All Sound and No Fury? Will The Trump Administration Get Tough on Currency in April?

A number of Asian countries could be designated as manipulators in the U.S. Treasury’s April foreign exchange report. And unlike the politically motivated designation of China last summer, there would be a clear analytical justification for a new round of designations.

President Trump came into office talking a big game on “currency.” China was going to be named a manipulator on day one (never mind that it was selling dollars to prop up its currency at the time). American allies would no longer get a free pass to take advantage of America economically—an argument that, at least in principle, should have put on notice those countries using government policy to keep their exchange rate undervalued to support their exports.

Yet Trump hasn’t actually been a big innovator on currency policy. The big changes have come elsewhere (a “shopping list” trade policy toward China for example).

Yes, the Trump Administration designated China a manipulator (almost by tweet, though not technically—it was done in a press release dictated by the President). But it then un-designated China without any substantive change in China’s currency regime, or any material change in China’s foreign exchange disclosure. And yes, the new NAFTA does include a substantive requirement that the parties disclose their intervention “inside” the actual agreement, which is new.* But the NAFTA countries were already disclosing their intervention, so this wasn’t a heavy lift.

In the cases where disclosure could actually matter, Trump’s Treasury has—to date—settled for very little. Korea’s new disclosure of intervention uses such a whacky definition of intervention that the Treasury literally decided not to use it in the last foreign exchange report (see footnote 14 in the foreign exchange report). Fortunately Korea does put out monthly balance of payments data and discloses its forward book monthly, so there is—broadly speaking—sufficient information available to form a judgement about Korea’s policies without relying on its more or less useless new disclosure. And in the currency chapter of the phase 1 deal, China didn’t commit to anything new. The transparency requirement required nothing more than a commitment by China to continue to disclose its reserves monthly using the IMF’s standard reporting template and release totally standard balance of payments data quarterly.**

The January version of the foreign exchange report did make it clear that the United States would look unfavorably upon a further depreciation of China’s currency, though it isn’t clear precisely what the United States would do—beyond putting China back on the manipulator list—if the yuan started to slide. The United States always could seek countervailing tariffs against the depreciation, but that would blow up the “Phase one” deal. Realistically, the agreement seems to do little more than codify the status quo.

But it increasingly looks like Trump will have one more chance to make a splash with the foreign exchange report (with a little help from Senator Bennet and the Obama Administration, which thrashed out the Bennet Amendment to the Trade Enforcement Act back in 2015).

A number of countries are at real risk of being designated in April, and thus the Treasury will have a chance to put the Bennet process to a test...***

Obviously we don’t know exactly what will be in the April report, as the data needed to do the full formal assessment isn’t yet out. Several key bits of the information the Treasury uses in its assessment (end year current account numbers for example) won’t be available for all countries until the end of March.

But there is enough information already out to know that a number of countries—Taiwan, Thailand and Vietnam in particular—are at risk of being designated as manipulators (under the 2015 Trade Enforcement Act). Switzerland also will be a close call, though I suspect its intervention in 2019 will not meet the “sustained” criteria as it was concentrated in July and August.****

The increase in the number of countries at risk of a mechanical designation is for two broad reasons.

