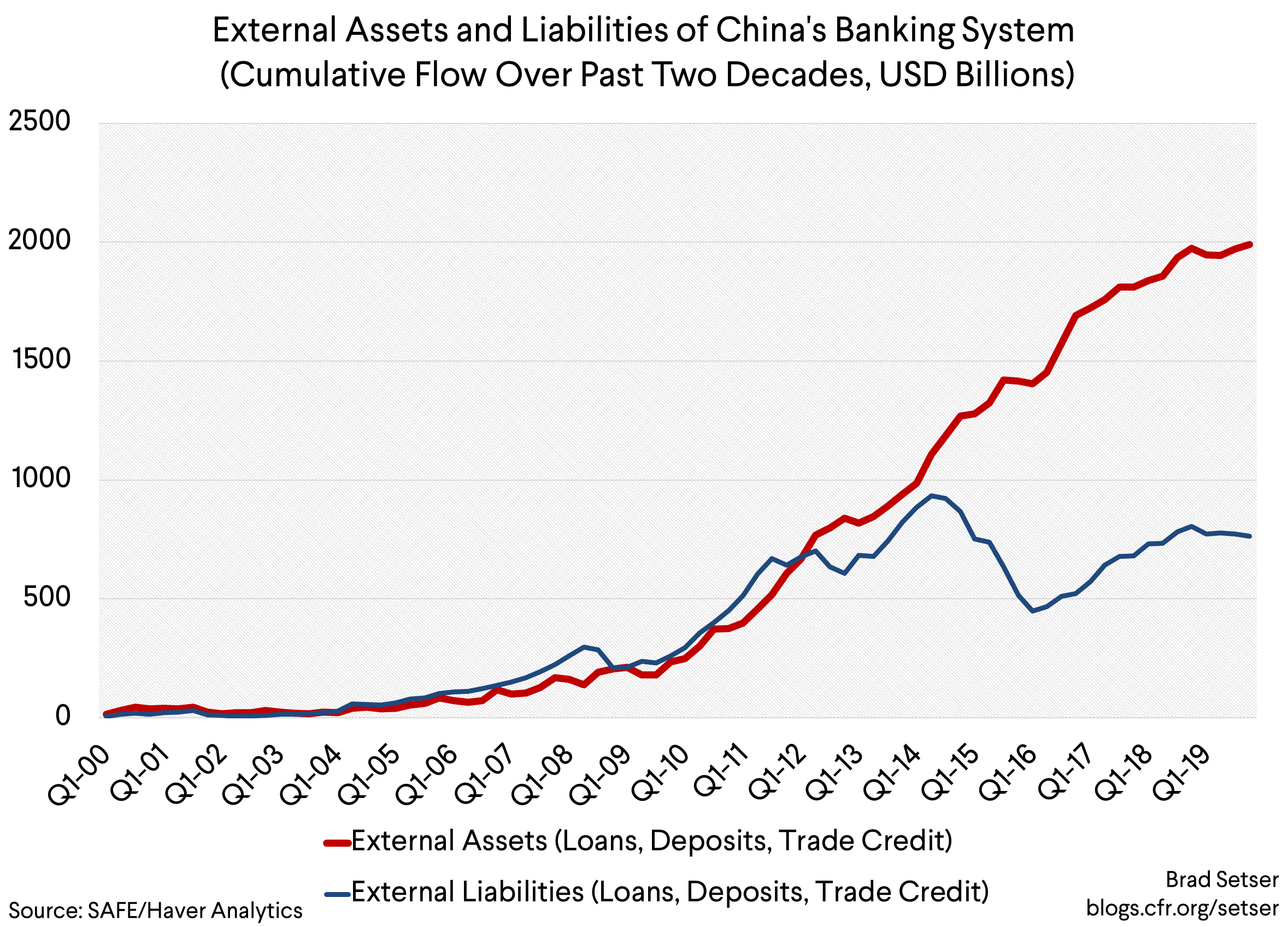

There is confusion on this point, I suspect, largely because China’s domestic debts have been growing so fast. Most people don’t differentiate between internal and external debt. But it is an important distinction—China’s SoEs and its local and provincial governments and their borrowing vehicles have borrowed a lot from China’s (state) banks and a range of new financial intermediaries (though most “shadow” banks are themselves backed by a state backed financial institution; they simply aren’t regulated as banks). But it is all money that China owes to itself. It doesn’t change the fact that the world owes China—and mostly the Chinese government—far more than China has borrowed from the world.**

* Reinvested earnings are notionally a debit in the current account, and then are credited in the financial account. The basic balance is thus in some ways a better measure of the underlying FX inflows into China than the current account, as reinvested earnings now dominate the “FDI” category.

** There is an argument that China’s reported $1.3 trillion in external foreign currency debt is somewhat understated, as some Chinese companies have issued debt in offshore financial centers (typically Hong Kong). That debt in turn either was invested in foreign assets (in which case it really isn’t a claim on China’s reserves), or in some cases it may have been onlent or invested back in China in yuan. Such flows should enter into China’s balance of payments, but they might not enter as “foreign currency borrowing.” I don’t think though that the scale of these flows is large enough to significantly alter my conclusions.