The dollar—to many people’s surprise—has depreciated this year. That depreciation comes after a rise in late 2016 following Trump’s election, and after a large appreciation in 2014.

To me, the dollar’s recent fall is a good thing.

Since its 2014 appreciation, the dollar has been too strong for the manufacturing side of the U.S. economy. Manufactured exports fell as a share of U.S. GDP in 2015 and 2016, and in my view were on track to continue to fall had the dollar’s late 2016 level been maintained. Even with the latest move the dollar would need to depreciate by substantially more (at least 10 percent) to get back to its early 2014 levels.

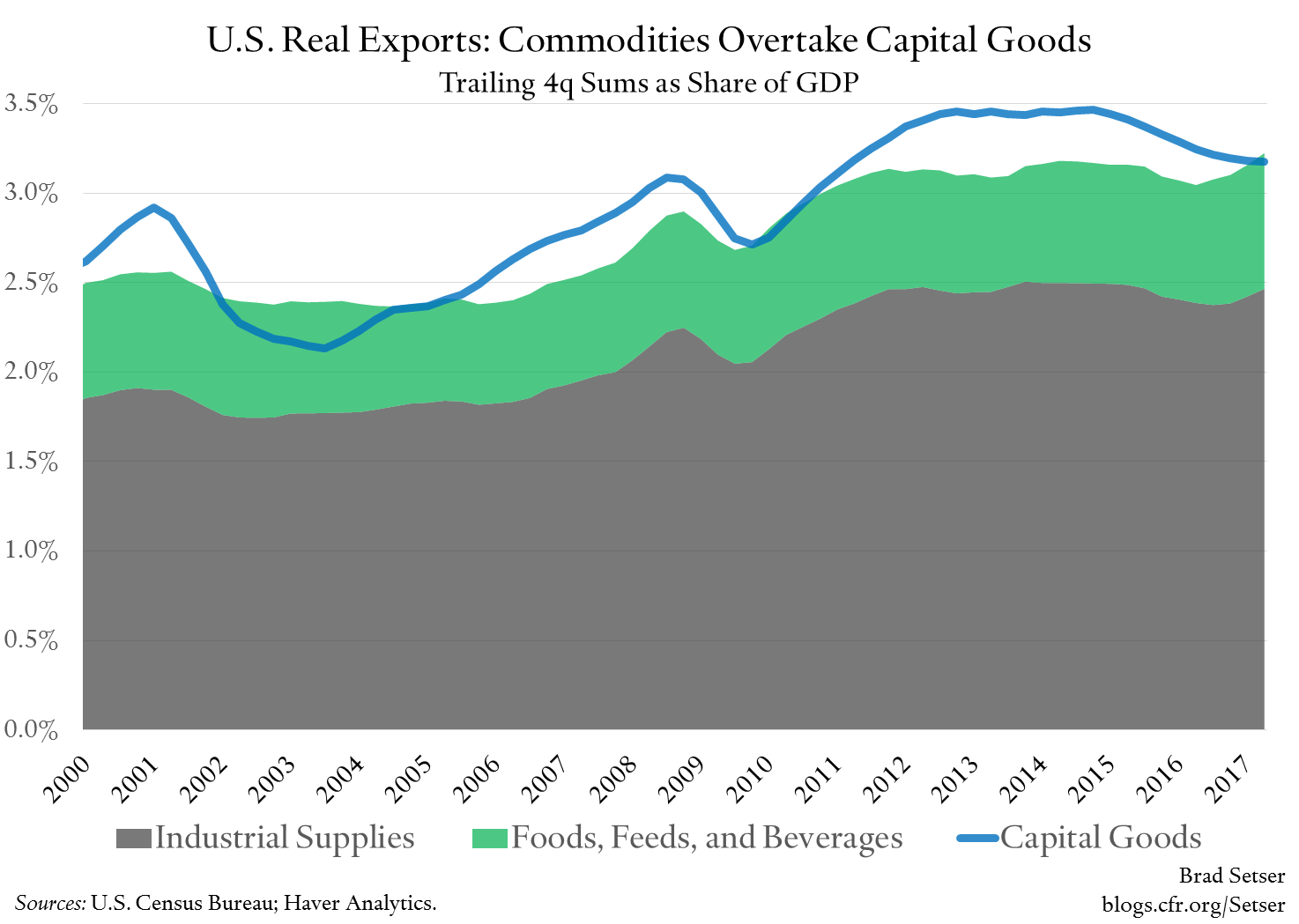

It is not hard to see the slump in manufactured exports in the trade data. Look at the Brookings data visualization. Or the following chart.

