Why Global Trade Imbalances Could Get Worse Before They Get Better…

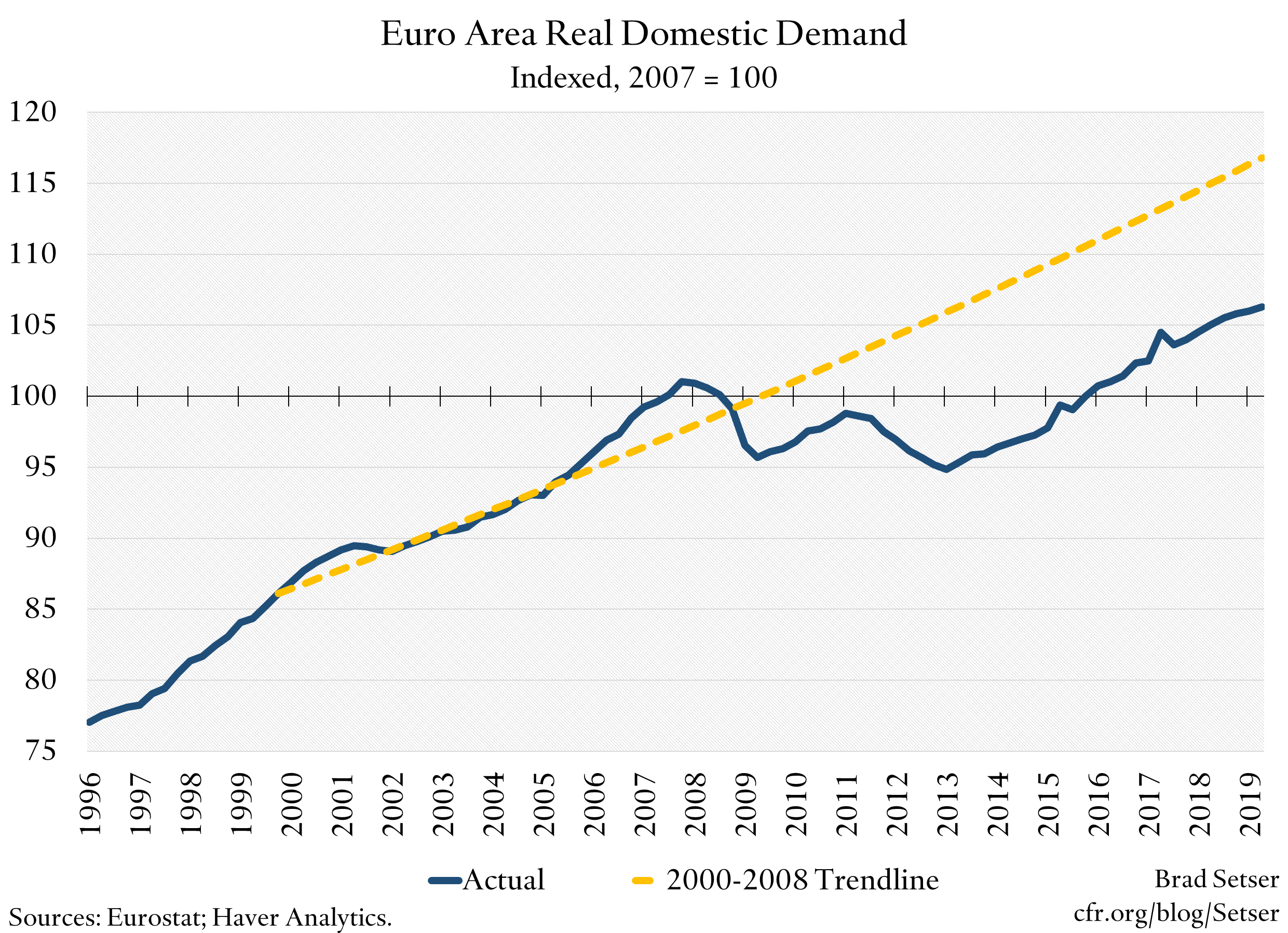

Transatlantic imbalances reflect Europe’s demand deficit, which should be easy to solve (but isn’t). Transpacific imbalances haven’t disappeared. And are likely harder to solve, as they stem from an underlying savings surplus.

