What Would Happen if China Started Selling Off Its Treasury Portfolio?

Just how important have foreign inflows been to the Treasury market?

The trade war between the U.S. and China is starting to get serious. President Trump is now threatening tariffs on up to $450 billion of Chinese imports, or about 90% of what the U.S. imported in 2017. Tariffs will soon be imposed on around $35 billion of Chinese goods, so the threat isn’t entirely hypothetical either—even though the administration has yet to go through all the legal hoops needed to implement the full $450 billion in tariffs.

As the Trump administration has emphasized, China cannot match the U.S. by putting tariffs on $250 billion, let alone $450 billion in U.S. exports. The U.S. just doesn’t export that much to China. China reports goods imports from the U.S. of $150 billion, and if you add in goods exports to Hong Kong, the U.S. data would suggest no more than $170 billion in exports (the reported $130 billion in exports directly to China in the U.S. bilateral data is clearly a bit too low, but only a bit).

China could try to match the U.S. by putting higher tariff rates on its imports from the U.S. than the 10 percent that the U.S. has proposed on most imports from China—but that’s rather artificial, and even self-defeating. For commodities, any tariff will redirect Chinese purchases toward other suppliers. And for manufactures, the goods China imports tend to be weighted heavily toward goods China either doesn’t make at home (wide body aircraft for example) or inputs into China’s export machine (where tariffs would encourage firms to shift assembly elsewhere).

China also could respond asymmetrically, and look toward other levers that it may have over the U.S.

Three stand out:

- Imposing new limits on U.S. firms operating in China, and taking actions that limit their sales in China. Apple and GM sell a lot of made-in-China phones and cars that wouldn’t be impacted by tariffs. I do though wish there was a bit more rigor in separating out the impact of Chinese action on the profits of U.S. companies from the impact of Chinese action on the U.S. economy: if China makes it harder for Starbucks to make coffee in China (maybe using Swiss beans? for tax purposes) or McDonalds to make hamburgers in China, there won’t be much impact on the overall U.S. economy. Chinese made hamburgers aren’t the same as U.S. made planes. In 2017 U.S.firms earned around $13 billion (according to the U.S. data) in China on roughly $200 billion in sales.*

- Weakening China’s currency to offset the drag on China’s economy from far reaching tariffs. A standard rule of thumb is that a 10% depreciation (against a basket) raises net exports by about 1.5 percentage points of GDP—which could effectively offset realistic estimates of the economic drag of a trade war on China.** This option isn’t without risks—it could reignite now contained capital outflows from China, and China might ultimately end up with a bigger-than-expected depreciation. But it isn’t beyond China’s capabilities to engineer a weaker currency (see 2015-16 for a playbook—all it would take is a surprise one-day depreciation, and the market would do the rest until China resists and signals the depreciation has gone far enough).

- And the perennial threat that China would sell its Treasuries. That could happen as a byproduct of a decision by China to push its currency down—if China signals that it wants a weaker currency, the market would sell yuan for dollars, and controlling the pace of depreciation would require that China sell reserves. Or could happen even if China maintained its current basket peg and shifted its portfolio around—selling Treasury notes for bills, or selling Treasuries and buying (gulp) Bunds (if it can find them—it might end up buying French bonds instead) or JGBs.

The bond market—judging from the market moves on Tuesday—doesn’t seem terribly worried about the risk that China would sell Treasuries. Rightly I think.

If Treasury sales came in the context of a decision by China that it wanted a weaker currency to offset the economic impact of Trump’s tariffs (or simply a decision by the PBOC that it needed to loosen monetary policy in response to a slowing Chinese economy, and thus to no longer follow the Fed), the disinflationary impulse from a weaker yuan (and a broader fall in most Asian currencies and a rise in the dollar) would likely be more powerful than the mechanical impact of Treasury sales. That is the lesson of 2015-16.

And that gets at a hugely contested question—just how big is the mechanical impact of Chinese sales (or for that matter Fed purchases) on the Treasury market?

A quick reminder. Treasury rates are usually understood to be a function of the expected path of Federal Reserve short-term policy rates. And a separate “term premium” that raises (in most states of the world) long-term interest rates a bit over the expected path of short-term rates. The impact of central bank purchases and sales on that term premium is a matter of huge debate.

