How Will the U.S. Fund its Twin Deficits?

Will there be a mismatch between what the U.S. wants to sell (Treasuries) and what the world wants to buy?

In the past few years, the U.S. Treasury has needed to, on net, raise about three percent of U.S. GDP from the market to fund the budget deficit. A portion of the deficit has been funded with short-term debt, so funding deficits of that size have required roughly 2 percent of GDP per year in (net) issuance of Treasury bonds and notes.

The U.S., as a whole, has needed to sell just under 3 percent of GDP in debt to fund ongoing trade and current account deficits. The external deficit could be financed by selling off equity, but, by and large, it hasn’t been—U.S. purchases of foreign equity and foreign purchases of U.S. equity have tended to largely offset, so the bulk of the current account deficit has been financed through the sale of bonds to the world (I did a big post on this).

The simplest equilibrium would have been one where the rest of the world purchases U.S. Treasuries—simultaneously funding both the budget deficit and the external deficit.

That, though, clearly hasn’t been the actual equilibrium.

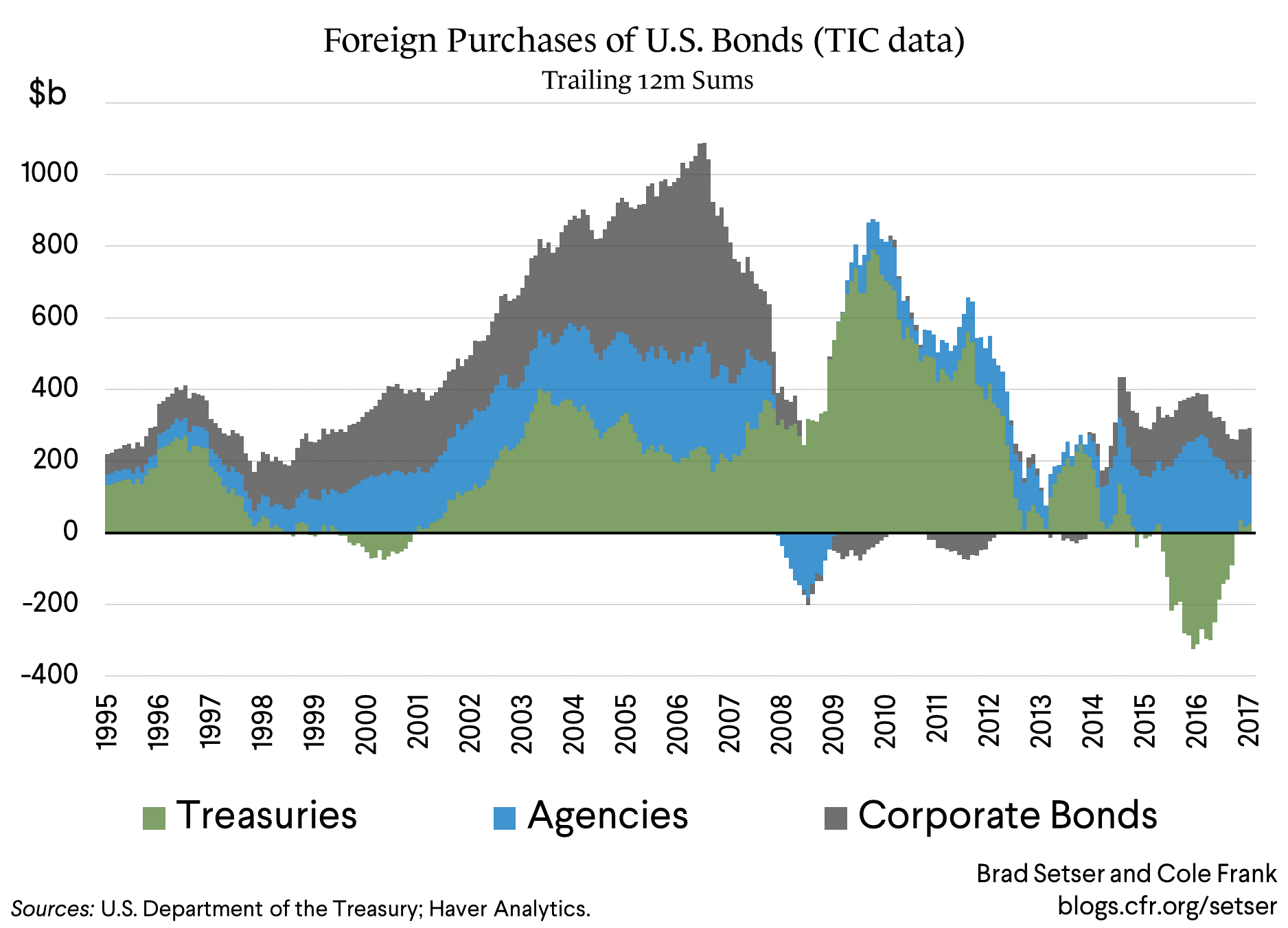

Foreign investors have been buying Agencies and corporate bonds.

