How Are Trade Disputes Resolved?

Updated

With President Trump taking aim at existing trade agreements, countries are increasingly grappling with dispute resolution mechanisms and their implications for global trading rules.

What are backgrounders?

Authoritative, accessible, and regularly updated Backgrounders on hundreds of foreign policy topics.

Who Makes them?

The entire CFR editorial team, with regular reviews by fellows and subject matter experts.

As global trade has flourished in recent decades, so have trade disputes. Trading nations have created various forums to adjudicate conflicts, but they are increasingly the subject of controversy. U.S. President Donald J. Trump has long criticized trade dispute resolution panels as unfair and ineffective, particularly those the United States is party to via the North American Free Trade Agreement (NAFTA)—which has since been renegotiated as the U.S.-Mexico-Canada Agreement, or USMCA—and the World Trade Organization (WTO). While some critics say dispute panels undermine national sovereignty, proponents argue they offer much-needed protections that boost confidence in global investment and prevent trade wars.

Why did dispute panels emerge?

As cross-border trade and investment increased rapidly through the 1990s, individual states as well as public and private investors sought ways to adjudicate conflicts or alleged violations of trade agreements. Over time, the international trading system has developed a number of mechanisms to do this, depending on the type of dispute and the parties involved.

The authority of these supranational bodies is established by agreements such as bilateral investment treaties and free trade agreements, or by membership in an international organization such as the WTO. Parties agree to accept rulings, though enforcement authority and appeals processes vary.

What types of disputes do they handle?

These bodies broadly deal with two types of disputes: state-state, in which governments challenge the trade policies of other governments, and investor-state, in which individual investors file complaints against governments.

State-State. Most state-state disputes are handled by the WTO system, the primary body governing international trade. Each of its 164 members have agreed to rules about trade policy, such as limiting tariffs and restricting subsidies. A member can bring its case to the WTO if it believes another member is violating those rules. The United States, for instance, has repeatedly brought WTO cases against China over its support for various export industries, including one in early 2017 alleging that Beijing unfairly subsidizes aluminum producers. While that case has not been decided, the Trump administration has retaliated by unilaterally imposing targeted tariffs on some individual Chinese aluminum producers as well as broader tariffs on all steel and aluminum imports to the United States in order to protect against Chinese overproduction.

Investor-State. Known as investor-state dispute settlement (ISDS) cases, these disputes typically involve foreign businesses claiming that a host government abused them by expropriating their assets, discriminating against them, or otherwise treating them unfairly. For example, a Canadian gold mining company claimed that Venezuela’s nationalization of the gold industry in 2011 violated an investment treaty between the two countries. A tribunal found that while Venezuela had the legal right to nationalize private sector industries, it failed to properly compensate the company for the expropriated assets.

How does the WTO adjudicate cases?

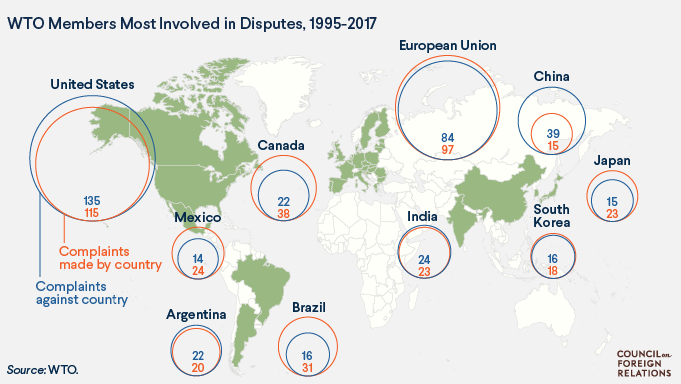

The WTO’s forum for arbitration is called the dispute settlement mechanism, which is run by a rotating staff of judges, as well as a permanent staff of lawyers and administrators. The WTO appoints a panel to hear a case if the opposing parties are unable to resolve the issue through negotiations. A panel’s rulings, if not overturned on appeal, are binding on the respondent country. If found guilty, it has the choice to cease the offending practice or provide compensation. If the country fails to respond, the plaintiff country can take tit-for-tat measures to offset any harm caused, such as by blocking imports or raising tariffs. Member states have filed nearly six hundred disputes since the WTO’s creation in 1995, but many of these cases have been settled prior to litigation.