Purists (Michael Woodford, for example) argue that “flows” have almost no impact on the Treasury market, and the only thing that really matters is the expected path of the Federal Reserve.

A bigger fiscal deficit and a larger Treasury financing need? Only matters if it changes the path of Fed policy (which it should, a larger fiscal deficit typically stimulates demand and leads to higher expected interest rates).

Chinese sales, assuming China puts the proceeds of its sales in cash rather than buying foreign exchange? They would only have an impact if they change the path of the Fed.***

I do, though, think “flows” matter. A standard, empirically well-grounded [PDF] rule of thumb is that 1% of GDP in Federal Reserve “QE” or asset purchases reduces long-term Treasury rates by about 5 basis points, so 10 percent of GDP in “QE” would be expected to reduce the ten year yield by something like -50 basis points (here are the latest projections from Fed staff).

Estimates for the impact of Treasury budget deficits on long-term rates are of similar though somewhat larger magnitude (Goldman—See their May 12th paper, no link—has done a lot of very good work on this, they put the impact of a 1% of GDP increase in the budget deficit at around 20 basis points, but that estimate includes the impact the fiscal deficit will have on the Federal Reserve’s expected interest rate path as well as the impact of increased issuance on the term premium).

And estimates of the impact of foreign central bank purchases on the Treasury and Agency market are in the same ballpark. The Warnocks’ canonical work [PDF] for example estimated that 4% of U.S. GDP in central bank purchases back in 2005 reduced 10 year yields by maybe 80 basis points. That is probably on the high side. Other work [PDF] by the Federal Reserve also found a substantial impact of foreign purchases on 5 year yields. And a guy named Ben Bernanke put his John Hancock on this paper.

You can get even more technical and say what matters is the Fed (or China’s) share of the marketable stock and the like, but the “flow” based rules of thumbs are good first approximations. The Beltran, Kretchmer, Marquez, and Thomas paper (p. 12), for example, estimates that a 1% increase in foreign official holdings vs. the outstanding stock lowers the term premium on 5 year bonds by about 5 basis points. At the end of the day, large flows lead to large changes in the stock of foreign central bank holdings.

So what happens if China starts selling now?

If China sold its entire Treasury portfolio (reported to be around $1.2 trillion, but likely more like $1.3 trillion because of the “Belgian” account, and China also has another $200 billion in Agencies) it would generate about 6% of U.S. GDP in sales (7% of GDP counting China’s $200 billion in Agencies). Using the “QE” literature to estimate the impact of Chinese “QT,” those sales in the first instance would be estimated to raise long-term interest rates by say 30 basis points. There is of course uncertainty around that estimate, as some of the pre-QE papers would suggest a bigger impact. The impact would be larger in the short-run but then higher U.S. rates (relative to still-low European rates) would pull private funds into the U.S. fixed income market.

A 30 basis point rise in the ten year, even 60 basis point rise in the ten year, would be painful, but also ultimately bearable.

Critically, these estimates assume that the Fed doesn’t react to a rising term premium and a steepening of the yield curve by easing.

Yet the Fed has every reason to react. If China’s sales are pushing up long-term rates and slowing the U.S. economy, the Fed logically should slow the pace of rate hikes, or scale back its “quantitative tightening”/ balance sheet roll-off.