That means that American investors have been the ones funding the U.S. government over the last few years: presumably split between banks for high-quality and liquid bonds to meet regulatory requirements, pension funds looking to match long-term liabilities, and, perhaps, risk parity funds that need more bonds as the value of their equities rises, and so on.

Consider a plot of foreign demand for U.S. bonds. There hasn’t been much of a flow into Treasuries. Since 2014 the inflow has been into Agencies and corporate bonds.*

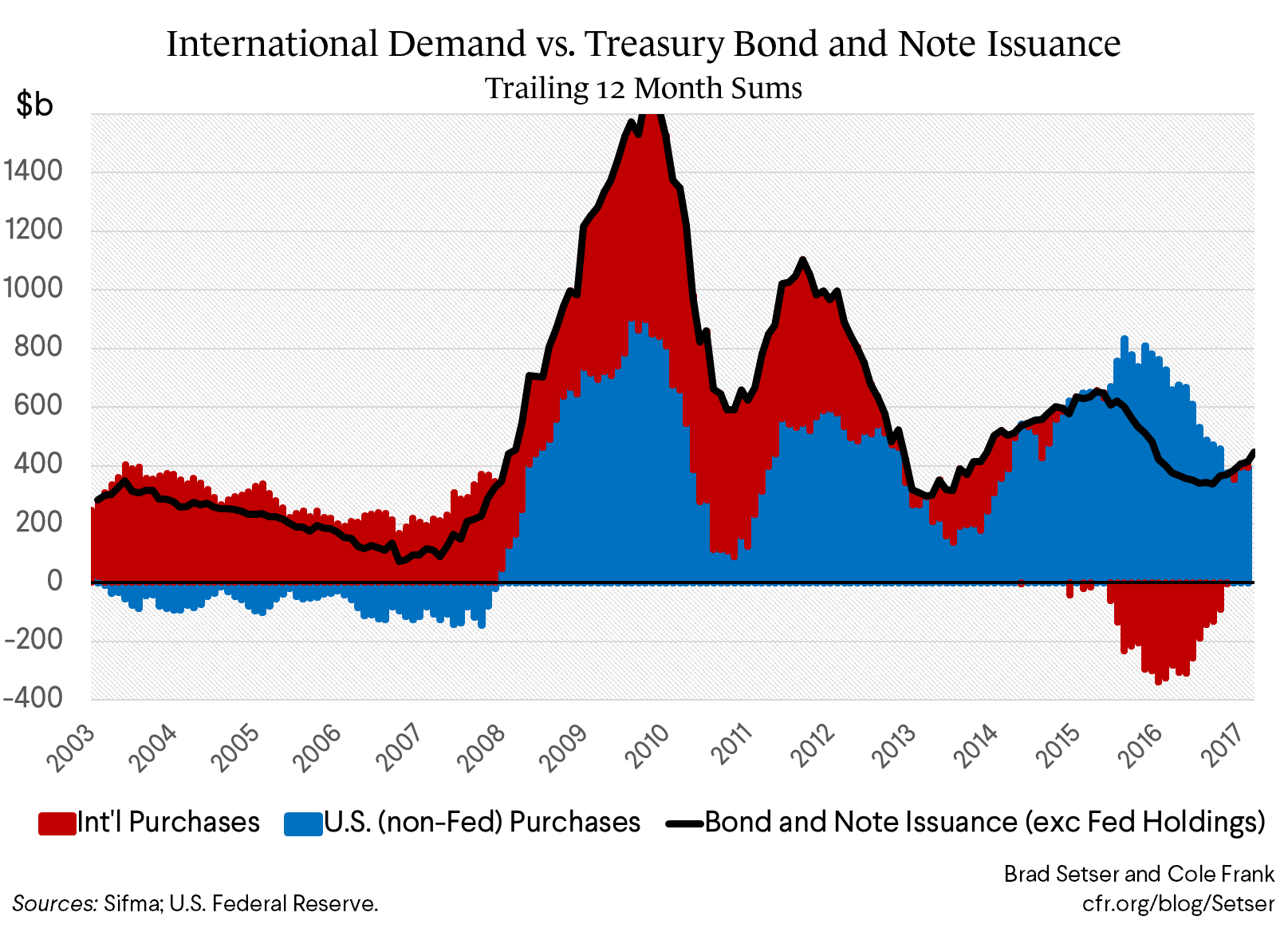

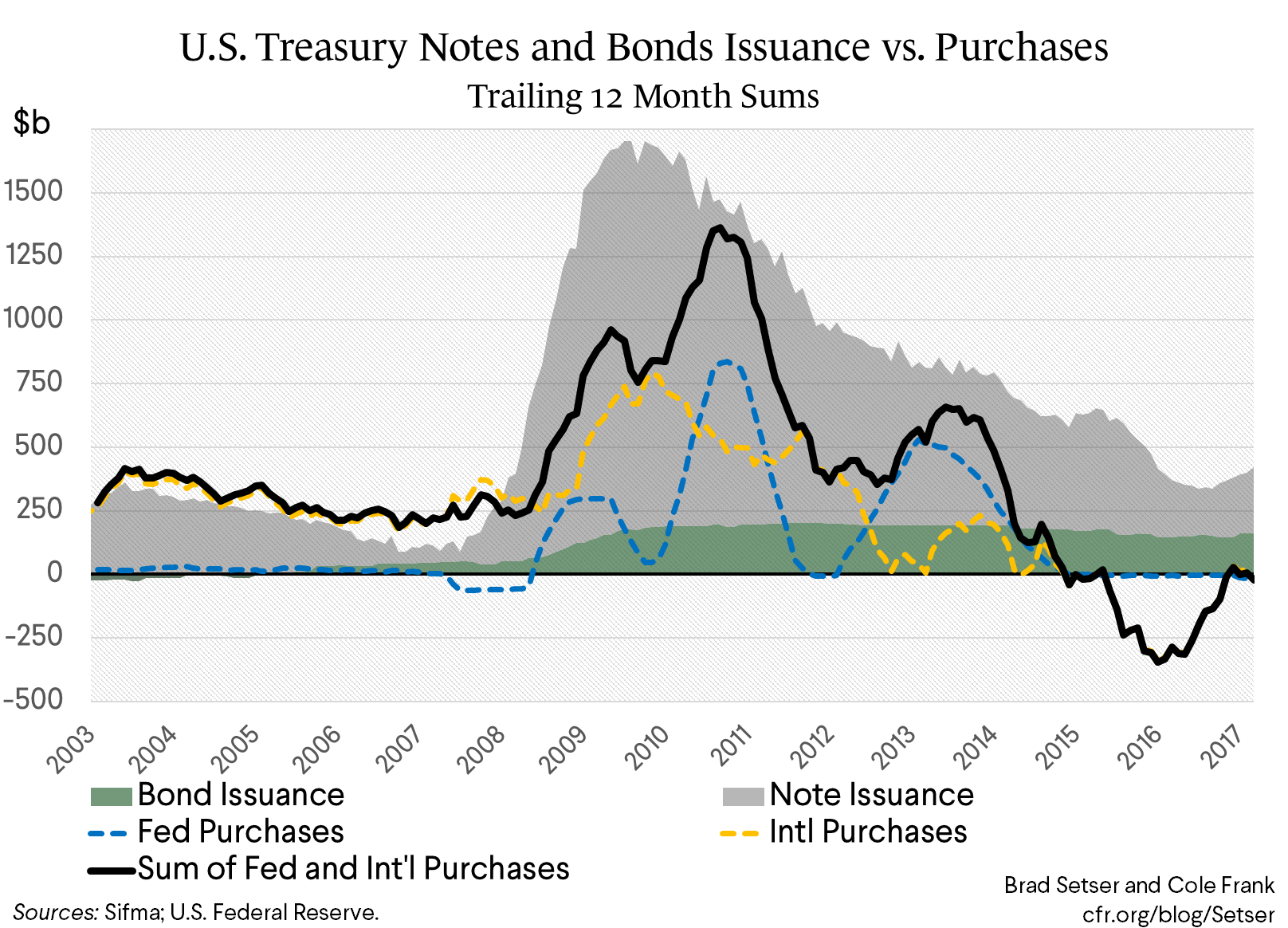

A plot of foreign inflows into Treasuries against net issuance of bonds and notes (net of Fed purchases) clearly shows the shift toward domestic buyers in the last few years (bills have been excluded from both categories).

