It Is Time To Scrap the IMF’s Reserve Adequacy Metric

The IMF reserve metric isn’t working: it is failing to differentiate between obviously under-reserved countries like Turkey and Argentina and adequately reserved countries like China.

Balance of payments surveillance is at the center of the IMF’s mission.

Or at least it should be, given the IMF’s mandate.

Assessing a country’s reserves is essential to evaluating a country’s overall external position. Too few reserves put a country’s economy and finances at risk. Too many reserves often imply that a country is artificially holding its currency down and trying to rely on the rest of the world’s demand, rather than taking action, to support its own demand.

Argentina, for example, clearly has too few reserves. Turkey obviously could benefit from a few more (non-borrowed) reserves too.

Taiwan, by contrast, obviously has too many reserves—and so too does Singapore.*

Unfortunately, the IMF’s reserve metric, a composite indicator of reserve adequacy, generally does not help the IMF identify either countries with too few reserves or countries with too many.

It never worked well. And it really isn’t working well right now. That is why, in my view, the current metric needs to be junked and replaced with a brand-new design.

A bit harsh, I know.

But, well, it is hard to think the IMF’s metric has any real use when the IMF, in its flagship external sector report on the balance of payments this summer, said that China and Turkey were equally under-reserved. That is a bit like waving a red flag in front of a bull—it almost seems designed to generate a bit of a reaction.

Turkey of course now has essentially no foreign exchange reserves (net reserves are negative). It also has large external debts and a current account deficit.

China by contrast has over $3 trillion in reserves. That sum still towers over China’s less than $1.3 trillion in external foreign currency debts. And China is now running a substantial trade and current account surplus.

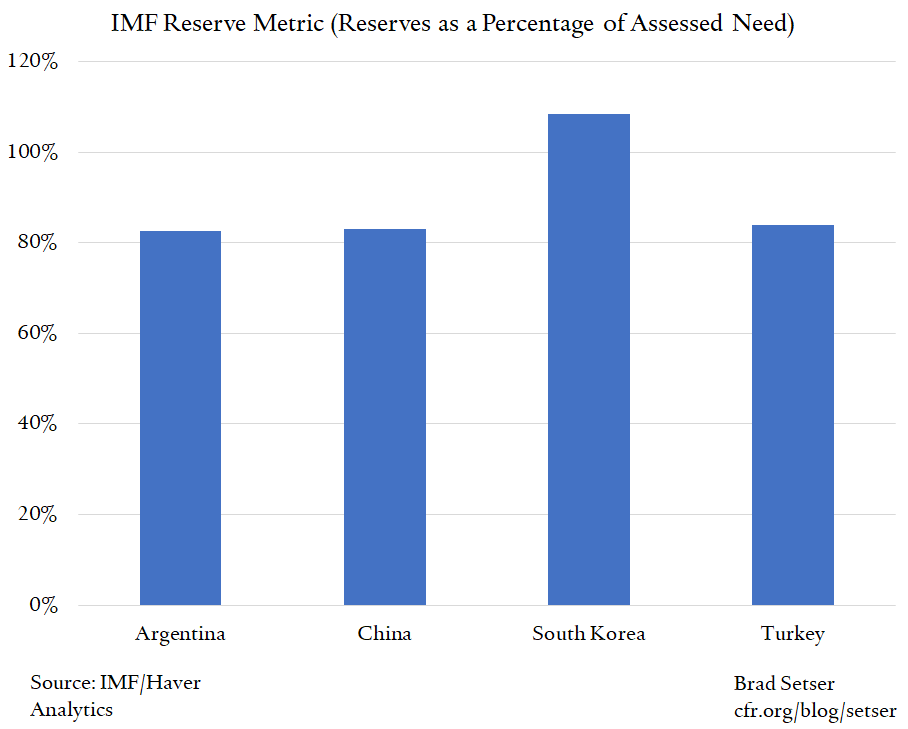

Yet Turkey scored ever so slightly better than China on the reserve metric.

