It is Time to Change How We View Foreign Direct Investment

FDI is increasingly driven by tax avoidance.

A lot of financial globalization has been driven by tax avoidance.

40 percent of FDI globally comes from just seven countries, which collectively account for 3 percent of the world economy.

That’s one striking result of a new IMF working paper.

It paints a picture of foreign direct investment that runs a bit against the common view of foreign direct investment as the virtuous, and low risk, form of financial integration.

Foreign direct investment is generally thought to be real investment in plant and equipment abroad—GE building gas turbines in France, GM building cars in China, Siemens building turbines in North Carolina, and BMW and Toyota building cars in South Carolina and Kentucky.

Statistically, though, FDI is often investment by one special purpose entity (generally located in a tax center) in another special purpose entity…so called phantom FDI.

That is why it is time to start viewing the direct investment data with a more jaundiced eye.

One of the biggest recent “direct” investments globally was Microsoft Ireland’s purchase of Microsoft Singapore. That transaction has a huge statistical impact on Ireland (and the euro area), but didn’t have much of an impact on the “real” Irish economy.

That same critical eye also needs to applied to the data on direct investment into and out of the United States, as it too is heavily influenced by transactions that are likely motivated primarily by tax considerations.

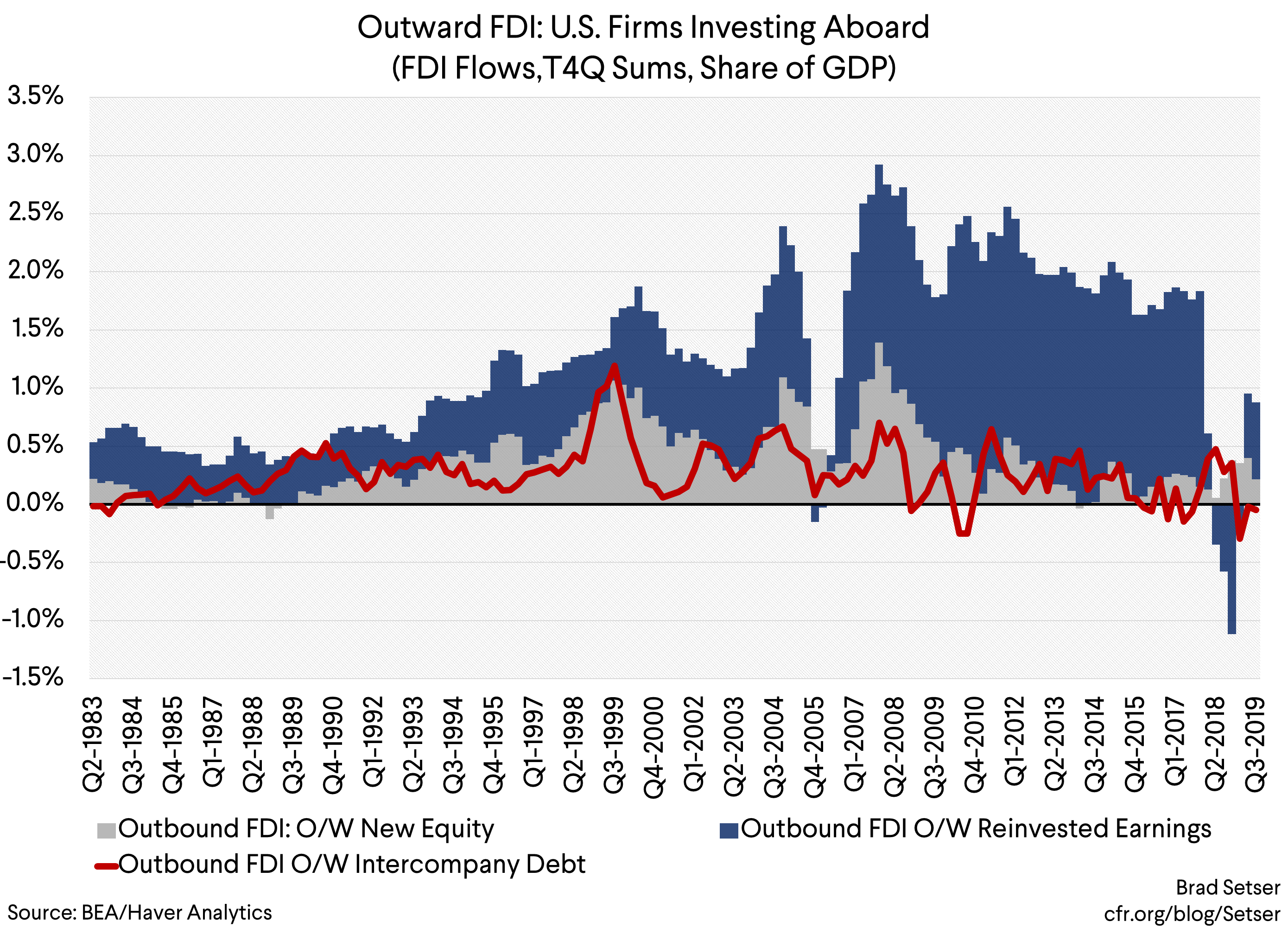

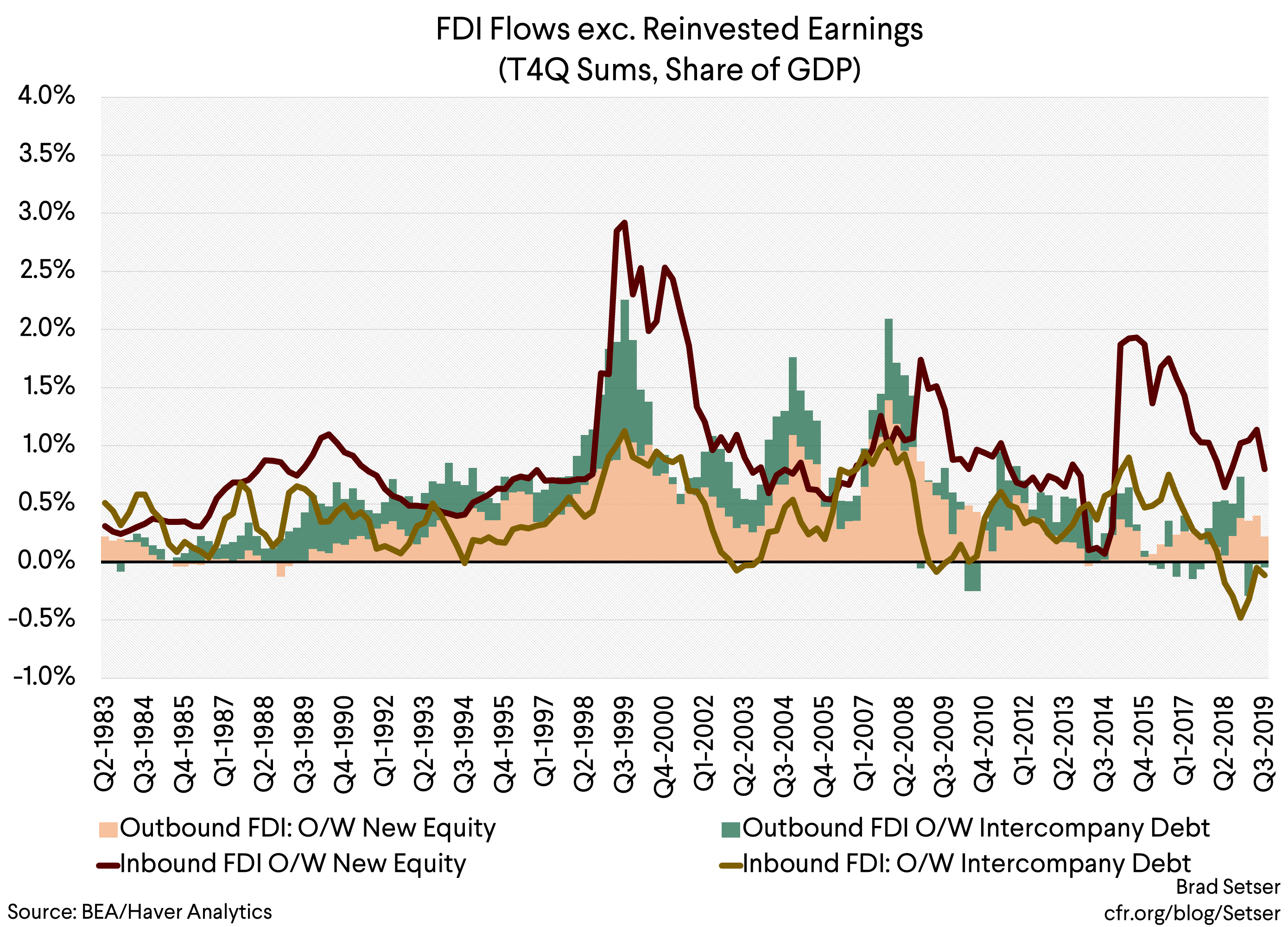

Consider the data on outward U.S. direct investment abroad.