The world today consequently looks very different than the world of 2003 to 2007, when foreign demand for Treasuries by and large exceeded net issuance (American investors were selling Treasuries to the world and investing in riskier assets that offered a bit more yield for much less safety, creating the foundation for the financial crisis). And different from 2009 to 2013—when foreign investors and the Fed snapped up much of the net supply of Treasuries associated with ongoing U.S. fiscal deficits.

I started by looking back, not by looking forward. But obviously the question of who is going to buy all the bonds the Treasury will issue has gained additional prominence recently.

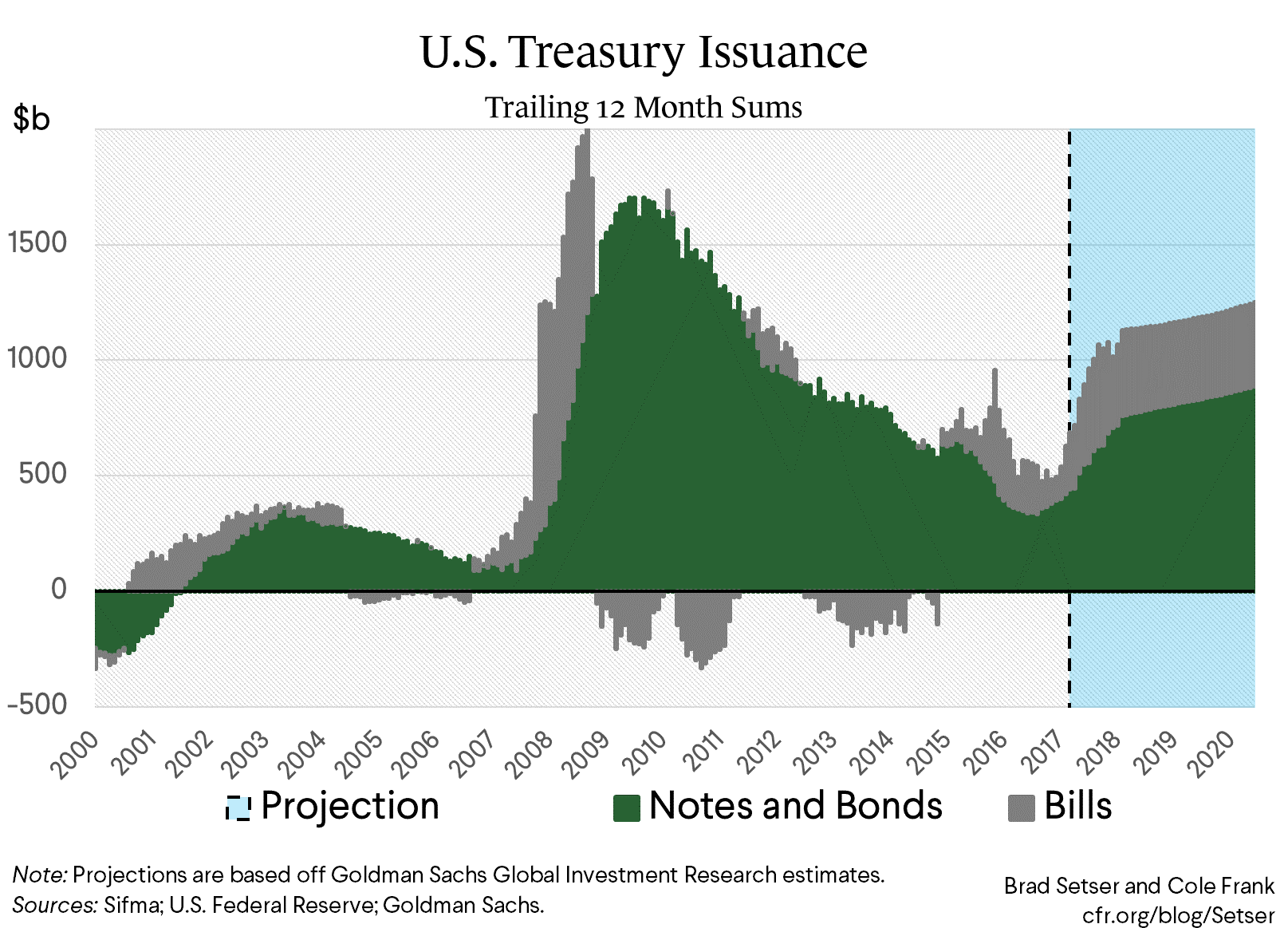

The fiscal deficit is rising toward 5.5 percent or so of GDP, which implies that the Treasury will need to sell about 4 percent of GDP of bonds (on net) a year—not the roughly 2 percent of GDP it now sells. These numbers assume—based on some work that Goldman Sachs has done—that increased bill issuance can cover around 1.5 percentage points of GDP of the annual funding need, so “note” and “bond” issuance will lag the headline fiscal deficit.

