The U.S. Shock to Global Demand in Q4 (Before the Coronavirus)

The large fall in U.S. imports in Q4 slowed global growth, as weak U.S. demand hurt the rest of the world more than it hurt the United States.

Tariffs, it is often said, impact the level of trade not the balance of trade. That’s the intuition behind the argument that Trump’s tariffs would not help him achieve his goal of bringing down the trade deficit. Especially if overall fiscal policy was expansive, and thus Trump’s fiscal (and tax) policy was working at cross purposes with his trade policy.

But there are a couple of important caveats here—caveats that sometimes get glossed over (I am guilty of this too).

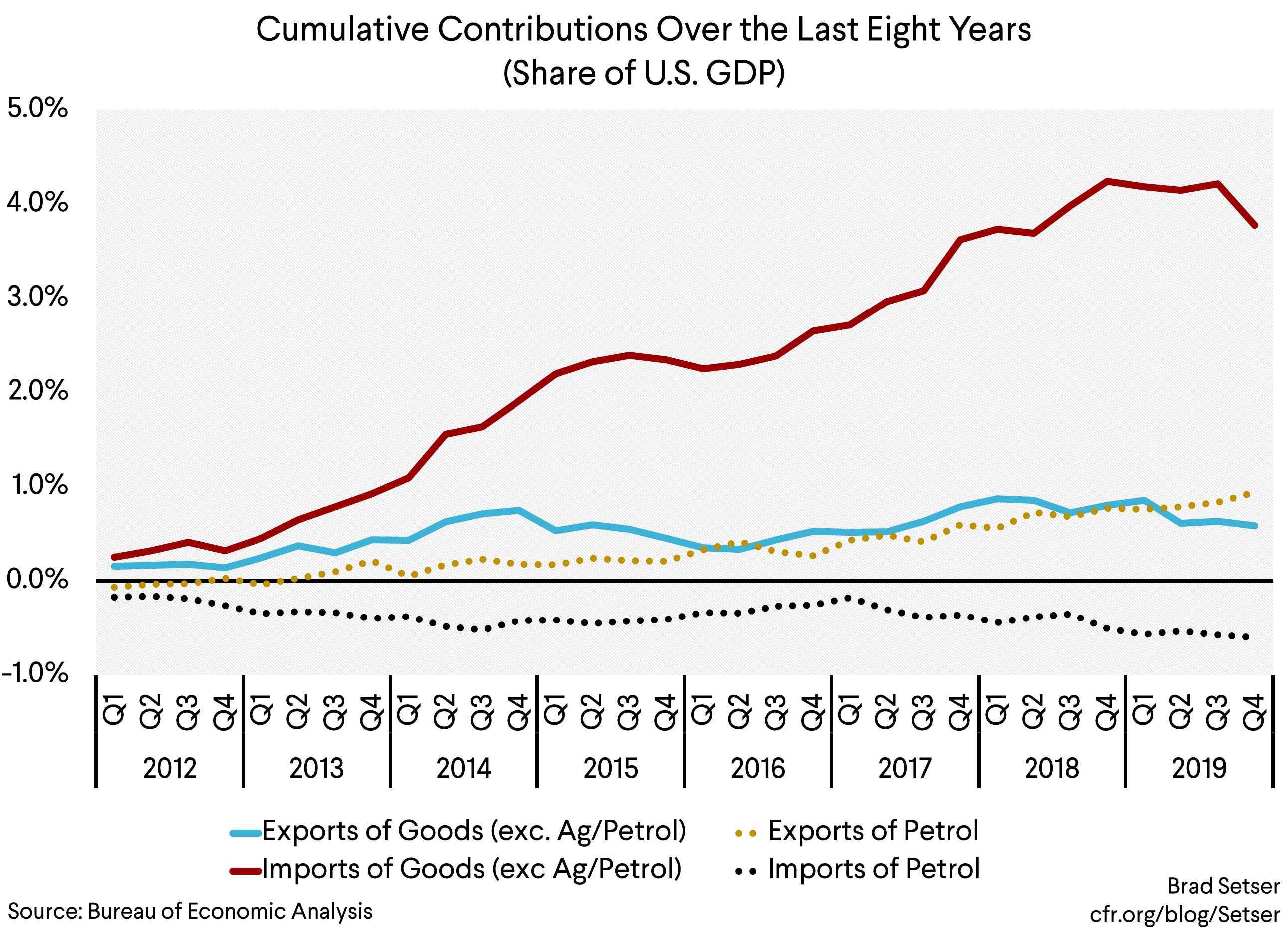

The tariffs can act as a form of backdoor fiscal consolidation. In order for tariffs to have no impact on the trade balance, the tariffs need to be “revenue” neutral. Trade scholars want to highlight the “trade” impact of the tariffs, not their fiscal impact—so they typically assume that any tariff revenues are offset elsewhere. But that’s not necessarily the case. The fairly broad based tariffs on China (+15 percent on average on a base of over $500b; total U.S. tariff revenue is now running at around $80 billion a year as compared to around $30 billion a year before Trump’s tariffs) act as a small tax on consumption (see Fajgelbaum, Goldberg, Kennedy, and Khandelwal; their most recent update/table on p. 6 suggests that the government captured 35 basis points of GDP out of the 60 basis points of GDP loss to consumers from the tariffs implemented before September 2019, which is over two times the gain to U.S. producers of import-competing goods).

Imported consumption to be sure, but in a lot of cases there aren’t great options for substituting away from China—which makes the tariffs a clear tax. And a consumption tax would be expected to have an impact on the trade balance.