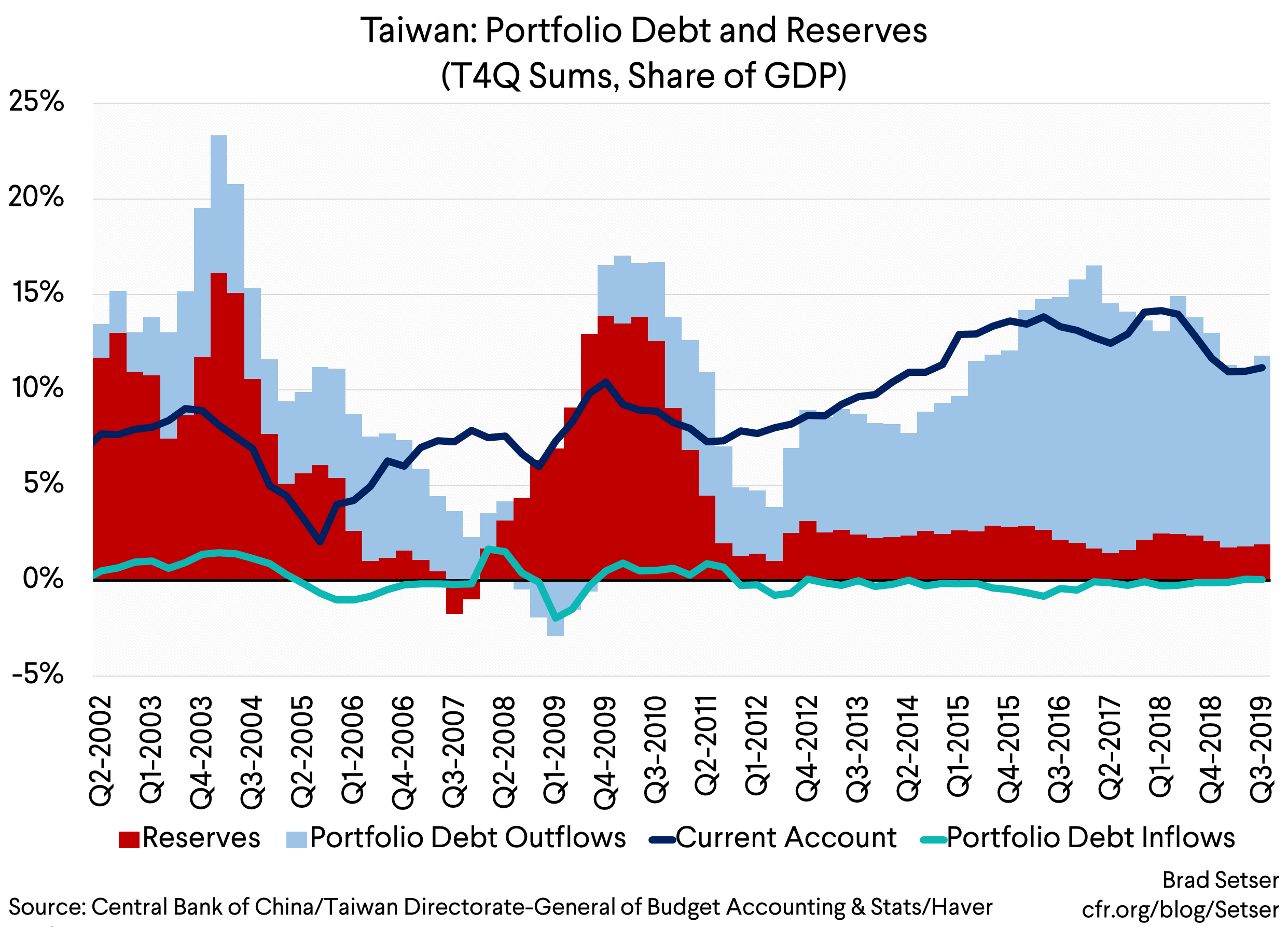

First, the tariffs have shifted the U.S. bilateral trade deficit away from China toward some other Asian countries. That means that a number of countries that previously got off because they didn’t run a large bilateral surplus with the United States are now at risk of a mechanical designation under the three criteria set out by the Treasury to meet the demands of the Bennet amendment. This matters for Thailand and Taiwan in particular.

I would be the first to acknowledge that the $20 billion threshold for a “troubling” bilateral surplus with the U.S. is entirely arbitrary—hell, I have argued that the Treasury should dump the bilateral surplus criteria entirely and focus on a country’s overall surplus. But over the course of the second half of 2019 Taiwan’s bilateral surplus decisively crossed the $20 billion mark and Thailand’s surplus just inched over $20 billion in November.

In a strange way, China’s enormous bilateral surplus with the United States used to help keep a lot of other Asian countries out of trouble so long as the Treasury stuck to the three Bennet criteria. China had a huge bilateral surplus with the United States, but an overall surplus that wasn’t huge (relative to the size of its economy) so it escaped mechanical designation. And many of the Asian countries with large overall surpluses didn’t have large bilateral surpluses with the United States (they were shipping parts to China for final assembly) so they also avoided a mechanical designation.

But that’s no longer necessarily the case.

