Record Chinese Bilateral Surpluses With the United States Are Not Mirrored in the U.S. Trade Data

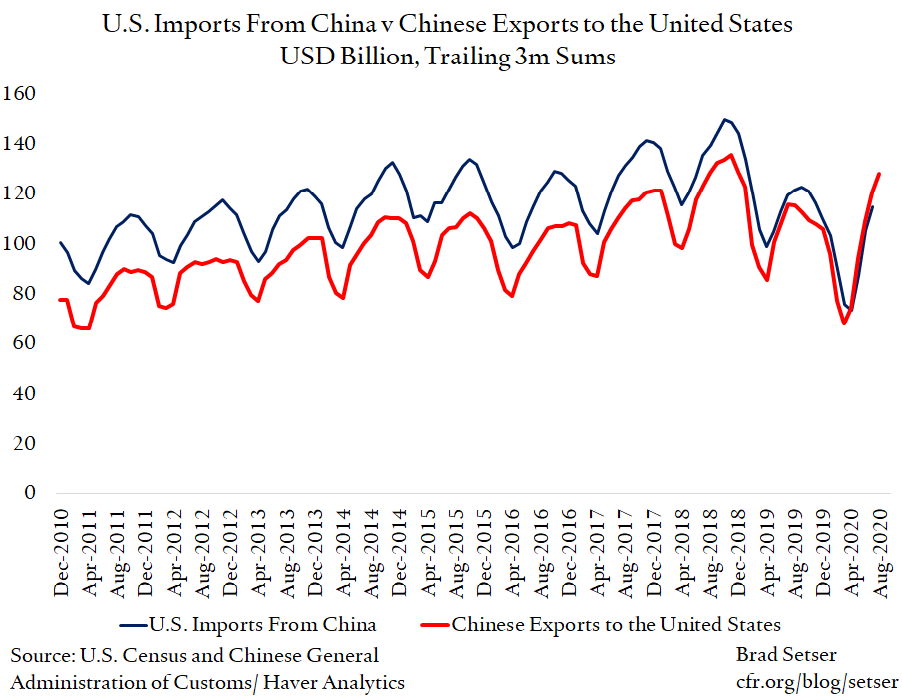

Is China’s surplus with the United States back at a record level? It depends. In China’s data, China’s exports to the United States and its surplus with the United States are at all-time highs. The United States’ import data, however, shows fewer imports from China than China reports exports—which is interesting, because the norm has long been the other way around.

There are certain rules of the thumb that you can usually rely on.

The sun rises in the East. And unless you are on equator, its angle in the sky will vary with the seasons.

No rules of thumb for trade data are quite as strongly grounded in the physical world.

But it historically it has always been the case that the U.S. data for imports from China showed more imports than the Chinese data showed exports to the United States.

Always. Predictable. Expected. You could count on it if you wanted to use the Chinese export data to forecast U.S. imports from China.

China’s data on imports from the United States also tends to show more imports than the U.S. data shows exports to China, but since imports are so much larger than exports, it almost always has been the case that the U.S. data shows a larger bilateral deficit with China than the Chinese data shows a surplus with the United States. (The Hong Kong port effect explains most, but not all, of the discrepancy; see this 2018 blog for my views on how to adjust the U.S.-Chinese balance of payments data.)

This is sort of a well-known—the U.S. and Chinese numbers generally do not line up, but they typically have not lined up in a predictable way. *

This rule of thumb now must be tossed out the window.

In the last few months of data, China’s reported exports to the United States have significantly exceeded reported U.S. imports (the exact opposite of the established pattern).