Since 2014, the U.S. slowly has been transforming into an exporter of commodities rather than an exporter of capital goods. Real exports (in 2009 dollars) of industrial supplies (lumber, coal, ores, petrol, chemicals and the like) and agricultural goods now exceed real exports of capital goods (aircraft, semiconductors, generators, large diesel engines, and the like).*

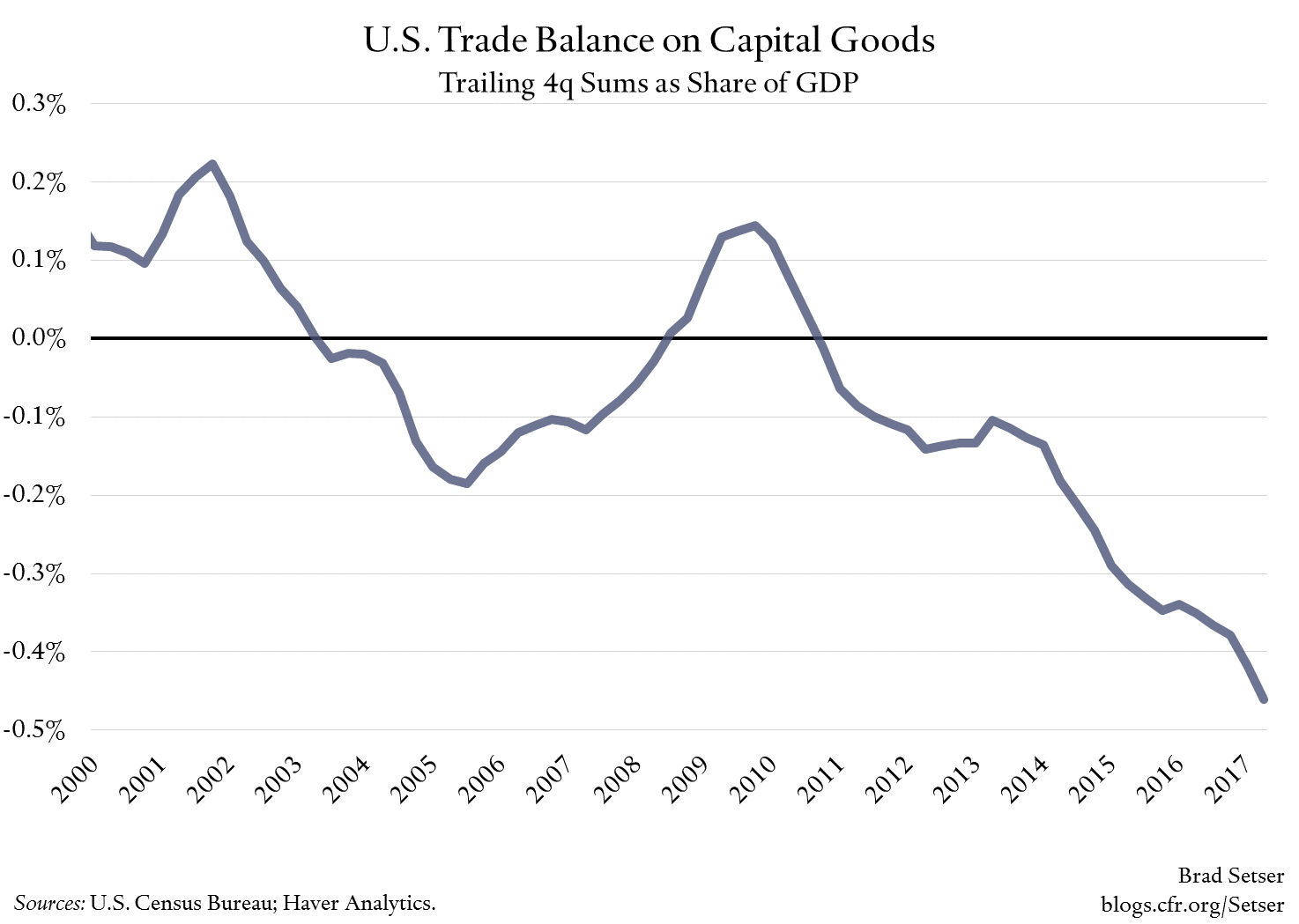

And you can see the impact of the dollar’s strength in the growing deficit the U.S. runs in high-end capital goods.

Much of the west coast of the U.S. probably “works” as an exporter of commodities, tourism services (Hollywood, Vegas, the Grand Canyon), high-end real estate and software and electronics related intellectual property (even if a lot of that IPR is currently exported to the Caribbean and Ireland at an artificially low price for tax reasons).**

But a currency union that includes the Midwest and Southeast, in my view, does not.*** Shrinking exports of high end manufactures—and a growing deficit in manufacturing trade—are a structural problem for the overall economy, and an even bigger problem for some regions (if you have a Wall Street Journal subscription, there is a great map here).