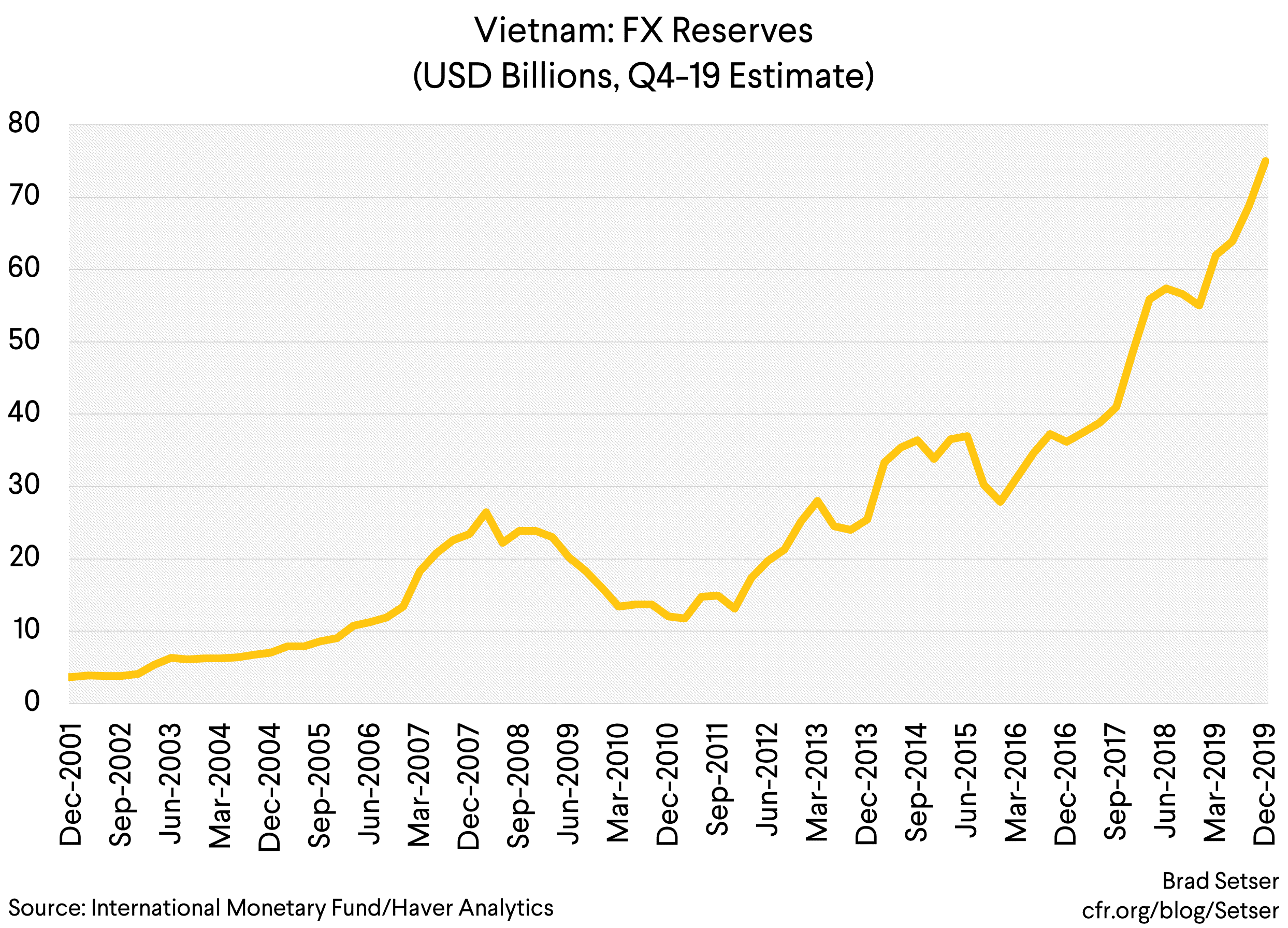

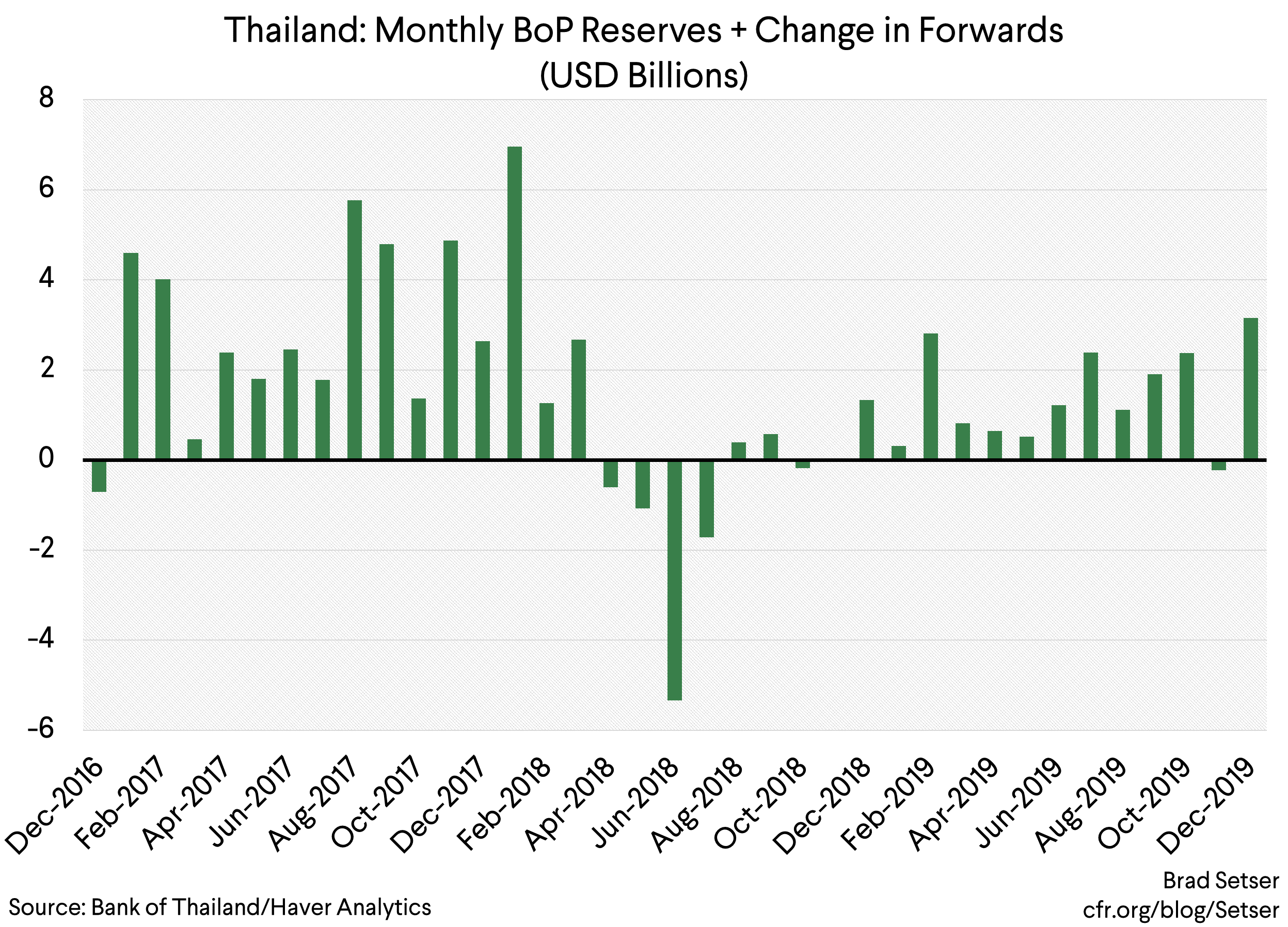

Second, a lot of Asian central banks have been intervening pretty heavily this fall. Progress toward a “phase 1” deal helped stabilize the yuan, and without the downdraft from a weaker yuan pulling all emerging Asian currencies down, a number of the smaller Asian countries have come under market pressure to appreciate. Thailand obviously has been intervening recently for example—its central bank has said as much. Vietnam also has been adding quite significantly to its reserves on the back of heavy State Bank of Vietnam intervention. And Taiwan has clearly been intervening to block the Taiwan dollar from appreciating through 30, at least until this week…

So if the Treasury goes strictly by the three criteria set out in the Bennet amendment to the 2015 trade enforcement act, several countries could be designated for manipulation. For real so to speak—as their designation would be grounded in a clear process, not a presidential whim.