However, the WTO process ground to a halt in December 2019, over a dispute about the appointment of new judges to the Appellate Body, which hears appeals to dispute settlement decisions. The United States, frustrated by Appellate Body decisions that it viewed as exceeding its mandate, has repeatedly vetoed all proposed new judges. The conflict began under the Barack Obama administration and intensified under Trump, and has now left the body without enough judges to hear appeals, which indefinitely delays any decision made by lower panels. CFR’s Jennifer Hillman, a former Appellate Body judge, says that a nonfunctioning Appellate Body could render the WTO dispute system powerless and threaten “to turn every future trade dispute into its own mini trade war.”

How are investor-state disputes handled?

A number of multilateral institutions adjudicate investor-state disputes, such as the Permanent Court of Arbitration in the Netherlands or the London Court of International Arbitration, but one of the most important is the International Center for Settlement of Investment Disputes (ICSID). Created in 1965 as part of the World Bank, the ICSID has 163 members, all of whom have agreed to recognize the legitimacy of its arbitration system.

Unlike the WTO, the ICSID has no permanent tribunals and does not directly rule on cases. Rather, it administers the process by which disputants choose an independent, ad hoc panel of arbitrators to hear their case. The arbitrators are generally legal experts, including professors, practicing lawyers, and former judges. The specifics on the sorts of conflicts that can be referred to an ICSID panel are set out in individual trade or investment agreements.

There are some 2,500 treaties with investment dispute provisions in force around the world, and the ISCID has administered more than six hundred disputes in its half-century existence. The number of cases accelerated through the 1990s and 2000s with the proliferation of investment agreements, reaching a peak of fifty-six in 2018. About a third of the cases are settled or withdrawn before concluding; a third are dismissed in favor of the defendant; and a third favor the investor in full or in part. An investor’s award generally holds the full force of domestic law in the country being sued.

What are the criticisms of the WTO’s system?

Most trade experts see the WTO’s arbitration forum as one of its most successful efforts, helping to institutionalize rules and reduce the threat of trade wars. However, critics, including the Trump administration, have criticized the WTO system on several grounds. U.S. Trade Representative (USTR) Robert Lighthizer has argued that the WTO has an anti-U.S. bias because over 150 complaints have been brought against the United States, more than any other country, and it has lost most of those cases.

Most trade experts see the WTO’s arbitration forum as one of its most successful efforts.

But many economists argue this is misguided, noting that complainant countries, including the United States, usually win cases they bring to the WTO because they tend to bring only the strongest cases. As former USTR Michael Froman points out, the United States under President Obama brought more cases to the WTO than any other country during that time, including sixteen against China. It has won all that have been decided.

Trump and Lighthizer have also said the WTO is incapable of policing China. The USTR’s 2017 report on China [PDF] asserted, for the first time, that Beijing’s state-led economic policy is so inimical to global free trade rules that it renders the WTO effectively irrelevant. “No amount of enforcement activities by other WTO members would be sufficient to remedy this type of behavior,” it states.

Other analysts argue that the WTO has been increasingly undermined by its most powerful members, including the United States. This is especially true of the battle over the Appellate Body. In December 2019, the body was reduced to one member out of seven, and was no longer able to form a quorum to hear cases.

What is the debate over investor-state dispute tribunals?

Investor-state dispute tribunals have become a flash point in the debates over multilateral trade deals such as NAFTA, the Trans-Pacific Partnership, and the proposed U.S.-Europe Transatlantic Trade and Investment Partnership.

Opponents say that these tribunals erode national sovereignty by allowing foreign corporations to bypass domestic legal systems. In 2017, a group of more than two hundred lawyers and economists warned that such provisions [PDF] give corporations “alarming power” to override domestic legislation, based on the secret deliberations of unaccountable tribunals that have no appeals process. Before the U.S.-Europe trade negotiations were put on hold in 2016, this worry was especially acute among the European public, which feared that ISDS would allow U.S. companies to challenge European Union (EU) rules on labor and environmental protections, food safety guidelines, and other public interest legislation.

