Not One Emerging Market Financial Crisis, but Many…

The common denominator across many emerging economies is a shortage of dollars. But the causes differ, as do the solutions.

The global economy has been hit with a nearly unprecedented set of shocks.

An oil price shock that has sent the price of Brent oil down to under $25, and pushed the prices of many other grades of crude even lower. That is below the balance of payments breakeven of almost all oil exporting economies, below the production (full cycle) breakeven of a lot of global output, and even below the “lift” (marginal) cost of a lot of producers. Many other commodity prices are also at multiyear lows: copper, for example.

A shock to manufacturing trade—tied to the shutdowns needed to slow the spread of the coronavirus in the absence of a vaccine or effective therapeutic—that far exceeds the (comparably modest) disruption to manufacturing trade associated with Trump’s trade war.

A sudden stop in private market flows to many emerging economies, as investors seek safety.

A reduction in the availability of cross-border dollar financing to credit worthy borrowers around the world as the banks with direct access to the Fed (and the ECB) face unprecedented demands on their balance sheets. Global finance is now quickly being re-intermediated through banks, as they offer a form of stability that the “shadow” (non-bank) financial system cannot replicate in a crisis.

These shocks can have offsetting impacts. A country that imports oil, for example, Turkey, will benefit from lower energy prices. But its manufactured exports will be hurt by Europe’s shutdown, and it will lose the income provided by summer tourism. And its banks of course will be hurt by any reduction in the availability of cross border finance, as Turkey’s banks (still) have a lot of syndicated loans that they need to roll over.

These shocks will touch almost all emerging economies.

But the impact of these shocks will differ radically, as will the needed global policy response.

Some countries have relatively strong balance sheets and are thus fairly well equipped to handle these shocks on their own.

Take, for example, oil exporters with large accumulated stocks of reserves. They will need to—and can—draw on those reserves (and the assets in their sovereign wealth funds) to cover the shortfall in export revenue created by the current plunge in oil prices. The weaker oil exporters have to adjust immediately, but the stronger oil exporters can in effect self-finance to avoid immediate adjustment. The Saudis have around $500 billion in reserves, and the Russians a comparable sum and the added advantage of a floating currency. The smaller GCC countries collectively have more than $1 trillion in their sovereign wealth funds. Those buffers can and should be used.