Turkey was at 85 percent of the IMF metric: “Gross reserves increased to 85 percent of the IMF’s ARA metric at end-2019, from 74 percent at end-2018, but dipped to 67 percent in mid-May 2020. Similarly, reserve coverage of external financing requirements rose to 64 percent in 2019, from 46 percent the year prior, and then dropped to 49 percent in mid-May.” [p. 91]

China was at 82 percent of the IMF’s reserve metric: “The level of reserves—at 82 percent of the IMF’s standard composite metric at end-2019 (89 percent in 2018) and 133 percent of the metric adjusted for capital controls (143 percent in 2018)—is assessed to be adequate “ [p. 69].

The IMF will of course point to the qualifications that they added to their assessment of both countries reserves.

But a lot of investment banks missed those qualifications and put out reports also saying that China and Turkey are equally under-reserved.

More importantly, the basic result of the IMF’s unadjusted metric—that Turkey was less under-reserved at the end of 2019 than China—highlights the systemic problems in the design of the metric, problems that go much deeper than the IMF’s use of gross rather than net reserves for Turkey.

Let me explain.

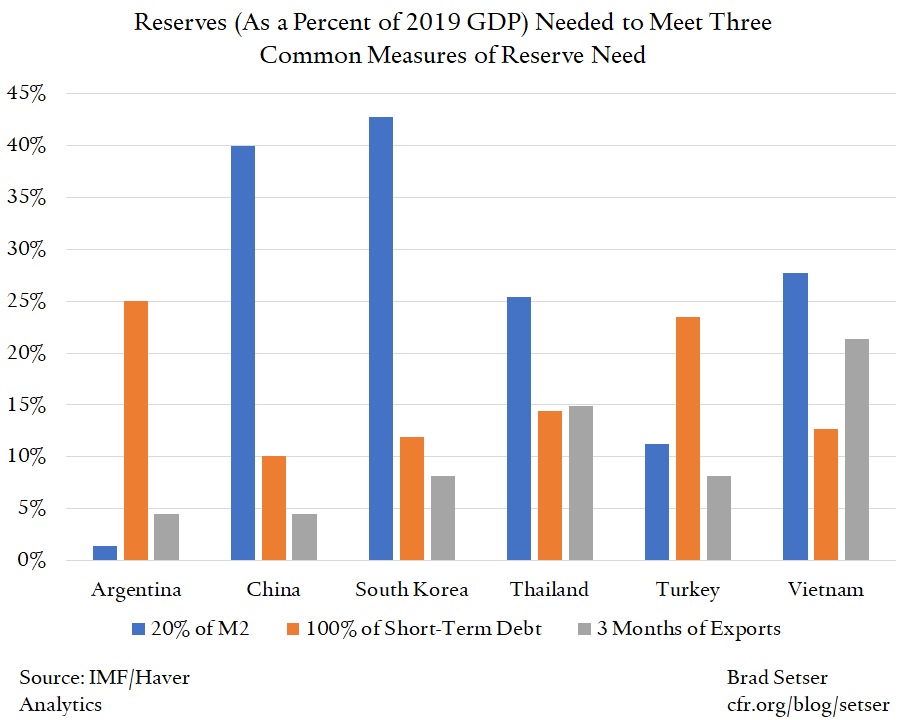

The IMF’s metric is basically a composite of three indicators: reserves to short-term debt, reserves to exports (the IMF-preferred exports to the classic imports), and reserves to broad money. A fourth variable—gross external liabilities net of short-term external debt—is added in but it doesn’t have a big impact on the composite.

Like any composite metric, it is only as strong as its components.

