It Is Time for a Currency Manipulation Truce… Especially as Taiwan Disclosed Its True Foreign Exchange Position

There is no need for the Treasury to put out its foreign exchange report on time this April. There are other, more pressing priorities. And if it does, the Treasury should exercise its discretion to allow those countries that came close to meeting the definition of manipulation last year off the hook.

Let me start by noting that COVID-19 should change the global, not just the national, economic policy agenda. Cooperation is vital. And that means avoiding unnecessary fights.

That includes unnecessary fights over currency. Last year, I was pushing the U.S. Treasury to take currency intervention (and hidden intervention) by the smaller Asian economies more seriously.

But that is no longer a priority. Time to declare victory and go home, so to speak. The Treasury really shouldn’t be using its scarce resources to write a currency report for April.

Taiwan’s central bank (the Central Bank of the Republic of China, or the CBC) helped make this an easy call with a significant increase in its disclosure last week.

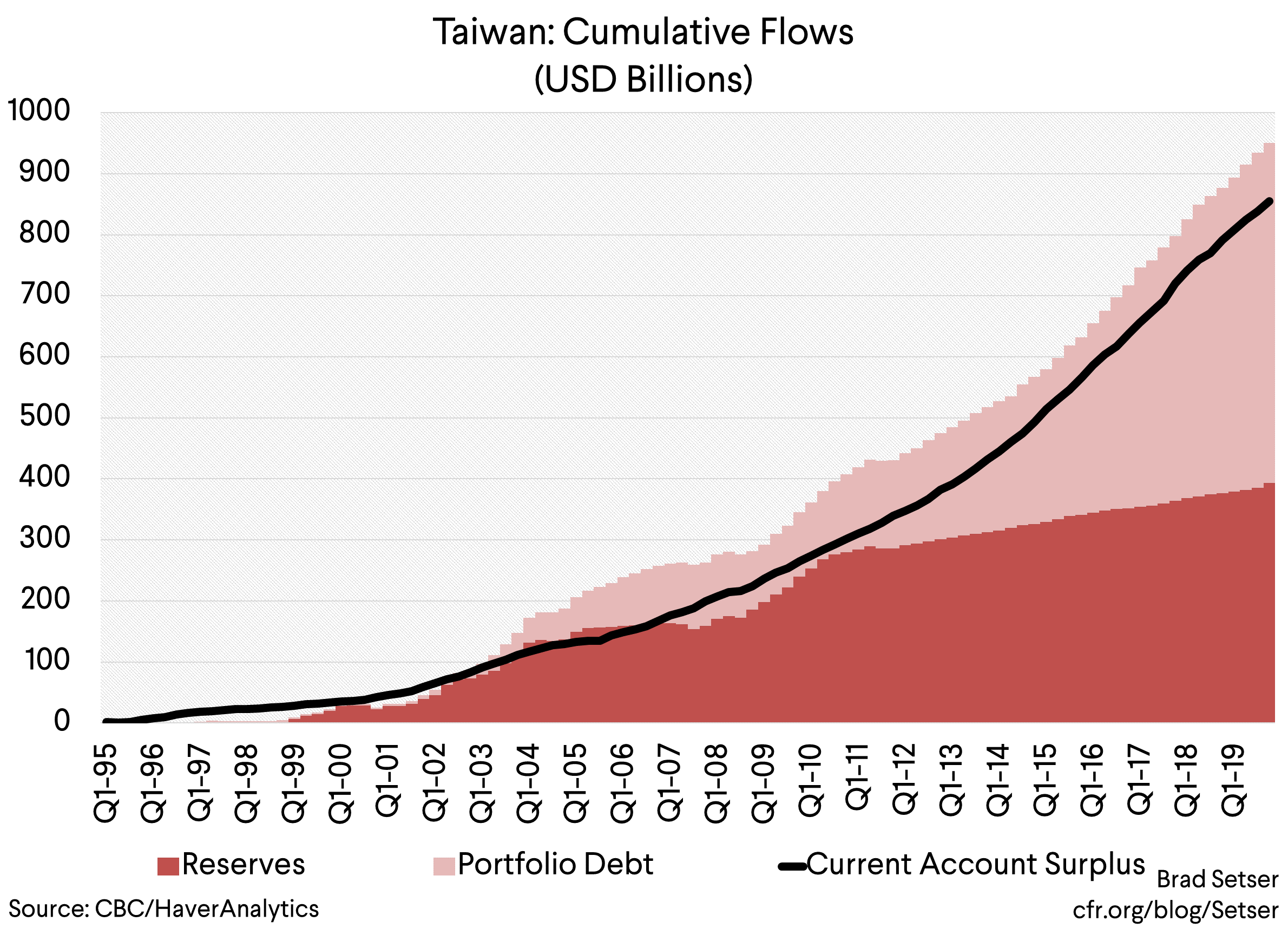

One that its true foreign exchange position is over $600 billion, as it has over $30 billion in domestic foreign currency bank deposits as well as almost $100 billion in foreign currency swaps with local financial institutions.