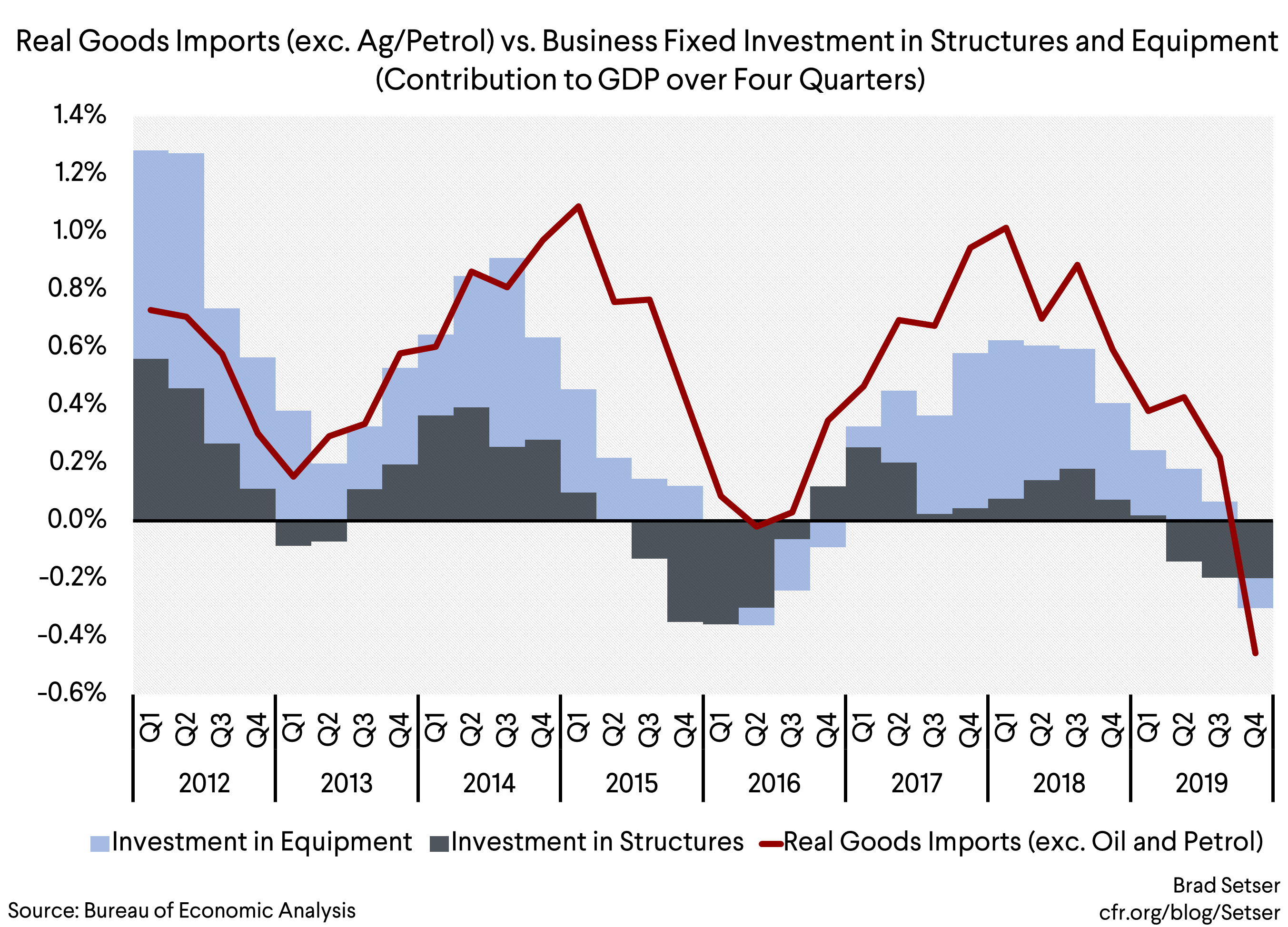

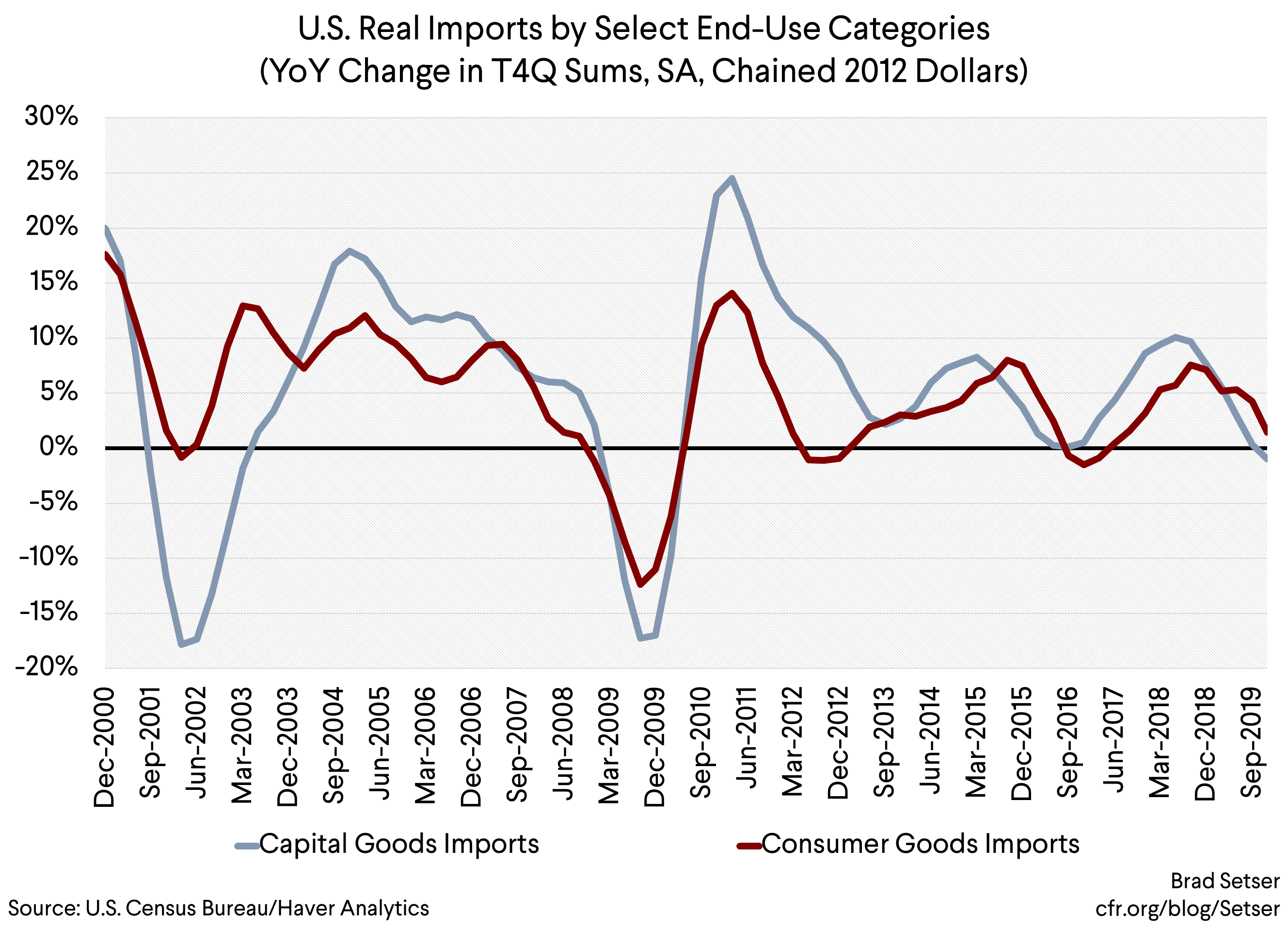

Tariff related uncertainty can also reduce investment. This argument can be exaggerated—there are several reasons why business investment in the United States has gone down that have nothing to do with tariffs. Global demand has been weak, weighing on investment in the export sector (and that export weakness is largely independent of Trump’s trade war; it is much more linked to dollar strength if you exclude soybeans). The Fed’s 2018 rate hikes should have reduced investment a bit in 2019 (they clearly contributed to the weakening of residential investment). And the oil patch’s increased discipline after a spending splurge in 2018 cut into investment. At the same time, there is little doubt that the tariffs did contribute to the slump in investment, especially the slump in new investment in business equipment. And there is plenty of empirical evidence that a slowdown in investment leads directly to a slowdown in imports (Bussière, Callegari, Ghironi, Sestieri and Yamano).

Now in both cases, the tariffs reduce the trade deficit by slowing growth—which isn’t the argument that Trump has typically made in their favor. Taxing imported consumption slows consumption growth —and higher uncertainty lowers business investment,