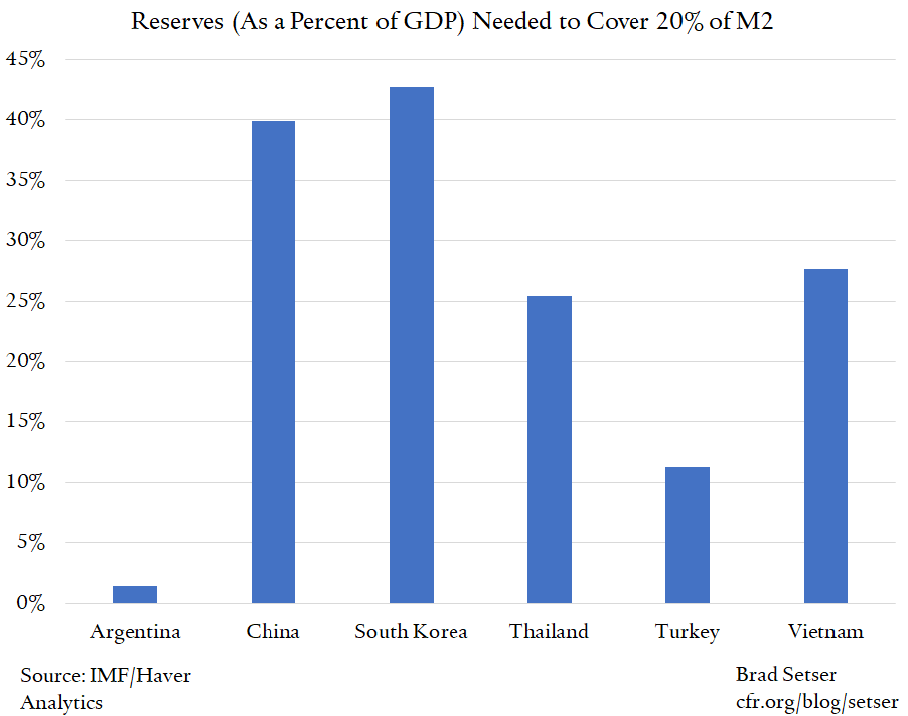

And one component—reserve to broad money—really mucks things up. As the chart below shows, there is enormous variation in the amount of reserves needed to cover broad money across key countries. Some Asian economies would need to hold 40 percent of their GDP in reserves according to this measure, while other countries like Argentina would hardly need any reserves at all.

There is another technical problem with M2 (broad money) as a measure of reserves, namely countries with high levels of broad money, or M2, tend to have a current account surplus and while countries with low levels of M2 to GDP tend to have current account deficits. So reserves to M2 systematically tends to raise the needed reserves of surplus countries and lower the needed reserves of deficit countries, which is backwards in my books. A good metric should do the opposite.

Including M2 also tends to mute the signal from short-term external debt* and from external debt more generally, as external debt (especially net external debt) is correlated with persistent current account deficits. Look at Argentina and Turkey. Both need to hold a lot more reserves if reserve need is assessed relative to short-term external debt than if reserve need is assessed relative to M2.

I would argue, and I think the experience of the 2013 taper tantrum, the 2018 rates hike, and the 2020 COVID-19 shock would support this, that the signal from short-term external debt should be amplified. Yet, an equally-weighted composite variable works the other way—it dampens the signal sent by short-term external debt. Broadly speaking, you tend to learn more by looking at the components of the IMF’s metric than by looking at the composite.

But there is also a more fundamental issue here—whether a large domestic deposit base a source of strength or a source of weakness.**

Or to put it bluntly, would you rather be China, which has a massive domestic deposit base, or Argentina, which has an itsy-bitsy domestic deposit base (Argentina’s reported reserves cover 20 percent of M2 seven times over)?

And more specifically, who should hold more reserves? Countries like China, with lots of deposits in their own currency but little external debt? Or countries like Argentina and Turkey, which have a much more limited domestic deposit base and high levels of external debt? (I actually discussed this at the Odd Lots Live variety show.)

I do not think it is a coincidence that countries with big domestic deposit bases (high levels of M2 to GDP) tend to run current account surpluses and have banking systems that are, on net, suppliers of funding to the rest of the world. Or they lend to their own central bank (buying central bank bills, or putting reserves on deposit at the central bank), which in turn is a net supplier of funding to the rest of the world.

Large quantities of domestic deposits lead to a high ratio of broad money to GDP. But a large deposit base also tends to be correlated with relatively high savings rates, and thus with countries that generally run current account surpluses.