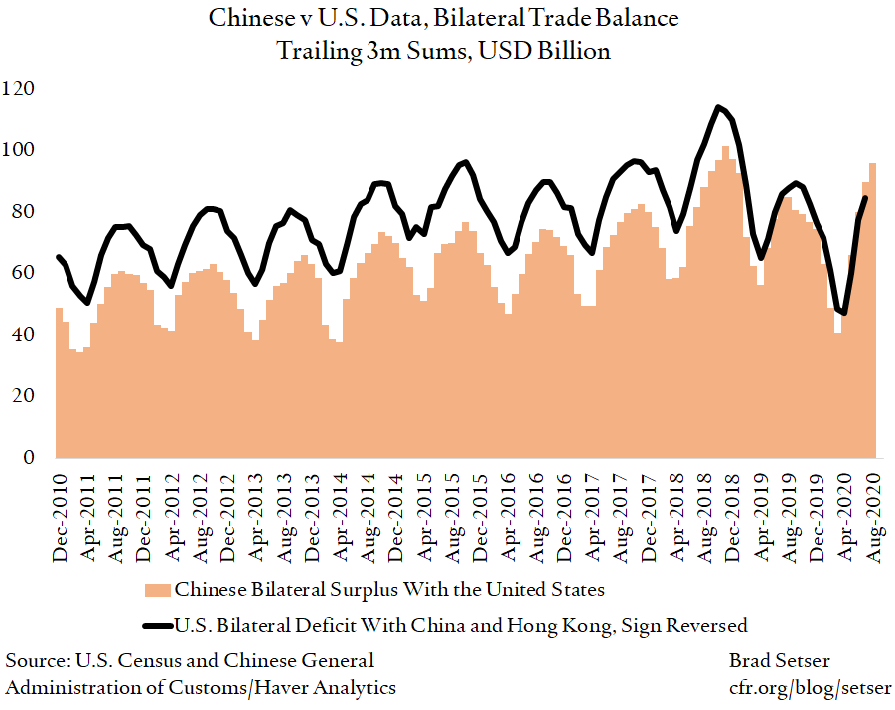

And China’s reported surplus with the United States thus is now larger than the U.S.’ reported deficit with China (again, the opposite of the norm).

This has only been apparent in the last few months of data—it jumps out in the monthly data and the trailing 3m sum but not in the trailing 12m sum. It was arguably present last year, but the shift in the size of the reported Chinese surplus relative to the U.S. deficit only really started to jump out over the summer.

Yet there is no doubt there is a gap.