The north-south dimension of global trade imbalances has waned over time—once oil prices fell, the “commodity” component of the world’s imbalances has shrunk. At $60 a barrel, most oil exporters cover their import need, but aren’t saving a ton. And the United States—thanks to a surge in domestic production that displaced imports—isn’t a big oil importer any more.

Even Australia—a wealthy, commodity-exporting country in the world’s geographic south—doesn’t have much of a current account deficit right now. High iron export prices (thanks to Brazil’s bad luck) and rising LNG exports to China in particular have closed Australia’s once large deficit.

As a result, trade imbalances run mostly along an east-west axis these days.

Across the Atlantic, where the United States, Canada, and Mexico absorb a portion of Europe’s surplus.

And across the Pacific, where the United States, Canada, and Mexico absorb East Asia’s surplus.

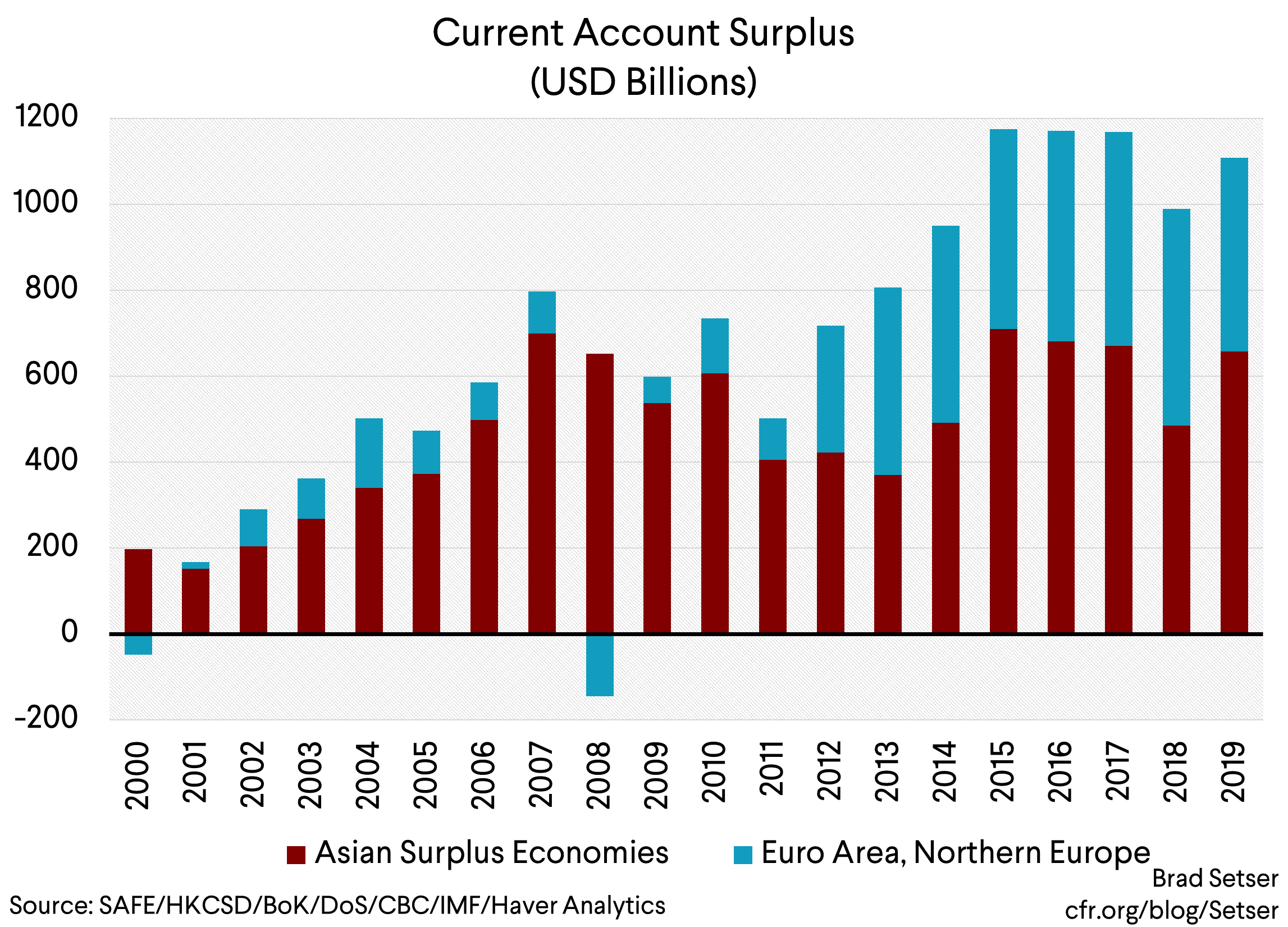

It is of course too simple to reduce everything to a single number—but in very rough terms, the U.S. trade deficit in manufactures right now just happens to be about equal to the combined current account surpluses of Europe and East Asia.

Looking only at the United States leaves out Canada and Mexico. Both have been running external deficits comparable to the U.S. deficit, though Mexico shifted into a surplus in the second quarter. The weak peso and all.

More importantly, looking only at manufacturing leaves out the surplus that the United States runs on intellectual property trade (which is fairly modest because of tax considerations) and the surplus the United States runs on its offshore investments (the entire surplus on foreign direct investment income comes from the seven main low tax jurisdictions these days, see Martin Wolf).

The United States‘ total current account deficit is now below the combined surplus of Europe and East Asia—but it’s still clearly the case that global trade cannot balance today without a sizable U.S. deficit. If China, the euro area, and Japan all have significant surpluses, someone big needs to have a significant deficit for global trade to add up.

The transatlantic imbalance tends to get the most intellectual attention these days, as that deficit is newer—and, well, it maps easily into a fiscal morality play.

Europe is too tight-fisted (Europe north of the Alps in particular, especially if Britain is excluded), the United States is too profligate.

With demand in short supply globally, negative interest rates in Europe and Japan, and real interest rates globally at very low levels, I would put more emphasis on the European side—but obviously, if the United States responded to tight fiscal policy in Europe with tight fiscal policy of its own, the U.S. trade deficit would shrink. In an unpleasant way, to be sure. But it would go down.*

