A Big Borrower and a Giant Corporate Tax Dodge? How Best to Describe the U.S. External Balance Sheet

Most grandiose explanations for the United States’ persistent surplus in the income balance of the U.S. current account miss the mark. The U.S. debt position tracks the sum of past current account deficits, and the interest rate on that debt tracks the U.S. Treasury rate. The surplus in the income line all comes from the excess income U.S. firms report earning in a few corporate tax havens.

The United States is…

A bank, making a profit by offering the world safe deposits while making profitable long-term loans?

A private equity fund, borrowing to invest in equity with a higher return?

A hedge fund, using leverage to juice returns in a range of markets?

There are a lot of different analogies out there for the United States‘ net international investment position.

And in my view, most of them are out of date.

The right metaphor is rather less glamorous. The United States is more like a household that has been allowed to take out a large home equity line at a very generous rate by its creditors, or even more accurately, a household that uniquely has been able to borrow on an unsecured basis at a fairly low rate.

The argument that the United States functions as a financial intermediary that borrows cheaply to buy higher yielding financial assets—e.g. a skilled user of leverage—has a long intellectual history. And it naturally has a certain amount of appeal to many American financiers. It dates back to the original French critique of the exorbitant privilege the Bretton Woods system accorded the United States. Under the (brief) gold-dollar standard, the rest of the world was more or less required to build up dollar reserves—providing an inflow to the United States. And back in the 1960s, the U.S. current account was in balance, so the United States was using the inflows to fund riskier and higher yielding investment abroad. France was complaining that it was funding the takeover of Europe by U.S. multinationals…

More recently, the argument was revived—by a group of very good French economists, incidentally—back when a falling dollar was generating capital gains on the United States’ holdings of foreign equities. The United States, it was argued, was just borrowing against its (unrealized) capital gains—so the then very large U.S. current account deficit wasn’t as much of problem as it seemed, financially speaking.

But that argument now runs into two problems.