On the other hand, the Fed will be cutting back its Treasury portfolio at an annualized pace of $90 billion a quarter, or a bit under 2 percent of GDP, once the roll-off is fully phased in. The market consequently will likely need to absorb over 5 percent of GDP of longer-dated Treasury issuance—a real step up from the current level.

The trade deficit and broader current account deficit is also likely to rise—probably by more than half a point (and possibly by a full point)—along with the fiscal deficit. In part because the interest bill on the United States’ external debt is going to go up with rising short-term rates and a growing term premium. And in part because—even with Trump’s turn toward protectionism—the trade deficit is also likely to go up.

As Neil Irwin has emphasized, the steel and aluminum tariffs would affect only a small fraction of U.S. imports, and by raising the cost of an input into other goods, any fall in imports of basic metals would be partially offset by falling exports of final goods (Martin Wolf nails this dynamic). Plus, well, the trade deficit jumped a lot in the fourth quarter, and then jumped up a bit more in January. Rising import demand from the guns-and-tax-cuts-late-cycle fiscal stimulus look poised to offset any pickup in exports from a weaker dollar.

It isn’t difficult, in my view, to understand why foreign demand has tilted away from Treasuries in the past few years. Private investors abroad haven’t been big buyers of Treasuries over the last twenty or so years. When reserve growth stopped as the dollar appreciated in the 2014, the U.S. lost the traditional source of incremental foreign demand for Treasuries.

And while reserves are trending up again, they aren’t growing at their previous pace—in part because countries like Korea and Taiwan have channeled foreign asset accumulation into their insurers and pension funds. They have been clever in finding policies that help keep their current account surpluses up while avoiding the kind of rapid reserve growth that would invite a formal Treasury designation of manipulation.

So what will give?

I can imagine three possible flow equilibria:

- Central banks return to buying large quantities of reserves, and those reserves are funneled into the Treasury market. That probably would require that the U.S. Treasury soften its criteria for determining manipulation, or for a host of countries to conclude that there is little to fear from designation.** Central bank purchases tend to rise when the dollar is falling versus the floating currencies (e.g. there is a shortfall in private demand for U.S. assets that surplus countries make up).*** Indeed, there are some signs this is what happened in the first quarter—there was a strong rise in the Fed’s custodial holdings of Treasuries in February.

- Higher rates induce private investors globally to buy more Treasuries (perhaps in conjunction with a weaker dollar, but this is not a necessary condition). The ECB and BoJ are still holding their policy rate below zero, so the higher U.S. rates go, the bigger the yield pickup. Even now the unhedged yield on long-term U.S. bonds is much higher than the yield offered by JGBs or the Eurozone’s existing safe assets—and somewhat above the yield on Korean and Taiwanese government bonds, which are also in short supply thanks to their home countries’ tight fiscal policies.

- Private investors abroad will continue to buy U.S. corporate bonds and start becoming net buyers of U.S. equities rather than Treasuries, and as the price of these assets rises relative to the price of Treasuries, Americans will conclude Treasuries are a comparative bargain and snap up the full increase in supply.

Or I guess, the Treasury could really shorten the maturity of its portfolio and issue a ton of bills rather than notes (offsetting the reduced supply of zero duration reserves associated with the Fed’s balance sheet reduction, see Jason Cummins in the Financial Times) and thus try to limit the increase in supply of bonds and notes.

Take your pick.

*/ The detailed TIC data also shows that much of this has gone into unsecured corporate bonds, not into asset backed securities (private label asset backed securities fall into the broad “corporate” category).

**/ The U.S. considers intervention by a current account surplus country of more than 2 percent of GDP to be excessive. It also gives countries a free pass on interest income, which will soon matter for places that hold a lot of reserves relative to GDP. Cough, Taiwan.

***/ And current account deficit countries like India that are receiving large inflows and do not want an larger deficit—their central banks effectively turn private demand for Indian assets into global demand for U.S. Treasuries (at a price, though, as the “carry” for the Reserve Bank of India is negative). They though might prefer tighter inflow controls to more reserves.