The Rising Bilateral Deficit with China and the Negotiations Over China 2025

A short review of the March U.S. trade data and a lot of speculation about the arc of the Sino-American economic relationship in light of the non-negotiability of Made in China 2025.

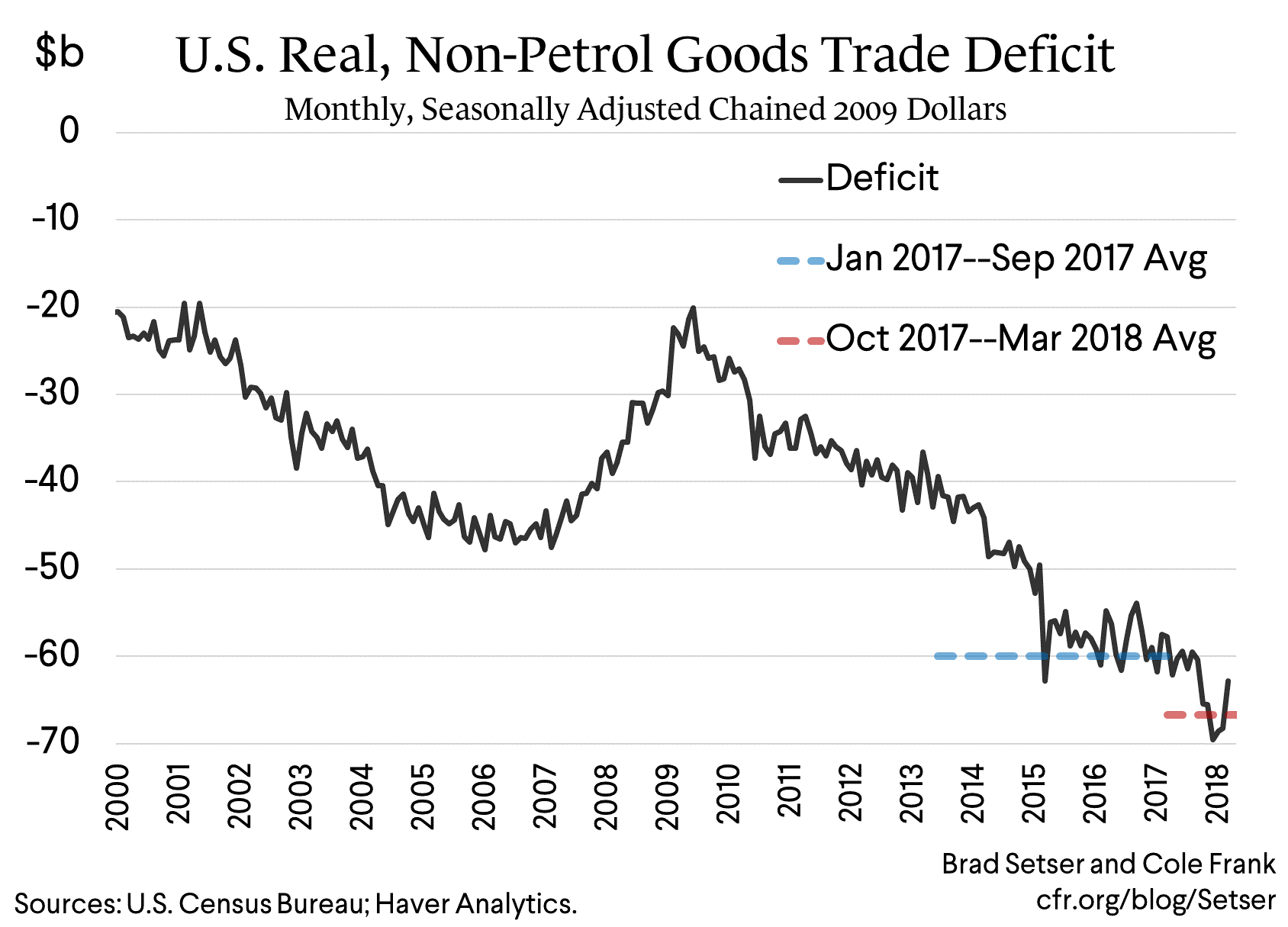

The U.S. trade deficit fell in March, for the first time in several months. That’s not really a surprise—the monthly data bounces around a lot, especially in the first quarter (the lunar new year distortion is now global) and the advance trade data had hinted at a lower deficit in March.

It is too early to tell if this really represents a break in the widening of the (non-oil) goods deficit that started in q4 2017, or it is just an interruption in the trend.

I would bet, given the size of the increase in the fiscal deficit and the dollar’s recent strengthening, that the improvement doesn’t last. The U.S. savings and investment fundamentals point toward a bigger not a smaller deficit over time.