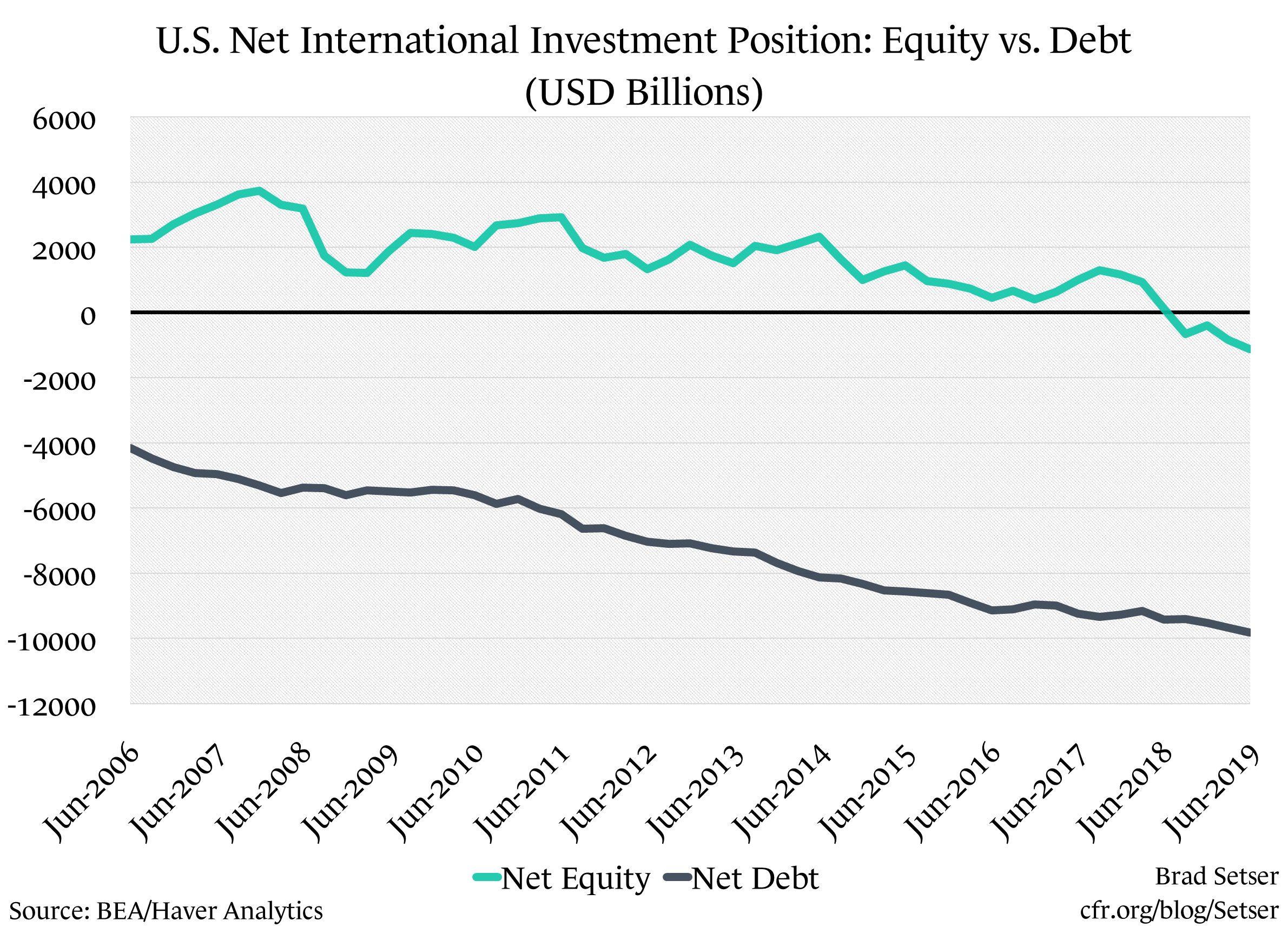

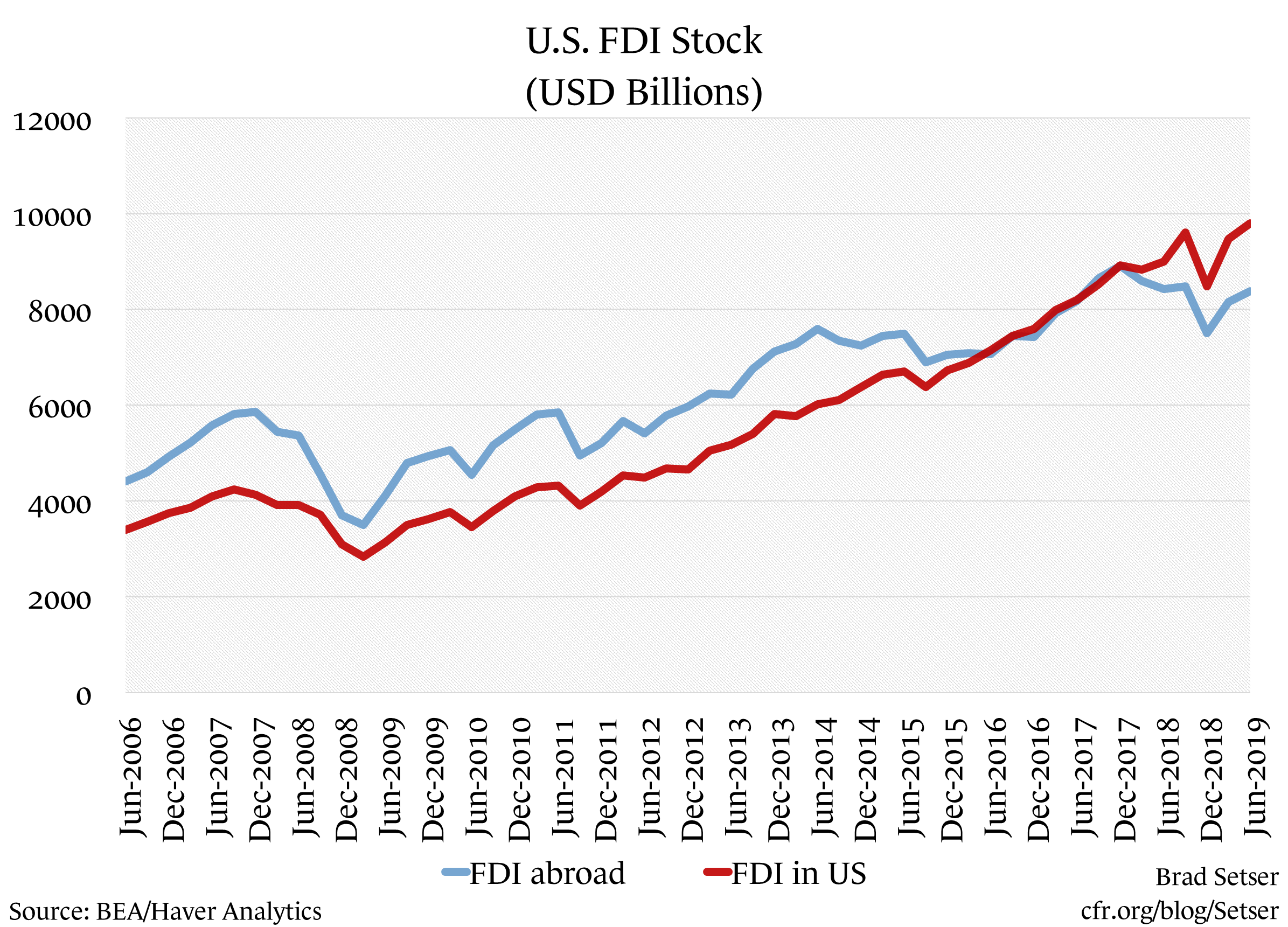

First, after the dollar’s appreciation in 2014, the United States no longer has, on net, an equity claim on the rest of the world. The market value of foreign direct investment in the United States now exceeds U.S. direct investment abroad.