Fortunately, the evidence of the past few years suggests that exports do respond, with a lag, to the dollar.

Nevertheless I do worry that the fall in exports from a strong dollar is a bit stronger than the rise in exports from a weak dollar: I suspect because there is a hysteresis effect: Once a factory is shut down, it stays shut down—and if firms don’t continuously invest to stay at the cutting edge of technology, it can be hard for a high-wage advanced economy to stay globally competitive.

The dollar’s depreciation is as much a function of what is going on outside the U.S. as it is a reaction to the low level of U.S. inflation and diminished expectations of large-scale tax-cut stimulus. China is growing at a decent pace again—for real I think, even if the IMF worries that its growth all comes from backdoor fiscal stimulus. And, at long last, the eurozone is recovering, and growing at a decent clip off internal demand.

But not everything that is happening outside the U.S. is positive.

Market pressure for the dollar to depreciate means other currencies face pressure to appreciate. And some countries—cough, especially some Asian economies—have a bad habit of resisting the appreciation of their currencies.

That is what is happening now.

Rather quietly, a large part of Asia is now intervening to try to cap the strength of their currencies.

India for example. Headline reserves are up $10 billion since the end of June, and the Reserve Bank of India’s forward book is also growing (it rose by almost $10 billion in July for example). India runs a current account deficit, so it gets a bit of a pass—.****

Thailand’s reserves are up $10 billion since the end of June (Thailand also has a big forward book, but that has been constant); it is now intervening at 33 baht to the dollar. And Thailand now runs a sizeable current account surplus.

Singapore looks to be intervening again, and probably by more than shows up on the balance sheet of its monetary authority. Singapore seems to be transferring a large share of the assets it buys to its sovereign wealth fund: that at least is how I explain the large rise in “official” deposits in the balance of payments data.

Taiwan, which scaled back its intervention and allowed the Taiwanese dollar to rise in the first part of the year, now seems to be back in the market to keep the Taiwanese dollar from rising through 30. The Taiwan dollar has been stuck near there all summer.