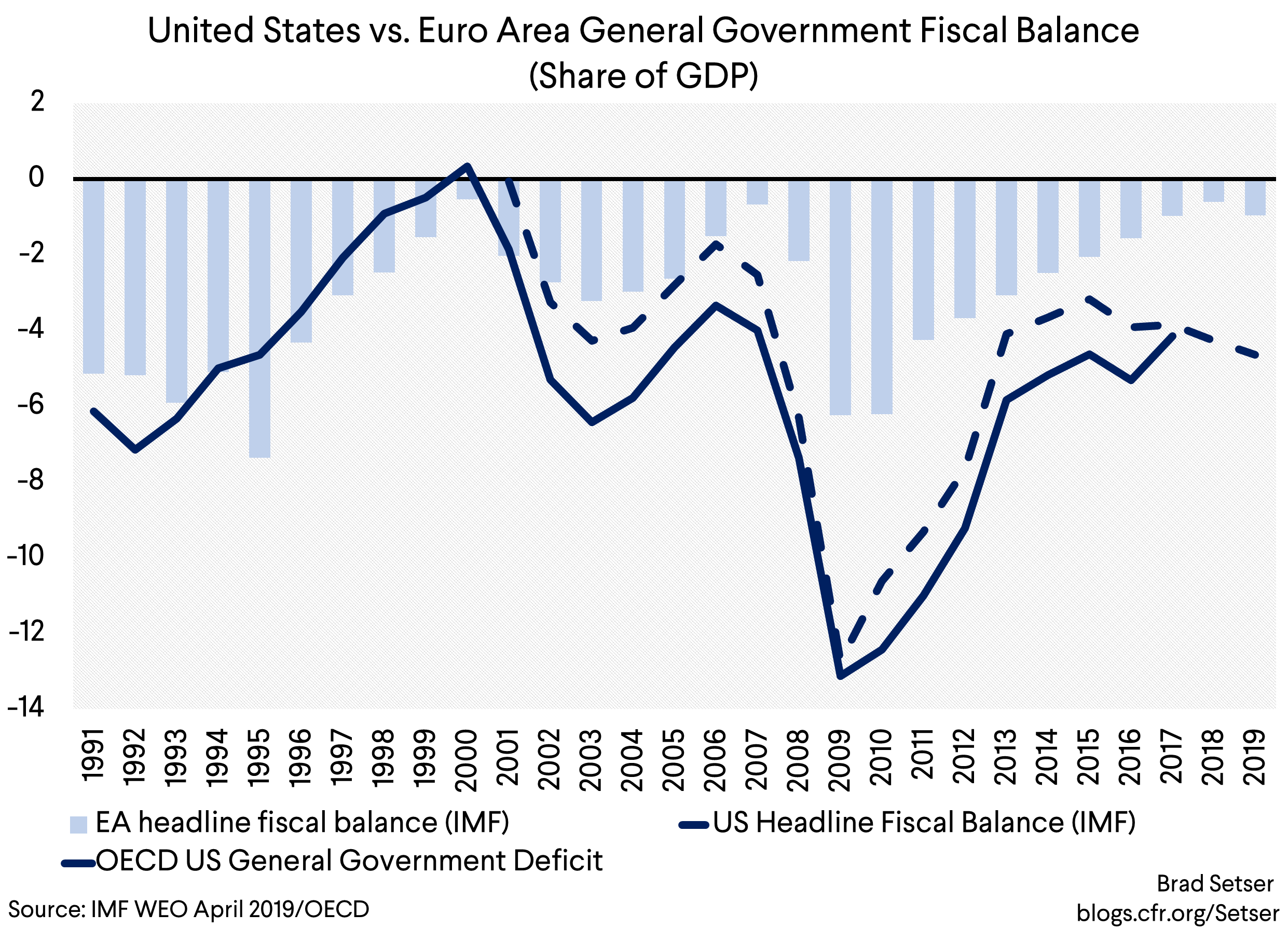

It doesn’t take a genius to figure out that the gap between European fiscal policy and U.S. fiscal policy is a major cause of the transatlantic imbalances (though the very stable genius in the White House hasn’t picked up on this point, he doesn’t attribute trade outcomes to fiscal policy choices).

Maybe European fiscal policy is about to change—Mario Draghi certainly thinks it should. The public debate in Germany is I think slowly shifting—negative rates and a recession helps clarify the mind (and the German high-speed rail network now lags its peers; there is a strong case for investing Euro 50 billion to bring it up to standard). But still Germany ran a (gulp) 2.7 pp of GDP fiscal surplus in the first half of the year. Sweden’s government has made it clear that Sweden isn’t for turning, even as Sweden slips toward recession (housing bubbles are preferred to modest fiscal deficits?). Switzerland prefers yet more intervention by the Swiss National Bank (which already has a balance sheet about equal to Switzerland’s GDP) to any fiscal expansion…

Maybe the French, Italians, and Spaniards will come through—though under the current rules they should be moving expeditiously to bring their debt levels down to 60 percent of GDP, which in a slow nominal growth world implies fiscal surpluses. (The typically European solution has been to basically ignore an unworkable rule, rather than you know, actually change it…see Isabelle Mateos y Lago for more)