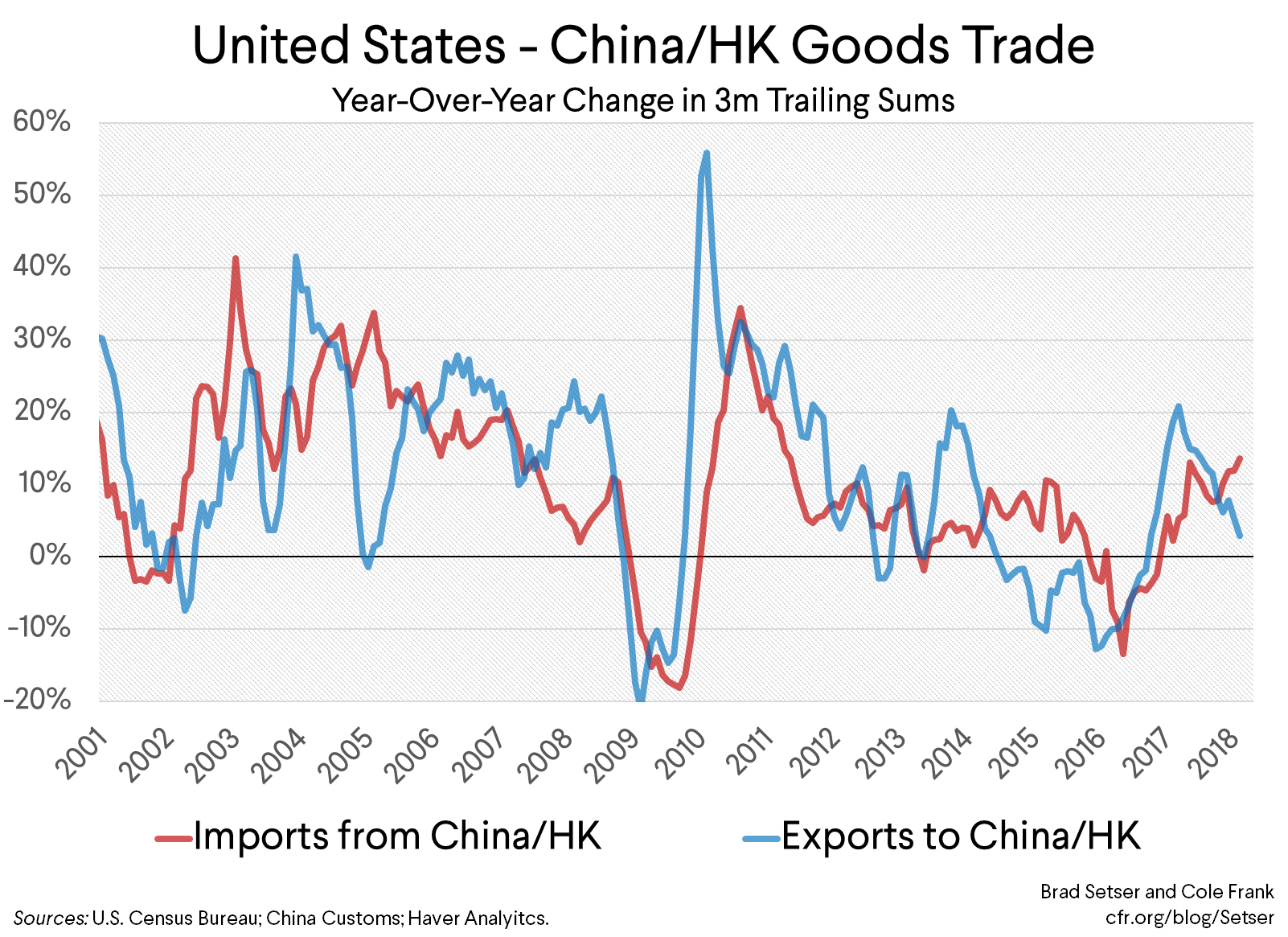

The bilateral deficit with China also narrowed in March, though it’s likely a lagged lunar New Year effect. China’s exports were down year-over-year in March, so it figures that U.S. imports dipped too.

But the basic trend in the bilateral balance over the past few months has been clear—the bilateral deficit is now rising at a reasonably rapid clip. U.S. consumer goods imports picked up in late 17, and China’s overall import growth has slowed over the last year as China started to tighten policy. That shows up in the year-over-year export and import growth numbers—U.S. imports from China are now clearly growing faster than U.S. exports to China. U.S. imports from China were up 13.5 percent in q1, while exports to China were up 8.5 percent (exports to China and Hong Kong combined were up only 4.5 percent, and I think that is the best measure).