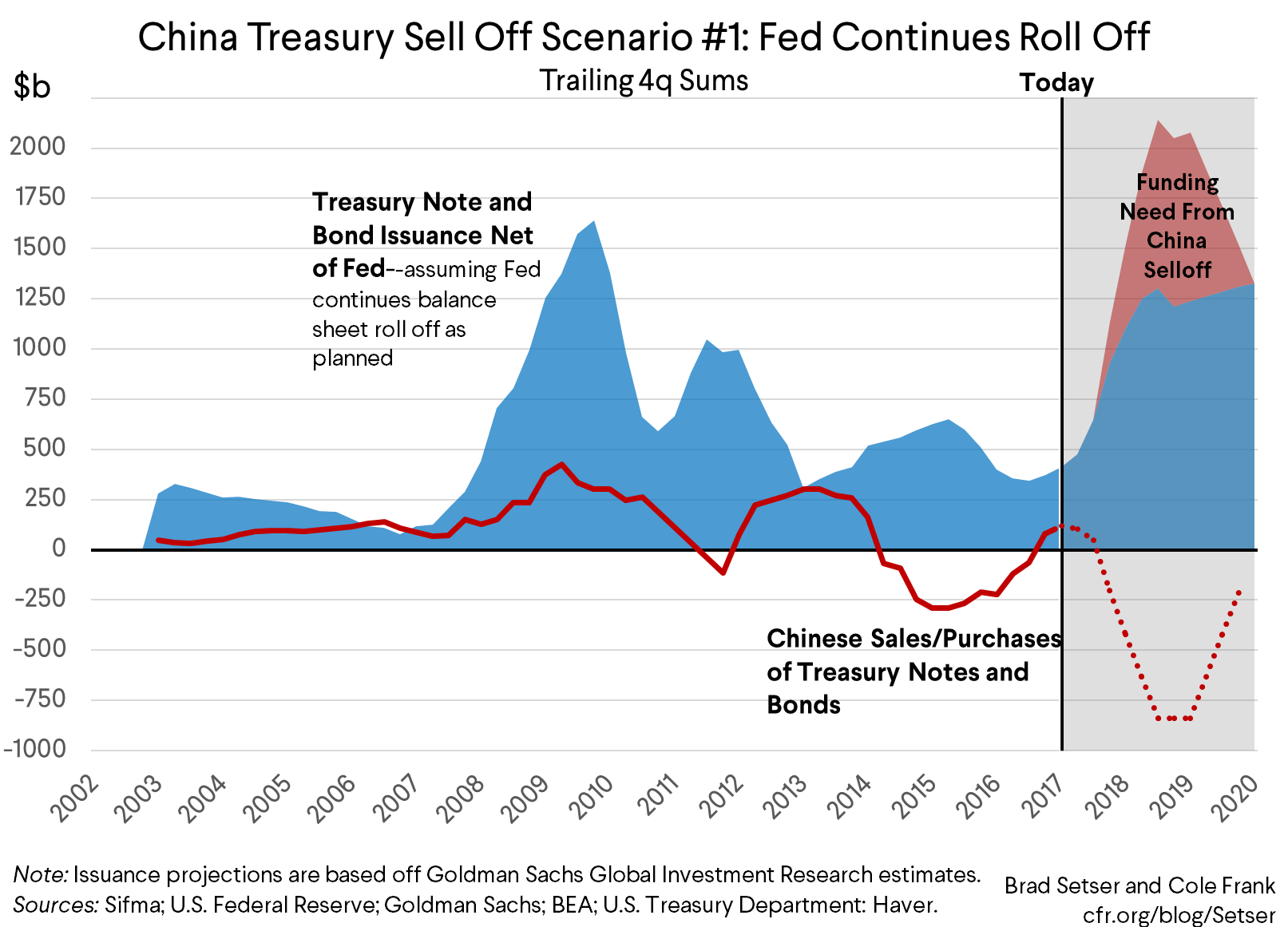

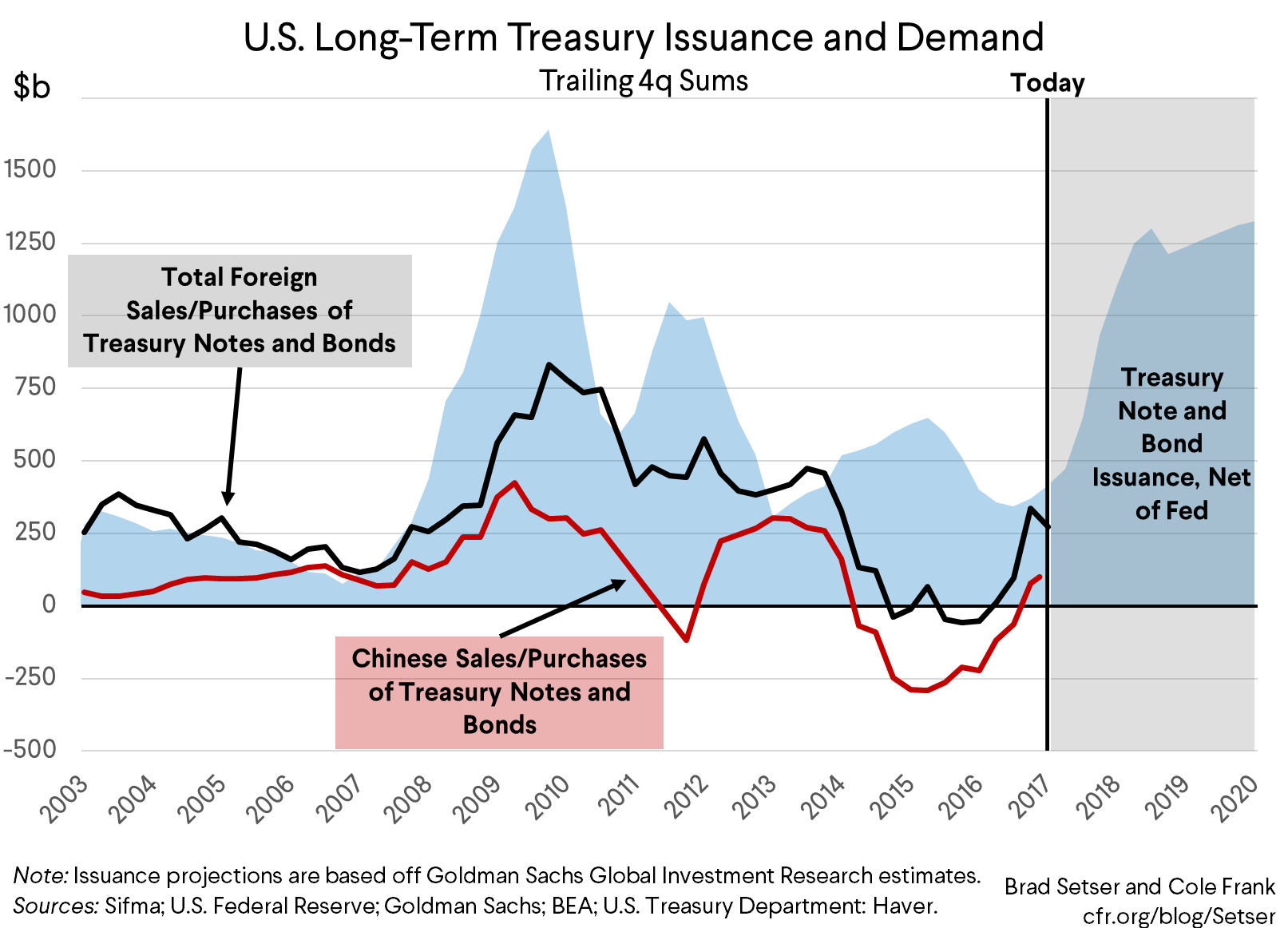

My data analyst extraordinaire Cole Frank and I tried to illustrate this all graphically. I won’t bore you you with the technical details of how we constructed the following graphs. Suffice to say that we used the balance of payments data by country, adjusted Chinese purchases to capture the “Belgian” distortion, and divied up the debt purchases in the balance of payments between Treasuries and other bonds using the survey data. Basically, we tried to replicate the methodology the BEA uses to estimate overall purchases of U.S. debt—but to provide detail that the BEA now suppresses on China’s purchases of Treasuries.****

And we didn’t bother with Agencies—even though we know looking only at Treasuries hugely understates China’s impact on the U.S. fixed income market from 2005 to 2008, when it was buying as many Treasuries as Agencies. That’s all ancient history now. The current flow, and current debate, is all about Treasuries.

On the surface, it looks like the U.S. is extraordinarily vulnerable. The stock of Treasuries that the market has to absorb to fund the rising U.S. fiscal deficit is objectively quite large, as the U.S. has ramped up issuance while the Fed is reducing its Treasury holdings.

And if China started to sell, the amount of U.S. paper that non-Chinese investors would need to absorb would be extremely large (Cole and I assumed about $200b in quarterly sales by China, i.e. the most they sold in a 3-month period between 2015 and 2016/ chart here)—or sales of around $850 billion (over 4% of U.S. GDP) in a year. Under these assumptions, it would take China a year and half to unload its Treasury portfolio. And, for that time, the U.S. then would need to place around $2 trillion a year with non-Chinese investors.

That said, looking at total issuance relative to Chinese purchases is only one way of cutting the data.