China is the most obvious example. But there are others. Taiwan is like China in this respect (even if the life insurers have captured a large part of Taiwan’s savings surplus). So too is Korea. All are countries with relatively high levels of M2 to GDP, high national savings rates, and persistent current account surpluses.

Countries with small domestic banking systems, by contrast, tend to have trouble funding fiscal deficits domestically (Argentina is the best example) or tend to have trouble funding a big blow out in credit domestically (Turkey is a case in point) and thus tend to need access to external financing to run large fiscal deficits or sustain a big expansion in domestic credit.

Bottom line: It is not all clear to me that a large domestic banking system is actually a source of vulnerability. The real vulnerability, in my view, comes when rapid credit growth exceeds what the banking system can finance organically at home, and a country starts borrowing from the rest of the world to run a current account deficit.

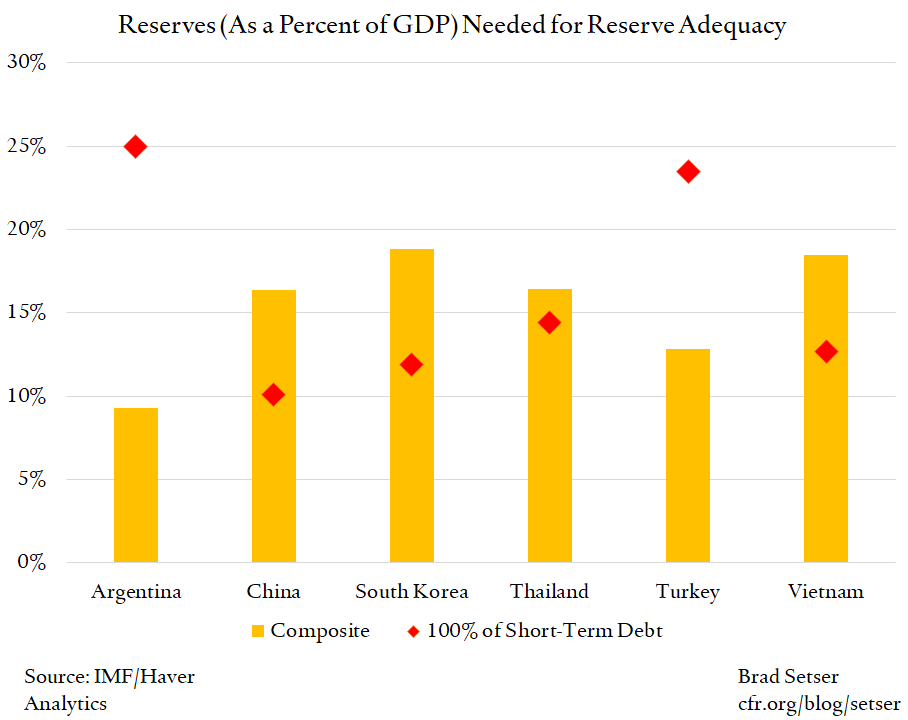

The IMF, fortunately, seems to be moving in this direction. Chapter Two of the External Sector Report focused on external assets and liabilities, and emphasized the vulnerabilities created by high levels of foreign currency denominated external debt. If “external debt is a strong predictor of external stress,” measures of reserve adequacy that focus on external debt naturally should take precedence. All, well, I was heartened that the IMF’s formal analysis used reserves versus GDP, not reserves versus its own reserve metric. Perhaps, just perhaps, there is a signal there...

*/ I have long thought the IMF’s surveillance of Singapore’s external position was rather cursory. See this thread, and my contribution to the 2018 IMF Research Department Workshop on External Imbalances.

**/ Go back and look at IMF Article IVs for Argentina, Turkey, and Ukraine over time. They generally are less under-reserved on the IMF’s reserve metric than they would be under a simple metric based on short-term debt to reserves.

***/ A high level of M2 to GDP means a large domestic deposit base, as M2 is sight plus time deposits. Of course, this gets mucked up if there are large institutions—like U.S. money market funds—that offer financial products that look a lot like deposits but aren’t called deposits. No measure is perfect.