Greenberg Center for Geoeconomics

The Greenberg Center for Geoeconomics examines how economic and geopolitical forces interact to shape the world. Sign up for our newsletter Geoeconomics Dispatch.

The work of the Geoeconomics Center is generously supported by the Amy Falls and Hartley Rogers Foundation.

article

The Age of Economic Warfare

Economic warfare has gone global, and the post-1990s economic order, built for an age of efficiency rather than rivalry, is fragmenting. Three futures are possible: managed globalization, competing blocs, or pure transactionalism.

By Edward Fishman

By Inu Manak and Allison J. Smith

By Edward Fishman

Five CFR experts weigh in on the effects of Trump’s Liberation Day on American consumers, businesses, and credibility, and the uncertainty that lays ahead for the global economy and supply chains.

By Inu Manak, Edward Alden, Benn Steil, Michael Werz and Allison J. Smith

Six CFR fellows assess the geoeconomic fallout of the war in Iran, and they analyze the challenges that the United States and the world will have to navigate as the conflict enters its third week.

By Edward Fishman, Brad W. Setser, Michael Werz, Chris McGuire, Roger W. Ferguson Jr. and Rebecca Patterson

The United States cannot out-mine and out-process China. Instead, it should leapfrog China’s dominance by scaling disruptive innovation, recovery, and recycling.

1/0

Core Questions

The Greenberg Center will address four foundational questions about how the United States should navigate a changing geoeconomic landscape.

- How can we deploy economic power without eroding its foundations?

- How can we safeguard economic security without undermining growth and prosperity?

- How can we secure leadership in the technologies and industries that will define the future?

- How is the global economic order changing—and what kind of order should we seek to build?

Research

The Broken Economic Order

By Heidi E. Crebo-Rediker

America’s rupture with allies, institutions, and global economic norms has left the next U.S. president an international economic system that bears little resemblance to the one that preceded it. The task at hand is not restoration but reinvention.

Macron’s Agenda Meets Trump’s at the G7 Summit

By Heidi E. Crebo-Rediker

Time to Stop Forecasting China’s Surplus Away

By Brad W. Setser

The Protectionist Turn

By Benn Steil

The Illusion of Reciprocity | Foreign Affairs

By Inu Manak and Allison J. Smith

What Is the Future of U.S.-Mexico-Canada Trade?

By Michael Froman

The U.S. Economy Was Shaky Before the Iran War. Now It's in Real Trouble.

By Roger W. Ferguson Jr. and Maximilian Hippold

Events

Meeting

Meeting

In the News

Featuring Edward Fishman

Featuring Edward Fishman

Featuring Edward Alden

Featuring Joshua Kurlantzick

Featuring Sebastian Mallaby

Featuring Sebastian Mallaby

Featuring Sebastian Mallaby

Featuring Edward Fishman

Featuring David M. Hart

Featuring Jonathan E. Hillman

Featuring Edward Fishman

Program Experts

Edward Fishman

Senior Fellow and Director of the Maurice R. Greenberg Center for Geoeconomics

Edward Alden

Senior Fellow

Thomas J. Bollyky

Bloomberg Chair in Global Health; Senior Fellow for International Economics, Law, and Development; and Director of the Global Health Program

Heidi E. Crebo-Rediker

Senior Fellow

James P. Dougherty

Adjunct Senior Fellow for Business and Foreign Policy

Roger W. Ferguson Jr.