In aggregate, the United States simply isn’t taking out debt to buy the rest of the world’s equity.

That’s also the case when you look at FDI flows as opposed to the market value—there hasn’t been a gap between cumulative FDI inflows and outflows (2018 was strange because of the deemed repatriation provisions of the Tax Cuts and Jobs Act, more on that later).

And second, the excess return that the United States earns on its direct investment abroad doesn’t come from borrowing at a low rate to buy risky equity, or even from the ability of American managers to get a higher return on their investments in France than French investors get on their investments in the United States (Americans investing in France somehow seem to earn basically nothing).

The excess return is entirely a function of the large profits U.S. firms book in the world’s corporate tax havens—the U.S. surplus stems from the large returns the United States appears to earn on its investments in Ireland, the Netherlands, and Bermuda. Basically, it looks to be a function of the United States’ willingness to tolerate a world where American tech and pharma companies’ offshore earnings aren’t really taxed by the United States at anything like the rate onshore profits are taxed at. Previously those profits were tax deferred, now they are largely taxed at the low GILTI rate of 10.5 percent.

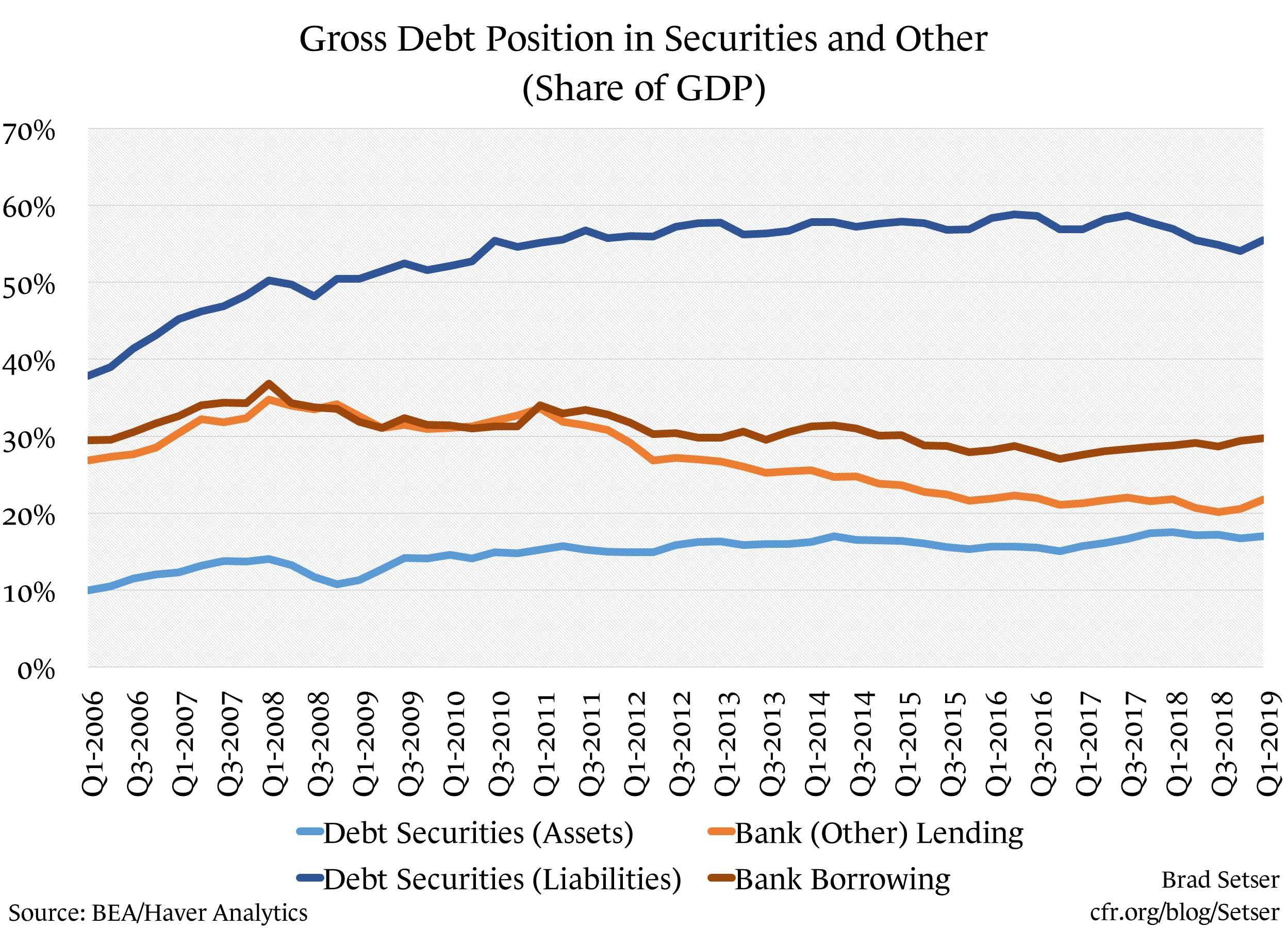

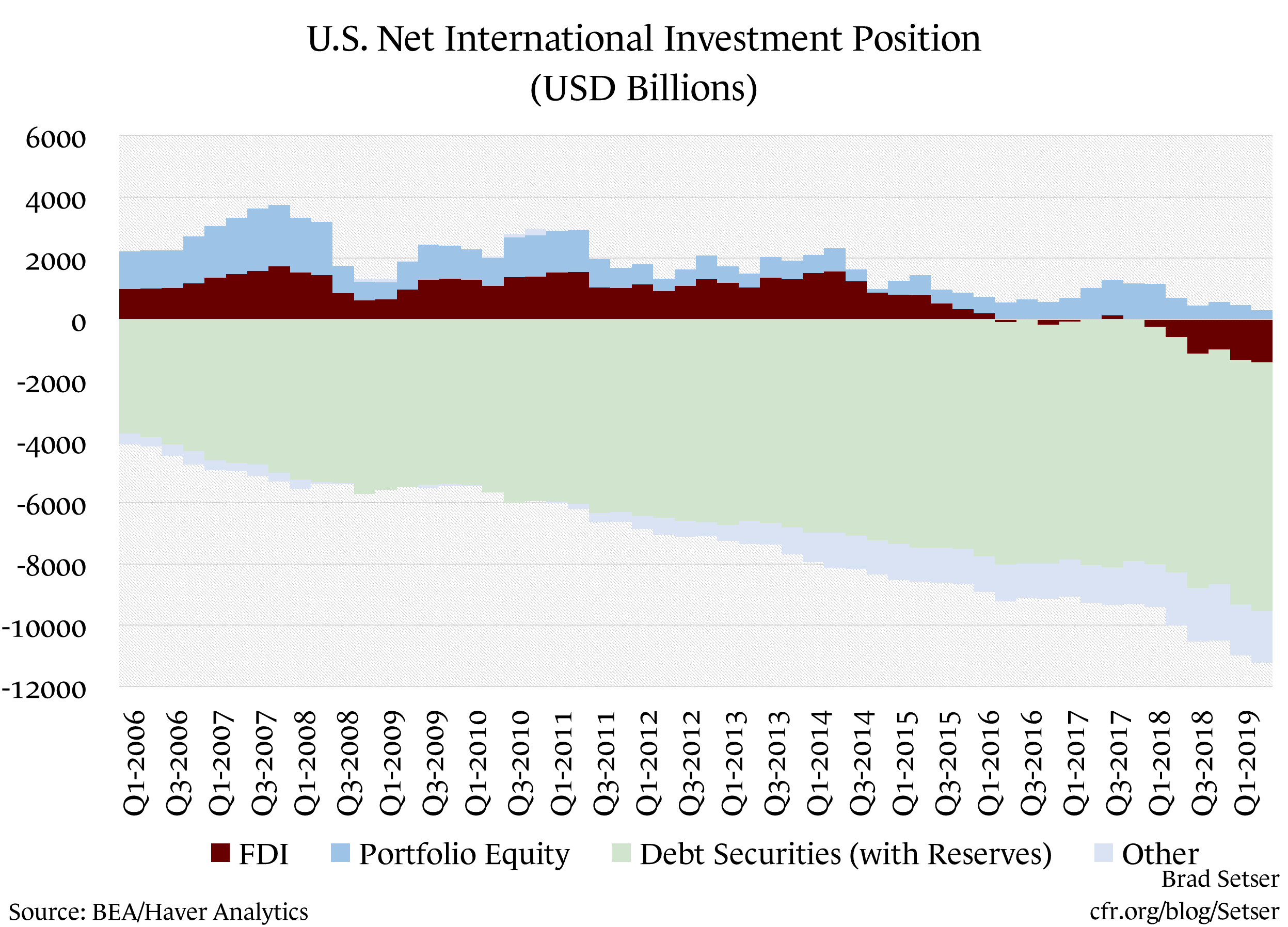

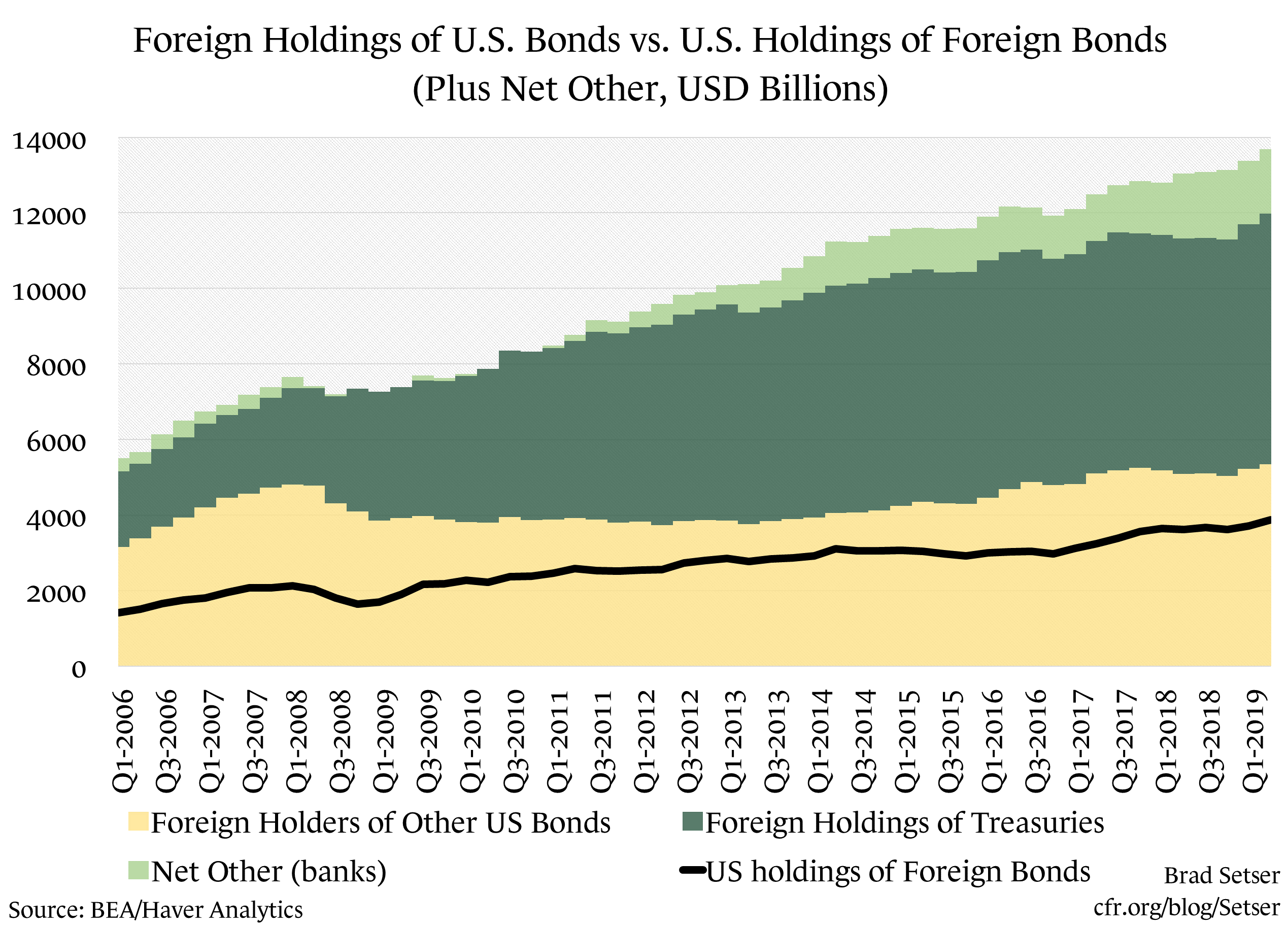

Take a look at the United States stylized external balance sheet. The United States has taken in a lot of deposits and short-term loans from the world. And it has sold an awful lot of bonds, especially Treasury bonds, to the world. Total debt related liabilities are around 90 percent of U.S. GDP. On the asset side, the U.S. has some deposits and short-term loans to the rest of the world (U.S. money market funds lending to Japanese banks, for example). And some corporate debt (largely the dollar denominated bonds firms have issued offshore—the U.S. has bought a lot of bonds issued by entities in the Caribbean). But the United States’ financial assets don’t come close to covering the United States debt liabilities.

No self-respecting bank regulator would let a bank operate with this kind of financial hole. It would be a bit much even for the regulators of Taiwan’s life insurers (who do let the insurers hold very few Taiwan dollar assets against their Taiwan dollar liabilities, and relatively little equity). For clarity, I netted out the equity book, so what shows up is the net claim—e.g. U.S. portfolio equity investment abroad in excess of foreign holdings of U.S. stocks.

Rather than a bank, the United States is basically a borrower—one who can borrow at a very low rate.

As the netting exercise below makes clear, the United States has sold a lot more government debt to the rest of the world than the U.S. government holds in its reserves—that in a sense is the United States real exorbitant privilege: it can fund itself from the rest of the world, with relatively short-term paper, without having to hold a lot of (negative yielding) euros or yen or gold to assure America’s creditors that they will be repaid.

