The Right and the Wrong Ways to Adjust the U.S.-China Trade Balance

The best way of painting a more accurate picture of the economic relationship between China and the U.S.? Add in data on U.S. exports to Hong Kong.

The desire to push back on Trump’s trade action against China has led to a resurgence of interest in “alternative measures” of the trade deficit. Or, to use a less loaded phrase a measure of the “aggregate economic relationship.”

The resulting measure though isn’t an alternative measure of the trade balance.

It is an incorrect measure of the trade balance.

It equates Starbucks’ sales in China—a service produced mostly with Chinese labor (plus some rented local real estate), though no doubt with some imported beans which should show up in the trade data—with Boeing’s very real exports. One adds a little to U.S. GDP, the other adds a lot.

The right way to account for the sales of U.S. firms in China is to add the profits U.S. firms earn on their “in-China” sales to U.S. exports, not their gross sales.

That’s how the BEA does it (see table 1.3 in the international transactions data set) when they calculate the bilateral current account balance with China.

It turns out that the results of the correct adjustment for FDI income just aren’t all that impressive—U.S. firms earned about $13.5 billion on their $200 billion plus in Chinese sales (total investment at historical cost in China as of end-2016 was $92 billion, which no doubt underestimates the real total a bit).

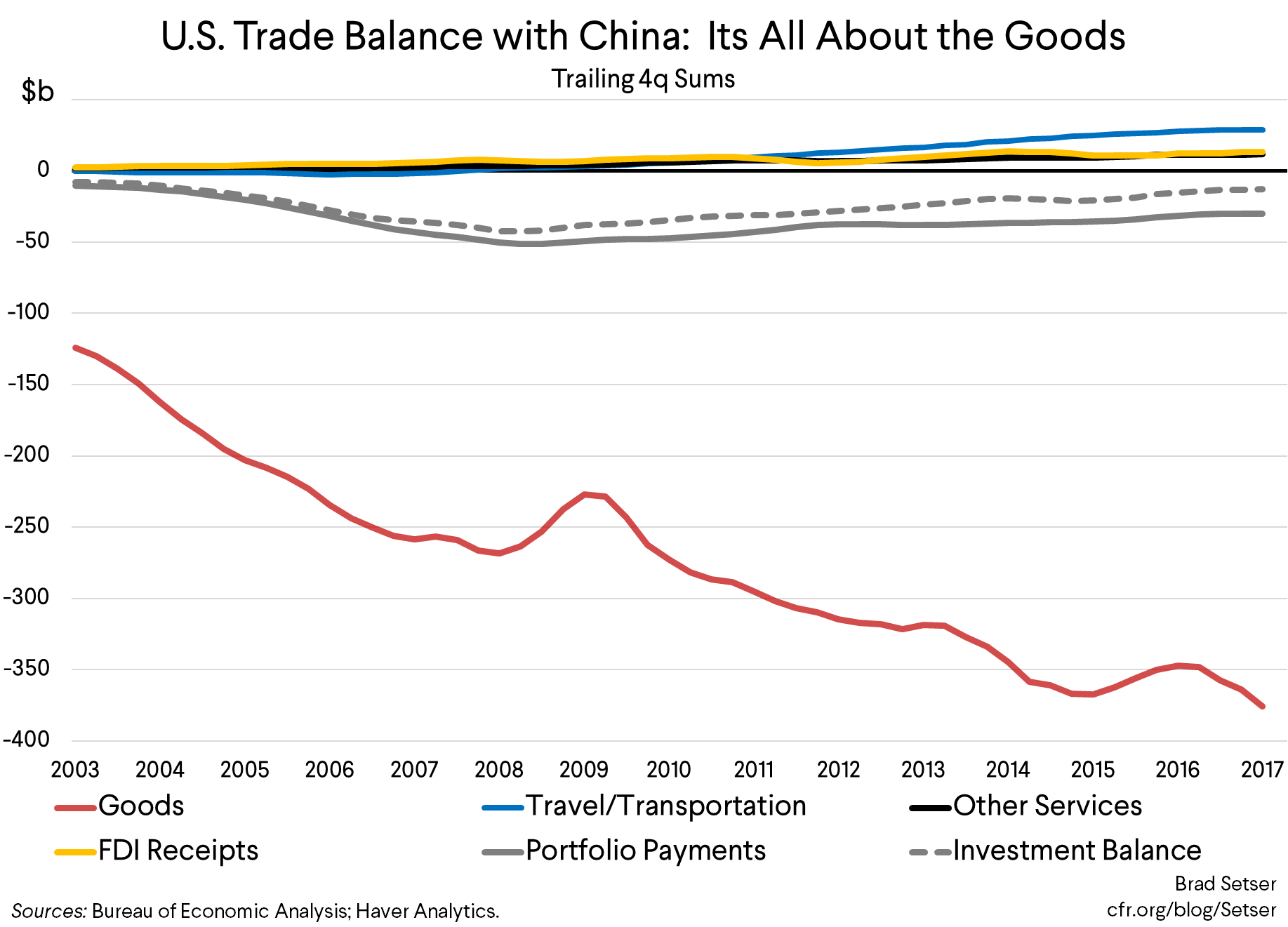

It also happens to be the case that adjusting the goods trade data for services trade doesn’t all change much either.

There is a significant flow of Chinese tourist dollars to the U.S. (the tourism data includes travel for education, so I suspect the numbers here are mostly real and not hugely inflated by Chinese residents moving funds abroad). But total exports of services other than “travel” and the transportation of goods and people amount to…drumroll…$20 billion. That’s 0.1 percent of U.S. GDP.