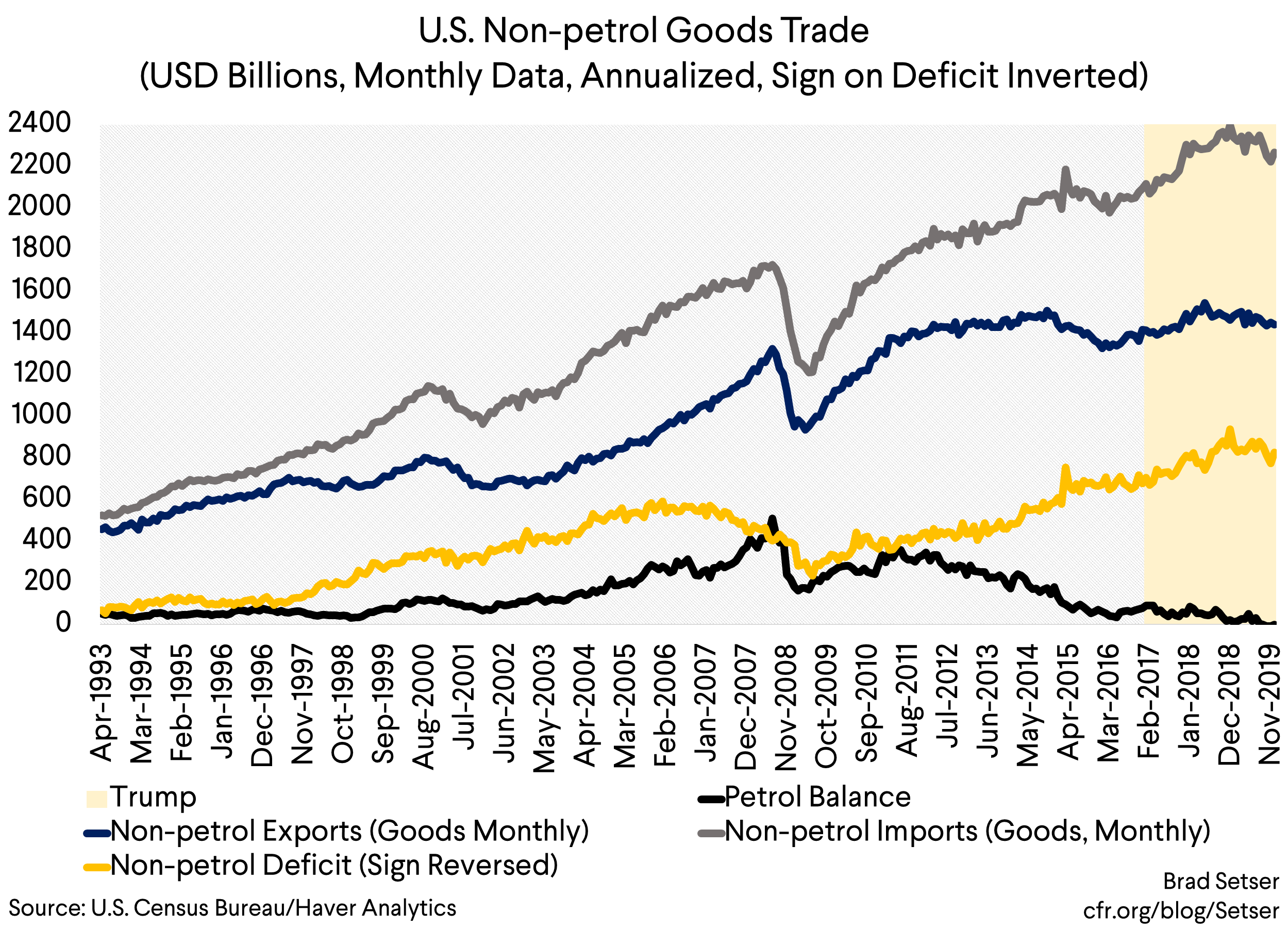

I mention these caveats because the story around Trump’s tariffs and their global impact changed a bit in the fourth quarter. U.S. import growth in Q4 was particularly weak and that brought the U.S. trade deficit down in Q4 (the non-petrol deficit is essentially flat for the full year).

This matters much more for the world than for the United States—in a sense, America’s trade partners absorbed much of the slump in business investment, limiting the direct impact of that slump on the broader U.S. economy. That’s in effect what a “positive” contribution to growth from falling imports means—the weakening of U.S. demand was felt globally, rather than in the United States.

And as a result, it isn’t really still accurate to say that Trump’s tariffs have simply diverted U.S. demand toward other trading partners. Overall imports fell a bit late last year (the January advance data suggests this continued in 2020, and subsequent data will be so influenced by the coronavirus, as a health shock has been layered onto the tariff shock and the January Phase 1 deal)

