How Asia’s Life Insurers Could “Shelter-In-Place”

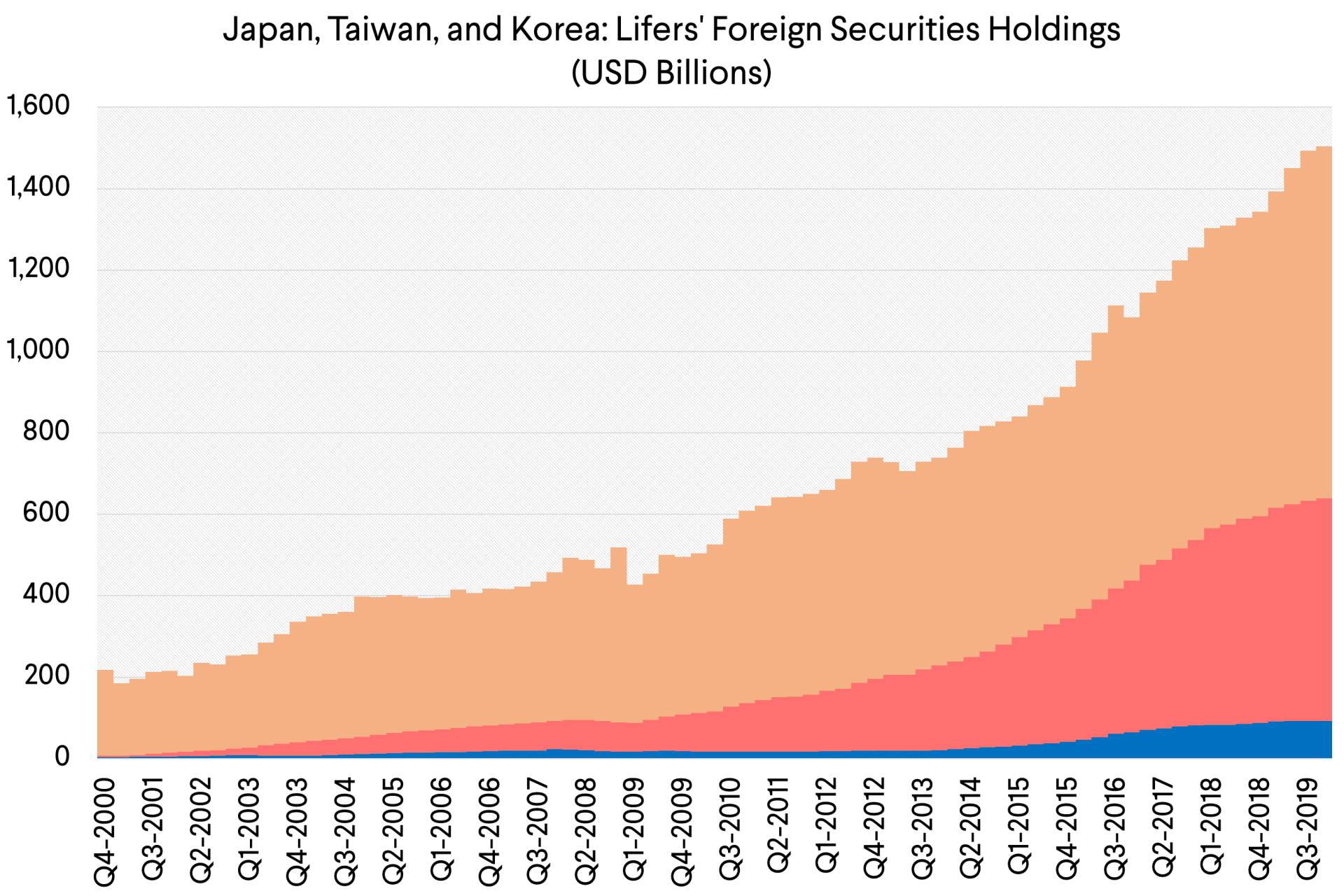

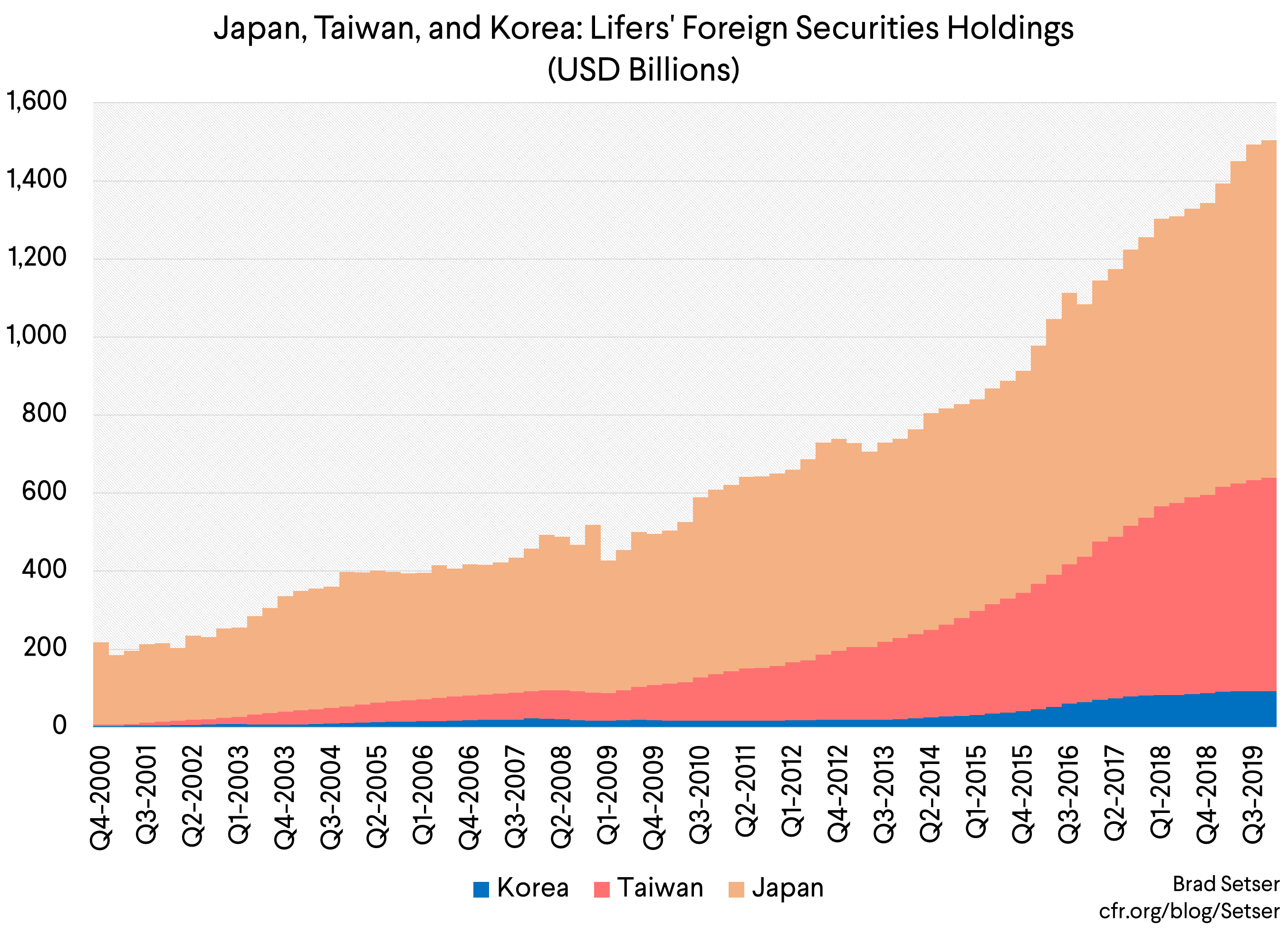

Asia’s life insurers likely hold somewhere between $1.5 trillion and $2 trillion of foreign currency denominated bonds as part of their portfolio—mostly dollar denominated, but some in euros. Japanese lifers report 10 trillion yen (~ $900b) in foreign securities (25 percent of their portfolio). Taiwan’s lifers, counting their holdings of ETFs that are listed in Taiwan but invest abroad, are heading toward $600 billion in foreign bonds (the latest data shows $555 billion in foreign securities holdings, and the insurers also have around $30b billion in indirect exposure through the bond ETFs; this is roughly 60 percent of their portfolio). Korea’s insurers have done something similar, but on a smaller scale. There was a reach for yield on a massive scale, as their “home” markets weren’t generating the returns they had promised savers.