There just isn’t much there “there” so to speak, at least not compared to the $500 billion that the U.S. spends on goods imported from China (with some non-Chinese content to be sure), or the $375 billion goods trade deficit. (Those are the end-2017 numbers. The likely number now is much larger—Chinese goods exports to the U.S. were on track to rise to $550 billion this year prior to the start of a tariff war. And even with the $35 billion in tariffs now in place and the $15 billion that are clearly coming, I still expect that the overall deficit may rise to$400 billion—as China shifts its soy imports to Brazil and the U.S. will still take delivery of the bulk of the goods ordered from China for the holiday season. That will only change if Trump really escalates quickly)

And, well, an “aggregate” measure of the economic relationship should probably take into account the interest income China gets on its $1.4 trillion in U.S. debt (the real number is a bit higher, not all of China’s bond holdings appear as “Chinese” in the U.S. data) and its $200 billion of U.S. stocks. China got $30 billion in interest and dividends from the U.S. in 2017—hence the deficit in “income” line of the balance of payments (that’s the official number, China’s real holdings of U.S. debt are a bit higher than thus the income deficit is probably a bit bigger).

China’s interest income is poised to grow as well—China may not be adding to its U.S. portfolio anymore, but U.S. interest rates are heading up. The U.S. fiscal deficit is many ways a boon to China—it is driving up U.S. rates and thus the interest income China gets on its reserves, and a certain fraction of the excess demand from the stimulus is spilling over to China. I suspect part of the backstory behind Trump’s tariffs is that so far at least China was “won” from Trump’s economic policies on Trump’s preferred measure.

Bottom line: rather than providing a better measure of trade, the “augmented” trade balance simply adds to the confusion. It suggests that China doesn’t run a surplus with the U.S. when in reality it does, and it suggests that China isn’t a creditor to the United States when in reality it is.

Now there are a couple of adjustments to the U.S. China bilateral balance that do make some sense.