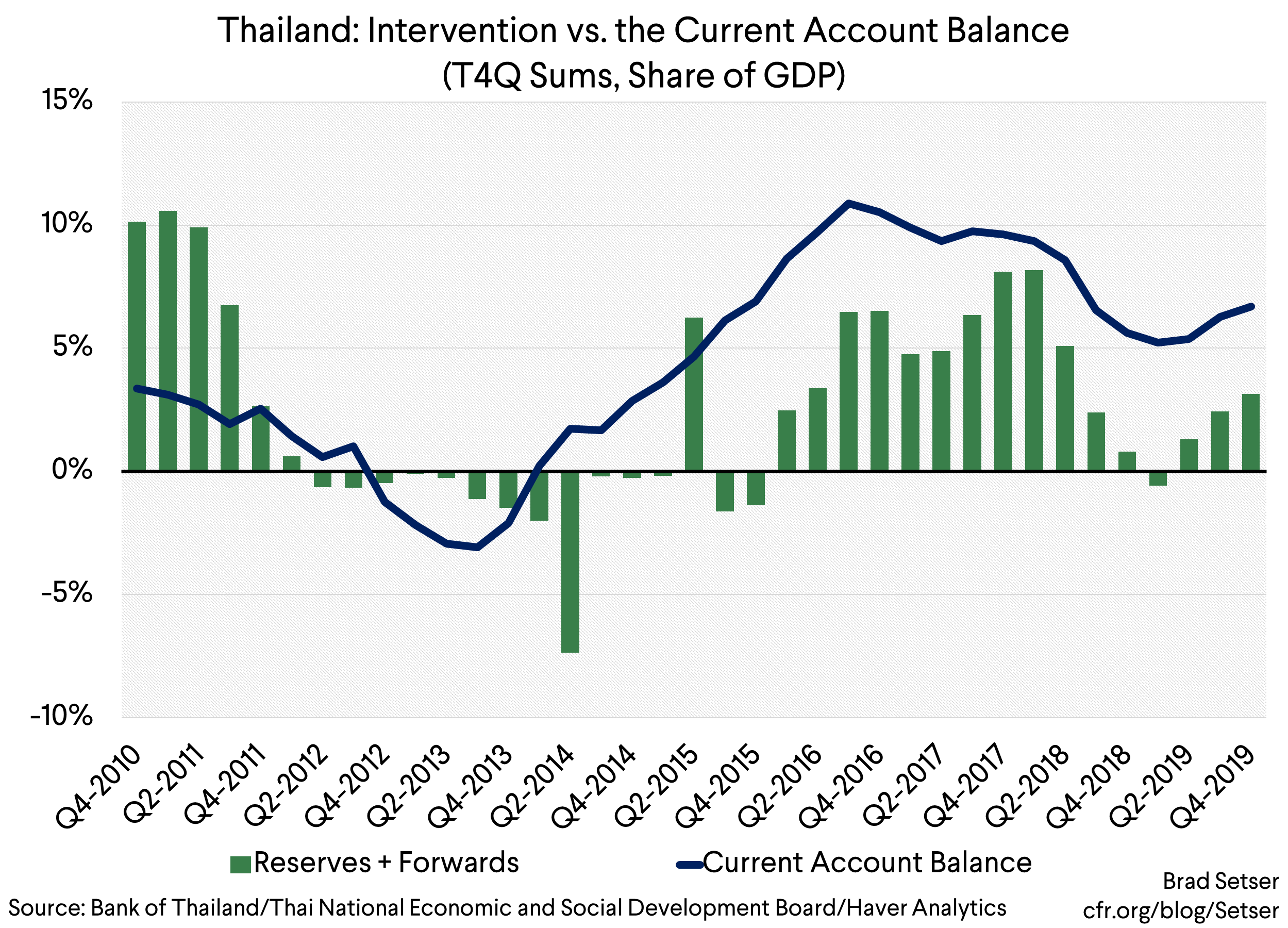

Thailand has a current account surplus well in excess of the Treasury’s threshold, and by my calculations, it has intervened enough to cross the Treasury’s trip wire on that criteria too. Total reserve growth for the year should be just over 3 percent of GDP. The Treasury will net out estimated interest income, but if my math is right, that isn’t likely to be enough to get Thailand’s estimated intervention down under 2 percent of its GDP. Thailand’s bilateral surplus with the United States topped $20 billion in the twelve months to November. If that continues in December, Thailand will, I think, meet all three criteria.

Now Thailand will just barely meet two of the criteria. So it will be a close call. But in my view it is likely to get an almost mechanical designation. The Thai central bank is consequently in a bit of a bind—though only a bit, as it really should accept more baht strength, difficult as that may be. For now though, it is doing everything it can to resist appreciation—and adopting some of the tricks others in Asia have used in the past to try to reduce the amount of intervention associated with its targeted exchange rate.