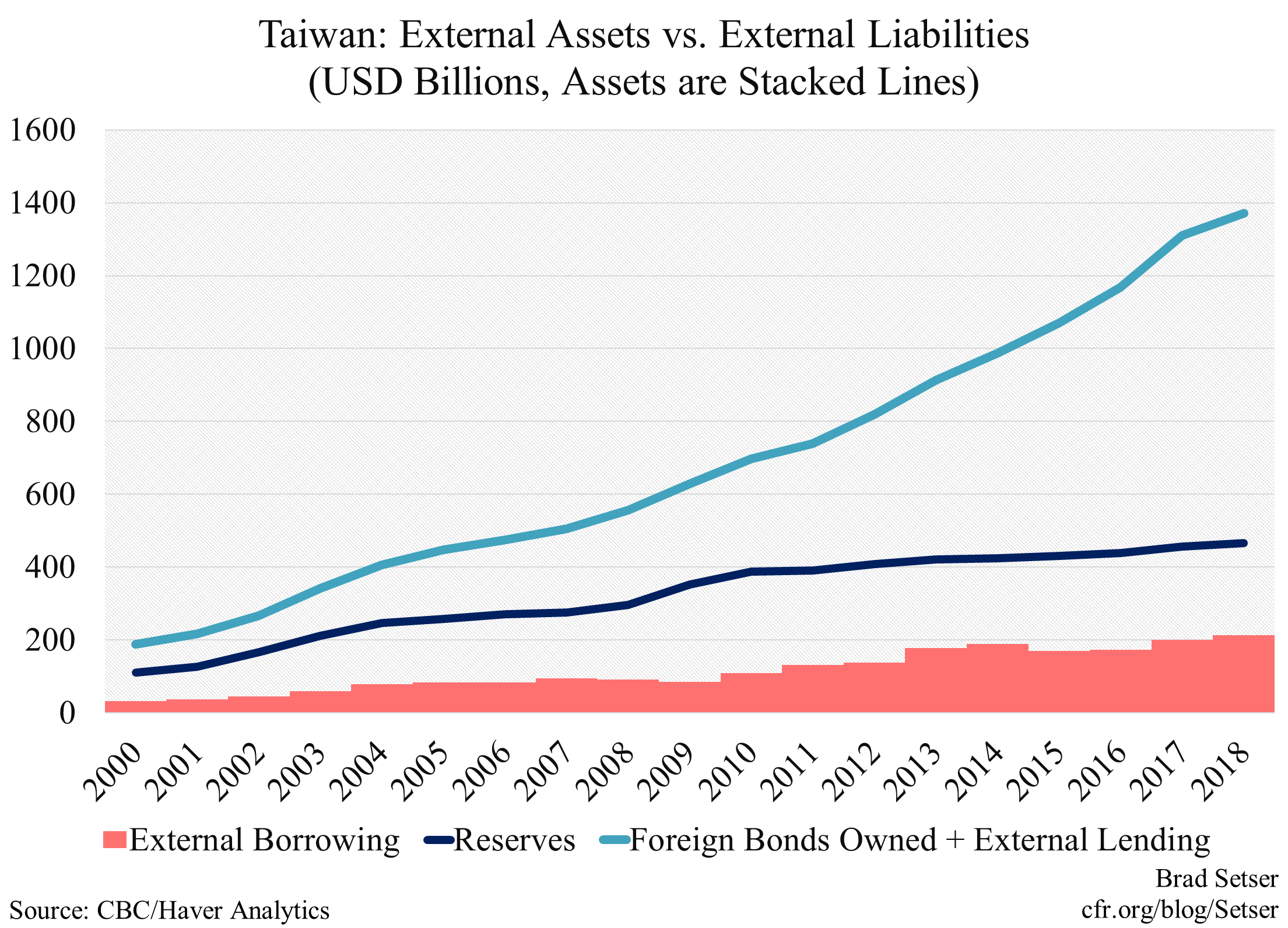

Or take the example of the Asian current account surplus countries that have large sums invested offshore—whether through their life insurers (Taiwan, Japan, Korea), government retirement funds (Japan, Korea, Singapore), their state banks (Japan through Post Bank, China), or their central bank (China, Japan, Taiwan, Thailand, Singapore). They will see the value of their accumulated offshore portfolio of assets drop. That’s only an immediate problem if the assets are held on levered balance sheets—some insurers, for example, are pretty thinly capitalized, and could face difficulties.

Now some of these institutions effectively need to borrow dollars to hedge their portfolios against currency risk (in this case the risk that the “home” currency appreciates against the dollar) and they may find it difficult to obtain hedges in the market.* Their “home” central banks in my view need to—and can—step up, and their regulators need to show flexibility.

Taiwan’s insurers for example have a large hedging need (one that its central bank could meet so long as the lifers don’t increase their hedge ratio). But it has significantly more foreign assets than foreign debt. It faces the same risk as other creditors, namely that it lent out funds that it may not get back in full or on time. But it isn’t at any financial risk. The equity capital of some of Taiwan’s life insurers (see chapter 3)—and for that matter Korean life insurers—is of course at risk. But any shortfall in the life insurers equity can be made up domestically, through a government recapitalization.

Countries with strong external balance sheets consequently can weather the storm if they act decisively and use their public sector balance sheet to backstop leveraged financial institutions. That is all the more true for countries with both strong balance sheets and access to the Fed’s swap lines (Japan, Korea, Singapore—which should first use their own excessive reserves). The swap lines allow central banks to act as dollar lenders of last resort to their local financial institutions**, and could be re-purposed (see Concentrated Ambiguity) to allow central banks around the world to supply hedges (through cross currency swaps) directly. The Fed’s new repo facility for central banks with large Treasury holdings should help here too.***

The more difficult and pressing problems arise among countries around the world that have weaker external balance sheets. There are a number of emerging economies with more external debt than liquid reserve assets, or for that matter, foreign assets of all sorts. In a crisis, those countries that most need financing are the least able to get it.

I would differentiate here between two different kinds of funding needs:

1) Funding trade receivables: i.e. trade finance or the funding needs from the intermediation of trade flows, which is primarily a dollar need; and

2) Offsetting a short-fall in external inflows: i.e. classic medium to long-term balance of payments funding needs. Right now those balance of payments shortfalls can arise from a massive terms of trade shock (many oil exporters), from a fall off in financial inflows (South Africa), or even from a run on a dollarized domestic banking system (Lebanon).

Both types of funding shortfalls need to be addressed. But different problems require different solutions.

Central banks globally—with help from the Fed—can help with trade finance. Remember that in many countries a lot of trade financing is provided by global banks (Japanese banks in particular), not just their home country banks. National export-import banks also have a role to play. Agustin Carstens of the BIS has provided some exceptionally helpful suggestions—building on the work Hyun Shin and the BIS research staff have done laying out trade and supply chain related dollar funding needs.