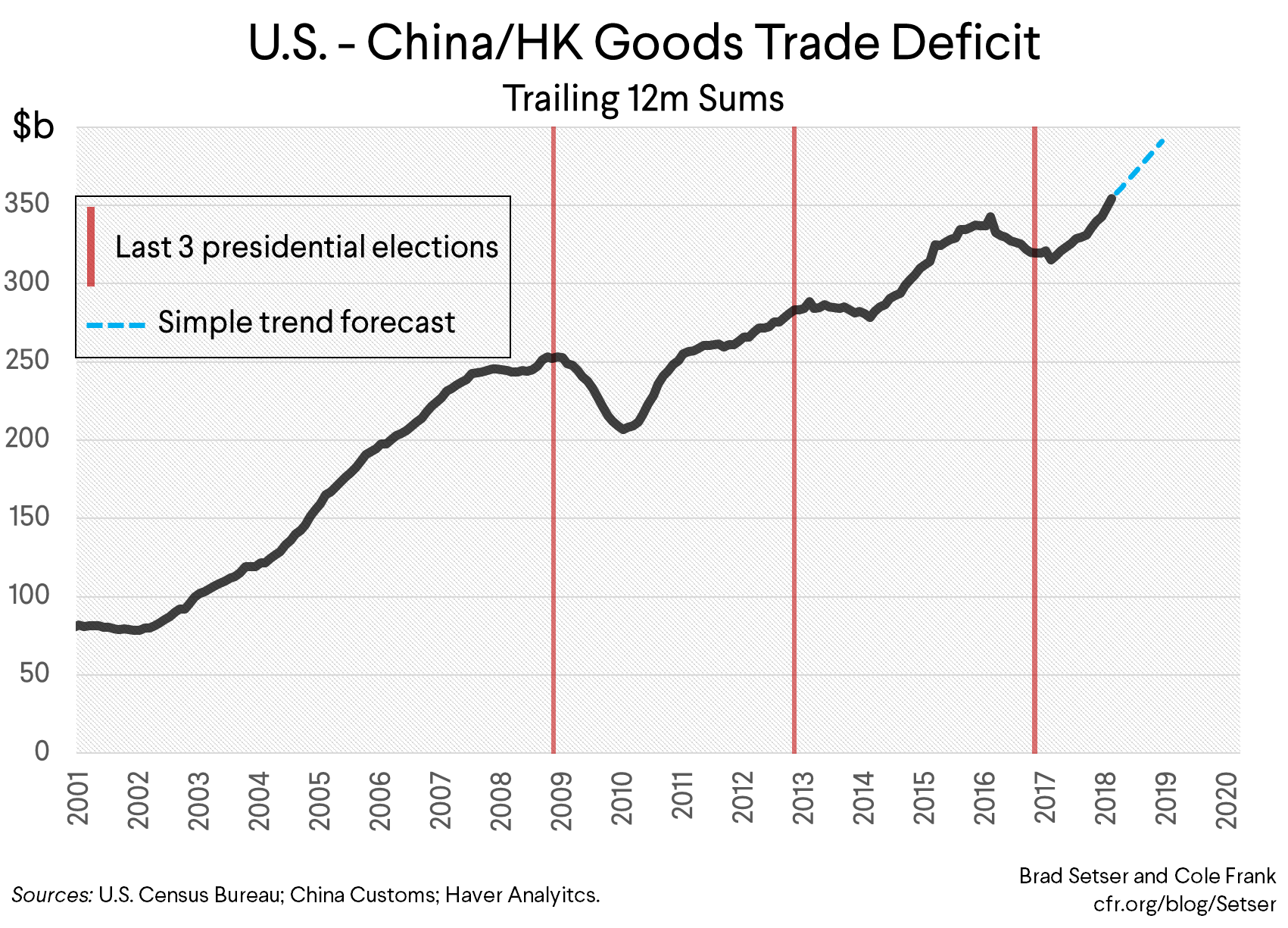

With a lot more imports than exports and faster growth in imports than exports, the bilateral (goods) deficit is growing fast. It increased by $25 to $30 billion in 2017 (it depends a bit on whether you use the balance of payments data or the customs data, and on whether or not Hong Kong is included), and is poised to grow by a similar amount, if not more, in 2018. A linear extrapolation based on q1 import and export growth rates would put the bilateral deficit up close to $50 billion.

I suspect China’s leaders have done this math too. It isn’t rocket science.* Cutting the bilateral deficit by the $100 billion Trump has demanded is likely a shift tof $125 to $150 billion relative to trend, as the bilateral balance is clearly rising now.

So it isn’t a surprise that China has rejected this demand. It wouldn’t even be possible if Apple joined Samsung and started to assemble (or hire contract manufacturers to assemble) the bulk of its smart phones in Vietnam (probably the easiest way to shift the bilateral balance around).

China’s leaders have also have indicated that Made in China 2025 is non-negotiable. China has a right to seek to catch-up technologically and all. The Wall Street Journal reports that Yang Weimin, an economic advisor to President Xi, said: “It’s unreasonable to only let China produce T-shirts and the U.S. produce high-tech.” Fair enough, though if Yang Wiemin thinks China only produces t-shirts now he is fifteen years out of date.

But I assume that China’s leaders also recognize that they cannot credibly defend China 2025 at it now stands while simultaneously claiming global trade leadership.

China 2025 is premised on domestic subsidies to raise Chinese production of a lot of goods that China now imports (as well as subsidies for more energy efficient vehicles, which would help China reduce its dependence on imported oil, wean itself from its current dependence on JVs, and help create a Chinese national champion in autos).

Such subsidies are within China’s WTO rights. Domestic subsidies are allowed (unlike explicit export subsidies). China’s trading partners also have the right to seek damages (so to speak) for the adverse impact of domestic subsidies ex post, particularly if the subsidies to domestic production lead to a surge in exports—but in practice such damages often come after the facts on the ground in the sector have changed. Think of the solar cell industry.

And in some cases China has been able to squeeze other countries‘ exports out of the Chinese market without paying an obvious trade price. China fairly clearly pushed imports from Europe and Japan out of its high speed rail market, without any obvious (trade) penalties that I can think of—though with some impact on European business opinion. China doesn’t (yet) really export high-speed rail to Europe, so there isn’t scope for a symmetric within-the-sector response.

China 2025 though goes beyond subsidies, easy access to credit, and state-backed investment funds. It includes targets for raising the market share of Chinese production in China’s domestic market—and also targets for the market share of Chinese-owned technologies (it isn’t enough for foreign firms to produce in China, China wants to do more than assemble blueprints owned abroad). See the U.S. Chamber of Commerce report. Those targets aren’t enforced by anything as crude as import quotas. But China, Inc has its ways.

Take aircraft. All the buyers of aircraft are state-owned enterprises. Sort of like high-speed rail. Or the energy produced by big wind farms. Guidance on what to buy can come in a lot of ways. It doesn’t have to be enforced at the border. That’s part of what makes China unique.

And in sectors like “new energy vehicles” where the state isn’t the main buyer, getting access to subsidies for the purchase of more energy efficient cars effectively provides the state with leverage. China’s bureaucracy loves making lists of what can and cannot be purchased/subsidized.**

The tools are there, more so in China than anywhere else.