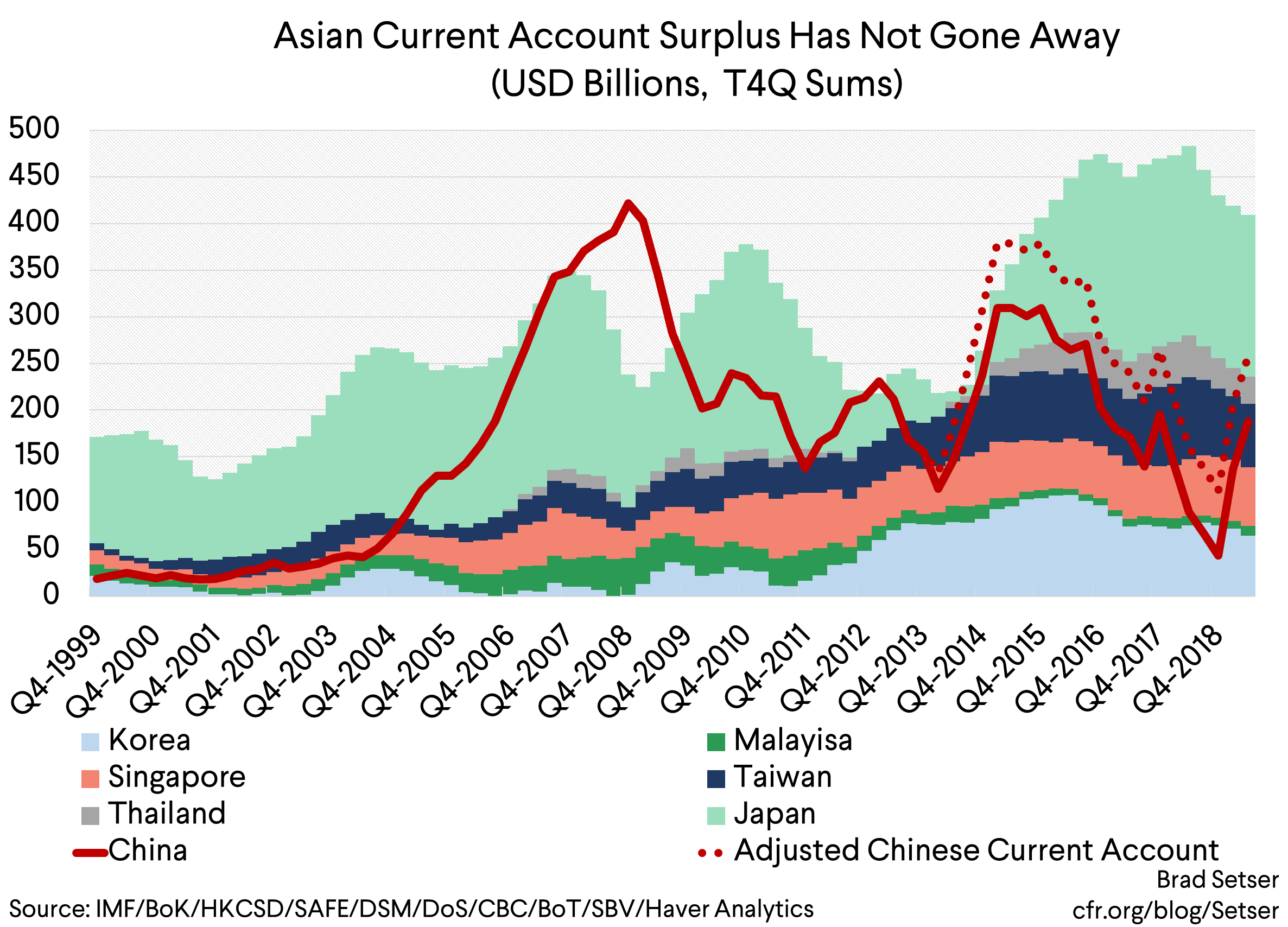

Asia—really all of East Asia and parts of South-East Asia—is harder.

There are the easy bits.

Asia has its Germany. Two really.

Korea and Taiwan. They both run tight fiscal policies when they don’t need to and also give their manufacturing heavy economies a boost with weak currencies sustained through a mix of direct and indirect intervention. Korea’s diversification of its massive National Pension Service helps keep the won weak without outright intervention, as does Taiwan’s light touch regulation of the foreign exchange exposure of its massive insurance industry.

Asia has its Switzerland. Singapore has so many reserves that it basically hides a portion of its national wealth in the Government Investment Corporation, it still intervenes to hold the Singapore dollar down, and its fiscal stance is tight.

And Asia has its holdover from the days of massive intervention by emerging market central banks: Thailand needs to break its recent habit of heavy intervention to manage the baht, and rely a bit more on fiscal policy to support demand.

But the two biggest economies in Asia run relatively loose fiscal policies. Their external surpluses don’t fit easily into a global narrative where imbalances stem primarily from differences in national fiscal policy.