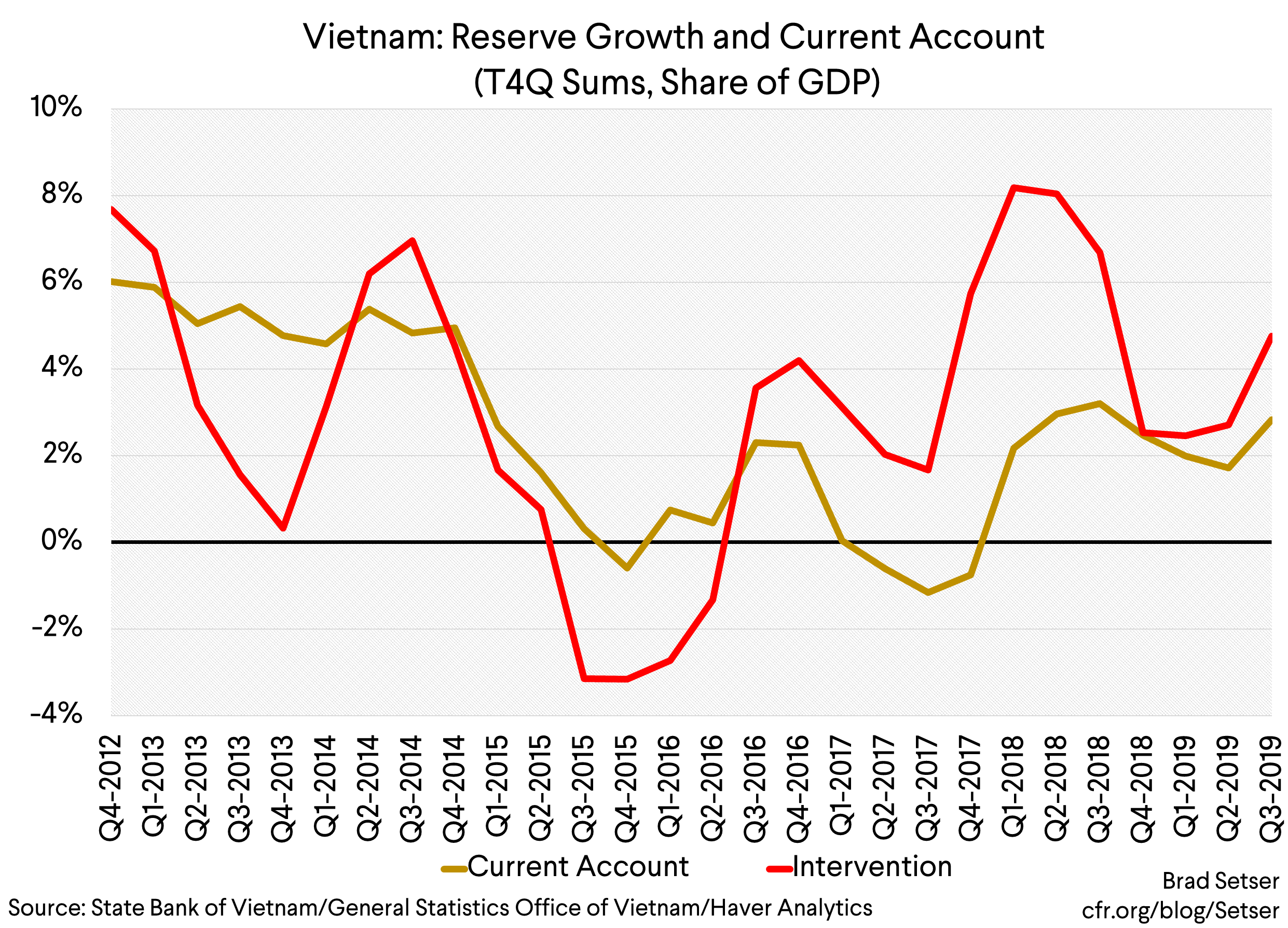

Vietnam is in a similar position as Thailand—as it is right on the cusp of crossing all three of the criteria the Treasury looks at. Its bilateral surplus clearly exceeds the Treasury’s $20 billion threshold, and its intervention also clearly has topped 2 percent of its GDP (the SBV has reported $16 billion in purchases, and that’s likely not the full year total). Everything comes down to whether or not Vietnam’s q4 current account surplus will put its full year surplus over the 2 percent of GDP threshold (it dipped up 2 percent in the first half of 2019, but rose back over the threshold in q3).

The most interesting case, though, is Taiwan.