Steven A. Tananbaum Distinguished Fellow for International Economics

William Henagan

Research Fellow

Alice C. Hill

David M. Rubenstein Senior Fellow for Energy and the Environment

Jennifer Hillman

Senior Fellow for Trade and International Political Economy

Jonathan E. Hillman

Senior Fellow for Geoeconomics

Kenneth I. Juster

Distinguished Fellow

David Lipton

Senior Fellow for Geoeconomics

Zongyuan Zoe Liu

Maurice R. Greenberg Senior Fellow for China Studies

Sebastian Mallaby

Paul A. Volcker Senior Fellow for International Economics

Inu Manak

Senior Fellow for International Trade

Shannon K. O'Neil

Senior Vice President of Studies and Maurice R. Greenberg Chair

Rebecca Patterson

Senior Fellow

Gina M. Raimondo

Distinguished Fellow

Kenneth S. Rogoff

Senior Fellow for Economics

Brad W. Setser

Whitney Shepardson Senior Fellow

A. Michael Spence

Distinguished Visiting Fellow

Benn Steil

Senior Fellow and Director of International Economics

Laura Taylor-Kale

Senior Fellow for Geoeconomics and Defense

Archive

1587 results

Featuring Edward Fishman

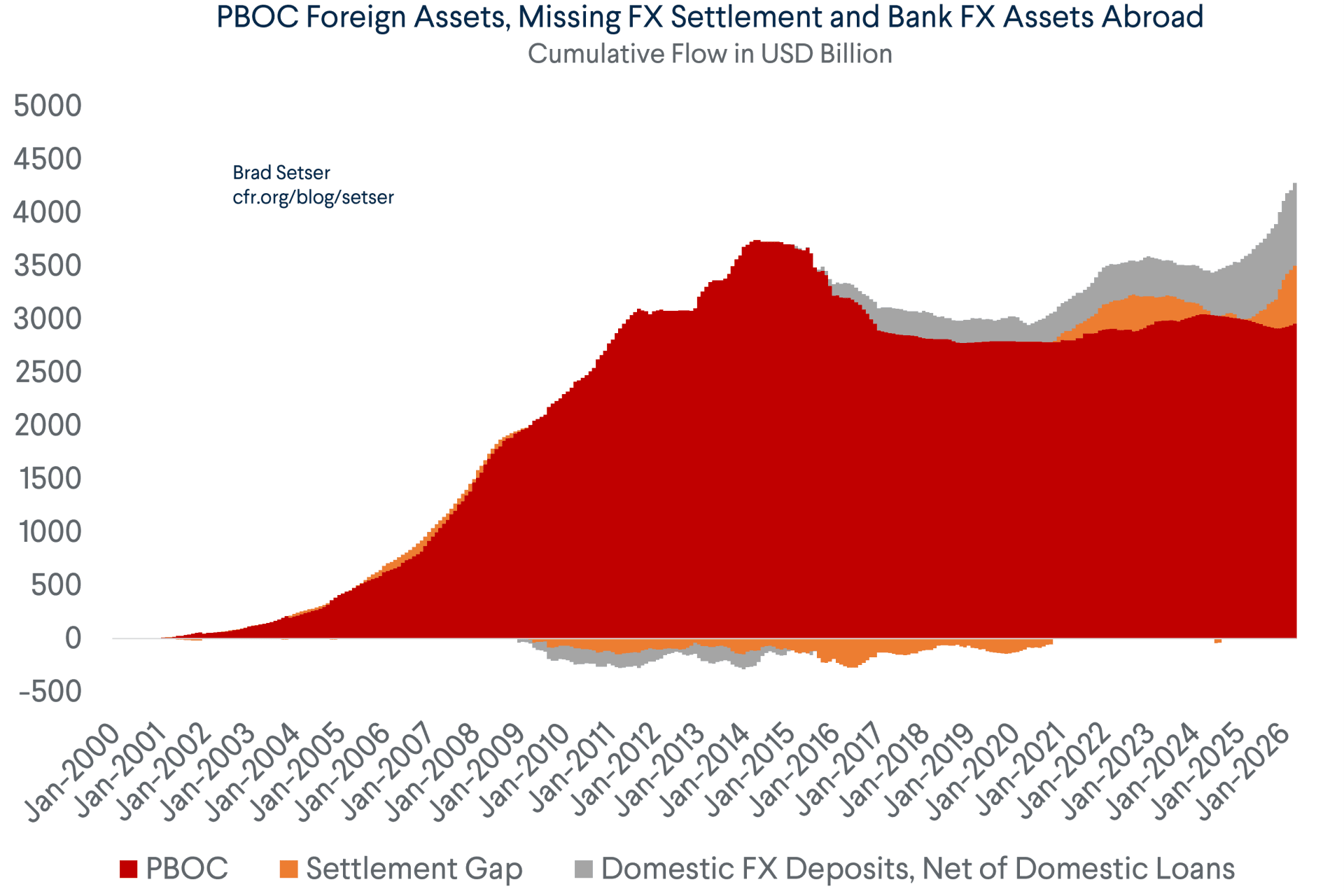

Featuring Edward Fishman By Brad W. Setser

By Brad W. Setser Featuring Edward Fishman

Featuring Edward Fishman Featuring Heidi E. Crebo-Rediker

Featuring Heidi E. Crebo-Rediker Featuring Heidi E. Crebo-Rediker

Featuring Heidi E. Crebo-Rediker Featuring Heidi E. Crebo-Rediker

Featuring Heidi E. Crebo-Rediker Featuring Heidi E. Crebo-Rediker

Featuring Heidi E. Crebo-Rediker By Benn Steil and Yuma Schuster

By Benn Steil and Yuma Schuster- Featuring Edward Fishman

Featuring Edward Fishman

Featuring Edward Fishman- Featuring Edward Fishman

By Brad W. Setser

By Brad W. Setser Featuring Edward Fishman

Featuring Edward Fishman- Featuring Edward Alden

Featuring Edward Fishman

Featuring Edward Fishman By Jonathan E. Hillman and Ishaan Thakker

By Jonathan E. Hillman and Ishaan Thakker Featuring Edward Fishman

Featuring Edward Fishman By Rebecca Patterson

By Rebecca Patterson Featuring Heidi E. Crebo-Rediker

Featuring Heidi E. Crebo-Rediker By Brad W. Setser

By Brad W. Setser By Benn Steil and Yuma Schuster

By Benn Steil and Yuma Schuster