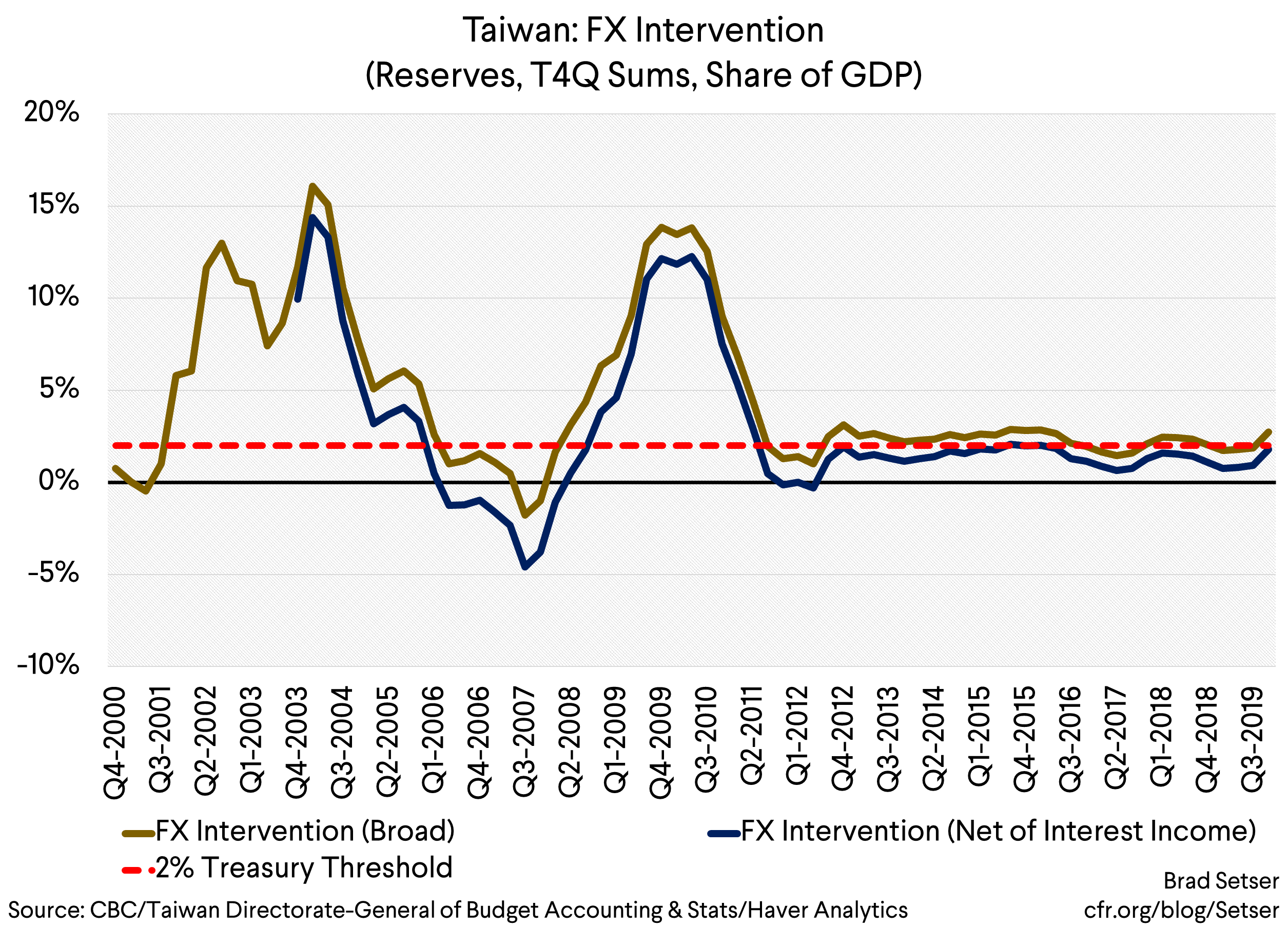

And two, that its actual intervention in the market in 2019 was $5.5 billion ($6.6 billion if you look just at the second half of 2019, as it reported that it sold in the first half of 2019). That’s around a percentage point of its GDP, below the Treasury threshold. Remember all those Taiwanese bond ETF purchases? That’s a probably big reason why the CBC didn’t have to intervene that much, as the lifers could buy ETFs (technically local currency products) unhedged (though the ETFs do now carry a higher capital charge).