Providing funding against “trade receivables” is however fundamentally different from making up for a lack of “receivables”— there will be a need for more financing as trade slows down, but also a need for long-term financing for those countries whose exports fall faster than their imports.

The Fed’s swap lines historically have not been used to make up for financing shortfalls from a classic fall off in portfolio inflows, or large swings in the current account.

Those are the kinds of financing shortfalls normally met out of national reserves—with the IMF and the World Bank stepping in to provide additional financing when national reserves are insufficient.

Now is the time when the IMF can and should use its ability to create global reserves through what’s called an “SDR allocation” (the IMF credits its members with “SDRs”, and SDRs in turn can be converted into dollars or euros). Raising global reserves right now to meet a higher global need for reserves makes sense. Even the United States could benefit—as the U.S. Treasury has been using the funds in the Exchange Stabilization Fund creatively to backstop various Fed programs. Those who have plenty of reserves already can lend their SDRs back to the IMF.

But SDRs are distributed according to a country’s IMF quota, not according to the amount of reserves a country now needs—so an SDR allocation on its own is insufficient. The IMF also needs more resources.

My friend (and teacher****) Ted Truman has laid out a detailed agenda for raising the IMF’s lending capacity. Much of this would need to be agreed on by the time of the IMF’s spring meeting.

The Center for Global Development (see Landers, Lee, and Morris) has put forward an innovative idea for expanding the lending capacity of MDBs by making use of their callable capital (this likely requires legislation that’s arguably warranted at this break the glass moment).

The IMF and World Bank’s call for bilateral creditors to defer payments is clearly justified—and in many cases, as Sean Hagan and Lee Buchheit have laid out, private creditors should also be encouraged to extend the maturity of bonds that are coming due in 2020. Of course, private creditors would rather be paid. But voluntarily pushing out maturities beats default, and no country should have to face a situation where it is unable to pay for food and medical supplies simply because it has an external bond coming due. This will take goodwill, including on the part of investors who aren’t always known for this, but it is technically possible.

When private capital retreats, the official sector needs to advance—and with creativity, sufficient resources can be mobilized to limit the global shock.

While none of this will prevent a massive global downturn, it is crisis economics—the financial equivalent of emergency medicine. The goal is to preserve the basic financial infrastructure of the global economy so that it can bounce back strongly once the virus has been contained. And when that bounce back happens, many more reforms will be needed.

* For more on the mechanics of dollar hedging, see this post, which offers a clear primer.

** A couple of words about the swap lines. They weren’t used in the crisis to provide balance of payments finance. Rather they were used to provide dollar funding to institutions that were regulated outside of the United States (even though they typically had large U.S. operations) and that had large dollar balance sheets. Think of the U.S. subsidiary of a European bank that had raised short-term dollars by selling commercial paper to U.S. money market funds and by taking in dollar deposits globally (including large dollar deposits from central banks with excess reserves) and then invested those funds in the U.S. mortgage backed securities market. That bank wasn’t actually providing the United States with current account financing— as it was raising the dollars either domestically in the United States or from a reserve manager. Rather it was acting as a classic intermediary and taking credit risk.

Many now remember how the dollar rallied during the peak of the crisis. But from 2005 to the middle of 2008, private financial flows—the dollar was steadily weakening—and real private financial flows into the United States fell. The current account deficit was financed by the well over a trillion dollars that the world’s central banks were adding to their reserve portfolios. But—as Brender and Pisani laid out so clearly, in a still under appreciated monograph—sustaining the U.S. external deficit during this period took both central bank dollar reserve accumulation to take the currency risk and private intermediaries to take the credit risk. The system of private credit risk intermediation broke down well before the world’s central banks lost their appetite for FX intervention (contrary to a forecast that I made with Dr. Roubini back in 2005).

I wrote about this in a paper for a conference on the tenth anniversary of the global financial crisis that was held in Iceland of all places—a paper (pdf) that I hope gets a bit more attention now. This history is again relevant.

*** I suggested that the Federal Reserve consider a repo facility for central banks to supplement the swap lines two weeks ago. Concentrated Ambiguity (STW) has put forward ideas for how central banks with strong external balance sheets could facilitate private sector hedging by a broader set of institutions than banks. Cheap Convexity (Jon Turek) also had laid out the case for action to support the hedging market, as “the biggest players in the FX swap market are not banks anymore, its non bank actors who use it to hedge longer duration USD exposure.”

**** Ted has taught me as much about the balance of payments as anyone over the last twenty years, usually by pointing out—sometimes loudly—my errors.