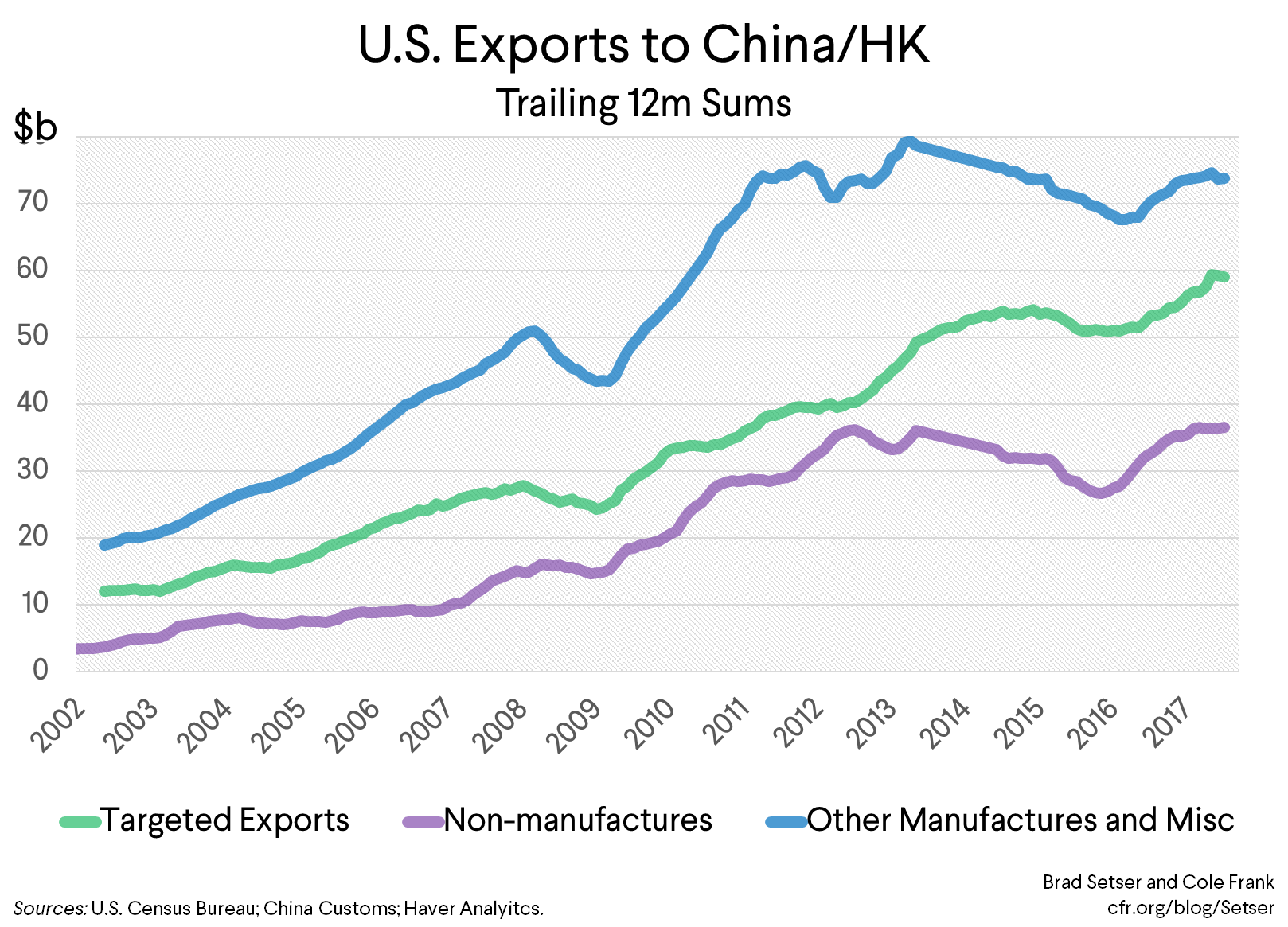

And, well, the sectors that China is targeting in China 2025 do matter to the U.S. I tend to look at U.S. exports to both China and Hong Kong, and by my rough count, U.S exports to China in these sector account for roughly a third of total U.S. exports to China and Hong Kong (and more like a half of U.S. manufacturing exports).

My count includes conventional autos (mostly German designed SUVs that are built in the U.S.) which would be displaced by new electric vehicles, but excludes U.S. designed semiconductors that are made in Asia by contract manufactures. The exact number can be debated, but the sectors on China’s list clearly add up to a sum, roughly $50 billion, that is much larger than the United States‘ current exports of soybeans to China.

Not to mention that competitive Chinese aircraft, medical device, and semiconductor industries would challenge a lot of U.S. exports to third-party markets. Looking at the bilateral data, as many note, is far too narrow.

To my mind, the issue isn’t just China’s encroachment on foreign intellectual property rights (the old deal of building products designed abroad in China for the Chinese market is insufficient in China’s eyes, as China wants to originate and own the technology — see Jane Perlez and Paul Mozur from back in 2016).*** It is also clear that China’s plans for industrial upgrading would infringe on a lot of current U.S. exports.

So what you (and Martin Wolf) might ask?

The U.S. (meaning both U.S. companies and U.S. based manufacturing supply chains) competes with Europe in the global market for aircraft and high-end medical equipment. U.S. firms compete with European, Japanese, and Korean firms for the global auto market. And the same for the global market for top-end semiconductors (with some additional competition from Taiwan).

All true. But China is likely to be competitive across a broad range of industries before its economic system (or political system) has converged toward U.S. or European norms. The relationship between firms, the banks, and the state (and the party) is different in China. China also aspires for technological parity long before wages have converged to U.S. or European levels. Keith Bradsher’s reporting suggests that Ford’s Chinese JV now produces cars with a largely Chinese supply chain with comparable quality and lower cost than in the U.S. or Europe.

And even among allies with similar political systems, technological competition in frontier industries hasn’t exactly been frictionless. Think about the rise of Airbus.

Economies of course adapt to new competition, and Chinese subsidies can generate innovation that has global benefits. Chinese solar subsidies, for example, both were unfair (they artifically shifted the locus of the solar cell production toward China, and drove a lot of the competition out of business) and good for the planet (as Chinese scale and process innovation significantly lowered the cost of solar).