To improve its credibility, the Central Bank of the Republic of China (CBC) should put out historical data on the evolution of its foreign exchange position. Obviously, it has intervened more heavily in the past that it has disclosed—and continue with its new transparency.

I though want to applaud Governor Yang Chin-long for taking this courageous step.

Obviously this is exactly what Concentrated Ambiguity and I publicly argued that Taiwan should do last fall. We argued that Taiwan had a large undisclosed foreign exchange position and we also more or less predicted its size (we didn’t consider the possibility that the CBC had undisclosed domestic foreign currency deposits in the domestic banking system though, our emphasis was on the swaps position). I am to be honest amazed—the math all checked out, but inferring the FX profit and loss from “other” items on a central bank’s balance sheet isn’t the way one usually estimates the size of a country’s foreign currency book. It certainly helped that the estimates inferred from the profit and loss statement mapped to the “hedging gap” on the lifer insurers books.

Taiwan’s disclosure also gives the Treasury an easy way to clear Taiwan of the charge of manipulation if they do write a foreign exchange report in April, as Taiwan’s disclosed intervention in 2019 fell under the Treasury’s 2 percent of GDP threshold.

That gets Taiwan off even though Taiwan’s current account surplus far exceeds the Treasury’s two percent of GDP threshold and its bilateral surplus with the United States now tops $20 billion (if Taiwan can ramp up its medical equipment production I would hope that surplus would grow…but that’s not at all bad). Total reserve growth incidentally was just under three percent of GDP—but a large share of that is from the interest income on its past intervention.

And yes, that intervention line looks suspiciously stable over the last ten years. That was one of the tip offs that the CBC wasn’t disclosing everything (until recently), as was the stability of the Taiwan dollar over an extended period of time.

There are two other countries that also come close to meeting all three criteria. Thailand and Vietnam.

A bit of background. The foreign exchange report is backward looking. The semi-mechanical assessment process set out in the 2015 Trade Enforcement Act is based on what happened in the previous year (in April) or the previous four quarters (in October). And, more importantly, the Treasury has a bit of discretion under the 2015 law. That discretion is both of the sneaky, technical kind, and of the more formal—there are exit ramps that allow the Treasury to avoid calling for enhanced dialogue—(the term the 2015 law uses for “manipulation”) even if a country meets all three of the criteria that the Treasury has laid out (the process of enhanced dialogue can be waived if it “i) would have an adverse impact on the United States economy greater than the benefits of such action; or (ii) would cause serious harm to the national security of the United States.”)