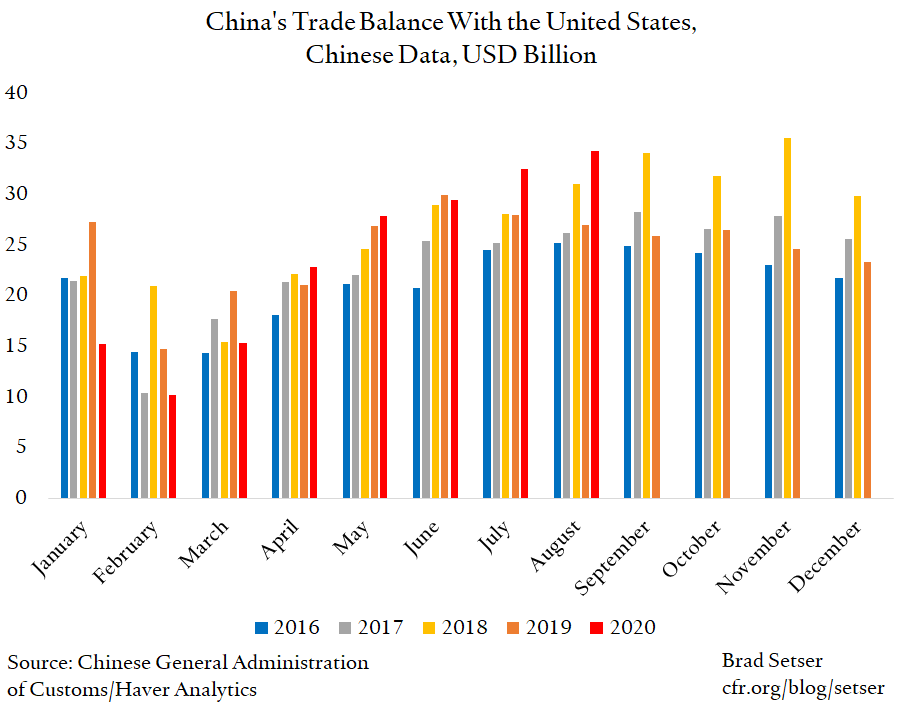

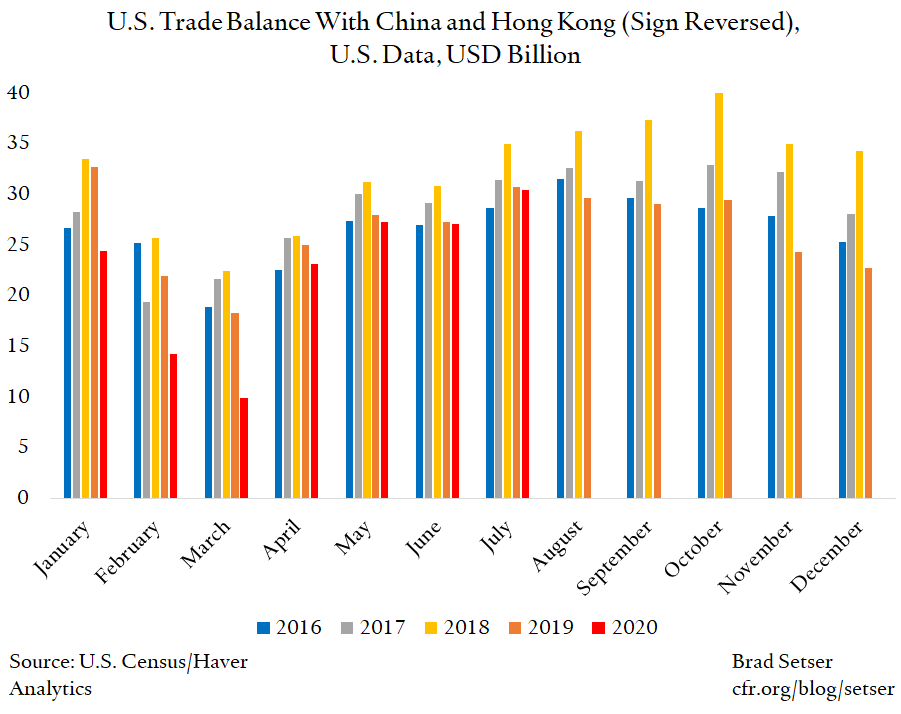

In July 2018, China said it exported $41.6 billion to the United States, and the United States reported importing $47 billion from China. In July 2019, China said it exported $38.9 billion to the United States (down because of the tariffs), and the United States reported importing $41.4 billion from China. And in July 2020, China said it exported $43.7 billion to the United States, while the United States only reported importing $40.7 billion from China.

As a result, the answer to a lot of politically-salient questions—for example, is the bilateral trade deficit with China larger or smaller now than in 2016?—hinges on whether you use the U.S. or the Chinese data. **

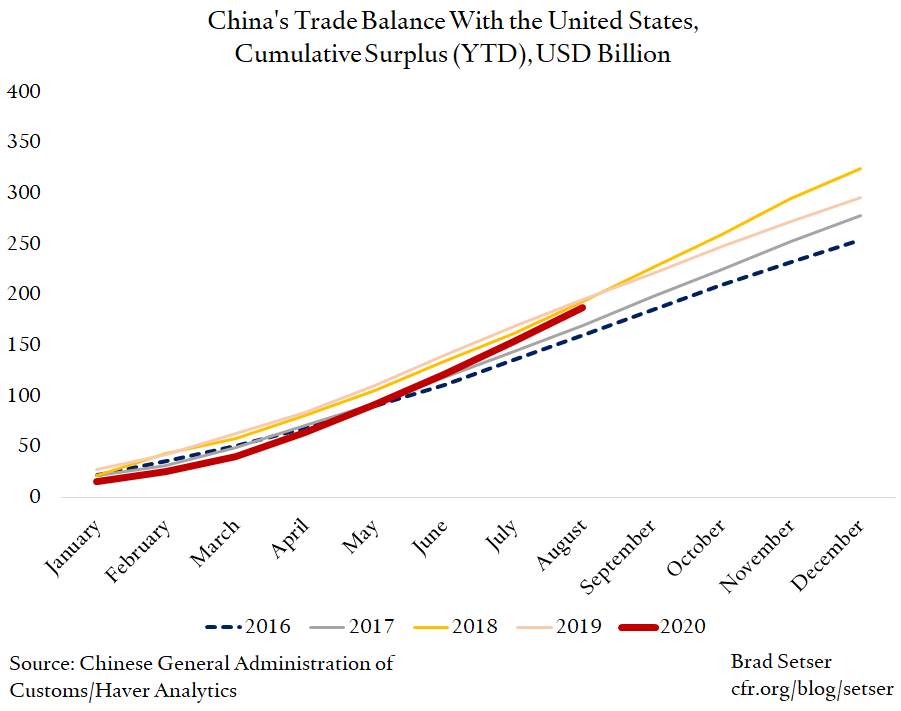

If you look at the Chinese data, its current monthly surplus with the United States is at an all-time high for the months of July and August, topping its pre-trade war peaks by substantial margins.