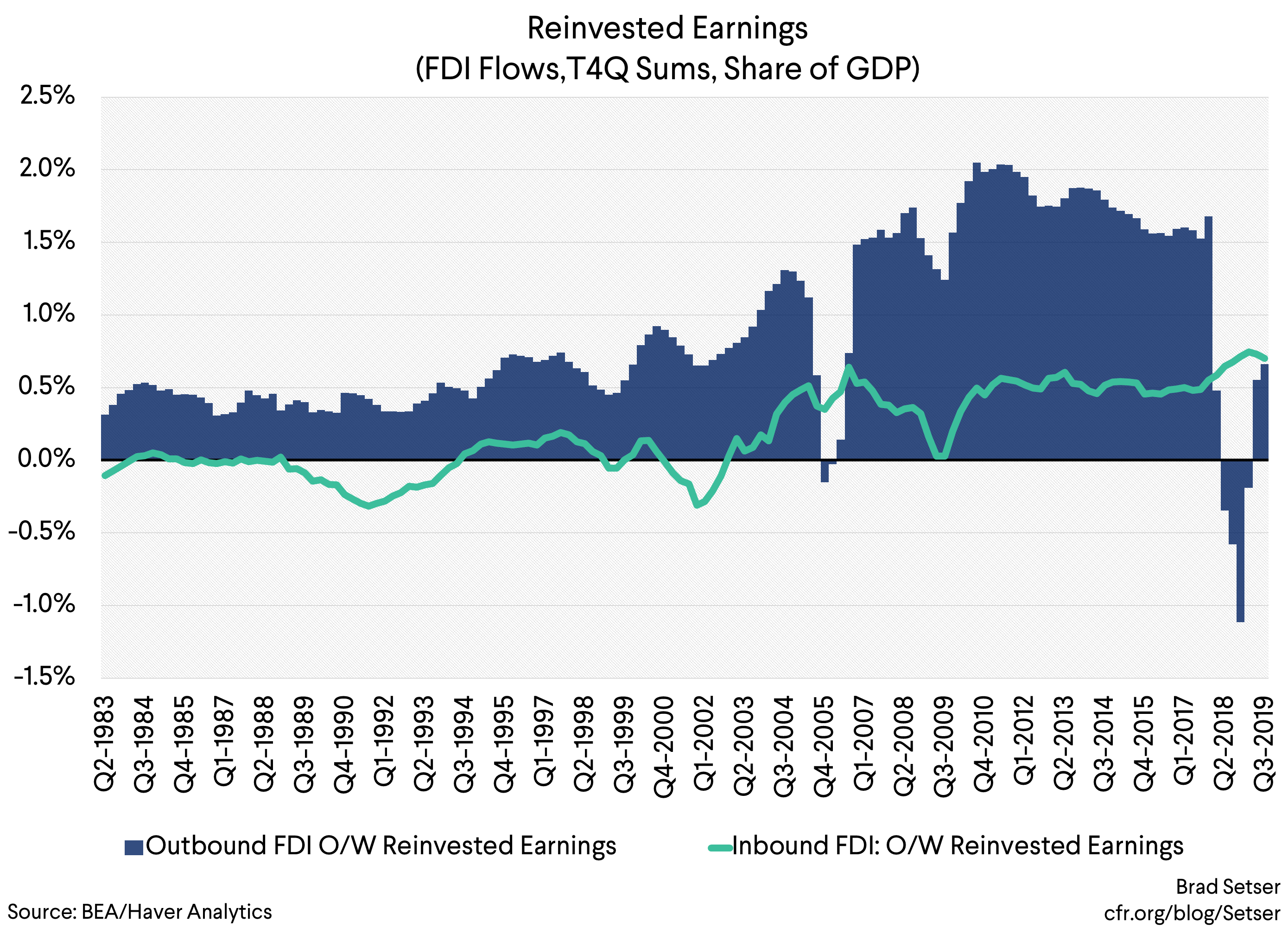

That data historically has been dominated by “reinvested” earnings—the profits American firms earn abroad that they legally kept in their offshore subsidiaries.