It easily meets the current account surplus criteria. Its exports to the United States are booming, so it also now easily meets the $20 billion bilateral surplus criteria as well (though there is talk of Taiwan making “Trumpian” style purchases of U.S. oil and the like to try to bring its bilateral surplus down). And there is no real doubt that it has been intervening rather heavily in the foreign exchange market.

That’s what Bloomberg has reported.

That’s more or less what Taiwan’s central bank governor has said.

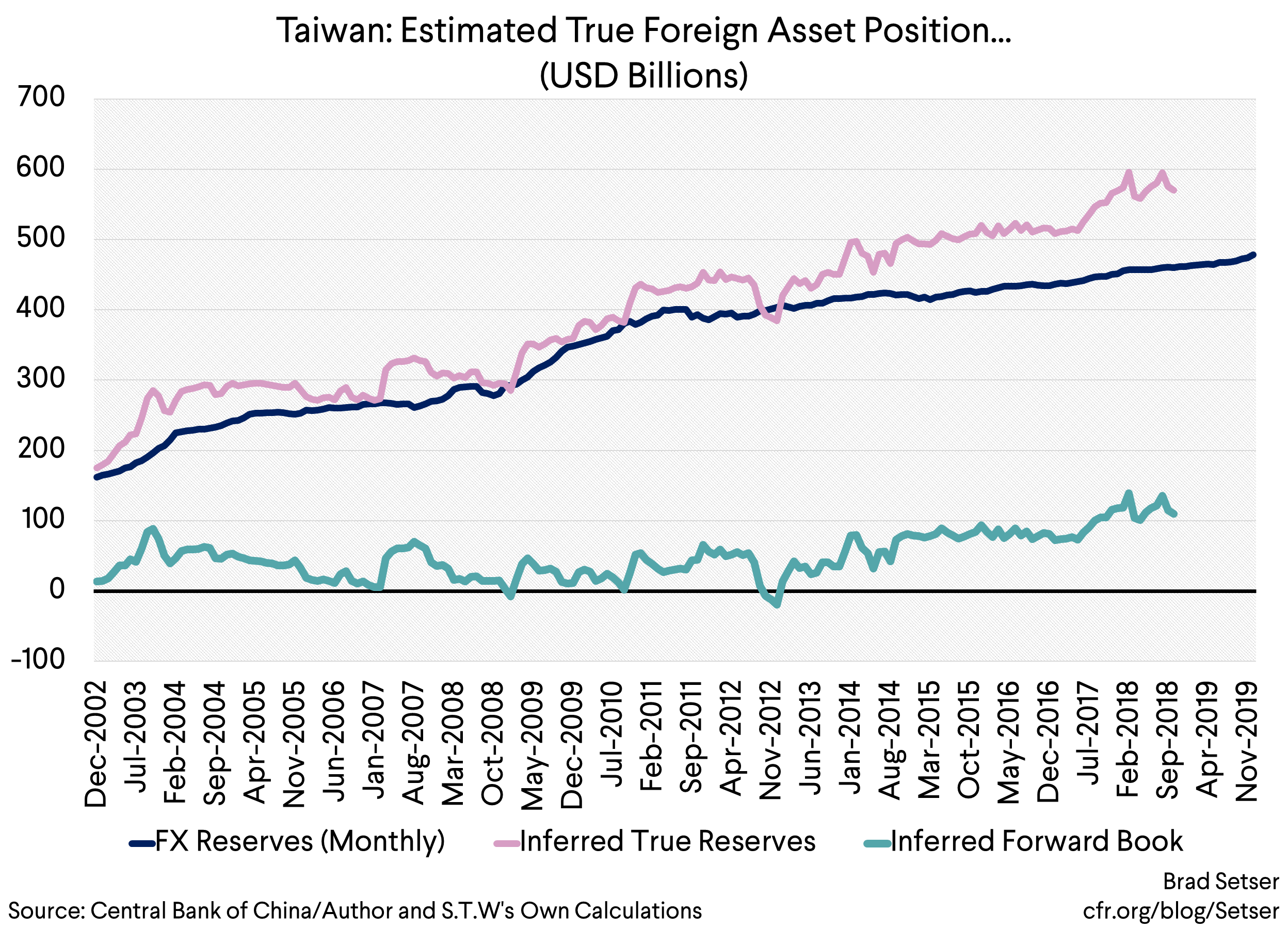

And it’s pretty clear if you look at a chart of the Taiwan dollar—the central bank was buying U.S. dollars (selling Taiwan dollar) to keep the Taiwan dollar from appreciating through 30.5 in November, and then buying U.S. dollars to keep the Taiwan dollar from appreciating through 30 in late December. Purchases were often concentrated at the end of the day for maximum impact (Bloomberg again)

But if the Treasury chooses to rely on Taiwan’s reported reserve growth, it would escape designation—as headline reserves have increased by a sum that, after taking into account the interest income on Taiwan’s large reserves, won’t trigger designation.