The Trump administration, too, is skeptical of ISDS, which Lighthizer has called “offensive” for giving non-Americans a veto over U.S. law. In the course of NAFTA renegotiations, the Trump administration proposed eliminating the ISDS provision or making it “opt-in” rather than automatic, which was strenuously opposed by both Canada and Mexico. While the final agreement kept ISDS, its scope was sharply limited and Canada was excluded from the provision; Canadian businesses can’t use it to sue the U.S. and Mexican governments, and U.S. and Mexican businesses can’t sue Canada.

Supporters say these concerns are overblown, pointing out that the United States has never lost an ISDS case to a foreign investor and that investors tend to lose more cases than they win. Furthermore, they argue that ISDS protects foreign investments made by U.S. businesses and generally boosts cross-border investment.

What are the options for reforming these systems?

At the WTO, reform discussions have focused on process, as the numbers of disputes and appeals, as well as the complexity of cases, have increased in recent decades. Reform proposals include expanding the pool of experts on panels, digitizing paperwork, and other tactics to streamline operations. Some have suggested the WTO’s dispute body take decisions based on majority vote rather than consensus, as it does now, though such a move would likely be opposed by the United States and others. Currently, a single member can delay proceedings.

Controversy over ISDS has led governments around the world to experiment with other approaches to investor protection.

Meanwhile, the public controversy over ISDS has led governments around the world to experiment with other approaches to investor protection [PDF]. One option is to remove ISDS from some agreements altogether, as countries such as Australia have done, pushing businesses to first pursue challenges through the domestic legal system and then, if unsuccessful, allowing for state-state dispute settlement. The USMCA provides a stripped-down model: jurisdiction will be limited to narrower cases, investors will have to exhaust all local courts first, and all proceedings and documents will be public.

In another alternative, the EU is developing an investment court that will operate more like the WTO tribunal system, with a permanent roster of judges, strict conflict-of-interest rules, public proceedings, and an appeals process. The EU and Canada included a version of this in their 2016 trade agreement.

Are there other mechanisms to resolve disputes?

Individual trade deals have also created separate state-state arbitration mechanisms. This was the case with the Canada-U.S. Free Trade Agreement (CUSFTA), the precursor to NAFTA. CUSFTA’s Chapter 19, which was kept in the original NAFTA, allows for one government to challenge the trade policies of another via an independent, binational panel, which bypasses domestic court systems.

NAFTA’s Chapter 19 proved controversial. Canada insisted on its inclusion in CUSFTA because of what it saw as a long history of unfair U.S. trade policies. Ottawa has relied upon the chapter’s independent panels in dozens of cases, many relating to U.S. duties on Canadian lumber. Some trade experts argue that Chapter 19 reduced trade disputes between NAFTA members because it increased the chances that any trade barriers would be overturned by the panels.

While the Trump administration wanted to remove Chapter 19 from the new USMCA, experts warned that doing so could have led to an increase in duties, especially by a U.S. administration that has seemed eager to apply them, and an uptick in retaliatory trade measures from Canada and Mexico. The deal ultimately maintained the Chapter 19 mechanism; however, it must still win legislative approval to take effect.

Recommended Resources

This Congressional Research Service report details the history and process [PDF] of international investment agreements.

Trade expert Geoffrey Gertz lays out possible scenarios [PDF] for ISDS reform in a renegotiated NAFTA agreement in this analysis from the Brookings Institution.

Paul Ames explores the causes for ISDS skepticism in the European Union in Politico.

Several hundred trade lawyers and economists argue against ISDS [PDF] in NAFTA and the TPP in this open letter.

Lindsay Oldenski of the Peterson Institute for International Economics argues that investment agreements have been successful in boosting international investment.t

Colophon

Staff Writers

- James McBride

- Andrew Chatzky

Additional Reporting

Header image by Khaled Abdullah/Reuters.

Backgrounder

Backgrounder

Backgrounder

Backgrounder Backgrounder

Backgrounder