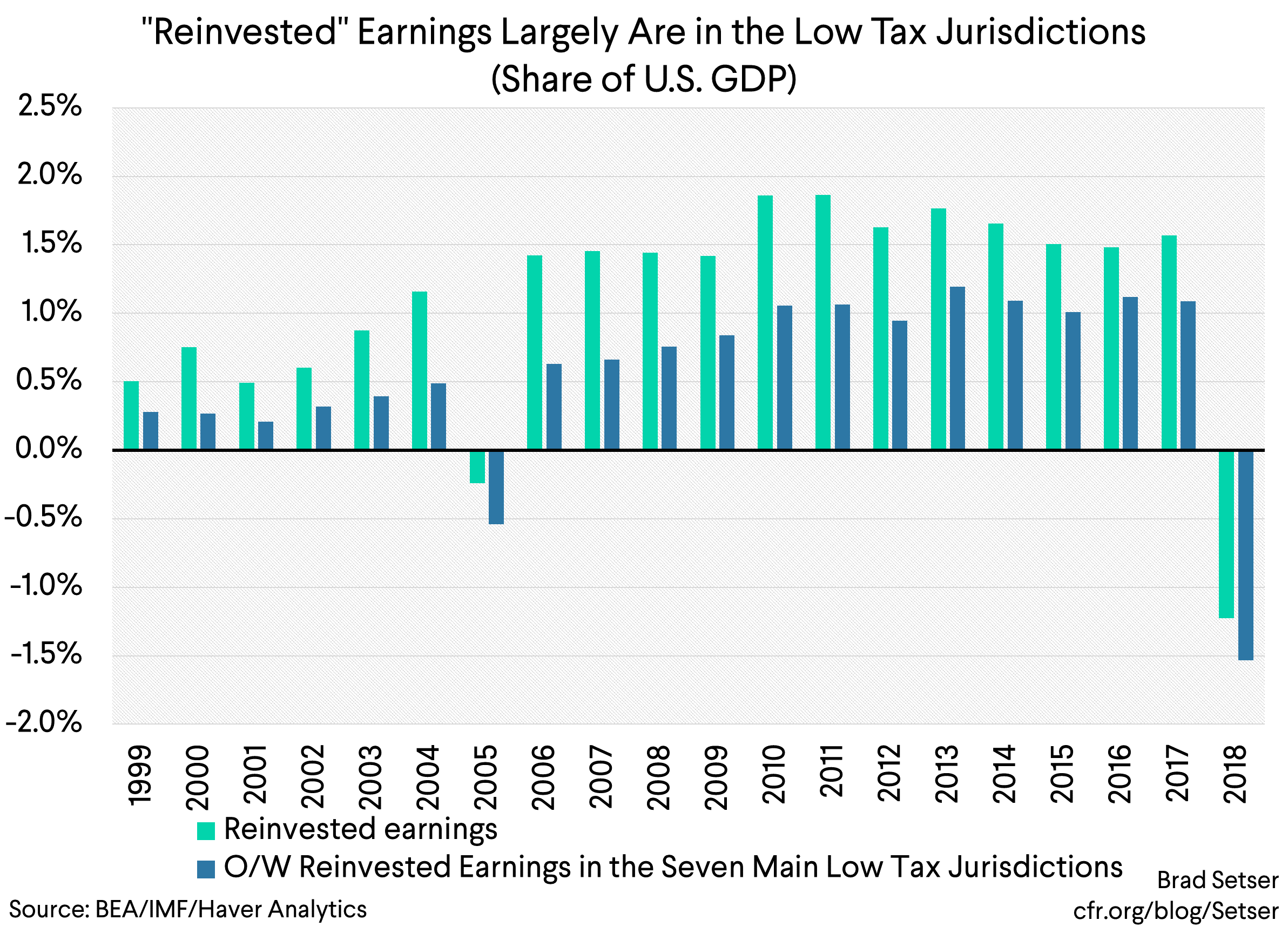

This was the source of the supposedly offshore cash stash of U.S. firms (the funds were only legally offshore, as they legally were assets of say Apple Ireland or Microsoft Bermuda; in practice they were invested in U.S. financial assets—and firms that wanted to access their offshore cash to say buyback their shares could do so by borrowing against their offshore cash). The bulk of those reinvested earnings—if you looked closely in the data—weren’t being reinvested in physical assets, but rather were piling up in the offshore subsidiaries U.S. firms had established in low tax jurisdictions. From 2010 to 2018, 65 percent of all reinvested earnings were “reinvested” in jurisdictions like Ireland and Bermuda (which works out to about $200b a year of investment in those jurisdictions, or about half of all US FDI in the “pre-tax reform” data).

That clearly was a function of firms’ ability to defer paying U.S. tax on otherwise un-taxed global profits under the old tax law. Profits earned in high tax jurisdictions didn’t have any U.S. tax liability under the old law, as firms could deduct taxes actually paid abroad. Indefinite deferral effectively distorted the global data—raising the amount of U.S. direct investment abroad (the cash Apple held in Ireland was an asset of Apple USA, so reinvestment raised the stock of U.S. equity assets abroad even if technically the equity investment abroad was the accumulation of offshore cash) and the amount of foreign claims on the United States (U.S. treasuries purchases by Apple Ireland were counted as foreign holdings of U.S. government debt, that’s why Ireland was at one time the world’s third largest holder of U.S. Treasuries).

In other words, financial globalization wasn’t all benign—rising “globalization” could simply mean more tax arbitrage, not more real integration. Reinvested earnings by U.S. firms abroad rose from about half a point of U.S. GDP in the 1990s to between 1.5 to 2 percent of GDP…a number out of line with the sum foreign firms “reinvested” in the United States.

And equally the big fall off in U.S. direct investment abroad after the new tax passed—which was the reversal of past “reinvesting” of earnings abroad, as firms with large holdings of U.S. assets in their foreign subsidiaries paid large dividends back to their parents—wasn’t evidence of any real slowdown in U.S. investment abroad.

It was basically just a big tax game, which inflated the FDI data until it (partially) reversed after the tax reform.