This poses a problem right now—especially as a large portion of this book, over 60 percent, typically needs to be hedged against FX risk in the market (some is balanced by domestic foreign currency policies) more or less continuously.

But it is in my view a solvable problem.

There are at least three potential issues—

1) The insurers have traditionally needed to hedge (through foreign exchange or cross currency swaps, see this blog) a portion of this exposure with the banking system to limit their currency mismatch (having invested abroad, they are exposed should their “home” currency appreciate, reducing the value of their investments abroad). Those hedges are typically done on a short-term rolling basis, as the insurers assumed they could roll over maturing swaps every 3 months or so. Hedging long-term investments with short-term hedges was a central element of this strategy.

2) A portion of their investments are in corporate bonds—whether the traditional investment grade bonds Japanese insurers bought, or the more adventurous bonds (dollar callables, ultra-long dated bonds, dollar bonds issued by non-U.S. firms) that the Taiwanese favored. Many of these bonds have lost value recently (safer Treasury and Agency portfolios have held up better).

3) In some case, a portion of the portfolio has been farmed out to third party asset managers who themselves face constraints as they may use leverage and may have promised to stay currency hedged. Big sovereign pensions funds with an allocation to “credit” often have done the same.

The first two problems are solvable in my view, with cooperation between the “home” country central bank and the regulators. The key countries have either very ample reserves, or ample reserves and access to the Fed’s swaplines. In normal times, I believe in strong prudential regulation—and I have criticized the Taiwanese for letting their lifers run a bit wild. But in the face of a pandemic, it can make sense to loosen regulatory constraints—this is the time to make use of regulatory flexibility and existing buffers.

And similarly, in normal times, it is risky for the government to enable these trades by providing the insurers with low cost hedges (the newly disclosed $100 billion swap book of Taiwan’s central bank, the CBC, is a case in point). But in times of crisis, the direct provision of hedges to regulated insurers who are in a bit of a pickle is a sensible use of reserves—and I believe the Japanese should be considering ways to facilitate the provision of swap financing to their regulated insurers (whether directly, or through a dedicated window used by a bank intermediary that basically acts as a pass through).

The broad idea is the financial equivalent of sheltering-in-place—insurers have long-term liabilities, so they need not be forced sellers, or even forced hedgers. They can use their balance sheet to absorb short-run volatility—and if needed, they can draw on their capital (and potentially new capital from their home governments) to absorb losses, as their home governments effectively provide a form of portfolio insurance.

Let’s start with the currency hedging need.

The risk of an open position in this case comes when the “home” currency appreciates against the dollar. Japanese insurers would lose money if the yen went to 90 (a rise in the yen’s value vs. the dollar; it takes fewer yen to buy a dollar, and in this case, dollar assets are then worth fewer yen). Taiwanese insurers would feel a bit of pain the Taiwanese dollar appreciated through say 28 or 29…

So far the currency market moves haven’t hurt these portfolios, even the unhedged bits, as the dollar has generally strengthened (and the yen depreciated). And should market conditions change, in all probability the Japanese government and the Taiwanese government would act to limit a disorderly appreciation. Remember, there is no limit to how much you can intervene to block appreciation. So even an open position is ultimately a manageable short-term risk, so in my view existing open books don’t now suddenly need to be closed to “derisk.” (Trying to do so would generate demand for dollars to borrow, as closing the book in this case means borrowing a dollar and then selling the dollar to buy your home currency—e.g. reversing the currency leg of the initial use of your home currency to purchase foreign bonds.)

If firms are worried about this, their home governments can directly provide portfolio insurance against extremely large FX moves (guaranteeing that the insurers wouldn’t lose money from a move bigger than a certain defined amount) while regulators relax prudential regulations and allow the lifers to temporarily run bigger open positions.

Alternatively, the government can directly step in and provide the hedge.

One unexpected advantage of Taiwan’s decision to disclose that it already has a substantial swaps book is that it provides a model here—not a model of good behavior in normal times, but a model of the options available to those countries with substantial reserves and private sector dollar exposure in a crisis.

I don’t know if the lifers directly hedge with the CBC, or, more likely, do so through the banking systems (most of the lifers are part of bigger financial conglomerates).* In some sense it doesn’t matter—the CBC has long used a portion of its reserves to provide FX funding or hedging for the lifers (the CBC swaps FX for TWD, the lifers swap TWD for FX which they then invest abroad). And it can increase the provision of these hedges.