But it also is hard to see how U.S. and European economies can adapt to declining exports to China (and potentially rising imports from China) in sectors like aircraft by shifting toward new cutting edge sectors. Aircraft, semiconductors, medical imaging devices are different than apparel, furniture and electronics assembly. China wants its own national champions in every major industry. And that may mean that in certain cutting-edge sectors, Chinese companies could win globally and meet global demand with Chinese production, using technologies that China thinks it owns. ****

Abstracting away from the drama associated with the trip of Trump’s gang of rivals to Beijing, I can envision four broad equilibria if China ultimately succeeds at reducing its imports of things like aircraft and semiconductors:

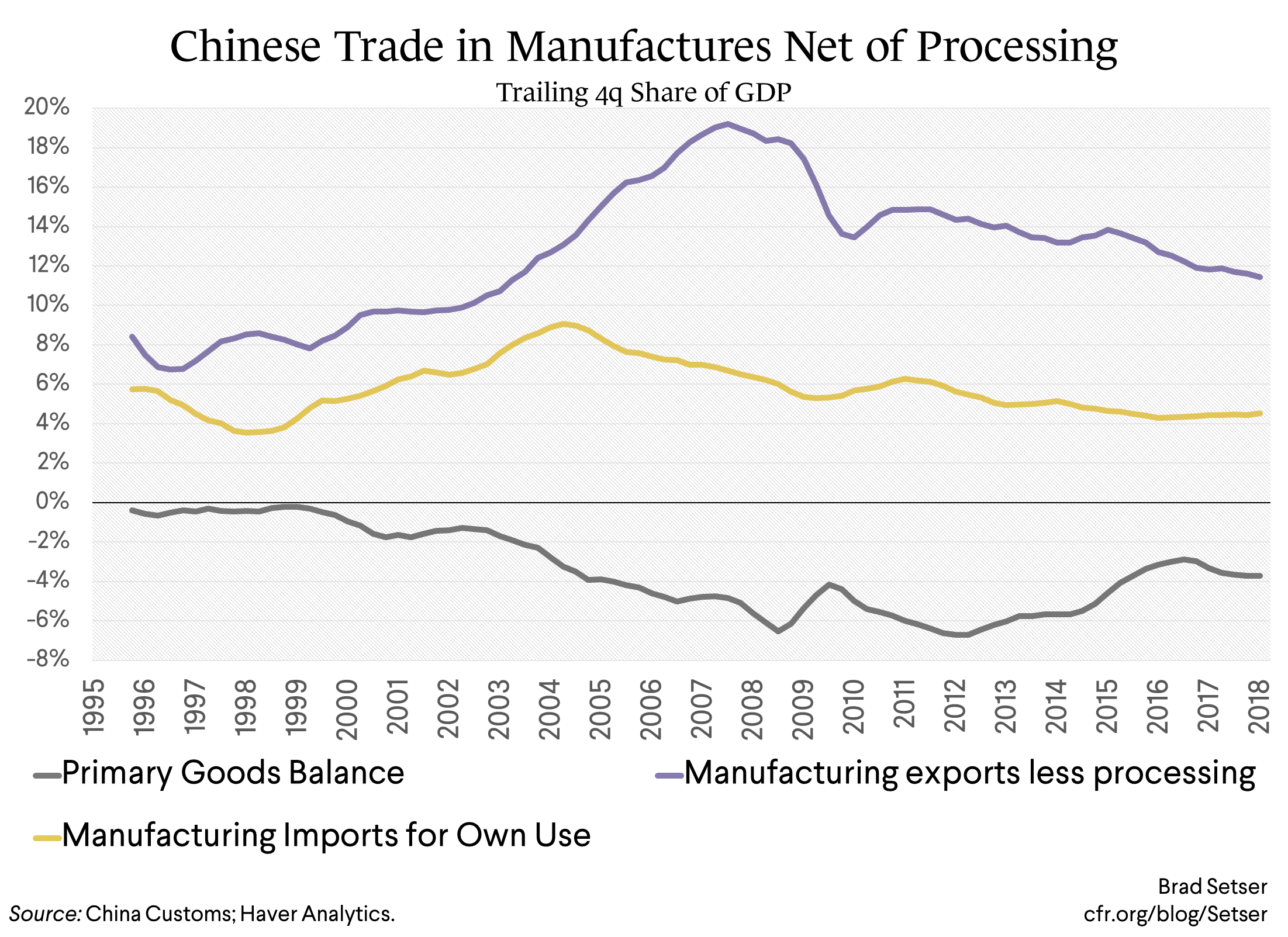

1. China imports more commodities and encourages more tourism spending abroad, keeping overall trade up even as Chinese imports of manufacture fall. That’s kind of what happened after the global crisis (manufactured exports have fallen as a share of China’s GDP, but so have imports of manufactures).***** This presumes that China won’t succeed at weaning itself from imported oil with electric cars and the like. It also could imply that many of China’s key trading partners (including the U.S.) will largely be trading commodities (soybeans, LNG) for Chinese manufactures, with few manufacturing exports of their own. Sort of like Australia, but on a bigger scale.

2. China imports fewer manufactures, but also exports fewer manufactures thanks to a rise in China’s exchange rate. Assembled in China turns out to be a temporary phenomenon. China returns to greater self-sufficiency technologically, and basically ends up trading less with the world (there is a theory that as countries converge technologically they should trade less). This outcome poses the fewest challenges to the WTO. It is part of how the world has adjusted to rising Chinese production of capital goods for its own market after 2008, though RMB real appreciation has stalled in the last couple of years.******

3. China imports fewer manufactures and exports fewer manufactures, as the world throws up trade barriers at the border in response to China’s formal and informal barriers to imports (and de facto barriers to large royalty payments on imported technology). Actual imposition of the threatened 301 tariffs would be a big step along this road. This of course also poses an existential challenge to the global rules, as many of the tactics China now deploys to support its technological champions aren’t obviously WTO illegal but the response to them may well be.

4. The development of Chinese national champions doesn’t mean that China’s market in those sectors is reserved for Chinese firms and Chinese production—the Chinese market doesn’t end up being the winner-take-all, so a China that has caught up technologically ends up both importing and exporting in a range of sectors. Personally I suspect this outcome would also requires some real appreciation, otherwise foreign firms would want to produce in China for the Chinese market (while retaining the intellectual property rights offshore).

There is of course a fifth possible equilibrium—one where China’s overall trade surplus with the world rises along with China’s technical skills. That though takes more than just China 2025. It also would require a shift in China’s savings and investment balance. A technologically almost caught-up China that lets its currency fall to support exports across a broader set of sectors than China has exported in the past is what really worries me. And that could happen if China cannot generate enough consumption growth to offset slowing investment (or it has to slam on the fiscal brakes), given China’s still far-too-high savings rate.