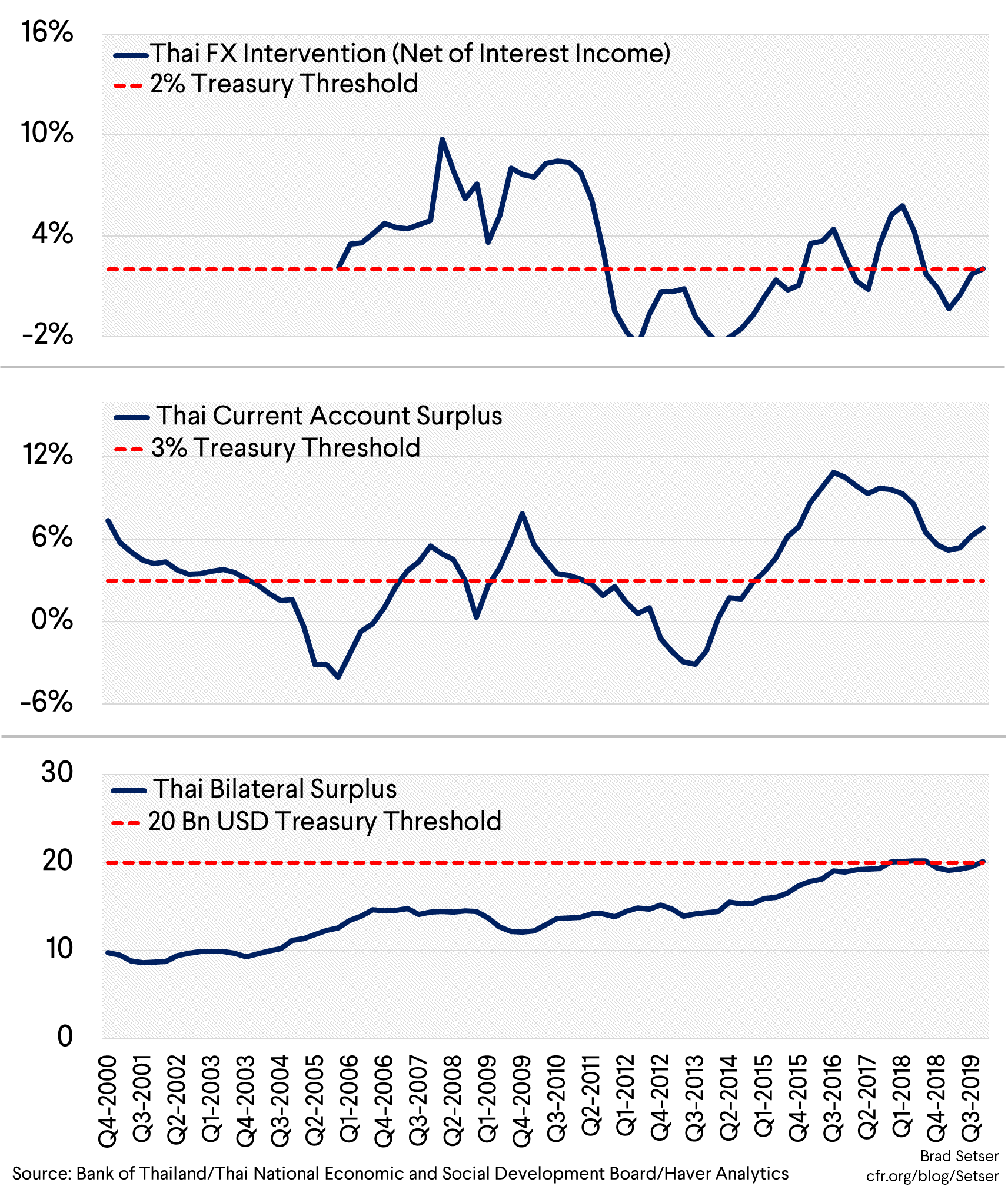

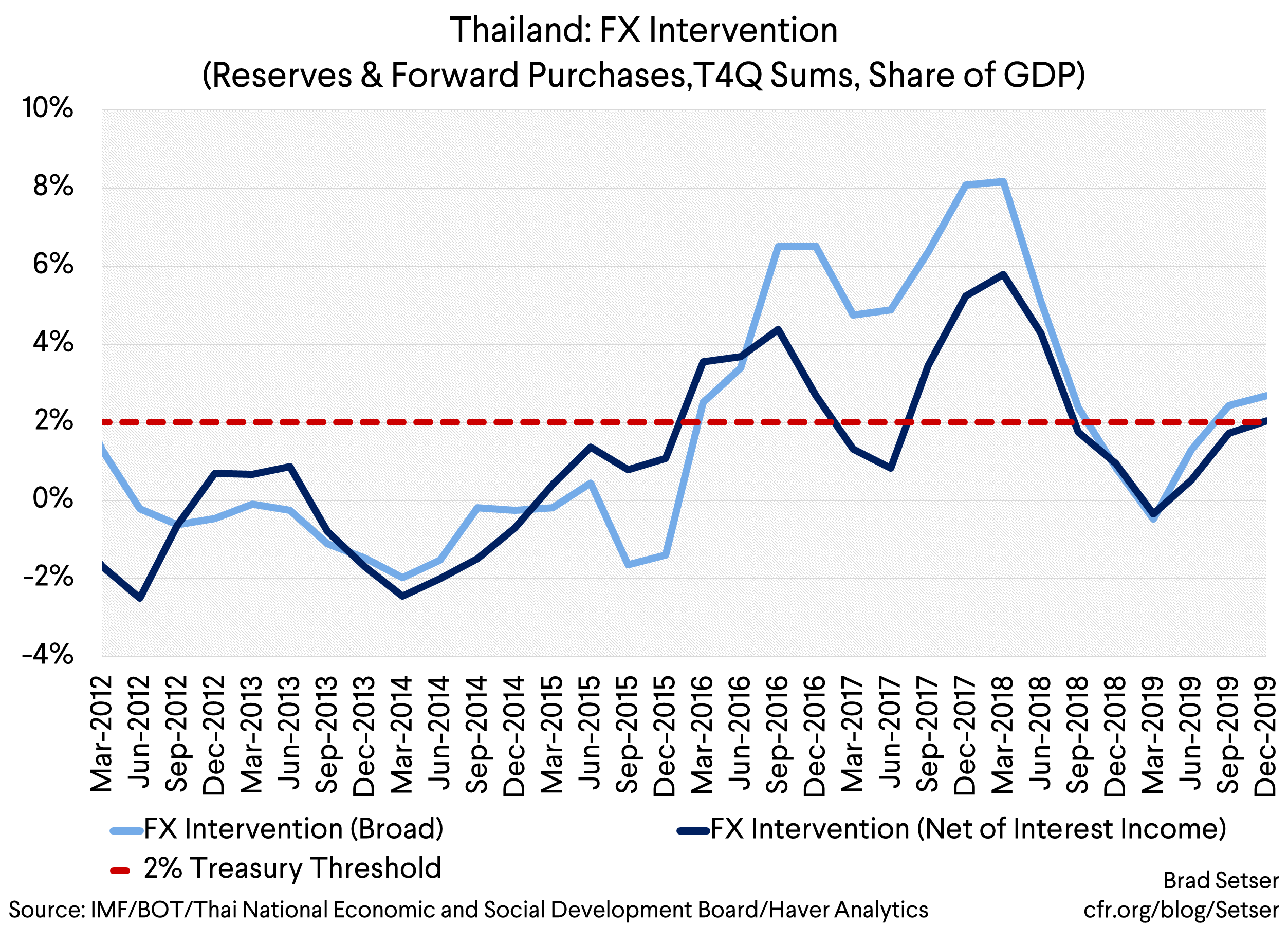

Thailand, like Taiwan, clearly meets two of the three criteria that the Treasury now uses to assess countries for violations of the 2015 act. Thailand’s 2019 current account surplus was close to 7 percent of its GDP. Its bilateral surplus with the U.S. inched over $20 billion (the bilateral balance isn’t my favorite indicator, but in this case it reflects a broader surplus). And Bank of Thailand was active in the foreign exchange market over the course of 2019, and clearly intervened heavily over the turn of the year. In fact, the governor of the Bank of Thailand more or less said that Thailand wants to keep the baht weaker than 30 to help Thailand’s exporters, and called for more domestic foreign currency deposits and more foreign investment by Thailand’s lifers so the central bank could intervene less.

But Thailand’s reserve growth, plus the change in its forward position, looks to be about 2.6 percent of its GDP, just over the Treasury’s 2 percent threshold. But the Treasury excludes interest income from its calculation—and that makes it close. But an average return of over 1.5 percent on its reserves would mean that Thailand’s market purchases were under 2 percent of GDP.

If Thailand has a roughly normal share of euros and yen in its reserves, I get “true” (that is, interest adjusted) purchases of around 2.1 percent of Thai GDP. But it is a close call (especially as some of Thailand’s heavy late 2019 intervention showed up in the data in the first week of January). If Thailand’s reserves were all in dollars and it got the average return of an international holder of Treasuries on its reserves, its “actual” intervention would fall just under 2 percent of GDP.

And in these times, Thailand deserves the benefit of doubt. Thailand depends heavily on tourism exports and the Thai baht if anything is now under pressure to depreciate. This isn’t the right moment to make Thailand into an example…