Foreign demand hasn’t been as central to the Treasury market in the past few years as it was in the past—in part because the current account deficit (2.5% of GDP) is below the fiscal deficit (4% of GDP, but heading to 5% fast). Foreigners bought $275 billion of long-term Treasuries last year, so total foreign inflows into Treasuries were a bit less than 1.5% of U.S. GDP, well below their pace immediately after the global crisis.*****

And Chinese demand hasn’t been as important as in the past (China’s large holdings reflect the legacy of past intervention more than current intervention—China’s recent flow has largely been channeled through the state banks to markets far riskier than Treasuries).

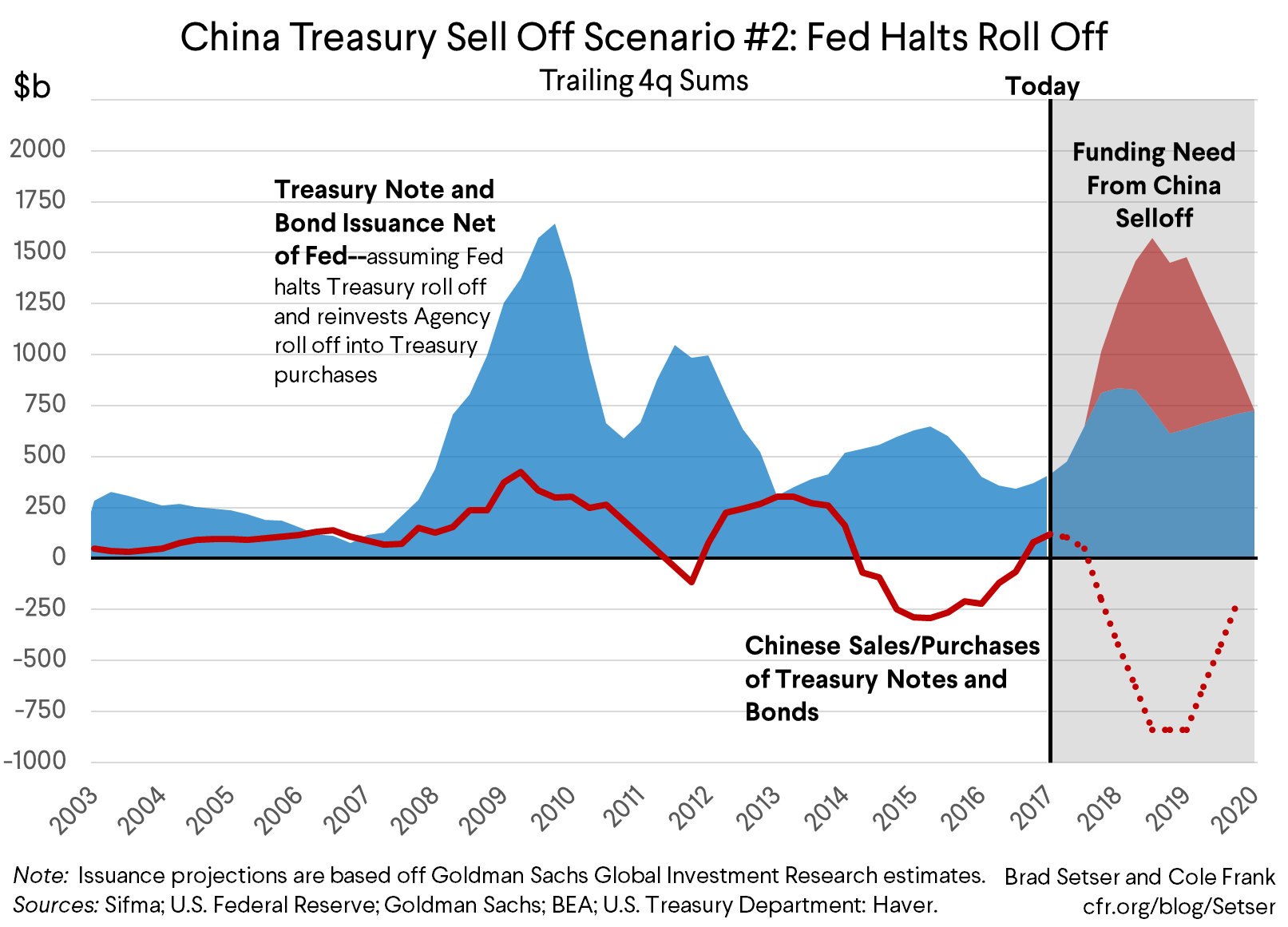

Most importantly, China’s sales are in some ways easier to counter now, as the Federal Reserve is in the middle of hiking cycle. It is fairly easy for the Fed to signal that it expects fewer rate hikes going forward than it expects now. And the Fed has a second, fairly direct, way to respond to Chinese sales: change its pace of balance sheet roll off. Roll off is scheduled, counting Agencies, to rise to $150 billion a quarter/$600 billion a year by the fourth quarter. Stopping that, and perhaps signalling that over time the Fed would raise the size of its balance sheet in the long-run would provide a powerful counter to Chinese sales. The combination of a bigger “terminal” Fed balance sheet and a change in rate expectations would, in my view, be more powerful than anything that China could threaten.