Author’s note: slightly edited after posting, I had an “imports” when I meant “exports.”

(*) For a bit of (almost) rocket science, try figuring out the balance of payments impact of the hedging strategies of Japanese lifers—cross-currency basis gets complex fast.

(**) The U.S. made a big push back in 2010 and 2011 to get China to change aspects of its policy on “indigenous innovation” in government procurement to make it less discriminatory. But I am not sure that the push had much long-term impact. The same basic idea (favor Chinese firms with indigenous Chinese technology/JVs that have transferred IPR to the JV so the Chinese partner has partial ownership) keeps popping up. China 2025 in a lot of ways goes beyond the procurement lists for indigenous innovation.

(***) This quote captures China’s policy well (from the New York Times in 2016), emphasis added: “ One viewpoint holds that we must close ourselves off, make a fresh start, thoroughly shake off our reliance on foreign technology and rely on indigenous innovation to pursue development,” Mr. Xi said, according to a transcript of the speech. “Otherwise, we would always follow in the footsteps of others, and would never be able to catch up.” Mr. Xi ultimately said China must find a middle ground and determine “which things can be imported but have to be secure and controllable; which things may be imported, digested and absorbed for re-innovation; which things can be developed in collaboration with others; and for which things we must rely on our own strength and indigenous innovation.”

(****) As in high speed rail where China claims to have “digested” imported technologies so thoroughly that they are now Chinese. It isn’t clear that European and Japanese firms agree.

