A Follow-up on the Thai Baht

Most countries intervene to limit appreciation, not directly to depreciate their currency. And limiting appreciation is a problem when the country has a large external surplus.

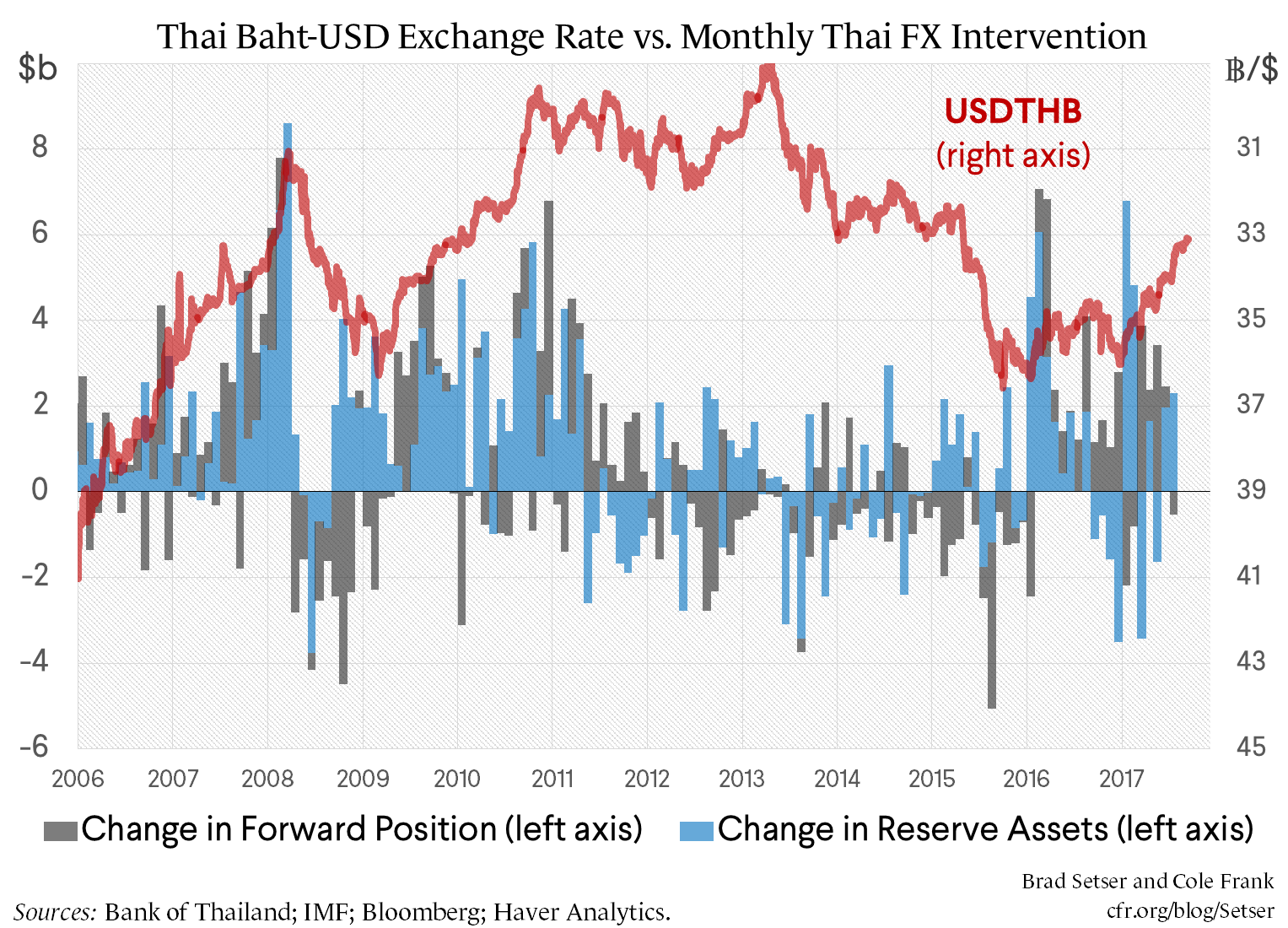

A quick follow up on yesterday’s post on the baht.

One objection to highlighting Thailand in the coming foreign exchange report is that the baht has appreciated this year, and, well, to be a really bad actor, you have to be intervening to drive your currency down.

That argument though fundamentally misses how most central banks currently act in the foreign exchange market to give their country a competitive edge.

It is rare for a central bank to actively seek to depreciate their currency (China did it in early 2013 I think when it was worried about excessive speculation on appreciation and wanted to push the yuan off the strong edge of its band, so it does happen—but not commonly). Rather central banks allow the market to push their currency down during periods of global risk aversion—the 2008 crisis, the taper tantrum, the 2015/early 2016 China scare–and then intervene to block appreciation when market conditions change.

Ted Truman–once of the Fed, then in the Clinton Treasury, now a fixture at the Peterson Institute–calls this competitive non-appreciation.

It happened in the first part of the 2000s, when emerging Asian countries that had seen their currencies depreciate against the dollar in the Asian crisis (and in the tech bust) didn’t want to see their currencies appreciate against the dollar when the tide turned in 2003.

It happened after the global crisis, when Korea, Taiwan, and others played this game aggressively. The won sold off hard in the global crisis–in large part because Korean banks were borrowing heavily from global banks and had too much short-term debt. Korea then discovered that it liked the boost the weak won provided to exports, and intervened to hold the won down (all while running a very tight fiscal policy compared to its peers).

And Thailand is playing this game now. The baht sold off big in 2013 (the taper tantrum), hung around 32 baht per dollar in 2014 (surprising stability given a military coup) and then fell again in 2015 (the China scare). But the weak baht worked its magic on the current account–in part through a surge in Chinese tourism; tourism tends to respond to exchange rate moves even more than goods trade. And when pressure for the baht to re-appreciate emerged in 2016, Thailand’s central bank stepped in to limit appreciation.

And it has kept that up in 2017.

I consequently do not find the argument “the baht is appreciating so Thailand isn’t manipulating” to be all that persuasive. Most countries intervene to limit appreciation, not to actively depreciate their currency. The question to be answered–whether by the IMF, its external surveillance process, or by the U.S. Treasury–is whether that intervention is coming at a level that blocks “effective adjustment of the balance of payments” or provides an unfair competitive advantage.

In Thailand’s case, it is intervening to keep the baht from appreciating more–both versus the dollar, and versus a basket–at far too weak a level given the size of Thailand’s external surplus .

I also would note Thailand has the fiscal space needed to maintain growth if a stronger currency slows exports. Gross public debt is about 40 percent of GDP and has been trending down. In 2015 and 2016 the general government had–according to the IMF–a structural budget surplus. The IMF forecasts a swing into a modest structural deficit in 2017. The headline deficit though is projected to fall in 2018.