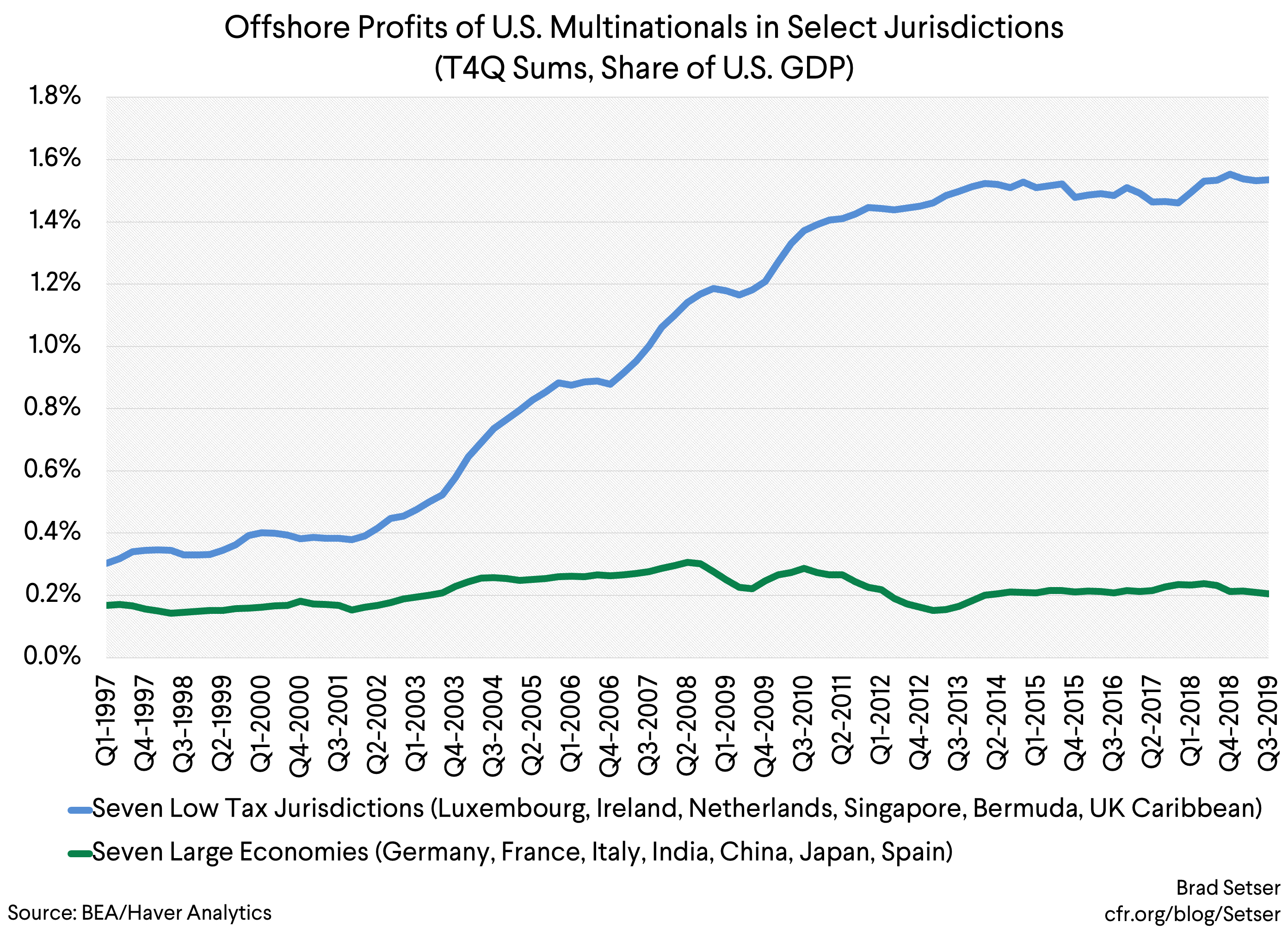

Under the new tax law, U.S. firms still earn large profits in low tax jurisdictions (see Martin Wolf, the IRS country by country data or Kim Clausing’s latest)* but they no longer have a federal corporate income tax incentive to “reinvest” those funds abroad and accumulate financial assets inside their very profitable subsidiaries in low tax jurisdictions. Profits booked in a low tax jurisdiction can now be returned to the United States with no tax penalty—and they equally can be held abroad with no tax limits on how they can be used.