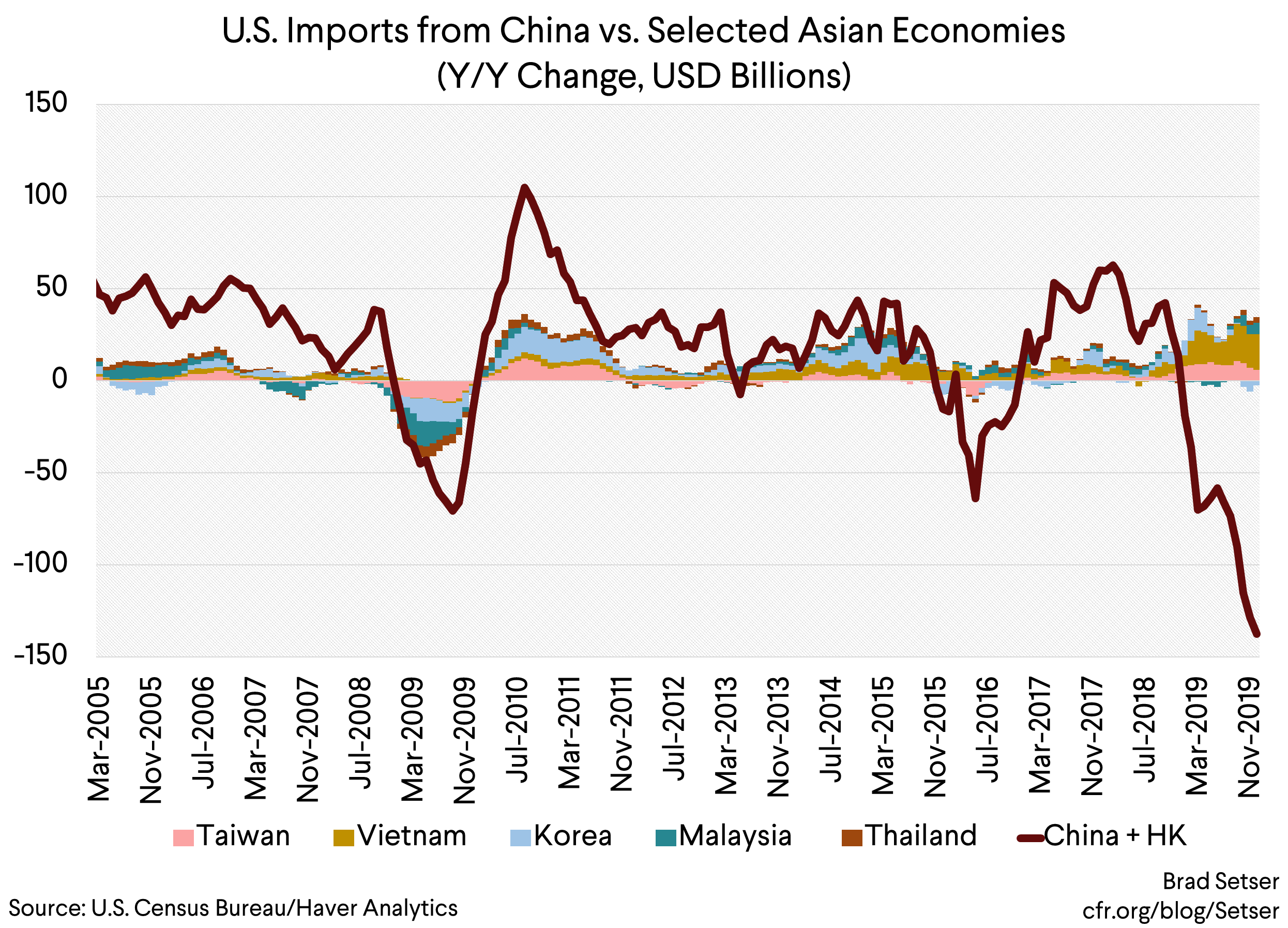

That to be sure is still an important part of the story—Trump has delivered an enormous positive shock to the Vietnamese economy. Vietnam’s exports to the U.S. jumped by $17.5 billion in 2019, driving a similar increase in its bilateral trade surplus with the United States (the parts that go into the world’s electronics are no longer primarily made in the United States, setting aside Intel’s Oregon chip production). But the rise in imports from other trading partners has not been anywhere near large enough to offset the fall in imports from China.

This is clear in the global data. In the summer, I noted that U.S. imports (excluding petrol) from the “not heavily tariffed” world were rising in line with the U.S. economy even as imports from heavily tariffed China were slumping. That’s no longer the case. In the fourth quarter, imports of consumer goods (tariffs on China, but also an inventory correction), autos, and capital goods were all weak.

U.S. GDP rose in the fourth quarter, in a sense, because the fall in U.S. demand was concentrated in goods, and concentrated in import goods—so demand for U.S. output (mostly services) stayed robust while the rest of the world saw a significant fall off in U.S. demand for its exports.

Now this all predates the coronavirus, which will deliver an enormous shock to all trade in the first quarter (but especially tourism trade, given the fall off in air travel) and likely the second quarter. More narrowly, the presence of a new shock will make it harder to determine if the fall in U.S. imports in the fourth quarter was a blip tied to a period of unusual weakness in investment in “tangible goods,” or if it was the start of a more persistent trend.