Stopping the reduction in the roll-off would reduce the total non-Chinese funding need by about a quarter, to around $1.5 trillion.

Finally, the Treasury could, at the margin, start issuing more bills and fewer notes (notes are the formal name for coupon paying treasuries with a maturity of over a year, bills don’t pay a coupon and that typically have a maturity of a year or less), offsetting the impact of China selling longer dated bonds and likely increasing its cash holdings. Or the Fed could raise the maturity of its holdings, selling short-dated bonds and buying long-dated bonds in a new operation twist. There are no shortage of technical options to limit the impact of China’s sales.******

I am not in the business of giving China advice on how to upset U.S. markets.

But if the National Security Council ever was convened to discuss China’s options for asymmetric retaliation, I would encourage it to spend most of its time worrying about the consequences of a Chinese exchange rate move. The impact on any such Chinese depreciation on the United States would be limited if the U.S. could convince its allies in Asia to take action to avoid following China’s currency down (even though it is against their short-run economic interest; their export driven economies compete directly with China). They have plenty of reserves—and could sell those reserves to absorb market pressure for their currencies to depreciate along with the Chinese yuan. But they aren’t likely to do that if they think the U.S. brought on the Chinese devaluation through reckless trade action.

And I would encourage the U.S. government to spend a bit of its time thinking about the impact of Chinese sales of assets other than Treasuries, a scenario that I discussed back in April with Joe Weisenthal and Tracy Alloway.

Treasuries sales in a sense are easy to counter, as the Fed is very comfortable buying and selling Treasuries for its own account. I have often said that the U.S. ultimately holds the high cards here: the Fed is the one actor in the world that can buy more than China can ever sell.*******

*/ It is quite likely that U.S. firms have found ways to shift profits out of China to low-tax jurisdictions, and the $13 billion in reported profits understates their “true” Chinese profits. But there isn’t any easy way to know just how much of the “excess” profits U.S. firms report in Bermuda, Ireland, the Netherlands, Singapore and Switzerland and other low-tax jurisdictions should be attributed to China.

**/ The U.S. has threatened tariffs on $450 billion of imports from China, which is close to 4% of China’s GDP. However, the actual economic impact of the full threatened tariffs on China would be smaller than the amount of trade covered. A reasonable estiomate would be in the range of 1.5 pp of China’s GDP. In a lot of cases U.S. importers would simply have to pay the tariff and continue importing from China as they have no viable alternative to Chinese assembly and supply in the short run.

***/ What would change if China shifted out of the dollar as well? Not much. Selling Treasuries and buying foreign bonds requires a series of transactions: first selling Treasuries for cash, then selling dollars for another currency, and then buying another country’s bonds. The first transaction in the only one the U.S. needs to worry about. Selling dollars for say the euro would drive the dollar down and the euro up, which would help, not hurt, the U.S. economy. Massive inflows into the euro area though might be a problem for the ECB ...

****/ The BEA releases data on purchases of all long-term debt by country in the “balance of payments by country” data set, but doesn’t provide a split between different kinds of long-term debt at such a disaggregated level. It does provide an overall split by instruments in another data table.