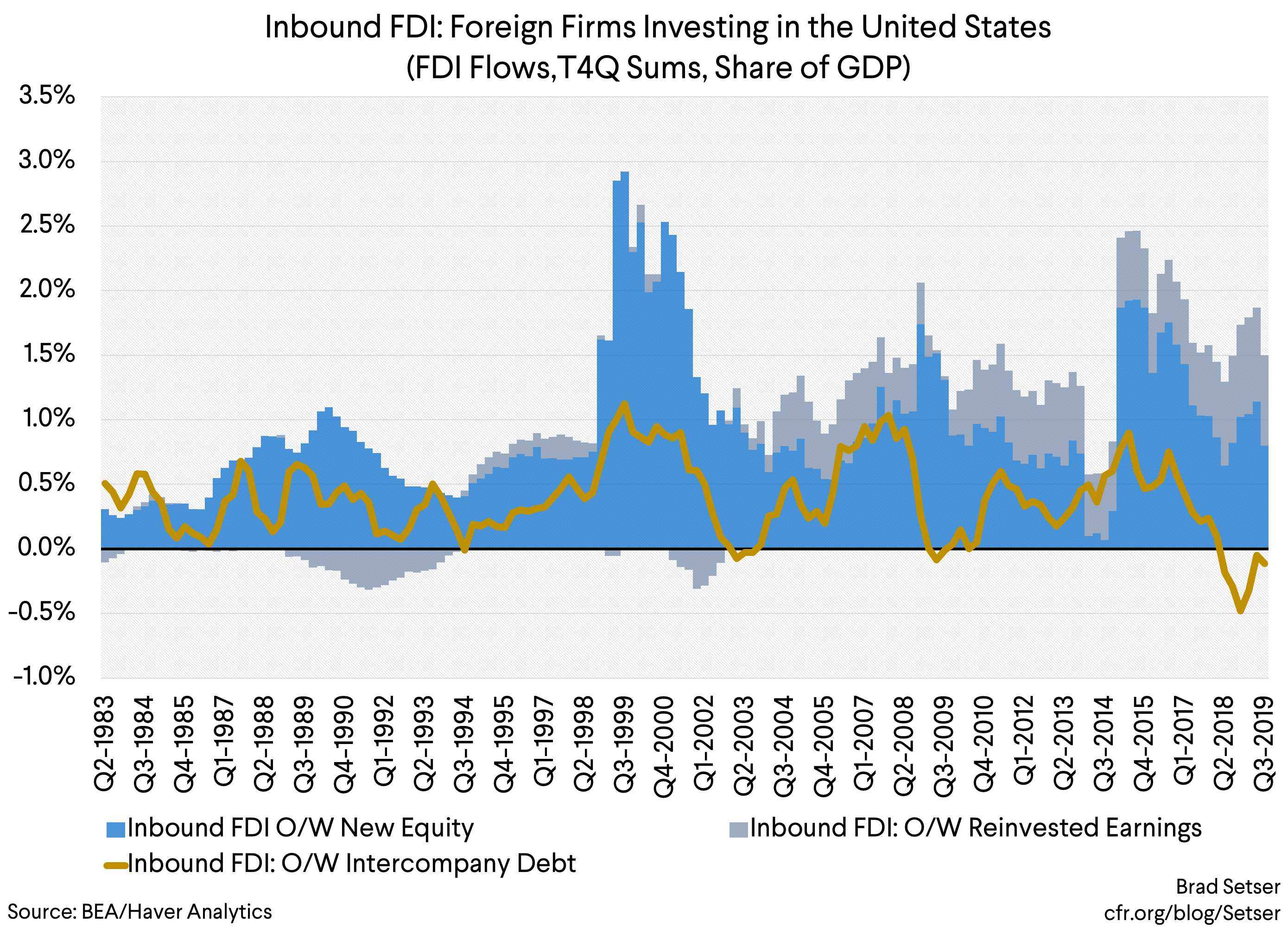

What about the data on inward direct investment into the United States? Is that a measure of the “attractiveness” of the United States as a destination for foreign firms?