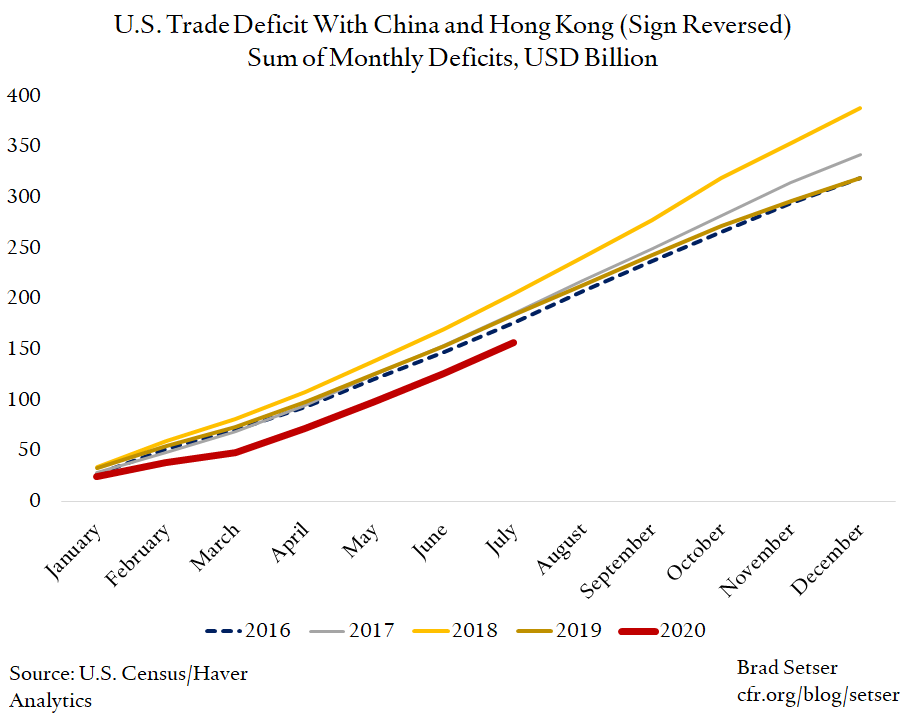

In the U.S. data, the July deficit with China and Hong Kong (adding in Hong Kong reduces the size of the deficit as the United States runs a surplus with HK) is only just above its 2016 levels.

These monthly differences produce a different trajectory in the year-to-date numbers.

If you just look at China’s data, its surplus with the United States looks poised to set an all-time high in 2020, as strong exports over the summer have made up for the obviously weak start of the year.

In the U.S. data, by contrast, the more muted recent deficits have not pushed the deficit toward all-time highs.

As I noted, the gap between China’s reported exports to the United States and reported U.S. imports (plus the larger deficit when reported from the U.S. side than the surplus on the Chinese side) is a long-standing pattern. It reflects Hong Kong’s role in U.S.-China trade—a lot of what China records in its data as an export to Hong Kong historically has ended up in the U.S. data as an import from China, and a lot of what the United States reports as an export to Hong Kong has historically ended up in the Chinese data as an import from the United States.

The signal here comes from the change in the pattern—a long established and well-understood discrepancy between the import and export side data has gone away.

The puzzle now is why the sign on the discrepancy looks to be flipping

There are a range of possible explanations.

Chinese exporters might be overstating their exports, in general and to the United States. Overstating exports is a classic way of getting capital into a country with capital controls.

But the simplest and most parsimonious explanation is that the U.S. tariffs have created a strong incentive for firms importing into the United States to go to some lengths to understate their imports from China. Thus, I would bet that U.S. imports from China are now slightly under-counted (which by implication holds the bilateral trade deficit down).

No doubt more investigation will yield evidence that points toward a conclusive answer.

Fact-checking can seem like a dull exercise. Mapping one country’s import data to a partner’s export data even more so, especially in a world where looking at bilateral trade balances is viewed as a bit retro, global value chain and all. But sometimes it yields interesting results. A similar exercise back in 2015—the Chinese current account surplus stopped tracking the goods balance—led me to look at whether the reported increase in tourism imports in the Chinese data was matched by a rise in the number of actual tourists (it wasn’t) and ultimately produced quite a good Fed paper. My guess is that the changing sign of the U.S. imports v. Chinese exports discrepancy will generate another good paper.

*/ For what it is worth, the bilateral data on services trade really does not line up at all in most states of the world. The United States at least used to report a surplus with the UK, and the UK a surplus with the US. The goods data by contrast usually fits together relatively well.

**/ Full disclosure of potential conflicts of interests: I am supporting Vice President Biden.