Japan’s fiscal deficit is somewhat higher than that of the euro area as a whole, and much looser than the euro area’s big surplus countries (Japan’s 2019 fiscal policy will be 4-5 pp of GDP looser than Germany’s fiscal policy). I don’t think Japan needs to consolidate more given its stable net debt dynamics and non-existent debt service bill. the coming hike in the consumption tax is a clear mistake. But so long as Japan runs a noticeable fiscal deficit it isn’t quite analogous to Europe’s north.

And then there is China.

Contrary to most forecasts, China is once again running a substantial current account surplus. The measured surplus was just under $200b in the last four quarters of data (more accurate measures of the tourism deficit would put the surplus at around $250 billion). And, to the IMF’s chagrin, that surplus has been sustained even with a 12 percent of GDP “augmented” fiscal deficit (the augmented deficit includes the quasi fiscal borrowing of local investment vehicles, the official general government deficit is more like 5 percent of GDP—and the reported headline central government deficit in the budget is under 3 percent of GDP).

Think about that for a minute. Countries with 12 percent of GDP fiscal deficits usually run large external deficits.

The fact that China isn’t running such a deficit, even with a trade war, tells us something important—namely that China saves way too much. In fact, China still saves about two times as much as a typical large economy—and more than a typical fast growing Asian tiger. The raw material for a much larger Chinese surplus exists.

There are a couple of ways of highlighting this point.