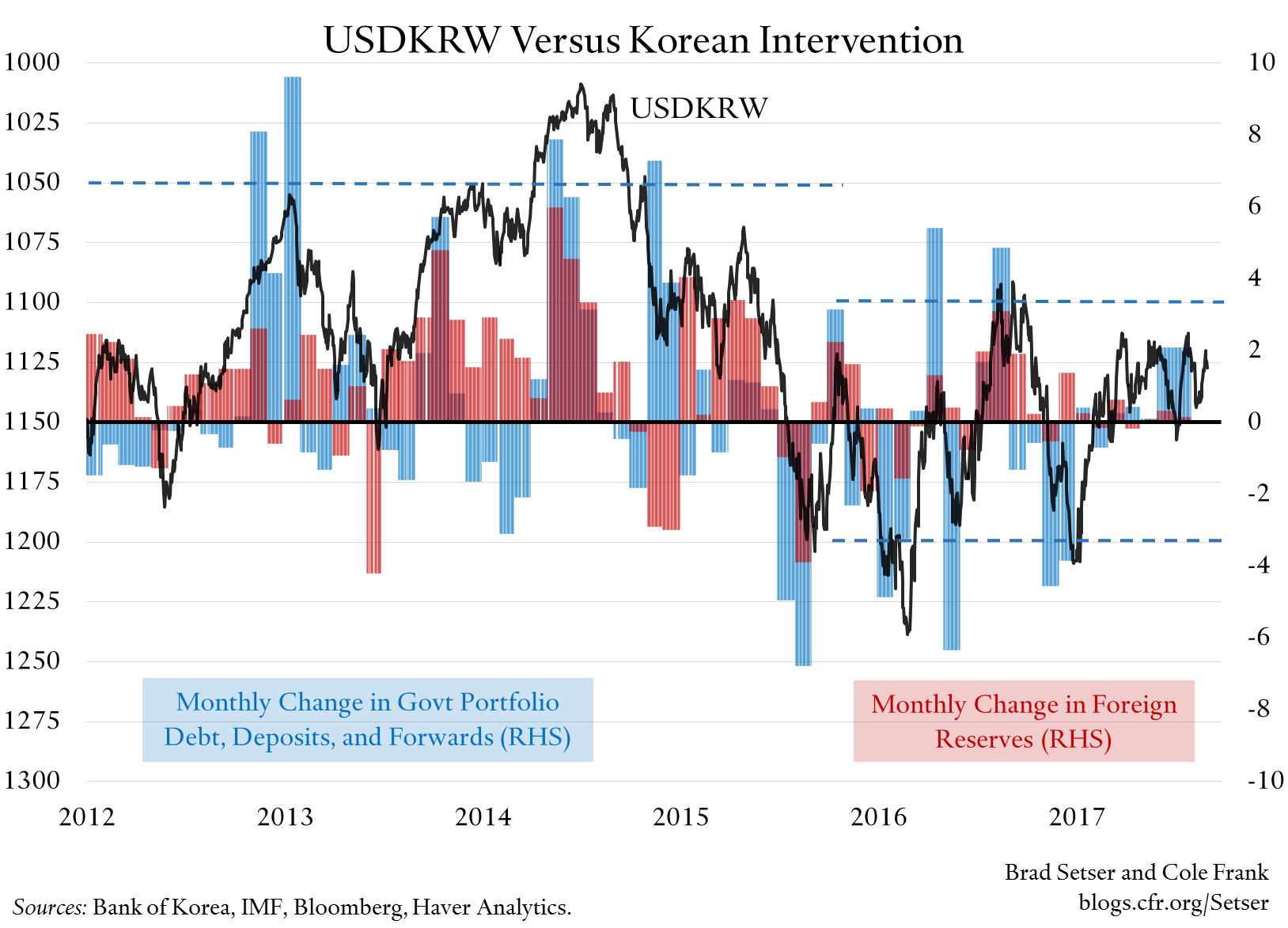

Korea has been intervening at times too. Korea’s forward book jumped by almost $1.5 billion in July—when the Bank of Korea almost certainly intervened to keep the won from rising through 1100 (it seems like Korea has been intervening between 1110 and 1120 this year). Then, well, the nuclear scare led the won to sell off a bit, taking the heat off the Bank of Korea. The Koreans also have structurally reduced their need to intervene by having their government pension fund build up its foreign assets at a rapid clip.

To be sure, the size of this renewed intervention isn’t huge, at least not compared the peak intervention levels of the past. Partially because a lot of countries aren’t keen to add to their formal reserves and thus have encouraged outflows through their sovereign wealth funds, their pension funds, their government development banks, and other state-controlled balance sheets. They don’t need more safe reserve assets for macro-prudential reasons, and pension fund and state bank outflows don’t catch the attention of the U.S. Treasury and the IMF in the way reserves do. And partially because China hasn’t returned to the days when it was buying between $30 to $70 billion a month. *****

But the return of the old correlation between dollar weakness against the euro and intervention in Asia is still unwelcome. Some balance of payments surplus countries are resisting pressure on their currencies to appreciate even when they have plenty of fiscal space to offset a slowdown in exports through an increase in domestic demand.

And in the process, they are working against global balance of payments adjustment, with real implications for parts of the U.S. economy. Their intervention ultimately means less U.S.—and less North American—production of auto parts, semiconductors, and the like.

No one looks poised to cross the U.S. Treasury’s new trip wires and mechanically trigger a designation of manipulation. The United States’ bilateral deficit with Thailand is just under the $20 billion threshold, and the U.S. runs a bilateral surplus with Singapore (even with Singapore’s massive global surplus) thanks in part to large exports of fuel oil. Taiwan and Korea are keeping their visible intervention below the Treasury’s two percent of GDP threshold.

But if I were in 1500 Pennsylvania Avenue, I would still want to use the October foreign exchange report to signal a bit of concern…and to indicate that “currency” isn’t just an issue with China.

* Real quantities technically shouldn’t be compared to other real quantities. But the distortion from scaling real exports to real GDP is smaller than the distortions created by swings in commodity prices in a nominal chart—I used a bit of poetic license to show that real capital goods exports have grown less rapidly than the overall U.S. economy in the last few years.

** I know am overgeneralizing a bit. Seattle is a huge exporter of aircraft, and Oregon exports a lot of semiconductors.

*** Texas and Louisiana have a big energy sector, but the Piedmont doesn’t—historically, it has been quite dependent on manufacturing jobs (furniture, textiles, and clothing, among others). Consequently, a large share of the communities most impacted by the China shock are in the southeast.

**** India holds a substantial share of its reserves in euros and pounds, so some of the rise in headline reserves comes from valuation. But India also intervenes in the forward market, and the data for end-August forwards isn’t yet out—so I am confident that I haven’t misstated the basic facts. India incidentally is a model for transparency here; you can find its actual intervention in the RBI’s monthly statistical bulletin ($3 billion in spot in June, with another $3 billion increase in forwards; $3 billion spot in July, with another $9 increase in forwards). Indonesia has also been adding to its reserves but I really give it a pass—as it has long been on the edge of being under-reserved.

***** I am watching to see if the August and then the September intervention proxies show any change in the PBOC’s behavior—the CNY is obviously appreciating right now, and in the past the PBOC has had to intervene both to limit the pace of appreciation—not just the pace of depreciation. China’s recent decision to make it cheaper to short the yuan—and, perhaps, to loosen some controls on outward direct investment—certainly suggests the PBOC is now worried about the pace of appreciation.