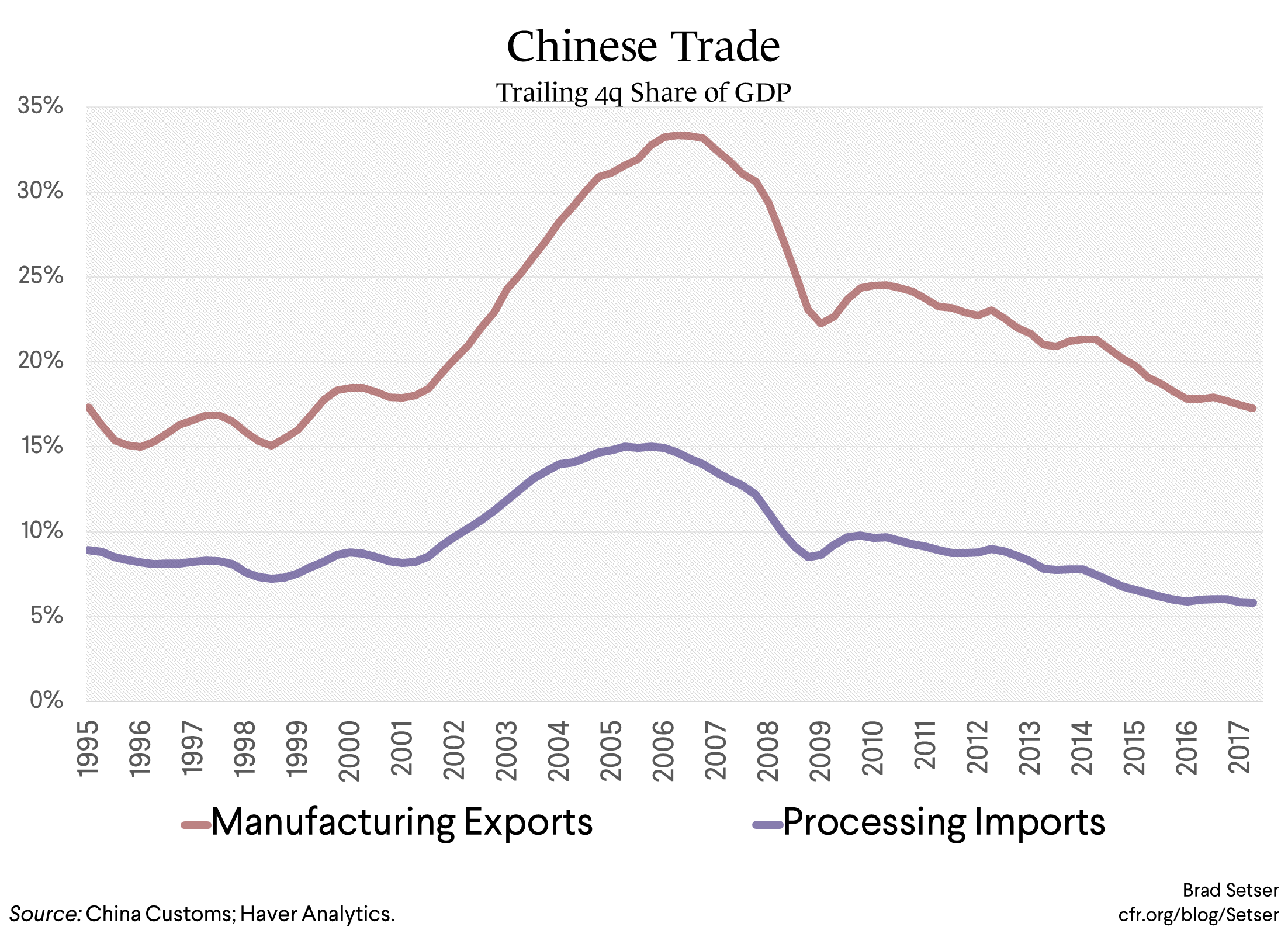

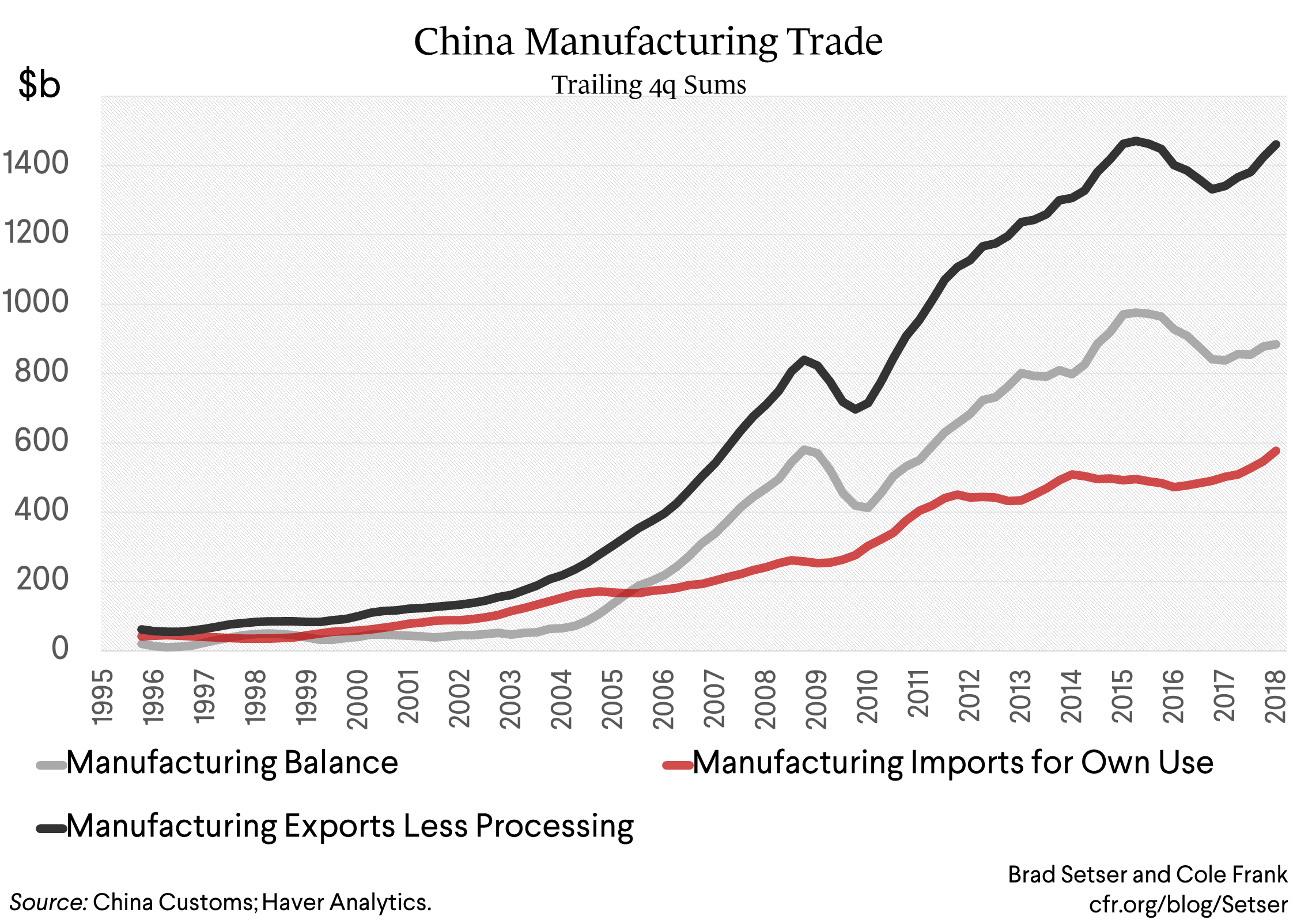

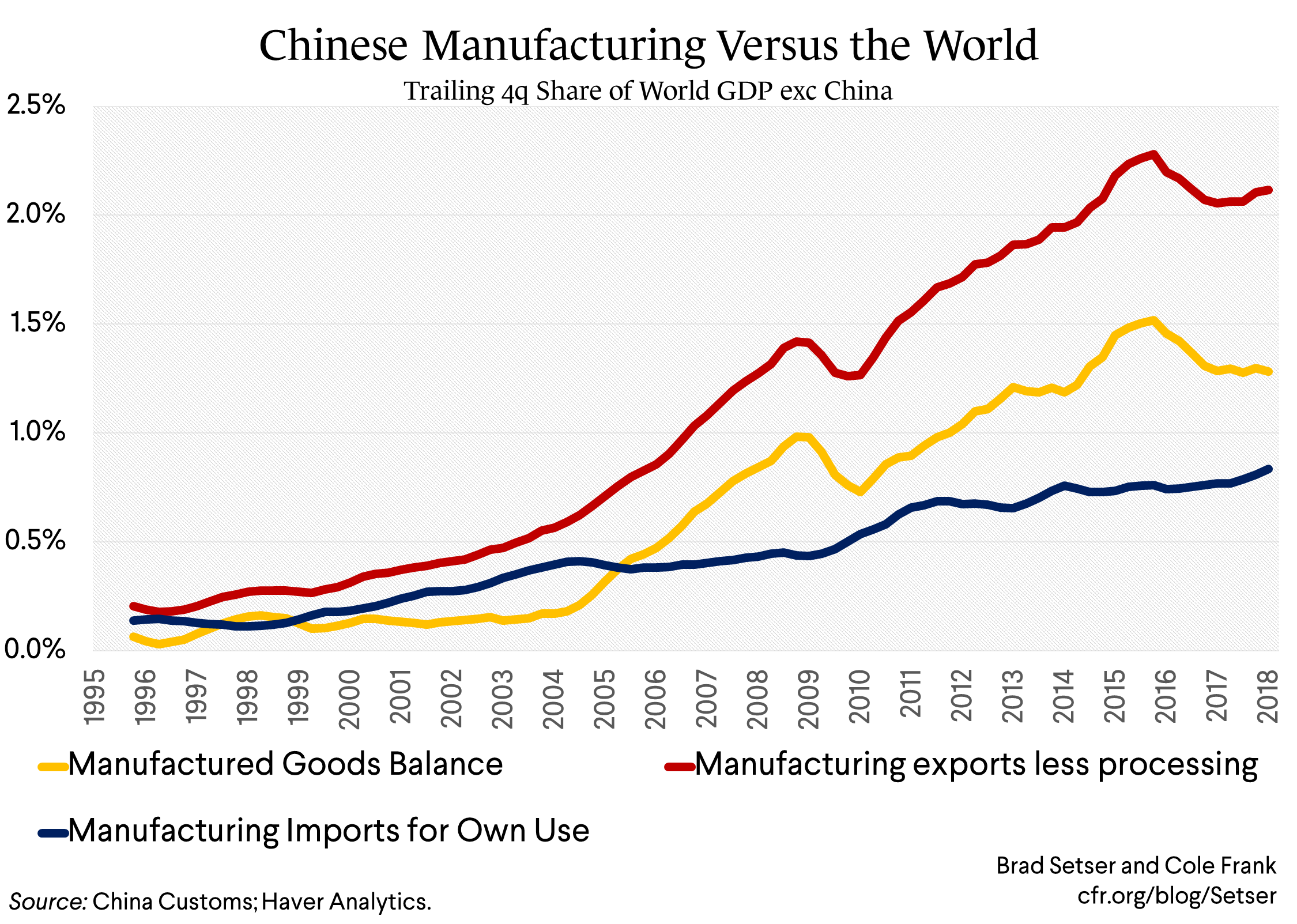

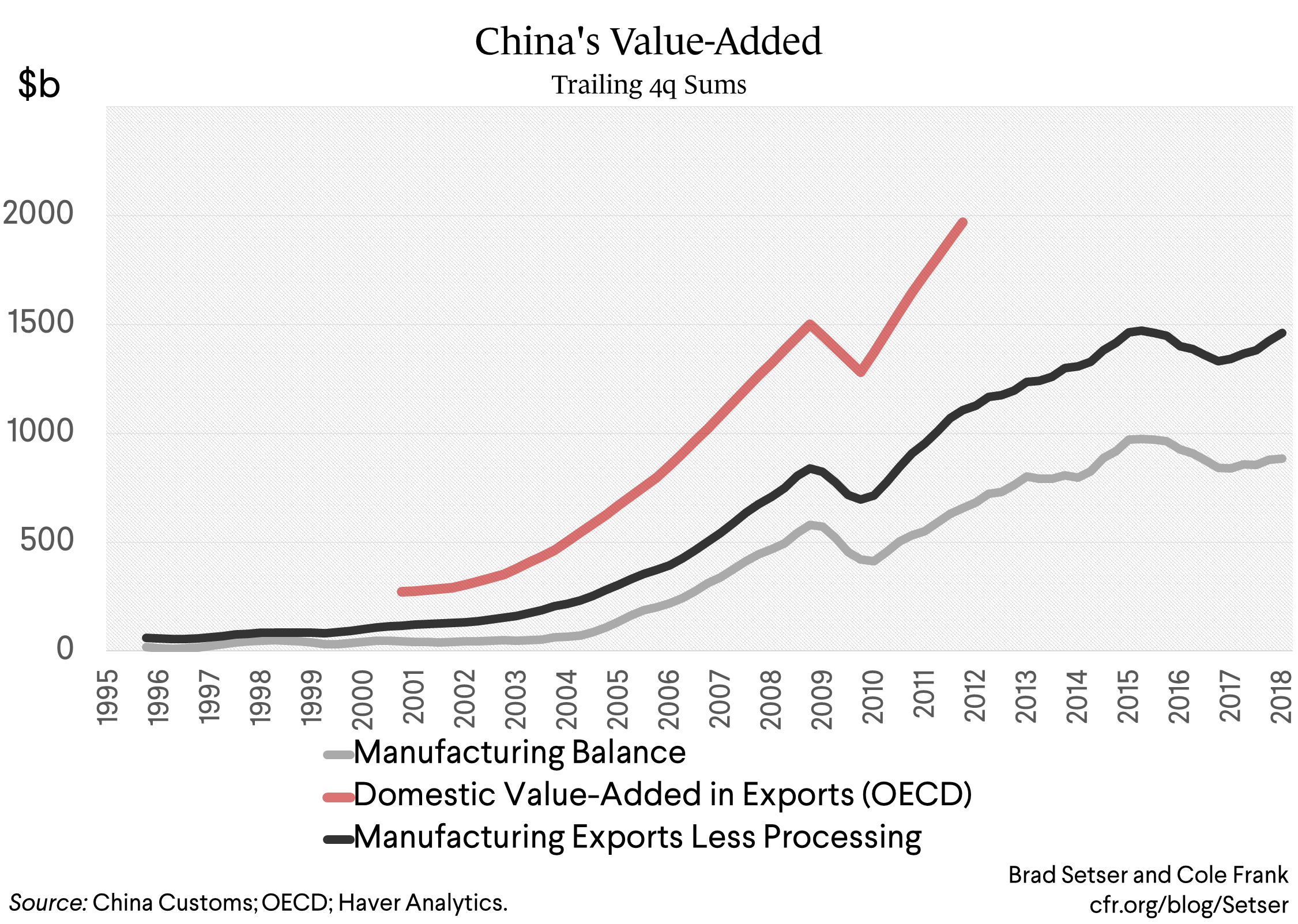

(*****) I have more charts too! The fall in China’s exports to GDP ratio over time has gone together with falling imports of components for re-export. As a share of China’s GDP, Chinese value-added in the export sector hasn’t actually fallen much. In dollar terms (or relative to the GDP of its trading partners) it is up.

(******) Goldman’s Asia team has a nice report showing China’s rising self-sufficiency in a range of capital goods sectors. Its continued reliance on imported semiconductors isn’t typical.