However, this would be bit of a cop out on the Treasury’s part. Taiwan doesn’t actually report enough information to allow an accurate calculation of its actual intervention. It has never disclosed the central bank’s forward position.

Concentrated Ambiguity and I have laid out at length why there is good reason to think that Taiwan’s forward book is big, and thus good reason to think that Taiwan’s intervention in the market exceeds the modest amount that can be inferred from the growth in Taiwan’s headline reserves.

The Central Bank of China recently denied that it was intervening in the currency market through foreign currency swaps. But that actually wasn’t our argument—our argument was that the Central Bank of China intervenes in the spot market, and then conducts foreign currency swaps to “sterilize” its intervention (a standard procedure). Normally this kind of intervention would show up as a rise in the central banks forward book (as the swap moves the foreign exchange off the central bank’s reported balance sheet into an “off balance sheet” account). But since Taiwan doesn’t disclose its forward book, the swap effectively makes Taiwan’s intervention disappear from its reported reserves.

So the Treasury doesn’t really have enough information to conclude that Taiwan isn’t intervening in excess of the 2 percent of GDP threshold …

To me the solution here is obvious. The United States either designates Taiwan under the 1998 act—as Taiwan clearly has intervened to impede balance of payments adjustment (one of the 1988 act criteria) even if we don’t know the size of Taiwan’s intervention. Or the United States refuses to clear Taiwan under the 2015 criteria absent additional information, and enters into negotiations with Taiwan to secure commitments from Taiwan to limit the Central Bank of China’s future intervention and to strengthen its foreign exchange disclosure.

What the U.S. Treasury shouldn’t do is just issue a report saying that Taiwan only meets two of the three criteria and then move on. If it wants to give Taiwan a political pass, it should do so explicitly (there are provisions in both the 1988 and 2015 law that provide flexibility).

* The TPP’s currency provisions were in a side agreement, not in the agreement itself. And to be fair, the disclosure requirement for intervention in the new NAFTA is stronger than the disclosure expectation in the TPP side agreement. Then again, the TPP standard was incredibly low, at the insistence of Singapore and Malaysia (intervention over a 6 month period would be disclosed with a 6 month lag, when best practice is disclosure of purchases and sales by currency monthly, with a month lag)

** Those who understand the balance of payments immediately understood how little China was committing to disclose—goods and services exports and imports, and the three most basic and standard line items in the financial account. Everyone apart from a few small African countries and a few oil exporters in the Gulf now discloses this information (it is the IMF’s standard balance of payments breakdown in BPM 6). Putting such basic disclosure into a formal agreement is almost insulting.

*** The Bennet thresholds, as identified by the Treasury, are a current account surplus of over 2 percent of GDP, a bilateral surplus with the United States of over $20 billion, and intervention of over 2 percent of GDP (with sustained intervention defined as intervention in 8 of the last 12 months). I have advocated dropping the bilateral surplus criteria, as it is analytically meaningless—Singapore automatically gets off even though it obviously has been intervening heavily for years, and, well it doesn’t really matter whether Thailand’s bilateral surplus is $19.9 or $20.1 billion. See my policy innovation memorandum, now available as a PDF. The Bennet sanction is in the first instance a year of dialogue, and then some very modest penalties.

**** Switzerland is fairly transparent about its intervention and the size of its reserves—so there isn’t much doubt. But with reserves equal to 100 percent of Swiss GDP, the exact split between interest and dividend earnings and outright purchases is hard to estimate, and the Swiss don’t technically disclose actual purchases. The Swiss bilateral surplus with the United States is now over 26 billion, so the Swiss are in line for a designation as well. And well, the negotiations with the Swiss that are required as a result of the law would be sort of fun—even if the actual sanctions specified in the Bennet amendment aren’t really designed for an economy like Switzerland. Analytically, though, I find it hard to justify designating the Swiss but not Singapore (both intervene heavily, and have current account surpluses inflated as a result of the, ummm, tax services they provide large multinationals). Singapore has a much weaker currency, way more foreign assets, and recently has been intervening more heavily.