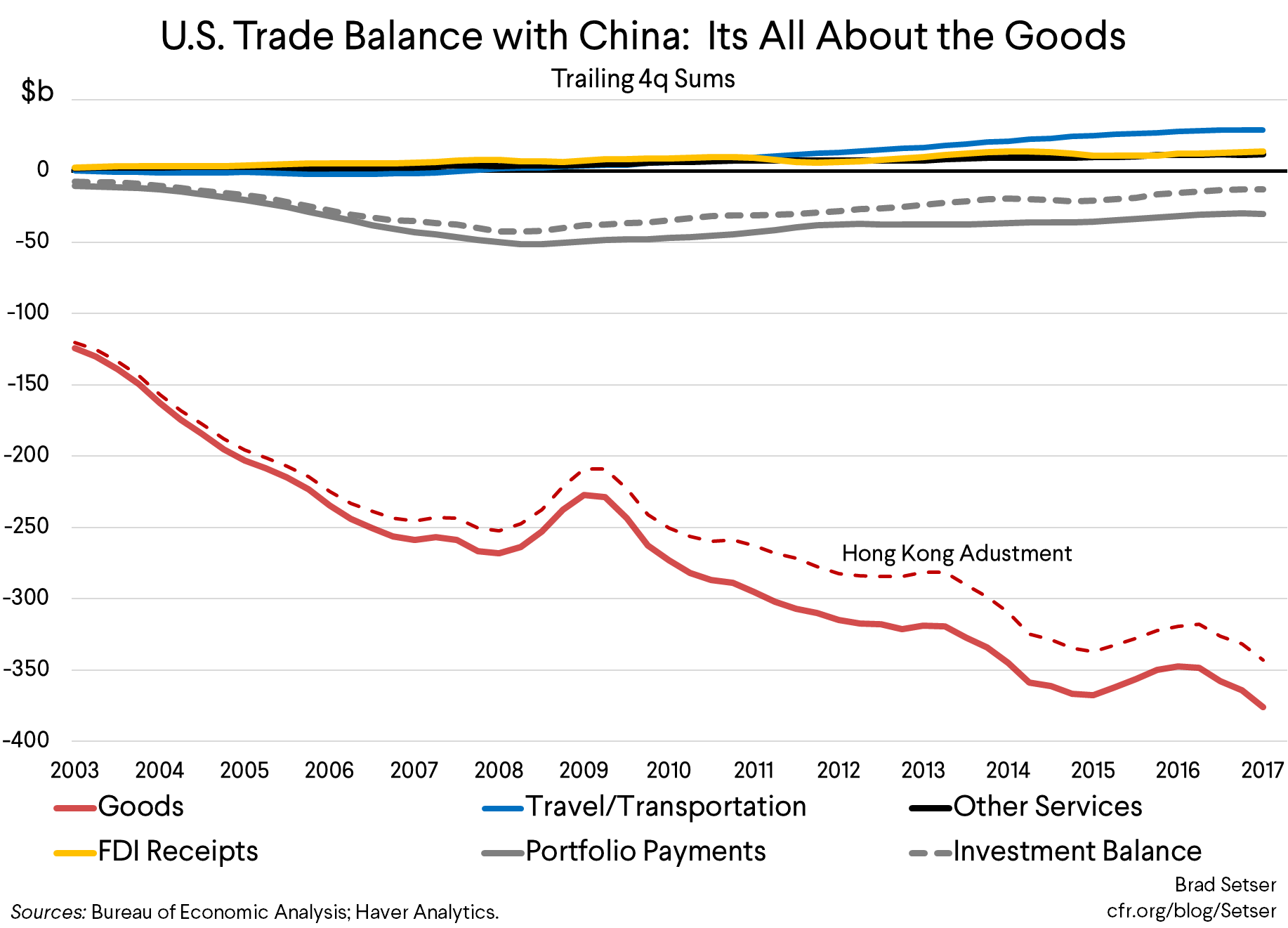

The first is extremely straightforward—add in trade with Hong Kong. Goods exports to Hong Kong are about 1/3 of goods exports to all of China—a number way out of line with the respective size of the economies of Hong Kong and China. It is pretty clear that some of these exports end up in China. Since goods imports from Hong Kong are negligible this adjustment reduces the bilateral deficit with China.*