Absent disclosure, this would have meant reserves would “disappear” from the CBCs balance sheet.

But now that the CBC is disclosing its forward book, it could show both a fall in reported reserves, and increased provision of swap funding to local financial institutions. With over $450 billion in reported reserves and close to $600 billion in foreign currency assets the CBC isn’t financially constrained.**

Japan also has a substantial pool of dollar reserves—and the ability to borrow more from the Fed. Korea the same.

So between the regulatory forbearance for open positions, government insurance against losses from big FX moves and the direct provision of hedges, the underlying currency mismatch among the big Asian insurers can be addressed. And it can be done in ways that put minimal stress on bank balance sheets.

Alas, the currency mismatch is an easier problem to solve than the fall in the value of the corporate bonds that Asian insurers were increasingly buying (as hedging cost rose, the insurers reached for credit risk).

The lower market value of investment grade bonds may reflect an overshoot, as there have been a lot of forced sellers in the market. Or it may reflect a real shock that really has reduced the expected return over time on these bonds. It depends on the individual company.

But let’s assume there are real losses. And let’s further assume that some bonds will be downgraded and fall out of the subset of bonds that regulated insurers normally can buy.

Those real losses can be absorbed by the equity capital of the life insurers.

And if, over time, the losses exceed the insurers’ equity capital, the policy holders—who have been promised a fixed payoff over time—can be bailed out by a government capital injection. The long-term “home” currency liability structure of the lifers allows them to be patient (they need to rollover their hedges, but hold the long-term bonds against their long-term liabilities).

In normal times a regulator would worry if the insurer’s capital fell, and likely encourage the insurer to sell its riskier assets and/or raise capital (and regulators do need to worry about the possibility that undercapitalized insurers would gamble for redemption by taking big new risks once the situation stabilizes). But at a time when those who can shelter in place should, the regulators can simply allow the insurers to operate with less capital (or inject government capital if they want) while they hold on to their existing portfolio (This no doubt will require relaxing some regulatory restrictions as portfolio quality falls). That portfolio may well be a long-term problem. It doesn’t have to be a short-term problem. The regulators can take steps to make sure the insurers aren’t forced sellers.

Note here that Taiwan’s insurers are more thinly capitalized than the Japanese insurers, so Taiwan’s government may need to be thinking seriously about government equity injections relatively quickly (see the IMF’s Global Financial Stability Report).

Finally, a brief word on third party managers—in a sense, these pose the most difficulties, as they typically have to invest to achieve a certain mandate and thus don’t have the flexibility of in house portfolios. It may make sense though to bring some of those portfolios back in house (when possible), or to give the third party manager flexibility to essentially maintain a static portfolio even if it breaches some contractually agreed risk and volatility thresholds. One basic truism of a market is not everyone can sell at the same time.

My point is simple: think creatively of ways long-term money can ride out a crisis that by its nature will be relatively short-term. Some strategies that worked in normal times may not work now. And the kind of prudential regulation that is absolutely essential to build buffers in normal times now needs to be turned on its head. In good times, you build buffers. In the face of an unexpected shock, you draw down on those buffers.

Finally, I no doubt have gotten some things wrong here. This is offered in the spirit of putting forward ideas that help, even if they haven’t been fully stress-tested.

* Very, very roughly—and this is a way of simplifying things to make the math easy that intentionally is not precise—a quarter of the $600 billion foreign bond book of Taiwan is hedged vs. domestic foreign currency policies, a quarter isn’t hedged (this can vary a bit, a quarter may be high), a quarter is hedged at home (vis a vis the domestic financial system and the CBC), and a quarter is hedged through proxies and in the offshore NDF market). In my view, the CBC could easily provide another $150 billion in hedges out of its $450 billion in on balance sheet reserves ($300 billion would still be 50 percent of Taiwan’s GDP).

** There is a longer-term issue here as well. The lifers accounted for over three quarters of the net portfolio outflow that balanced Taiwan’s 10 percent of GDP current account surplus—so a likely slowdown in new foreign bond purchases would potentially generate pressure on the Taiwan dollar to rise. I thus expect the CBC to resume buying foreign exchange if global trade starts to normalize. Normally that would worry me—Taiwan’s dollar should be stronger in a normal world. But right now there are more important fights.