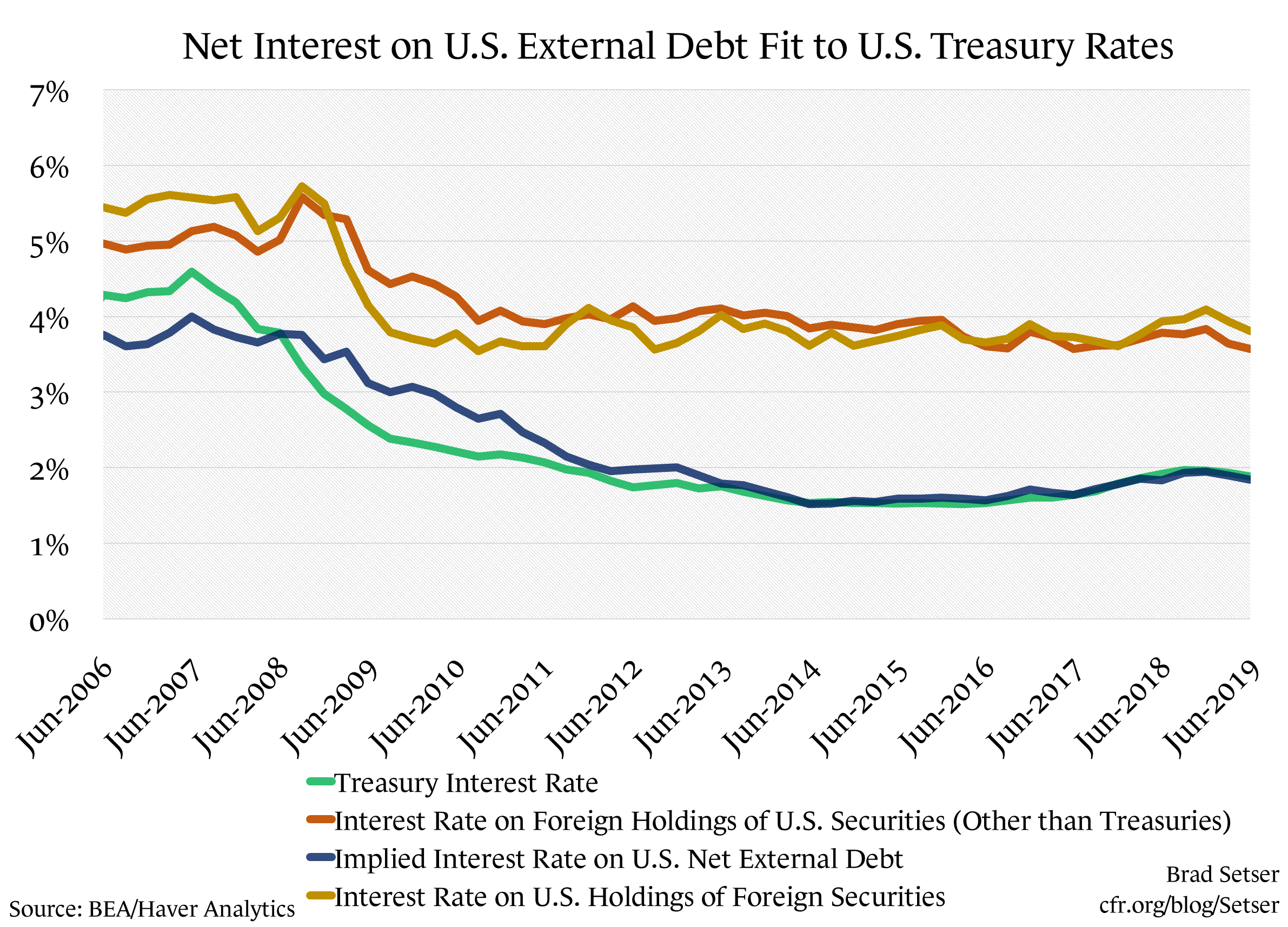

The United States these days doesn’t actually borrow at an unusually cheap rate. Listen to President Trump, who regularly complains that the Fed has kept U.S. rates well above those in Germany. It also pays more than Japan, Taiwan, France, the Netherlands, Australia, Sweden, Spain, and no doubt others.