The other is to adjust the bilateral balance for the imported content of Chinese exports (and to be fair and balanced, the imported content of U.S. exports). The OECD data on trade in value-added appears with really long lags—the last numbers are from 2014. And rather than do a detailed disaggregation, I did the lazy adjustment, as well, any adjustment using 2014 data is going to be imprecise.**

The U.S. content of U.S. exports is around 85%. And the Chinese content of Chinese exports is now around 70% (using 65% for the U.S. doesn’t change the total much).

That brings the estimated U.S. content of $170 billion in exports to China and Hong Kong down to around $145 billion. And the estimated Chinese content of China’s $500 billion of goods exports down to around $350 billion. The total goods deficit then falls to around $200 billion (or 1 percent of GDP). Add in the U.S. surplus in tourism and other services and the “true” bilateral balance is probably a deficit of around $150 billion—not quite the number Trump cites, but still substantial. My estimate by the way has the advantage of fitting comfortably within China’s overall trade balance.***

In some ways though the most surprising bit of this analysis is that the combination of U.S. firms “in-China” profits and services exports that don’t involve the physical movement of goods and people only add $30 billion to the United States measured bottom line with China.

Why?

Three reasons in my view.

The first is kind of boring. Most services are still pretty hard to trade across time zones, let alone across time zones and linguistic barriers. Just because services account for the bulk of the U.S. domestic economy doesn’t mean that they “should” account for the bulk of U.S. exports.

The second is fairly obvious. China isn’t all that open a market, and that has an impact. It doesn’t take a rocket scientist or a fancy algorithm to figure out why neither Google nor Facebook generates any real income out of China…

And the third, well, is kind of interesting. Both the services trade data and the income balance are massively distorted by American firms’ desire to minimize their tax burden. They generally don’t want to report income in China (and pay Chinese income tax) or book services exports in the U.S. (and pay U.S. income tax) if they can report income in a low tax jurisdiction (Ireland or Bermuda) and pay the much lower global minimum tax on intangibles income. “Sophisticated” U.S. firms export their intellectual property to a low tax jurisdiction before reexporting it to places like China. Apple’s profits on iPhone sales in China almost certainly appear in the U.S. balance of payments not as profits in China but as profits in Ireland. And Apple is just the most visible of many cases…

I don’t have a formal estimate of the size of the profits that U.S. firms have tax-shifted away from China. Maybe Gabriel Zucman does. But even if doubles or triples the true income U.S. firms earn in China (e.g. raises the income U.S. firms earn from their over $200 billion in Chinese sales from around $15 billion to somewhere between $30 and $45 billion) it wouldn’t make the deficit go away.