Well, not entirely.

There are two tax related distortions in the inbound data.

Foreign firms historically haven’t necessarily wanted to pay U.S. corporate tax on their U.S. profits, and the standard way to shift profits out of the United States was to structure investment in the United States as a large intercompany loan. The interest paid on the loan could be deducted from the firm’s U.S. profits, reducing the firm’s U.S. tax burden—and the financial profit on the loan could be booked in a more favorable (tax wise) jurisdiction.

And, well, there was a time when U.S. firms would buy small firms in a low tax jurisdiction, and then have the firm in the low tax jurisdiction buy the parent (an inversion). That would make a formerly U.S. firm “Irish” for tax purposes—and it would register in the data as a big surge in inward direct investment. The bulk of FDI flows, if you set aside the “reinvested earnings” that were favored by the old U.S. tax law, are the result of mergers and acquisitions, not of greenfield investments. An Irish company taking over a U.S. company thus would result in a surge in FDI inflows.

But I wouldn’t call that evidence of healthy financial globalization.

All this is reasonably clear in the numbers on inward FDI flows over time.

Inflows from inter-company loans historically have been about a third of the total direct investment in the United States. as foreign firms investing in the U.S. have wanted to reduce their taxable U.S. profits.

And the recent peak in direct investment “equity” inflows to the United States was also tax driven.

The first peak in the late 1980s was real—Japanese auto firms set up shop in the United States to produce cars in the United States after the yen appreciated.

The second peak in 2000 was a function of the dot-com bubble, as foreigners bought U.S. firms at really high valuations. Most direct investment these days stems from mergers and acquisitions, not greenfield investment.

And the third peak in 2015 was basically tax—it reflected the surge in inversions, and it fell off when the rules on inversions were tightened.

The fall-off in FDI is sometimes seen as evidence that Trump has scared away foreign investors—but that’s not really what the data shows.

And equally there are some who argue that the rise in “equity” FDI in 2019 is evidence that the tax law has made the United States more attractive to foreign direct investors.

That though isn’t how I would look at it. FDI is about where it normally is (around 1 percent of US GDP), but after the tax reform, a bigger share is taking the form of “equity” and a smaller share the form of “intercompany loans”—that’s no doubt a function of the BEAT provisions in the new tax code.

Bottom line: the FDI data often tells us more about the tax code than anything about the relative attractiveness of a country for “real” investment. And those blindly celebrating a rise in financial globalization need to be careful not to celebrate the rise in measured financial globalization that effectively is a result of “phantom” FDI motivated by (legal) tax avoidance.

* Kim Clausing has a nice review of the debate on how much of the profits U.S. firms earn offshore is earned in low tax jurisdictions. I share her conclusions—the “equity-like income” number (which puts “only” 40 percent of U.S. firms offshore profits in the main low tax jurisdictions) seems too low. Zero or negative earnings in Bermuda (see table F) isn’t credible when Microsoft Ireland and Microsoft Singapore are tax residents of Bermuda (or were at the time of the data—Microsoft’s tax structure, which was laid out by the Senate subcommittee on investigations—has changed this year), and when Google’s Dutch subsidiary serves as a way station between its Irish subsidiary and its Bermuda subsidiary (i.e. the Dutch twist in a double Irish). So called foreign to foreign tax shifting is real—it isn’t credible to argue that the Irish and Dutch subs of U.S. multinationals are just aggregating the profits that these firms have already booked in their French and Germany subsidiaries (if so, they would be paying a lot more tax in France and Germany than shows up in the IRS data, or in the coffers of the French Treasury). The balance of payments “income” data—which I use—may slightly over count (e.g. some of the income booked in the Netherlands may have been earned and taxed in high tax jurisdictions as the Dutch subsidiary acts as a parent for the firms‘ investments elsewhere) , but only slightly. It maps pretty well to the country by country IRS data (which alas is only available for 2016 right now).