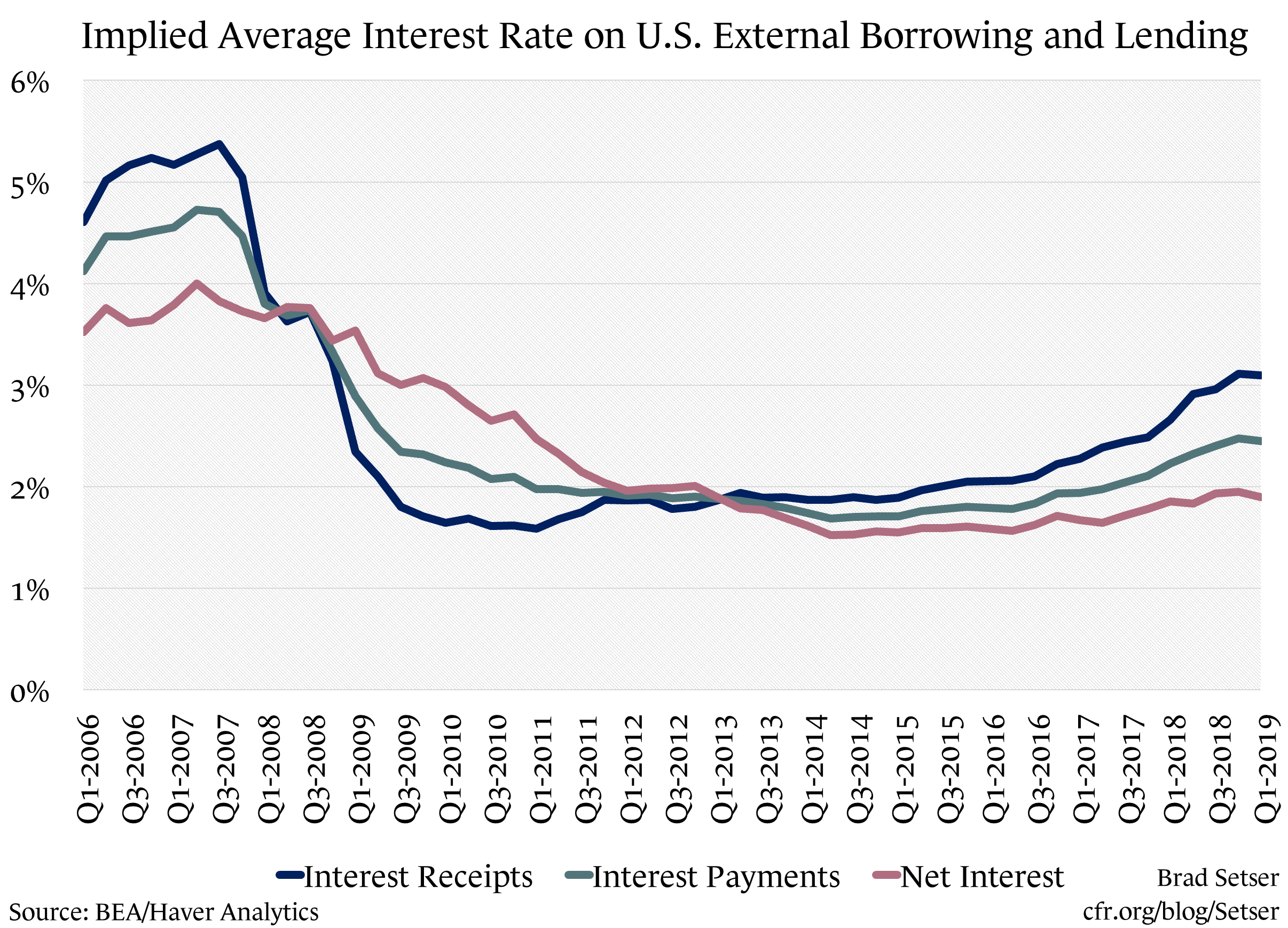

The net interest the U.S. pays the world on all of its debt actually tracks the interest the U.S. pays the world on their Treasury holdings remarkably closely (as it should given that the net debt claim on the U.S. is largely a net claim on the Treasury department, and U.S. holdings of foreign debt are largely dollar denominated corporate bonds which pay about the same as foreign holdings of U.S. corporate bonds).

And that highlights one thing I have gotten wrong over the past few years: I thought Trump’s tax cuts and the widening of the fiscal deficit would push up the interest cost of the United States‘ external debt, and that in turn would contribute to the widening of the U.S. current account deficit.

It hasn’t happened. The interest rate the United States pays on its net debt to the rest of the world is actually now falling again—as lower interest payments on the world’s holdings of Treasuries outweighs any portfolio shift on the part of U.S. creditors toward higher yielding U.S. corporate bonds.