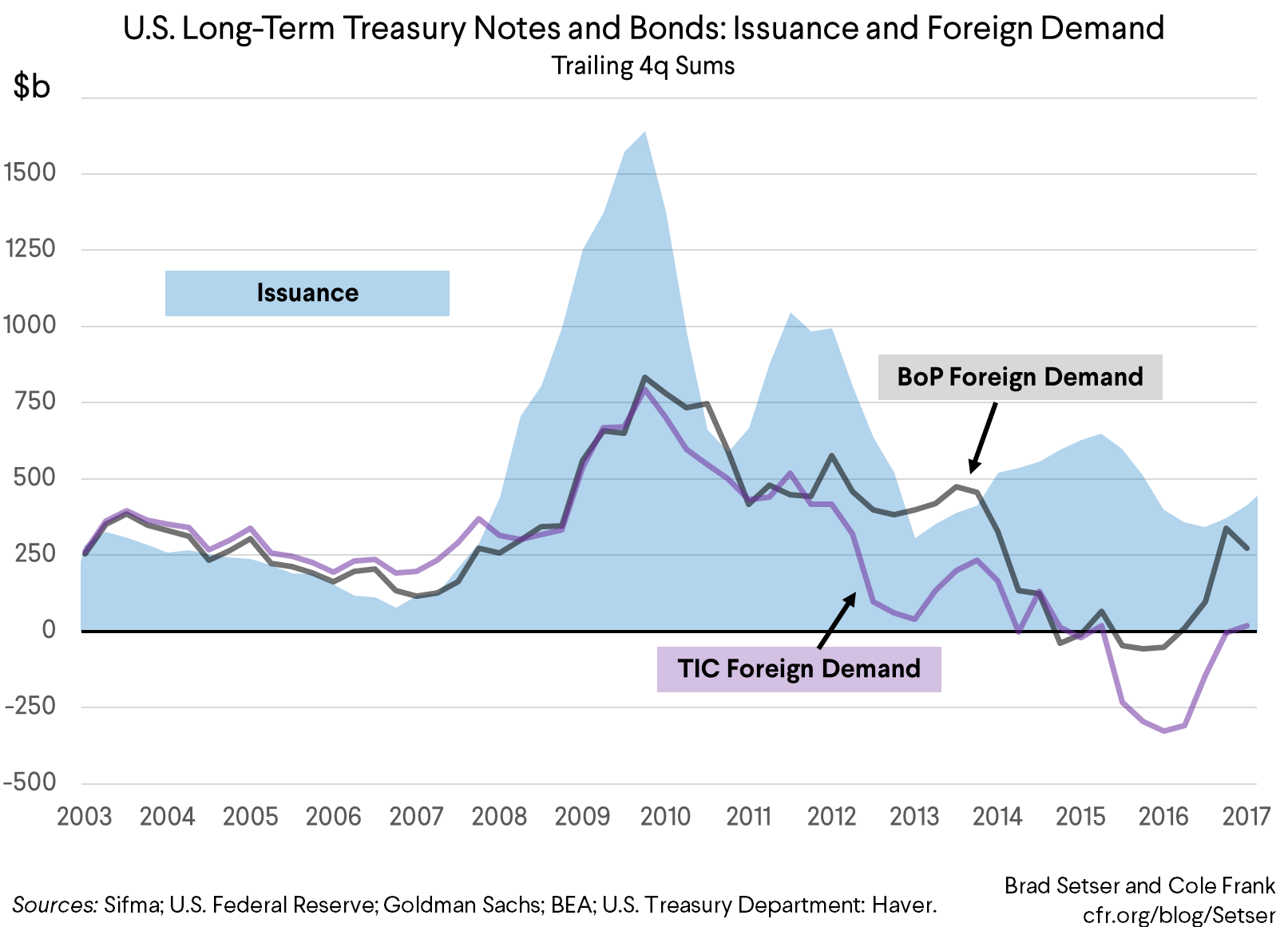

*****/ The balance of payments data, which maps to the custodial data, shows more Treasury purchases than the monthly TIC “transactional” data. The custodial data and the transactional data are collected in completely different ways. Most think the custodial data is better. The BoP data that we used for these charts ultimately is based on the survey data, and that shows a modest pickup in foreign purchases of Treasuries in 2017.

The discrepancy between the two data sources looks like this:

******/ I suspect Jerome Powell understands this; he has been on the Fed board a long time and has undoubtedly sat through many presentations on the impact of QE and QT. He served as the Under Secretary of Domestic Finance (the office of the Treasury in charge of debt issuance and cash management) in the Administration of George W. Bush. Plus, well, I think Ben Bernanke would take his call…

*******/ The Fed estimates the “peak” impact of QE on the ten-year term premium to be over 100 basis points (see Figure 3, p. 39). That’s bigger than any estimate I have seen of the impact of China’s purchases (logically enough, as the Fed ended up buying more ...)