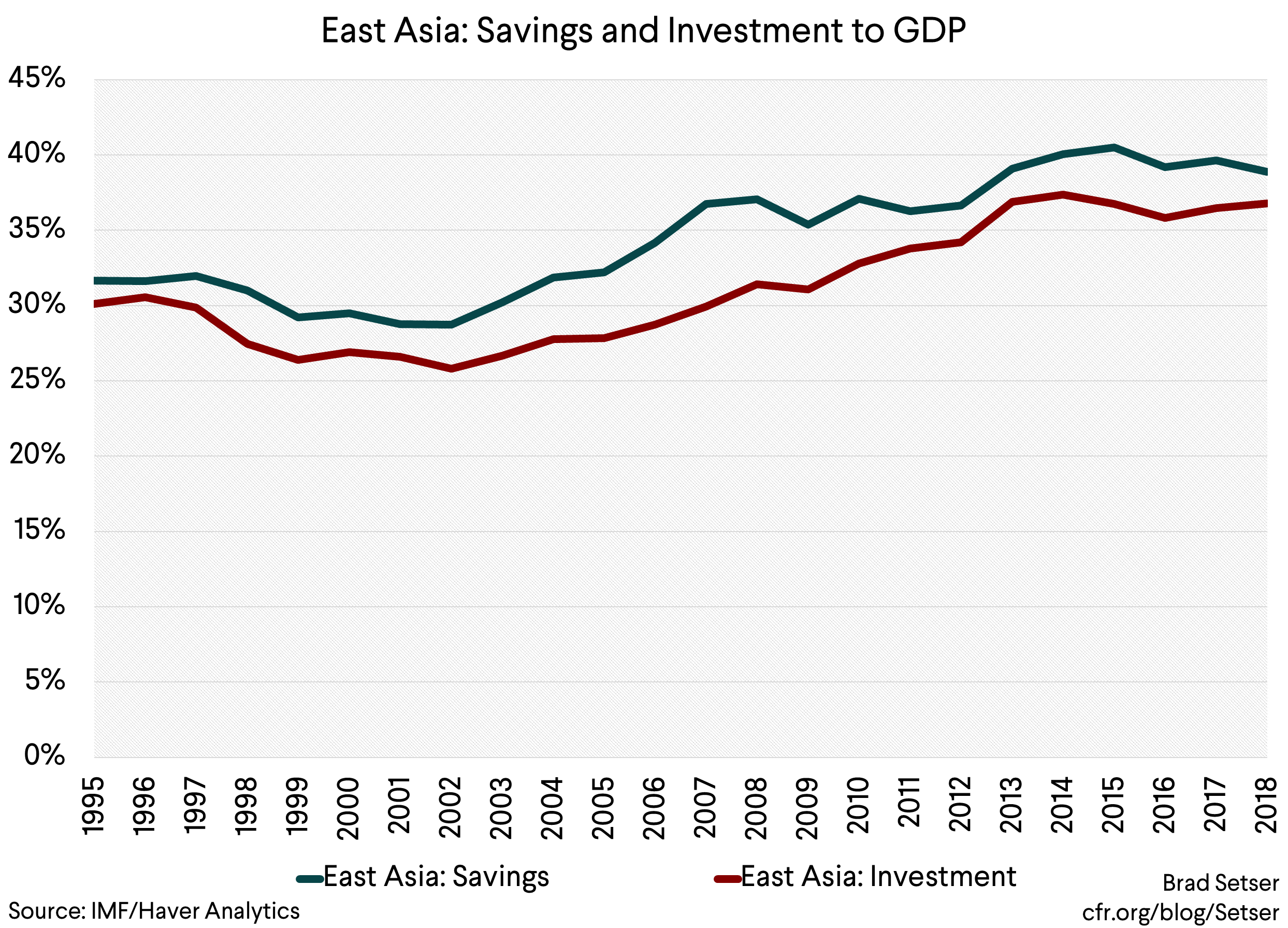

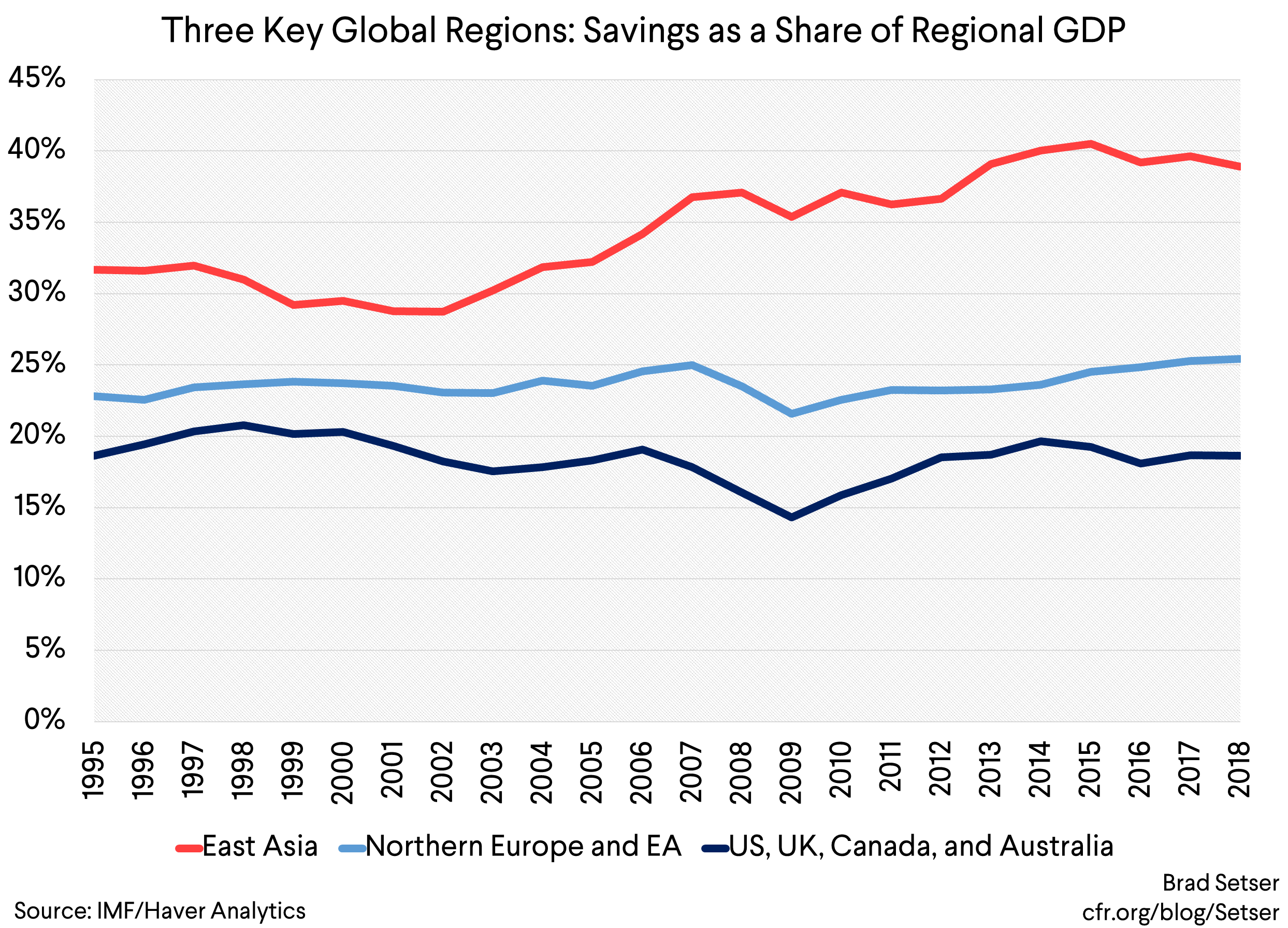

One is to look at the aggregate savings rate of East Asia (China, Japan, and the NIEs).

Despite all the talk of how China’s economy has rebalanced, the aggregated savings rate of East Asia is as high as it has ever been—it remains close to 40 percent of the region’s GDP. That’s far higher than the savings rate in Europe, let alone in the United States.

China’s savings rate has dropped a bit from its super high level of 12 years ago (07)—it is now 44 percent of GDP rather than 51 percent of China’s GDP. But China’s share of East Asia’s GDP has increased from 49 percent in 2007 to 72 percent today.

The only thing preventing that high savings rate from turning into a much larger current account surplus is China’s large augmented fiscal deficit and the associated high level of public investment.

There is another way of showing this—back in 2007, when China’s current account surplus was $400b (10 percent of its GDP), it was saving about $2 trillion a year (50 percent of a $4 trillion economy). Today it is saving close to $6 trillion a year—it wouldn’t be hard to get a $600b current account surplus out of that kind of savings.