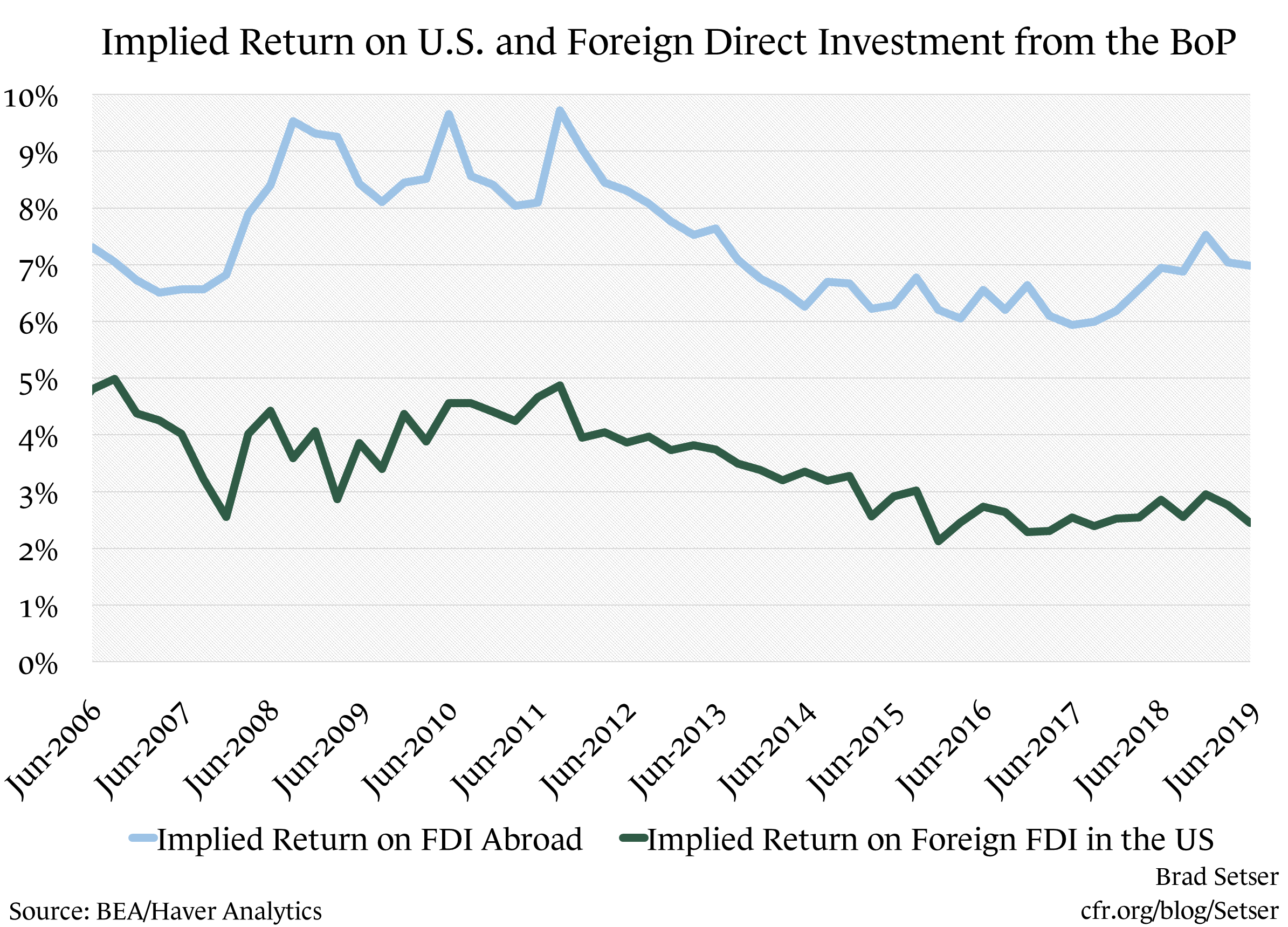

I got one other small thing wrong—but it is an interesting error. The excess return on U.S. foreign direct investment abroad has been rising over the past couple of years, even as the stock of U.S. direct investment abroad has been falling.

There is a very technical reason for this. The cash holdings of U.S. technology and pharma companies in their offshore subsidiaries technically were counted as U.S. foreign direct investment (the United States had an equity claim on the sub, and the sub had as its assets the rights to use the firms intellectual property outside the United States and its offshore cash). So when the subsidiaries of U.S. firms in Bermuda, the Netherlands, and Ireland paid $500 billion in dividends back to the United States in 2018 and ran down their cash balances by something like $300 billion, they effectively got rid of the low-return portion of their investment abroad—and what was left was all the valuable intellectual property that had been tax-shifted to a low tax jurisdiction.

Basically, the same profit on a smaller stock of investment, so a higher implied rate of return.

At the end of the day, perhaps, the equity side of the U.S. external balance sheet should be understood not by thinking of the U.S. as a giant and very successful private equity fund that borrows to buy equity—but rather as one giant corporate tax dodge for U.S. based multinationals…

If you think I am exaggerating, I would encourage you to take a look at the IRS data on the location of U.S. corporate profits—and the location of the taxes that American firms pay abroad. U.S. firms are earning big profits in jurisdictions where they don’t pay tax, and small profits in jurisdictions where they do…and by shifting what should be U.S. income to low-tax jurisdictions, reducing their U.S. tax bill as well. That’s real exorbitant privilege.