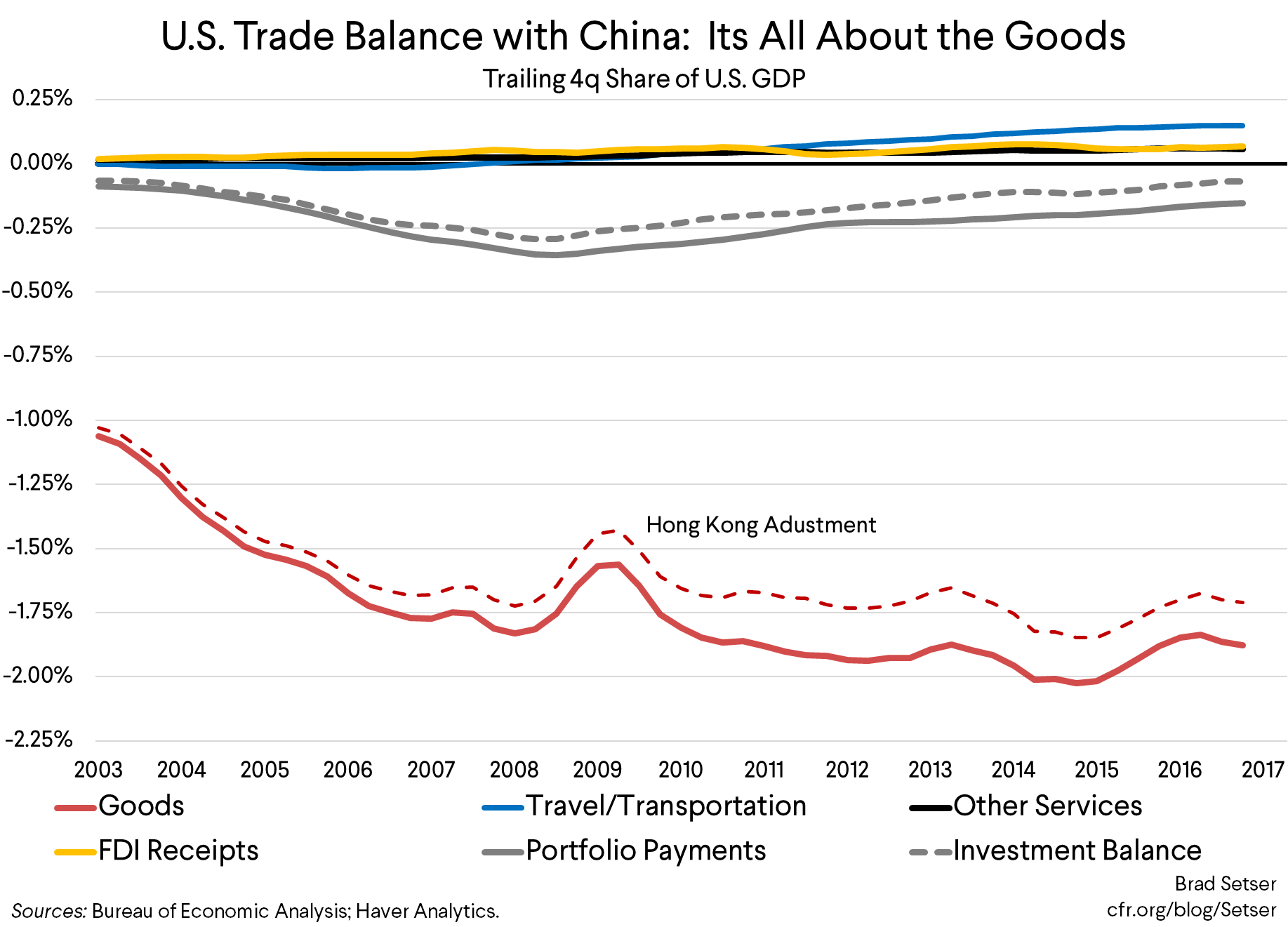

*/ Here is a version of the chart with the Hong Kong adjustment scaled to U.S. GDP.

**/ The Chinese content of China’s exports to the U.S. could differ from the aggregate number. A high share of electronics in exports to the U.S. for example would likely pull Chinese value-added down a bit, but the 2014 number is also likely out of data as Chinese value-added has increased since then—and you have to account for through-trade with Hong Kong too. And a full adjustment would account for the Chinese content embedded in goods the U.S. imports from Mexico and Europe, and for the U.S. content in the goods China imports from places like Taiwan, Singapore, and Malaysia (where there are lots of fabs that manufacture U.S. designed chips). I assume all this nets out, which is probably closer to being true than false.

***/ The bulk of the adjustment away from China comes from the non-Chinese content of China’s exports—which effectively redistributes some of the measured bilateral surplus with China toward the big “current account” surplus economies of East Asia—e.g. Korea, Taiwan and Japan. They all get off lightly in a “Trumpian” bilateral imbalance focused world.