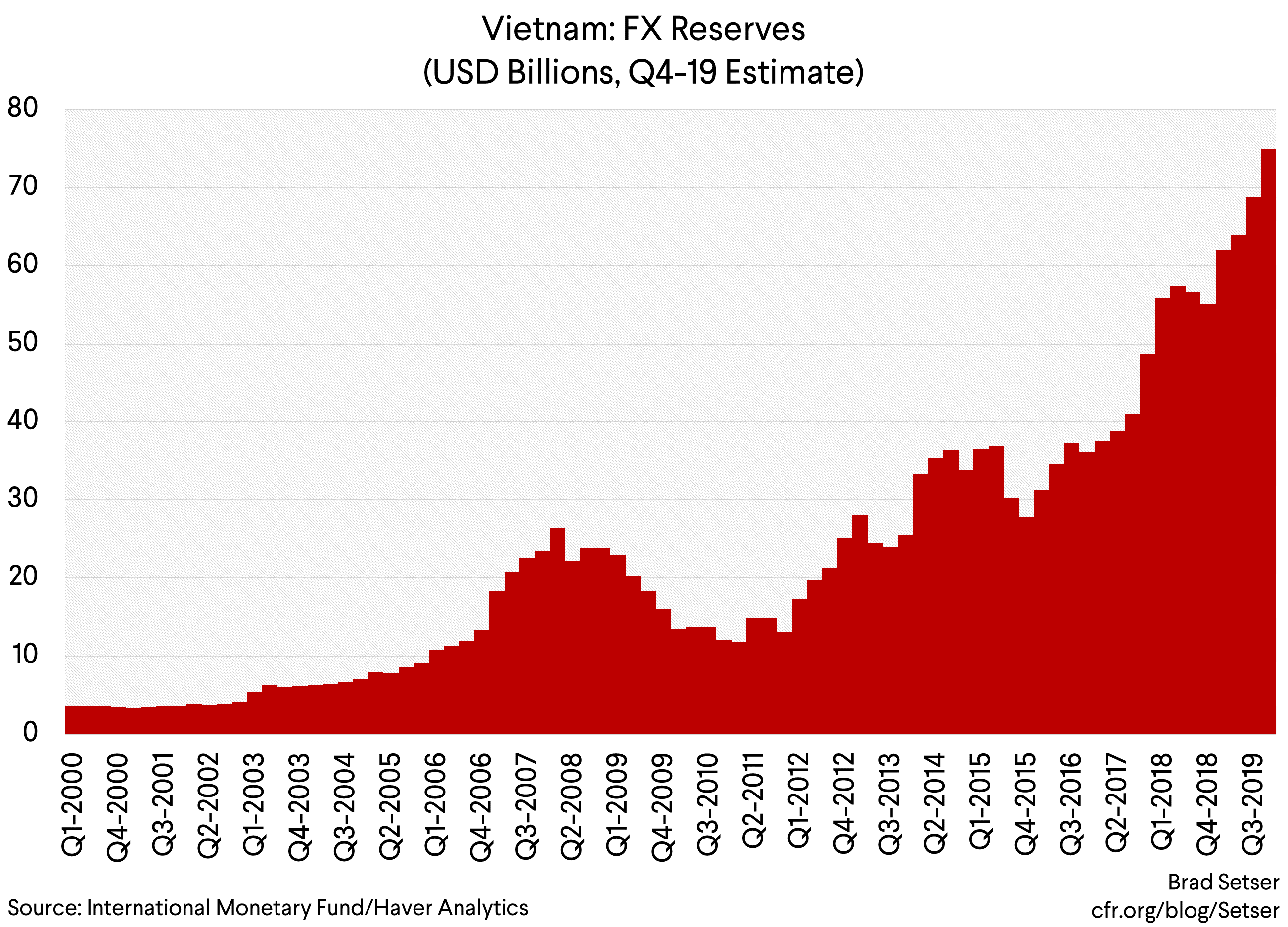

With Vietnam there is no doubt that its intervention far exceeded the two percent of GDP threshold. Vietnam’s reserves soared over the course of 2019—rising by over $18 billion through November (roughly 7 percent of GDP) , with purchases of $20 billion if the central bank’s December intervention is included. Vietnam’s bilateral surplus with the U.S. is now huge—so it easily crosses that threshold.

In the middle of 2019, Vietnam’s current account surplus dipped under 2 percent of GDP, which is one reason why it wasn’t covered in the Treasury’s foreign currency report. But over the second half of 2019 it looks like Vietnam’s surplus rose back over 3 percent of GDP. There isn’t current account data for q4 yet, so this is based in part on the trade data.

Yet at a time when some flexibility is called for, the Treasury has two options:

1) It could argue, as it did in the fall, that Vietnam’s reserves are relatively modest (something the IMF noted in the summer of 2019)—and thus let Vietnam off in 2019 on the grounds that it still needs more reserves. In normal times, I might quibble with this—Vietnam’s reserves now aren’t objectively small relative to the size of its economy, I am not a fan of the IMF’s reserve metric and the IMF’s assessment is at this stage stale given the size of Vietnam’s purchases late last year. But these aren’t normal times.

Or

2) the Treasury also could exercise the “not in the interest of the U.S. clause” to avoid a formal designation even if it concludes that Vietnam otherwise meets all three criteria.

Bottom line: I have long argued that the United States needs to take currency manipulation (and other domestic policies that lead to large current account surpluses) by countries other than China more seriously. But Taiwan made a good faith effort to avoid a designation—and it should be rewarded. The other two cases aren’t at all clean cases. And this is clearly a time for comity and cooperation not currency wars.