So long as China’s adjustment is based on a set of fiscal (and credit) policies that are generally viewed as unsustainable, so there are questions about the durability of China’s adjustment. A more sustainable adjustment requires policies that raise household income and reduce savings—basically more progressive tax policies and a much bigger system of social insurance, one that isn’t just funded out of regressive social contributions.

These risks have seemed hypothetical for a while. But I suspect that part of today’s global malaise is that some of these risks are being realized.

China’s stimulus in 2019 was modest—the credit impulse (according to UBS) is flat, but not expansionary (it was negative in 2018). Too modest in fact to counter the effects of China’s 2018 policy tightening and the trade war. China’s import growth has collapsed—imports are falling in nominal terms, and at best flat in real terms.

That’s all pushed China’s surplus back up. And it has done so without any real fiscal tightening on China’s side—though the fall off in new investment in manufacturing associated with the trade war has contributed (ironically) to the rise in China’s surplus.

The current “flow” deficit in the United States external accounts isn’t obviously unsustainable. The manufacturing deficit is a record high, but thanks to the U.S. oil boom and the large offshore profits American companies now book in the world’s corporate tax havens, the overall current account deficit has stayed under 3 percent of GDP. And external debt isn’t obviously rising relative to U.S. GDP, thanks to a nominal interest rate on U.S. external debt (2 percent or so) well below the United States nominal growth rate (4 percent or so…)

Yet the stock of U.S. external debt is large. The scars from the decade of manipulation haven’t gone away. At 45 percent of U.S. GDP, it is actually quite large relative to the United States’ limited export base. Especially if you assume that the United States won’t be a long-run exporter of energy (too much internal demand in a world where the United States is likely to lag the rest of the world in a transition to a low carbon economy).

Exports of manufactures, (net) exports of IP and net offshore profits total about 8 percent of U.S. GDP. Add a half point of net travel exports if you want. That’s a very modest non-commodity export base.

Broadly speaking the United States has three times more net external debt than it had twenty years ago.

Trump or no Trump. that at some point will limit its ability to take the other side of the world’s saving surpluses.

* To be somewhat undiplomatic, that’s the IMF’s stated long-term plan for reducing imbalances: they want the euro area to continue to tighten but only by a bit, while the US would tighten by a lot—the new MD may want to question whether the long-term fiscal norm for most countries should be fiscal balance.